Author: Mario S.

Translated by: Deep Tide TechFlow

Deep Tide Guide: Circle's largest single-day drop since its IPO, falling 20%, is not just a coincidence but the result of a triple hit from regulation, vulnerability in business models, and frozen assets on-chain.

This analysis clearly explains Circle's 95.5% reliance on interest income from reserves and why the damage from this bill is far deeper than it appears on the surface.

The full text is as follows:

On Tuesday, CRCL plummeted 20% in a single day, marking the largest intraday decline since its IPO, with a market cap evaporation of $5 billion. Trading volume reached 56.4 million shares, nearly four times the 90-day average. Coinbase also declined by 11% on the same day.

The pricing of the entire stablecoin market was reset within a few hours. The trigger was a new draft of the "Clarity Act," which would effectively end passive income from stablecoins.

This is not just a story of one drop day. Behind it is a regulatory game, a flaw in the business model, and an incident of wallet freezing—three factors combined that led to the explosive reaction of an already burning stock.

The Bomb of the "Clarity Act"

On March 20, Senators Thom Tillis (Republican, North Carolina) and Angela Alsobrooks (Democrat, Maryland) announced a principled agreement on stablecoin income provisions, backed by the White House. The full text was disclosed to leaders in the crypto industry during a closed-door meeting on Capitol Hill on Monday.

The core provision: The passive income earned solely by holding dollar-pegged tokens will be explicitly prohibited. Exchanges, brokers, and their affiliates are prohibited from providing stablecoin balance income, whether directly or indirectly, or in any form that is "economically equivalent to interest."

Activity-based rewards tied to payments, transfers, or platform usage are still permitted. The SEC, CFTC, and Treasury Department will jointly define the allowed forms of rewards and anti-avoidance rules within a year. Notably, the SEC and CFTC have just announced a historic inter-agency memorandum, ending years of inter-agency disputes.

Congress has just drawn the line that the bank lobbying group has been seeking for two years in writing: stablecoins can be payment tools but cannot become substitutes for deposits.

According to an internal stakeholder email obtained by Eleanor Terrett, an industry leader who attended the closed-door meeting described the text as a "deviation" from earlier discussions with the White House. They warned that the "economic equivalence" standard is deliberately vague, and future regulators may interpret it more strictly.

The Impact on Circle is Deeper than Anyone Else

Circle currently derives 95.5% of its revenue from interest income on USDC reserves, explaining why the market reacted so violently.

CRCL issues USDC, holding reserves in short-term government bonds and overnight repurchase agreements, earning the interest spread. In Q4 2025, reserve income reached $711 million, a 60% year-over-year increase driven by a 97% growth in average USDC supply. Full-year revenue for 2025 is projected to be $2.7 billion, a 64% increase year-over-year.

The "Clarity Act" does not directly attack Circle's reserve income (as CRCL earns that income itself), but it directly strikes at Circle's demand engine. Currently, platforms like Coinbase distribute stablecoin income to users as an incentive for holding USDC. Coinbase's stablecoin income is expected to reach $1.35 billion in 2025, up from $910 million in 2024. If exchanges can no longer provide returns on USDC balances, the motivation for users to hold USDC instead of traditional bank deposits will be significantly weakened.

Reduction in income sharing → Decrease in USDC adoption → Shrinking reserve sizes → Reduction in Circle's interest income.

The timing makes matters worse. As the Federal Reserve lowers interest rates, reserve yield has decreased from 4.49% in Q4 2024 to 3.81% in Q4 2025. Although the market no longer expects cuts this year, Circle's interest income was already under pressure before this bill emerged.

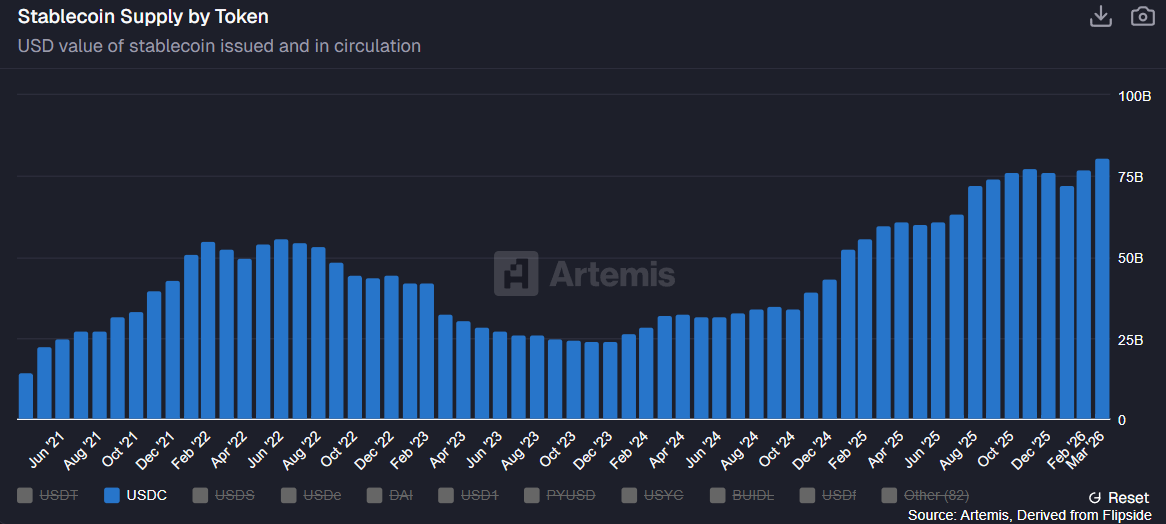

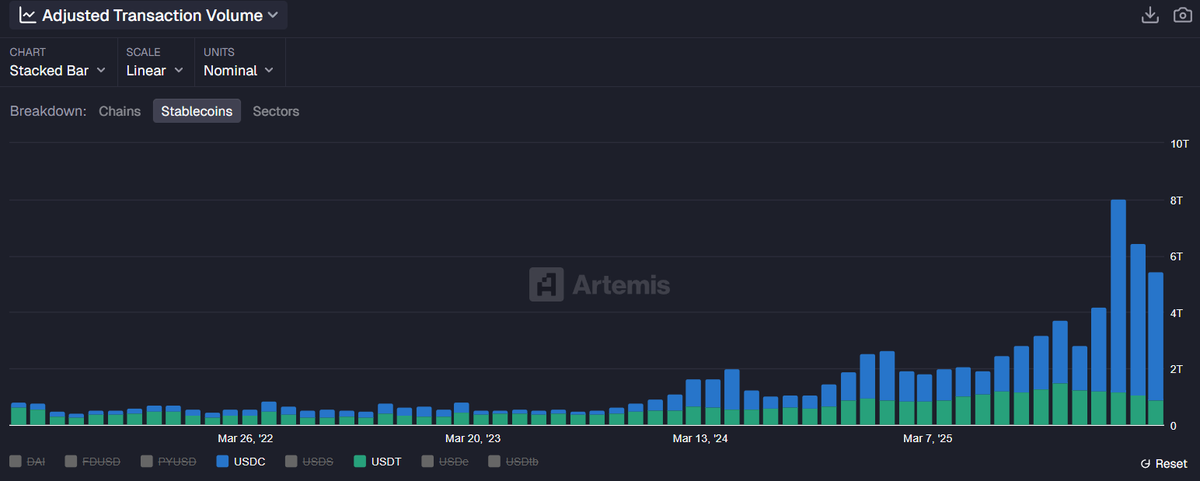

The Fundamentals of USDC Have Never Been Stronger

The stock price crash occurred on the same day that USDC's underlying metrics hit all-time highs:

Circulating supply: reached $81 billion by late March, above the $76 billion at the end of 2025.

On-chain transaction volume: reached $6.8 trillion (adjusted) in Q4 2025, more than double year-over-year.

Relative market share against USDT: USDC's trading volume has surpassed Tether's USDT since August 2025, with a market share exceeding 80% by 2026.

Q4 earnings report beat expectations: revenue of $770 million, above the expected $745 million; EPS of $0.43, exceeding market consensus by 23%.

Circle has also just announced its entry into Africa through a partnership with Sasai Fintech and has secured a significant integration with Intuit.

Wallet Freezes Add Fuel to the Fire

Late Monday night, Circle froze the USDC balances of 16 enterprise hot wallets, affecting several exchanges, casinos, and Forex platforms, including FxPro, Pepperstone, AMarkets, and HeroFX.

This freeze reportedly stemmed from a U.S. civil case whose details have not been disclosed. @zachxbt raised sharp questions, pointing out that anyone using basic on-chain tools could see these were operational wallets handling thousands of transactions. He warned of the risk of turning USDC into a "politicized censorship tool" based on opaque freezes stemming from undisclosed civil suits.

The power to freeze and even clear the balances of frozen addresses has been clearly written into USDC's smart contracts. However, on a day when the market already began questioning the risks of centralized stablecoins, this action could not look worse.

Bulls still have reason to exist

This round of selling has priced in the most pessimistic interpretation of the "Clarity Act." But on the other hand, there are several points worth noting.

Activity-based rewards remain intact. The bill draws a line between passive income (prohibited) and transaction-based incentives (allowed). Platforms like Coinbase are exploring workarounds: marketing incentives, activity-based payments, and partnerships that blur the line between interest and rewards. The "economic equivalence" standard's vagueness means lawyers will exploit loopholes.

The impact on Coinbase's income statement may be limited. Most of Coinbase's stablecoin earnings are directly passed on to users, so this revenue often corresponds with matching expenses. Analysts believe direct profit impact will be limited. The bigger issue is whether the restrictions will hinder USDC's long-term adoption.

This bill has not yet become law. Committee review is expected to wait until after the Easter recess in late April. There is still room for lobbying, amendments, and negotiations. Brian Armstrong has notably remained silent on the latest text, but his previous stance indicates that Coinbase will take a strong stance on the "economic equivalence" wording.

Non-reserve revenue is growing rapidly. Platform services, transaction processing, and other non-reserve revenues grew 15.3 times year-over-year in Q4 2025, reaching $37 million, with total other revenues for the year reaching $110 million. While still relatively small compared to interest income, the logic of revenue diversification has already been established.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。