Author: Michel Athayde

Many traders experience the same frustration: they clearly see the right direction, but end up not making money.

You predict that Bitcoin will rise, and it indeed rises, but you chase in after the breakout and are quickly washed out by a sharp pullback. You judge the market is about to change, and indeed a movement comes, but before the big volatility is truly released, the small back-and-forth fluctuations have already consumed all your position size, patience, and stop-loss space. On the surface, it seems you are losing to timing; on a deeper level, you lose due to a misjudgment of volatility.

This is precisely why many people who focus on price for a long time still struggle with trading. Price answers the question "where is the market right now", while volatility answers "how restless the market might be next". The former describes the outcome, while the latter describes the path; the former tells you the direction, while the latter informs you of the density of risk.

Thus, truly mature market participants are concerned not just with whether BTC will rise or fall, but with how the market is pricing "future volatility".

This point is especially noteworthy recently. An increasing number of platforms and institutions have begun to transform "crypto volatility" from a specialized variable hidden in options into more explicit indices and trading objects. Gate has launched BVIX and EVIX perpetual contracts, and BitMart has also introduced the corresponding BVIXUSDT and EVIXUSDT; meanwhile, Cboe announced in March 2026 the launch of BITVX based on IBIT options, which employs a methodology similar to VIX to measure the 30-day forward volatility of Bitcoin.

This indicates that the crypto market is moving from "just trading price" to "simultaneously trading price, expectations, and risks".

What exactly is volatility?

If I were to explain in a straightforward manner, volatility is a measure of how much price changes. It does not answer direction but only answers "how much it will move".

This means that even if a market has no significant rise or fall, as long as there are substantial intraday and daily oscillations, volatility can be very high. Conversely, even if a market is rising, as long as the upward movement is smooth enough, volatility may not be high.

To understand Bitcoin volatility, it is crucial to distinguish between three levels.

The first level is historical volatility. It is calculated based on past price data, measuring how much BTC has fluctuated over a certain period. It acts like a rearview mirror, telling you how bumpy the market has been in the past but does not directly represent the future. Historical volatility is suitable for review, horizontal comparison, and risk management baseline, but it is not suitable as a direct prediction of the future.

The second level is implied volatility. It is not directly calculated from past prices but is inferred from option prices to gauge market expectations of future fluctuations. The mainstream definition generally emphasizes that implied volatility reflects the market's expectations of future price movements, not the volatility that has already occurred. In other words, options are expensive not just because the market is bullish or bearish, but because the market is assigning prices to future uncertainties.

The third level is the volatility index. You can think of it as compressing the market's expectations of future volatility into a more intuitive, observable, and comparable number. In traditional finance, the VIX is the most typical example. Nowadays, Bitcoin is also gaining similar "fear gauges". Cboe's description of BITVX is based on IBIT options, using the VIX methodology to measure Bitcoin's 30-day forward volatility.

From this perspective, the truly important aspect of indicators like BVIX and EVIX is not whether their names are new, but that they transform a core variable that originally only existed in the pricing of complex derivatives into something more traders can directly understand and observe.

Why does a lack of price movement not imply a low risk?

Many people tend to interpret "sideways" as "safe" and "low volatility" as "no issue". However, in real markets, the opposite is often true.

A calm price merely indicates that volatility has not yet been released; it does not mean that risk has disappeared or that the system is more stable. Many times, long-repressed low volatility will be accompanied by the rise of something more hidden: fragility.

When the market becomes accustomed to calmness, participant behavior will also change. Leverage gradually increases, stop-loss orders loosen, risk budgets become more aggressive, and strategies like selling volatility, earning carry, and capturing time value become increasingly crowded. On the surface, volatility has vanished; but more accurately, risk has been pushed to a place that is harder to see.

This is also why the truly dangerous moments are often not when sharp fluctuations have occurred, but when volatility has been long suppressed and everyone starts to believe "there shouldn't be any issues."

Once an unexpected shock occurs at this time, the market faces not just ordinary volatility, but a potential sudden realization of tail risks. What originally appears as linear price fluctuations can rapidly turn into non-linear cascades, forced liquidations, and evaporating liquidity. Many who profited in low-volatility phases only made some small, stable "calm收益"; however, a fat-tail extreme event can easily consume all those earnings along with the principal.

Therefore, low volatility does not inherently equal low risk. Often, it merely shifts the risk from "visible fluctuations" to "invisible fragility".

This is also why volatility deserves independent study. It not only tells you how much the market has recently moved, but also reminds you whether the market's pricing of future uncertainties has started to deviate from the apparent calmness in front of you.

For traders, there is an important saying: when volatility is extremely compressed, do not take on asymmetrically high risks for small profits. What you see before you may just be calm; but deep within the market, there may be an intense release yet to be realized.

Why does volatility often reflect sentiment earlier than price?

Price is explicit, while volatility is often leading.

A market may seem unchanged over a certain period; candlesticks may appear dull, but once the market begins to pay a higher premium for future uncertainties, volatility will start to move first. In other words, the market hasn't truly moved yet, but funds are already paying for "potential large fluctuations".

This is where volatility is more valuable than price. Price reflects the already transacted results, while volatility is closer to the anticipatory pricing of the market's collective psychology. It reflects not just the basic bullish or bearish direction, but the degree of divergence, density of anxiety, and intensity of expectations.

Conversely, a decline in volatility does not automatically equate to bullish sentiment, nor does it automatically mean bearish sentiment. Commonly, it implies a narrowing of the market's divergence about future paths, or a belief that short-term risks are no longer pressing. However, another important situation is that continued compression of volatility often does not mean risks have vanished, but rather that risks have yet to manifest. Experienced traders don't just ask "will it rise?", but first inquire: will volatility expand or continue to contract?

This is the core understanding of the entire article: volatility is not an accessory to price, but rather the price of market expectations themselves.

From BVIX, EVIX to BITVX: Volatility is becoming a new infrastructure for the crypto market

If we expand our perspective a bit, products like BVIX, EVIX, and BITVX really indicate not just that a platform has added two new products, but a clearer industry trend: the crypto market is gradually completing the infrastructure layer of "volatility pricing".

Gate's announcement shows that BVIX and EVIX perpetual contracts will go live on January 28, 2026, supporting 1 to 50 times leverage; BitMart also published a notice indicating that BVIXUSDT and EVIXUSDT perpetual contracts will go live on the same day. Cboe has announced plans to launch BITVX on March 23, 2026, introducing its VIX-styled volatility methodology into the Bitcoin market.

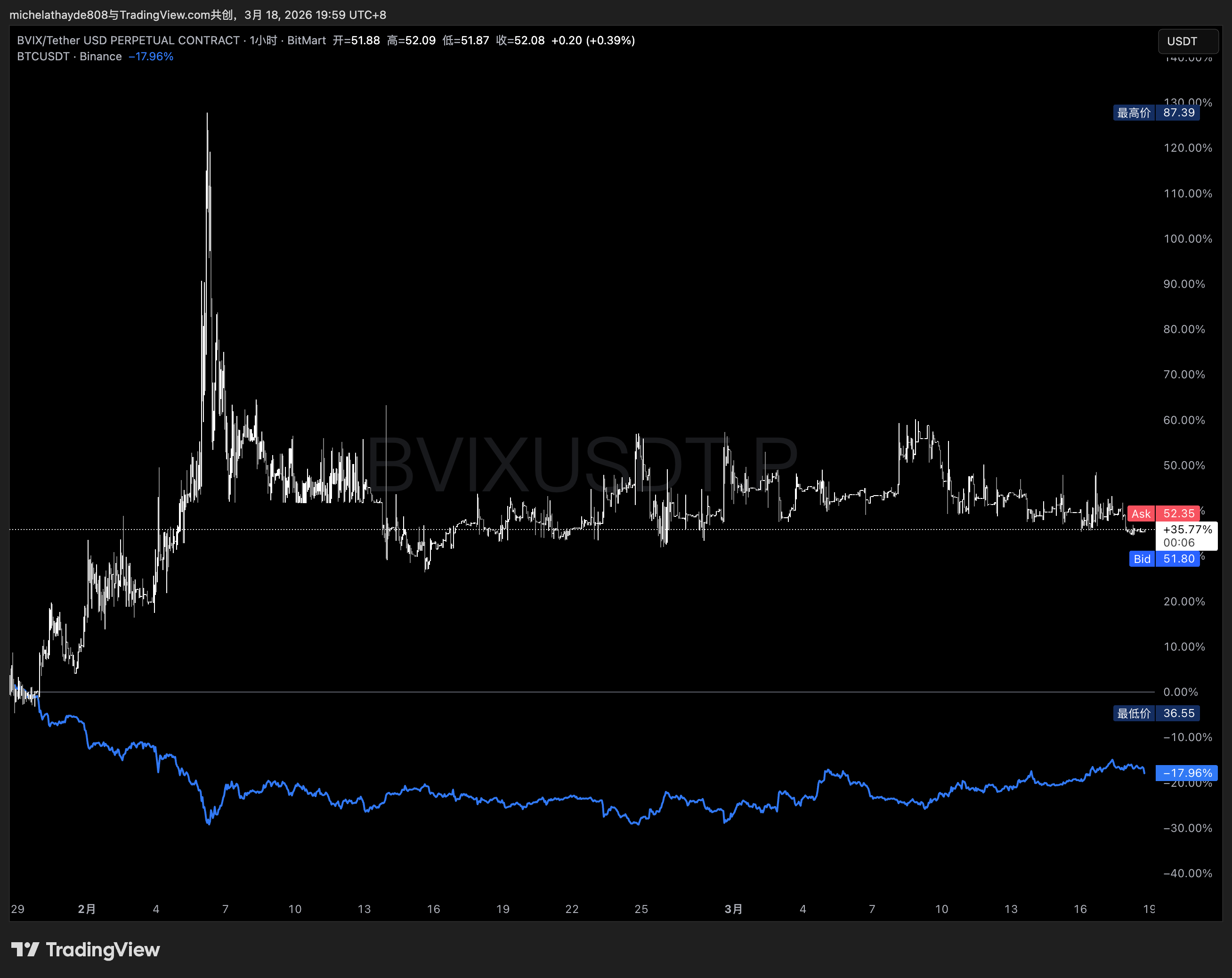

Figure: The trends of BVIX and BTC, gray and white candlestick for BVIX, blue line for BTC

Figure: The trends of BVIX and BTC, gray and white candlestick for BVIX, blue line for BTC

When viewed together, the significance becomes clear: the expression of volatility around crypto assets is gradually transitioning from scattered, specialized information hidden in the options surface, to a more standardized and explicit index system.

The more mature a market becomes, the less it solely trades direction. It will also trade risks, divergences, and uncertainties about future paths. Those who can more accurately understand what risks the market is pricing are closer to the true core of that market.

Therefore, the most noteworthy aspect of products like BVIX and EVIX is not whether they are the latest hotspots, but rather that they represent a change in the structure of the crypto market: this market is starting to take the pricing of "future uncertainties" more seriously.

How to apply volatility in practice?

When talking about volatility, many people's first reaction is risk management. However, this is only partially correct. Volatility can certainly help you defend, but more importantly, it can help you understand when the market is selling panic at a high price and when it is selling calm at a low price.

1. Defensive perspective: Don't chase in at the most expensive emotional moment

When the price just breaks through, market sentiment rapidly ignites, and BVIX or EVIX spikes synchronously, many people instinctively feel "this is the real breakout". However, from a volatility perspective, this often means the market is paying a high premium for future uncertainty.

At this point, it doesn't mean you can't go long; rather, you need to understand: what you might be buying is not just direction but also an already expensive emotional price.

When volatility is high, the margin for error in chasing up and down typically decreases significantly. Your direction may be correct, but because your entry point is at the most excited, expensive expectation position, you still fail to achieve ideal returns. Being right directionally doesn't mean the trade is correct; often, what truly consumes profit is not being wrong directionally but buying too expensively.

2. Risk identification perspective: Surface calm does not necessarily mean true safety

Another more hidden and dangerous scenario is when prices narrow, the market becomes dull, and many people start to think "there’s no risk now". However, if you observe that the volatility structure begins to show anomalies, or the market's pricing for future events subtly rises, it indicates that the calm may just be a surface phenomenon.

At this stage, the most important thing is not to immediately take a directional position, but to first acknowledge one thing: the market may be accumulating fragility that you cannot see with the naked eye.

For high-leverage traders, this phase is especially dangerous. Because what truly destroys accounts is often not the visible large fluctuations, but amplifying risk exposure during "what seems to be fine".

3. Offensive perspective: When panic is sold at high prices, selling volatility may be more attractive

What is truly interesting about volatility is that it can not only indicate danger but also provide strategic offensive windows.

When BVIX, EVIX soar, or more broadly when implied volatility significantly exceeds historical actual volatility, it indicates that the market is paying a high premium for future uncertainty. For directional traders, this is often one of the most uncomfortable areas, as you are buying not just direction but also the expensive panic itself.

However, for more seasoned traders, this can also present an opportunity: to sell overvalued volatility.

In a traditional derivatives framework, these ideas usually manifest as selling high implied volatility options, collecting higher premiums, or executing systematic rolling sell option strategies to earn emotional premiums and time decay. The core logic here is not "I am definitely bearish", but rather "I believe the market's pricing for future volatility is too high".

Of course, this is not an approach suitable for novices to blindly imitate. Selling volatility is essentially a business of earning small profits while taking on significant risks, most afraid of sudden tail events. It has high requirements for margin management, position limits, liquidity judgments, and tail hedging. Hence, what is truly important is not to have everyone become sellers, but to understand a higher-dimensional trading logic: when everyone is trading direction, mature traders may be trading "whether expectations are overvalued".

4. Relative value perspective: Observe the volatility differences between BTC and ETH

In addition to looking at individual volatility levels, the volatility differences between BTC and ETH are also worth observing.

If EVIX continues to be significantly higher than BVIX, it usually indicates that the market believes ETH faces higher uncertainty or is willing to pay a higher risk premium for ETH's future path. This does not necessarily provide a simple bullish or bearish conclusion but can help you understand where funds are betting risk, and aid in determining whether the market is currently more inclined towards core risk aversion or more towards high-elasticity speculation.

Often, the truly valuable information lies not in a certain absolute number, but in the relative changes between different assets and over different time periods. Volatility differentials are, in a sense, the temperature differences in risk appetite.

Real upgrading is not just about knowing bullish or bearish, but about understanding "expectations"

Many traders grow to a stage where they gradually discover a fact: the hardest part of the market is not guessing an up or down, but understanding what the market is pricing.

Sometimes the market is pricing direction; sometimes it is pricing liquidity; but at many critical moments, what the market is truly trading at a high price is uncertainty itself.

This is why volatility should not be understood as an accessory indicator of price. It is neither a footnote next to the market nor only terminology that options players need to care about. It itself is a price, a price for future paths, risk distributions, and expectation divergences.

Price reflects the present, while volatility prices the future.

And what is often most expensive about the future is not the trend itself, but people's fear of the unknown or their misplaced belief in calmness.

As more and more traders begin to pay attention to volatility indicators like BVIX, EVIX, and BITVX, what they are truly concerned about is no longer just whether Bitcoin will rise or fall, but:

Will this market be more intense than imagined?

Has this expectation already been priced too high or too low?

Am I trading direction or the overvalued emotional price itself?

The crypto market is transitioning from "only trading price" to "trading expectations, trading risks, and trading volatility". Those who accept this earlier have a better chance of moving away from simply guessing direction to entering the next stage of truly understanding market structure.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。