Author: Yuan Chuan Investment Review

Anthropic's recent unemployment report has sent chills down the spines of financial professionals.

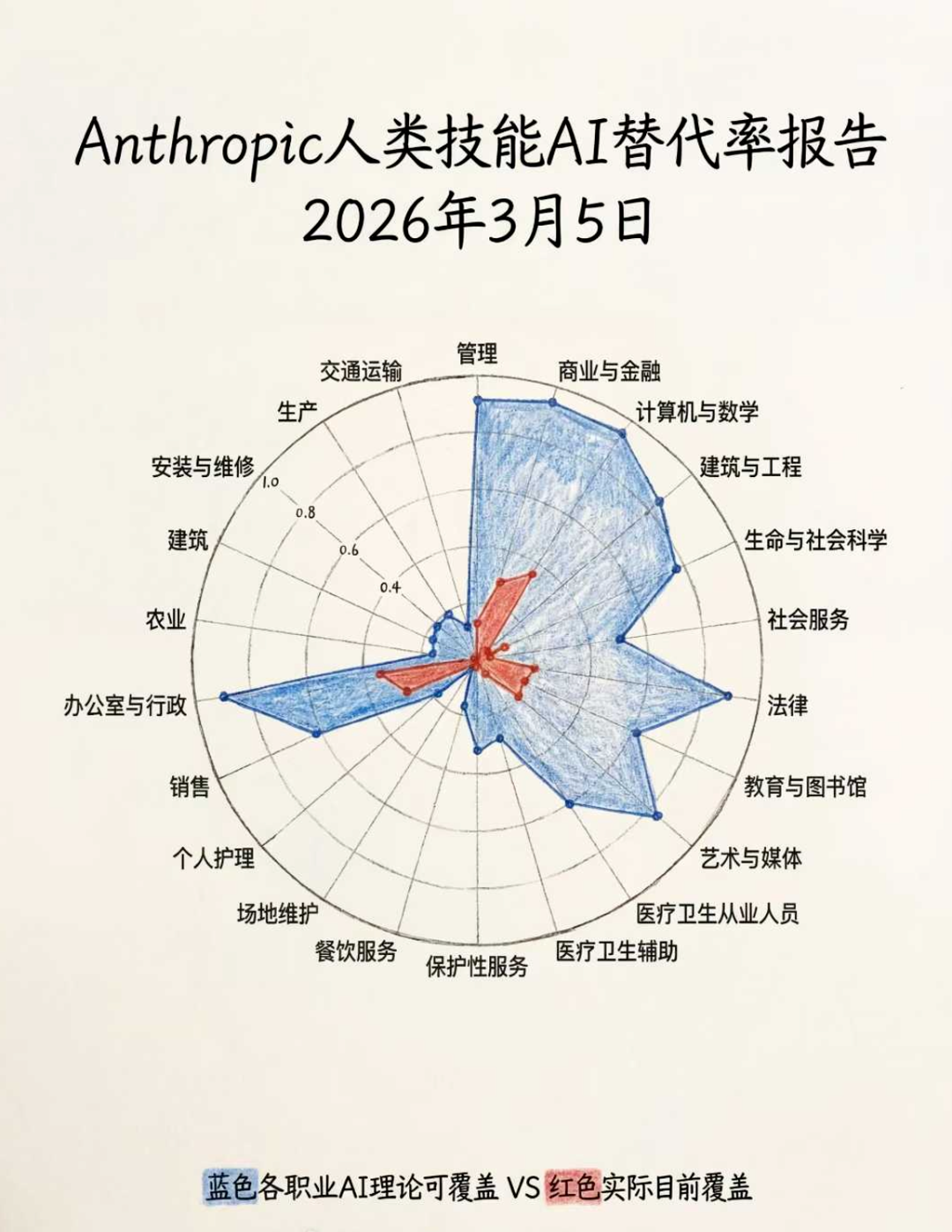

The report shows that the replacement rate for financial positions is as high as 94%, ranking second among all occupations, but the actual replacement rate is only 28% at the moment, leaving a huge potential for the future. Fortunately, 30% of professions are hardly affected, and financial practitioners can also consider reemployment opportunities such as dishwasher or plumber.

Having been in the industry for a long time, one always feels anxious—financial professionals live in a “comparative” world where sales evaluations and performance rankings weigh heavily every day, and without continuous learning, a sense of unease arises.

It’s like after the Spring Festival holiday, when financial practitioners return to their desks and are still engaging with chatbots, while the colleague at the next desk has already raised 8 lobsters, passionately discussing the ups and downs of crude oil.

The financial industry never rejects efficiency, whether it’s from manually placing orders to programmed trading, or from offline bank sales to internet proxy sales, it’s all the same. But this time, AI is not replacing inefficient financial tools, but rather the inefficient people behind those tools. After all, the highest cost in the financial industry is people, and the profits of asset management companies depend on how to manage more money with fewer people.

Thus, private equity firms have started to embrace advanced productivity: Die Wei Asset has launched online courses teaching people how to tame digital researchers that work 24/7; Mingxi Capital uses Manus to automatically generate promotional flyers for dividends that boast a level of sophistication reminiscent of the magazine era. Even clients have become more discerning, as soon as the financial manager finishes recommending a popular private equity fund, they turn to ask whether they should buy Doubao.

The private equity industry is gradually entering a moment reminiscent of Detroit's transformation into humans, where replacements are already beginning to happen across the mature chain of investment research, operations, and sales.

Salary VS Token Cost

In a competitive environment where operating costs remain high and Alpha becomes increasingly difficult to obtain, human efficiency ratio is the metric that private equity owners strive to optimize every night before bed.

In the private equity industry chain, the salaries of researchers are generally not low. According to data from Mu Li Fang, the annual salary for stock quantitative researchers usually ranges from 800,000 to 1.5 million yuan, while subjective researchers earn slightly less but sometimes see staggering incentives—earlier this year, a 10 billion yuan subjective researcher earned over 20 million in year-end bonuses for promoting NVIDIA.

If private equity can successfully utilize AI for investment research, they could save tens of millions in costs. If it can work 24 hours, while reducing hourly wages, it also achieves greater output. Business travel, overtime, transportation fees, and meal allowances—expenses that usually cut into the carry of the boss—would cost nothing for AI.

In the asset management field, all technological advancements boil down to two words: increasing efficiency and reducing costs. Private equity owners do not care whether AI can truly think like humans; they only care if the work can be completed.

In this regard, Howard Marks calculated an economic account: if the output of an analysis is equivalent to that of a 200,000 USD annual salary research assistant, then whether the person paying the salary thinks this work is truly thinking or merely pattern matching does not matter; what matters is whether the work output is reliable enough to have utility value.

After the Spring Festival, eight brokerage firms’ quantitative teams collectively released a tutorial on “Raising Lobsters,” personally accelerating the process of replacing human researchers; they tested OpenClaw, which can actively produce research results like humans.

On the entrance APP, an open-source quantitative roadshow titled “OpenClaw: From Beginner to Pro” was played 4,839 times; Northeast’s Xu Jianhua recommended 20 skills that could increase investment research efficiency tenfold; Fangzheng’s Cao Chunxiao used lobsters to replicate PB-ROE strategy, cup-handle pattern stock selection strategy, and fully automated factor mining and backtesting.

Thinking deeply, this is equivalent to simultaneously OTAing the skill sets of Buffett, O’Neil, and Simons.

Learning Traders

Sellers are working hard on education, and buyers are very proactive in learning. A certain private equity firm in Beijing worried about contamination from the mainframe and issued new computers to each investment researcher, as well as a 50,000 yuan token subsidy specifically for raising lobsters.

Xueqiu Asset’s Yang Xinbin has trained two lobster researchers. He stated that he dialogues with AI far more than with people, and the AI Agent he has autonomously trained works harder in two days than a mature quantitative researcher does in six months, and its potential might even be greater.

Qinyuan Investment’s Paul Wu is gradually incorporating AI into various departments. He feels that AI is completing closed loops in some job roles, capable of independent iterative operation. He foresees that in the near future, the company’s expenditure will turn into the cost of procuring and maintaining an Apple analyst AI agent, and later perhaps an investment portfolio consultant named Paul.

In the past, many private equity firms experienced friction in translating research into practice—researchers felt fund managers were inadequate, while fund managers felt researchers were useless. The emergence of OpenClaw has shown private equity owners a new possibility for the first time—there is no need to endure repetitious internal friction with mediocre researchers, nor worry about core researchers being poached by peers for high salaries.

From a characteristic perspective, lobsters fulfill all the wonderful imaginations that fund managers have of researchers: they work around the clock, don’t take vacations or slack off; they retain long-term memory and can recite key data; they display absolute loyalty and obedience, and won’t take core strategies to establish their own turf; and they continuously self-iterate, unlike old researchers who become trapped in their own path dependence and are eventually eliminated by the times.

If in the future, silicon-based token costs are far lower than carbon-based salaries, how can the bosses of private equity firms refuse a docile, useful AI researcher that can be trained and developed?

Replacement Beyond Lobsters

Subjective private equity still weighs whether the token cost is worthwhile, while quantitative giants, relying on self-built computing infrastructure, have already compressed token costs to exceptionally low levels. However, in the face of this trend, they remain unusually calm.

“OpenClaw is just a semi-finished product that is akin to a toy in the quantitative tech circle,” a leading quantitative figure from Shanghai told me. Its significance lies in lowering technical barriers for subjective organizations and retail investors, providing a clear cost recovery path for the massive upfront investment in infrastructure by large model companies, but it means little in such a serious production environment as quantitative investment.

Another leading quantitative figure expressed his opinion more bluntly, stating that lobsters are operating in the financial circle like a pyramid scheme. OpenClaw features randomness, non-systematic aspects, and low safety, which can introduce great uncertainty to the entire quantitative system.

OpenClaw is not an advanced productive force in the quant circle, and Xun Tu Technology’s Cui Yuchun believes there is no need for anxiety:

Lobsters significantly underperform compared to Agents like Manus and Kimi in Agent optimization and tool usage (involving research browsing, writing, data analysis, etc.). For a researcher without a programming background, it takes 5-10 hours to deploy and initiate, and most tasks cannot achieve results above 60 points.

When retail investors use Lobsters with the China Stock Analysis Skill for stock selection, it feels like opening the door to a new world. Quantitative systems have already built a Multi-Agent platform that crushes lobsters with a richer arsenal of Agents. However, the operation of such a powerful system may not require more humans.

Traditional quantitative investment research systems typically use an assembly line structure: data cleaning → factor calculation → model prediction → portfolio optimization. With the advent of the AI era, some institutions have started simplifying this to role division → tool usage → workflow design, similar to top foreign quantitative firms like Man Group. Standardized and repetitive work is gradually being taken over by AI Agents, freeing research staff from being alienated in factor sweatshops.

For example, Xiyue Investment’s Apollo AI multi-agent system embeds AI Agents into various sectors of investment research, data, trading, and operations. Founder Zhou Xin describes it as adding seven or eight hundred AI employees.

With the previous sci-fi-like crushing of quantitative “unmanned factories” and the subsequent decrease in information disparities by retail investors using OpenClaw, subjective fund managers, who are caught in this intermediate efficiency zone, face a rather awkward situation—they watch as researchers toil to produce information, only to be undermined by quantitative systems from above and pressured step-by-step by retail investors from below, inevitably falling into the urgency of AI FOMO.

During the Spring Festival, I reviewed an annual report from a leading subjective fund manager in Shenzhen, who remarked that fund managers have overly high expectations of researchers:

Fund managers hope researchers can be sensitive to the market, prompt opportunities in a timely manner, provide leading research and judgment compared to their peers, and even need to always remain within the “core circle.” Why do researchers capable of achieving this degree still need fund managers? They could easily make a fortune trading stocks on their own, why do they need to serve fund managers?

As a result, he lowered his expectations—researchers would only be responsible for studying specific targets and questions, with no need to discover opportunities or provide investment advice, as those are the responsibilities of the fund manager.

Conversely, if what a subjective fund manager needs is merely someone who does not penetrate the core industry circle and relies solely on desk analysis to track targets, isn’t that kind of researcher to be replaced by AI Agents next?

Epilogue

Being in the A-share market, these past two years feel like the fast-forward button has been pressed.

Especially in the first half of the year, there were especially many events. Last year, during the Spring Festival, Deepseek was released, the tax was violently increased during the Qingming holiday, and then this year during the Spring Festival, everyone started raising lobsters. Before the first month was over, wars began in the Middle East. Financial professionals' brains have been in an overloaded state, and they can no longer recall when the last holiday without learning was. At least for me as an editor, the computational power of the human brain has become insufficient.

I remember that two years ago, when communicating with fund managers about writing articles, I often heard them cheerfully describe their work status with an awkward sentence—“Every day is like going to work doing a tap dance.” But in the past two years, they have talked about team organization’s “iteration,” investment philosophy’s “iteration,” and industry understanding’s “iteration” without a smile.

AI is developing so fast, and peers are advancing so quickly, it seems that only through iteration can one avoid being eliminated.

The industry is still too anxious.

AI does not understand human nature; it cannot predict whether it’s third-order derivatives or fifth-order derivatives being traded at this moment in the crowded A-share market; AI finds it difficult to empathize; it cannot comprehend why some people have been stuck in two oil stocks for so many years but still hold onto them just to wait for that day to break even; AI cannot take responsibility; it will not face investors blocking them at the door for a 30% loss, nor will it need to draft an apology letter to reflect on its soul or to reconsider itself.

If in the future AI replaces all fund managers and researchers, then the market efficiency hypothesis would hold, and there would be no such thing as Alpha, nor would we likely see the next Buffett.

Thus, the real question is, in the future asset management industry, when AI takes over data extraction, running models, and writing reports, what will remain for humans? What remains is precisely the love for investing, the intuition for uncertainty, and the reasons for staying despite being scolded that research is inferior to AI.

We cannot change the trend of AI's increasing share, but we can change the mindset of being busy coping and exhausted from trying to catch up.

Just like in the game "Detroit: Become Human," the choice players ultimately have to make is not to eliminate AI or surrender to it, but to decide what roles humans and AI should each play.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。