Author: Gu Yu, ChainCatcher

After several months, the Layer 1 public chain track recently saw another round of financing with a valuation of $1 billion. The purported high-performance parallel Layer 1 public chain Pharos announced a new round of capital cooperation upgrade with the Hong Kong-listed company Xiexin New Energy, with Xiexin New Energy completing an investment subscription in Pharos valued at $950 million, amounting to $24.73 million.

Xiexin New Energy is a well-known private photovoltaic power generation company in China, mainly engaged in the development, construction, operation, and management of solar power plants, which aligns very well with Pharos's key development direction in RWA. It appears that this is a deal that holds positive strategic significance for both parties.

However, this transaction has raised many questions in the market. In the current dismal secondary market, can Layer 1 and RWA track projects really achieve a $1 billion valuation in the primary market? Will listed companies easily invest in such high-risk assets?

Mutually Bound Betting Deals

Many details hidden in the complicated announcement indicate that this is not a conventional direct financing transaction but a bundled deal of mutual investment, phased delivery, and market cap betting, with all core delivery conditions firmly in the hands of Xiexin New Energy. If any condition is not met, this transaction will just be a mere paper document with no substantive constraints.

Among them, Pharos's share subscription for Xiexin New Energy is a pre-investment, which will allow the company to subscribe for up to 183,480,000 new shares at a price of HKD 1.05 each, valued at approximately HKD 150 million. This price represents a 15% discount compared to Xiexin New Energy's current price (HKD 1.23).

This deal seems to favor Pharos, but Xiexin New Energy evidently understands the intricacies of financial operations, setting five stringent delivery thresholds for this share subscription transaction. Furthermore, if any batch of delivery conditions is not met, all subsequent deliveries will cease, and the entire agreement will only be valid for 18 months. Specifically, this investment is divided into five batches of delivery, with unlocking conditions all tied to the listing performance of Pharos Token:

The first batch of delivery accounts for 50% and will proceed only if Pharos Token successfully obtains approval for listing on relevant Web3 exchanges, with the opening price not lower than the company's agreed investment price (based on a valuation of $950 million). If the listing fails or the opening price falls below the issue price, the company has the right not to proceed with the delivery.

The second batch of delivery accounts for 12.5% and will proceed only if the average FDV (fully diluted market value) of Pharos Token over the three months leading up to the listing is not lower than $760 million.

The unlocking conditions for the subsequent three batches are roughly similar, with the main difference being the periods over which the average FDV is calculated: the fourth to sixth months, the seventh to ninth months, and the ninth to twelfth months.

Once Pharos Token meets the delivery conditions, the share subscription by Pharos for Xiexin New Energy will take effect correspondingly, and Xiexin New Energy's subscription for Pharos Token will also take effect, with unlocking ratios being the same.

In other words, once Pharos Token is successfully listed, Pharos will immediately deliver a subscription worth HKD 75 million in shares to Xiexin New Energy, while Xiexin New Energy, at a valuation of $950 million, will acquire Pharos Token worth approximately HKD 96.73 million.

For Xiexin New Energy, this is a deal that is almost guaranteed to be profitable; on one hand, it can secure HKD 75 million in subscription funds, and on the other hand, if Pharos Token performs well, it can obtain tokens worth nearly HKD 100 million based on initial opening valuation, providing substantial profit margins.

The favorable conditions have already manifested in the stock price. Although Xiexin New Energy disclosed the cooperation news with Pharos on January 8, its stock price had already risen significantly one week prior, from HKD 0.8 to HKD 1.3 on the announcement date, reaching as high as HKD 1.8 afterward, before consistently trending down. In trading markets, this is a typical “mouse warehouse” trend.

Another potential issue is that Pharos's previously publicly disclosed cumulative financing was only $8 million, equivalent to HKD 62.61 million. Therefore, even if the pre-investment conditions are met, this funding gap may still pose a challenge for Pharos.

Source: RootData

How was the $950 million valuation derived?

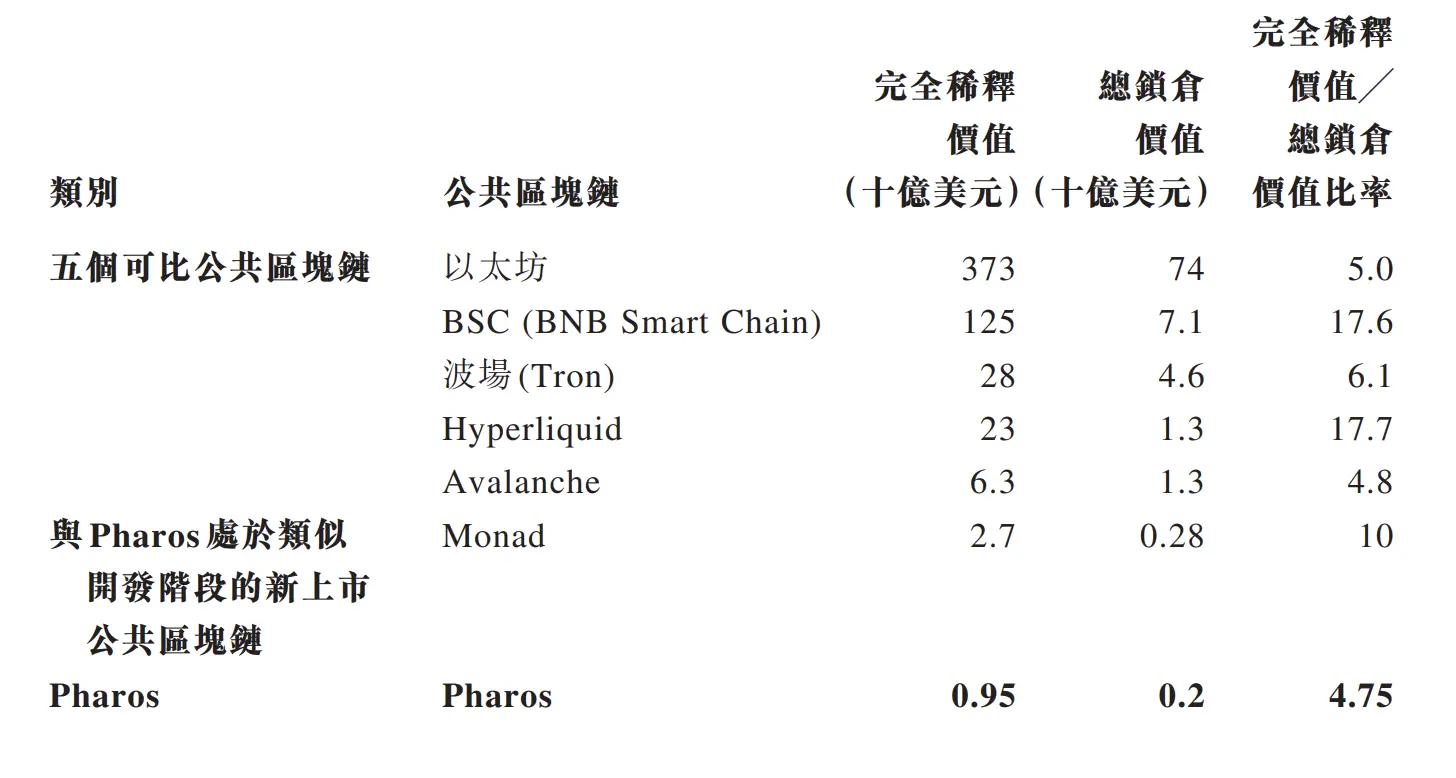

Another interesting piece of information is that Xiexin New Energy detailed in the agreement why it assessed Pharos's valuation at $950 million. According to this agreement, the investment valuation is primarily based on the calculation of the total locked market value on-chain. In the Layer 1 track, the average ratio of fully diluted market value/total locked asset value for Ethereum, BSC, Hyperliquid, Tron, and Avalanche is 10 times, with a median of 6 times, and the ratio for similar technical route Monad is also 10 times.

Therefore, both parties decided to set Pharos's calculation coefficient at 4.75 times, while the current total locked asset value of Pharos is $250 million, calculated with a 20% discount; hence the initial valuation should be $950 million.

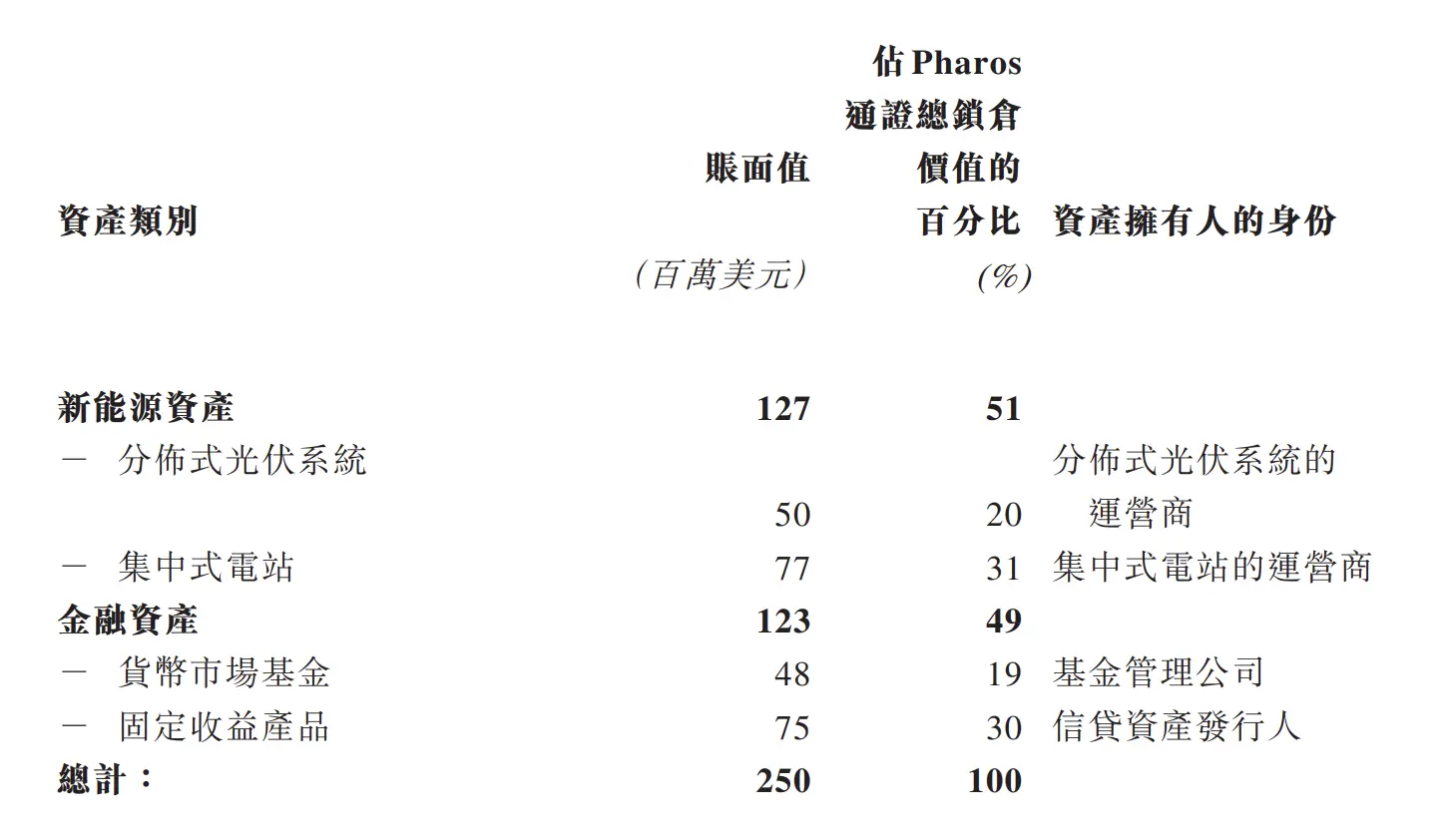

Regarding the types of locked assets on-chain, the agreement discloses that currently, 51% of all locked assets of Pharos come from distributed photovoltaic operators and centralized power station operators' new energy assets, while 49% come from financial assets of fund management companies and credit asset issuers.

In other words, the total locked value of Pharos also includes calculations of physical assets, specifically the power stations and photovoltaic assets closely related to the parties involved in this transaction. This method of calculation sets a precedent in the Layer 1 industry.

In fact, Pharos's mainnet has not yet been officially announced to be online, and the professional on-chain data statistics platform DeFillama has not included Pharos's locked data; hence, the $250 million figure is entirely based on the project's unilateral disclosure data.

The preemptive price movements, combined with the layered betting conditions in the agreement and the inflated valuation calculations, make it clear what the true purpose of this transaction is: for Xiexin New Energy, this may be a financial maneuver to leverage the hype around crypto concepts to boost stock prices and enhance the company's market value; for Pharos, it is an attempt to ride on the back of listed companies' physical assets to generate hype around high valuations and create momentum for the subsequent token listing. Both parties take what they need while leaving the risks to the market and subsequent investors.

When a physical industry company injects physical assets into a Layer 1 project and can easily create a $950 million valuation by calculating based on multiples of physical asset value, is this type of capital game not too outrageous? Does the crypto market really need such RWA?

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。