Author: darkzodchi, Crypto KOL

Translation: Felix, PANews

There are many highly educated and intelligent people in the financial markets, but only a few make money, and a significant portion of those have lower education levels. Despite having learned a lot of theory, they fail to make money. What causes this "anomalous" phenomenon? Crypto KOL darkzodchi analyzes this phenomenon based on personal experience and research, and presents five major cognitive errors commonly made by smart individuals. The details are as follows.

I know someone who can mentally solve differential equations. He graduated with excellent grades and works at a top technology company you have definitely heard of, earning $180,000 a year. But his net worth is essentially zero. If you count the car loan, it might even be negative.

In sharp contrast, most of my friends dropped out of school by age 20 and dedicated themselves to entrepreneurship or trading, and their current income is higher than that of those with finance degrees. Half of them do not even understand basic economic terms; they only know when to take action.

What is going on here?

I have seen this scenario countless times: strategists almost never take action. Have you ever wondered why university professors don’t drive Ferraris? Because they know in theory how to act but don’t know how to do it in practice.

Let’s talk about five mathematical errors that particularly trouble smart people, and "foolproof" solutions for each error.

Mistake 1: Pursuing precision while ignoring the importance of action

Smart people like to pursue absolutely correct answers. This pursuit is rewarded in school: in math exams, a 97% accuracy rate is far less than 100%.

But in the world of money? Achieving a 97% accuracy rate next month is far less valuable than a 70% accuracy rate right now.

I witnessed a friend spend two years building a "perfect" liquidity provision project, even raising funding for it. He used custom indicators and conducted backtesting over a span of 15 years, covering three different volatility environments. To be honest, it was indeed an impressive effort.

But by the time he launched, the market environment had changed. His model was designed for a market that no longer existed. Meanwhile, an unknown person on the CT forum made $80,000 with three lines of simple heuristic code—"buy when the funding rate is negative, sell when it's positive"—while my friend was still struggling to refine his model.

There is actually a formula called the value of information, which tells you when it’s worth doing more research:

VoI = EV (decision after obtaining more information) - EV (immediate decision) - delay cost

If VoI > 0, stop researching and take action immediately.

Delay cost is something that smart people often underestimate. They think the cost is zero because doing research makes them "feel productive." This is not the case. The market is changing, opportunities will disappear, and capital will sit idle.

Individuals also frequently make this mistake. In August 2025, I spent a month contemplating how to build a Polymarket project, trying to come up with an extremely complex plan, until I completely forgot about it.

By October, I changed my mindset and started coding every day. By November, the project was live.

The time wasted on "thinking about ideas" was greater than the time spent actually creating ideas. A typical case of self-sabotage.

Solution: Set a deadline before you begin researching. "No matter how much information I have, I will make a decision by Friday." This single habit is more valuable than any formula.

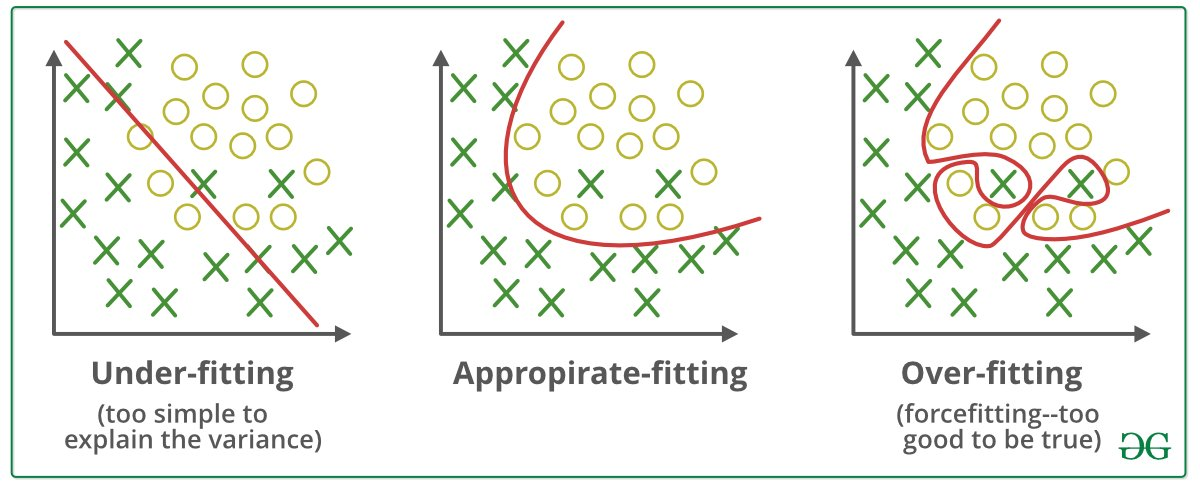

Mistake 2: Looking for patterns in noise (and betting on them)

This is a big problem and is unique to smart people.

If you are smart, your brain acts like a pattern recognition machine. It is this ability that has helped you achieve excellent grades and ideal jobs. You can always see structure where others see chaos.

The problem is that financial markets are mostly chaotic. Your remarkable pattern-matching brain will find patterns that do not exist. Then it will convince you that these patterns are real, and you will place bets, ultimately leading you to lose everything.

This situation is known as "overfitting." Here is an example to illustrate how it works.

Pick any dataset: stock prices, temperature readings, anything will do. Run enough combinations of indicators, and you will surely find a formula that "predicts" the past with 95% accuracy. In backtesting, it looks great. But it is garbage; it found patterns in noise.

Overfitting test:

- If your model has N parameters and you tested K combinations:

- Expected number of false discoveries = K × significance level

- Testing 100 indicators at p = 0.05 will generate 5 "significant" results that are purely noise.

I have been caught in this trap as well. In 2022, I discovered a "pattern" on ETH that worked for three months of data, likely related to the trading volume ratio of Binance and Coinbase. The backtesting looked flawless, and I was excited and immediately invested $2,000.

The result? I lost $400 in the first week. The pattern was just noise. At that time, I wasn’t smart enough to realize that being able to "discover it" was the problem itself.

Data from Polymarket strongly corroborated this. When I analyzed 112,000 wallets, those employing the most complex strategies (more than 10 signals, complicated machine learning models) performed worse than those that only used 2-3 simple rules. The more complexity = the more overfitting = the more losses.

Solution: Before trusting any pattern, ask yourself: "If I test 100 random strategies, how many would look this good purely by luck?" If the answer is more than 1 or 2, then your "discovery" is likely just noise. The Bonferroni correction can help: divide the significance threshold by the number of strategies you are testing.

Mistake 3: Diversifying investments when you should concentrate (and vice versa)

This resonates deeply with me because several years ago, I operated five different projects simultaneously, and they all failed.

Every smart person knows "not to put all your eggs in one basket." It's like the first rule of finance: diversify your investments. Modern portfolio theory, Markowitz, Nobel Prize winner.

However... actual mathematical calculations reveal some more subtle truths that most people overlook.

When you have no edge, diversification protects you. If you are stock picking randomly, then diversification is certainly fine. You truly don’t know what will happen in the future.

However, when you actually have an edge (you have truly uncovered an undervalued investment opportunity), diversification can dilute your returns. You’re diluting your best ideas with those mediocre ones.

- Kelly concentration criterion: f* = edge / odds

- If your edge is 15% and the odds are 1:1, then f* = 0.15 / 1.0 = 15% of capital

- If your edge is 3%, then f* = 0.03 / 1.0 = 3% of capital

The literal meaning of this formula is: the greater the edge, the more you should bet; the smaller the edge, the less you should bet. It does not say to "evenly distribute all capital across 47 positions."

Buffett (who is quite skilled at this) has repeatedly stated that diversification is a protection against ignorance. If you know what you are doing, then diversification makes no sense.

Previously, during the SOL and BSC craze, I held 5-10 different tokens. The best-performing token rose 120%, but it only accounted for 4% of my portfolio, earning me about $80 in total. Meanwhile, my largest position fell 40%.

The top wallets I studied on Polymarket always held only 3-5 positions at any time, and that’s it, but the size of each position was determined based on their edge.

Solution: Honestly ask yourself: Do I have an edge in this trade? If yes, then increase your position (within the Kelly criterion). If not, either completely abandon it or allocate it index-wise. The compromise of "putting a little in each" is a graveyard for returns.

Mistake 4: Anchoring to irrelevant numbers

Smart people are particularly susceptible to the anchoring effect because they remember numbers, and those remembered numbers become subconscious reference points for all future decisions.

"I bought ETH at $4,800."

So what? The market doesn’t care. This number is completely, utterly, 100% irrelevant to whether ETH is worth buying today. But your brain has welded $4,800 to your self-esteem. Now, every price below that feels like a "loss," and every price above that feels like "breaking even."

This is not just a feeling. It measurably alters your behavior:

- You hold losing positions too long (waiting to "break even")

- You sell winning positions too early (fearing to give back profits).

- You evaluate new opportunities based on past prices rather than future value.

There’s a very simple test to verify this. Daniel Kahneman calls it "Would I buy it today?"

- You hold an asset, and the current price is P.

- You bought it at price P_0.

- Completely ignore P_0; it is sunk cost.

Question: If you had cash now, would you buy this asset at price P?

- If yes → hold

- If no → sell

- If unsure → your position is too large

I had to write this phrase on a sticky note and put it on my monitor: "Would I buy it today?" Because even knowing this bias, I still subconsciously think: "But I’m only down 20% now; let’s see if there’s a rebound." The anchoring effect is that powerful.

This is not just applicable to trading. Salary negotiation? If your current annual salary is $90,000, you anchor it and request $100,000. But the market salary for your role might be $130,000. You are negotiating with yourself using an irrelevant anchor. Changing jobs? "I’ve been here for 4 years." So what? The question is whether you should stay here for the next four years or go elsewhere. The past four years are, in any case, in the past.

Solution: Before making any financial decision, write down the numbers that influence you. Then ask yourself: "Is this number really related to future outcomes, or am I just constrained by past experiences?" If it’s past experiences, cross it out (literally, cross it out with a pen).

Mistake 5: Confusing understanding with action

This is the cruelest mistake. To be honest, it is also my biggest weakness.

Smart people have read about compound interest and will nod in agreement. They understand the Kelly criterion, can explain loss aversion at dinner parties, and have read "Thinking, Fast and Slow" (or at least the summary).

Then they assume that understanding equates to action. This is not the case; there is a wide gap.

Understanding compound interest does not mean you are investing, understanding the Kelly criterion does not mean you are correctly allocating positions, and understanding loss aversion does not mean you are immune to its effects.

Research in this area exists. It’s called the "knowledge-behavior gap," and it is vast. One study found that there is almost no correlation between financial literacy scores and actual financial outcomes. Those who scored 95 on financial literacy tests were just as likely to carry credit card debt as those who scored 50.

Financial outcome = knowledge × action × persistence

No matter how erudite the knowledge, if the action is zero, the outcome is also zero.

The formula is obvious, but smart people always get stuck on the first part. They accumulate knowledge continuously: read another book, take another course, listen to another podcast. Because the feeling of learning is both secure and safe. The feeling of acting, on the other hand, is both risky and uncomfortable.

I know because I have experienced it firsthand. Before making my first trade, I read three books on investing. I could explain the efficient market hypothesis, factor investing, option pricing—all of it. But what about my first practical trade? I panicked and lost 12% within three days. After learning so much knowledge, it was still emotions that dominated everything.

You know what ultimately helped me? I was on the basketball court at the time, pulled out my phone, and placed a $50 bet on Polymarket, purely to try. Not $5,000, just $50. The stakes were low, real money was involved, and there was almost no chance of winning—but I just wanted to experience what placing a bet felt like.

Suddenly, those probability formulas were no longer abstract. They were directly related to my money. That $50 bet taught me more about my biases than reading 11 books combined.

Solution: After finishing this article, do just one thing, not five things, just one thing. Place a small bet, calculate the expected value, and verify a hypothesis. The gap between knowledge and action is filled through small actions.

Why is this more important than you think?

What troubles me the most about all this is that these five mistakes are not due to being "dumb," but rather "being smart in the wrong direction." Schools train us to be meticulous, precise, and erudite. The market rewards speed, approximate correctness, and proactive action.

The rules of the game have changed, but no one told us.

The good news is that once you see these traps clearly, you cannot ignore them anymore. Whenever you find yourself spending 3 hours researching a $200 decision—that’s mistake one. Whenever you discover an exciting "pattern" in crypto charts—that’s mistake two. Every time you spread capital across 20 positions because of "diversification"—that’s mistake three.

The smartest thing smart people can do is to make themselves a little "dumber." Simpler strategies, fewer positions, quicker decisions. A little less research, a little more action.

Mathematics supports this; the 112,000 wallets I have studied prove it, books prove it, and personal costly mistakes prove it.

Now don’t just sit there; go and practice.

Further reading: Beginner’s Guide: Experienced Traders Share Five Key Trading "Secrets"

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。