Author: Max.s

With the rapid deterioration of the geopolitical situation in the Middle East, the conflict between the US and Iran is pushing the global commodity market towards a new extreme of volatility. In this macro context, a phenomenon that previously existed mainly in the native narratives of cryptocurrency is taking place: decentralized exchanges (DEX) are taking over the pricing power of tail risks and sudden risks in traditional commodities.

As of March 11, the trading volume of WTI crude oil perpetual contracts (WTI-USDT) on the decentralized derivatives exchange Hyperliquid, based on an application chain architecture, has surpassed 1.3 billion dollars (with a 72-hour trading volume exceeding 4.5 billion dollars, and open interest fluctuating between 169 million and 183 million dollars). This figure not only makes it the second largest trading variety on the platform, after Bitcoin, but also marks a substantial expansion of the boundaries of crypto finance. Intensive reports from institutions such as InvestingNews, The Block, and CoinMarketCap confirm that this liquidity surplus phenomenon is not merely incidental hype, but rather an inevitable result of global capital seeking a "all-weather safe haven" under extreme geopolitical turbulence.

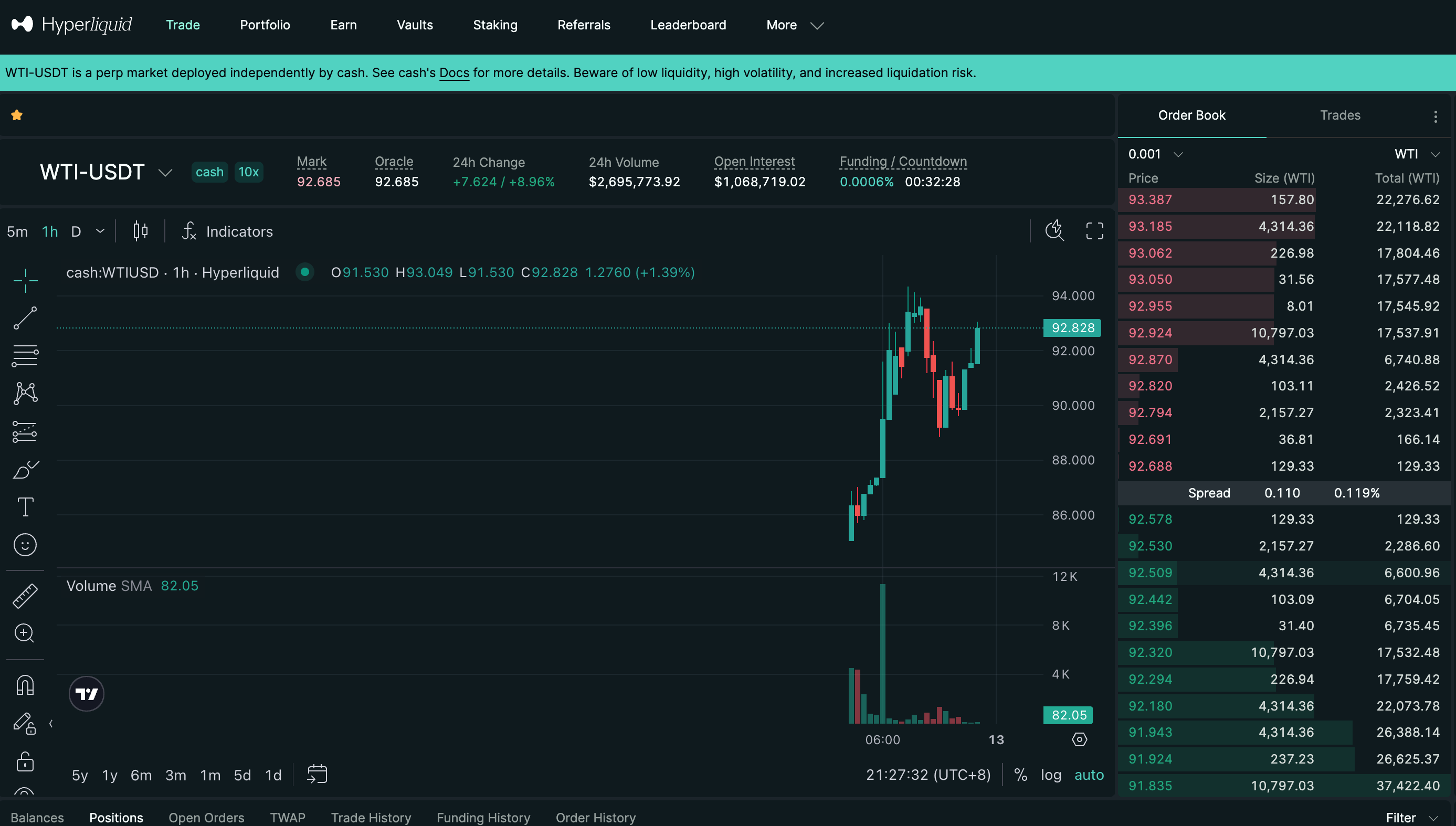

From the snapshot of trading terminal data, we can clearly see the intensity of this financial contest: the mark price of WTI-USDT violently surged to 94.351 dollars in a short period, with a stunning 24-hour increase of 9.99%. The continuous rising green candlesticks on the chart, accompanied by a surge in trading volume, perfectly replicated the panic buying in the traditional energy market in the face of threats of war.

However, what is more worthy of our contemplation is: when oil, the most traditional physical asset, is massively traded in the form of perpetual contracts on a crypto-native DEX, what kind of shift in pricing power is hidden behind this?

The operation logic of traditional commodity markets (such as CME or NYMEX) is based on fixed trading hours, limits on price fluctuations (circuit breaker mechanisms), and strict clearing entry requirements. This structure can effectively control risks during stable operating periods, but often becomes a "dammed lake" of liquidity in the face of sudden "black swan" events.

The escalation of geopolitical conflicts often does not adhere to Wall Street's working hours. When attacks occur during the weekends or off-hours of traditional markets, global macro hedge funds, multinational energy traders, and speculative capital can suddenly face enormous exposure risks without the ability to find counterparties to execute trades in the traditional financial system.

At this time, the crypto market, which operates 24/7, requires no permissions, and has extremely high execution efficiency, naturally becomes the "all-weather alternative" to accommodate this portion of hedging and speculative demand. The emergence of high-performance order book DEX like Hyperliquid perfectly fills this infrastructure gap. Unlike earlier automated market makers based on the Ethereum mainnet, Hyperliquid, relying on customized L1 application chains, achieves sub-second latency and a zero Gas fee trading experience. Its front-end interface professionalism (such as including depth charts, funding rates, limit orders, and take profit/stop loss functions) is already indistinguishable from centralized exchanges and even approaches the trading terminals of traditional finance.

The daily trading volume of 1.3 billion dollars is not just a figure; it is real capital voting with its feet. It proves that the infrastructure of the crypto market has matured sufficiently to support liquidity at the macro asset level of billions of dollars. Under the ancient macro theme of "war and oil," cryptocurrency provides a completely new liquidity escape route.

To explore the deeper meaning of this phenomenon, we must confront a core proposition: the transfer of pricing power.

In traditional contexts, the pricing of derivatives relies on the spot market. Synthetic assets on DEX typically obtain off-chain asset prices as index prices through oracle systems to anchor their value. However, under extreme market conditions when traditional markets are closed, an interesting quantitative gaming mechanism begins to operate.

When the traditional oil market is closed, the spot prices relayed by oracles remain stagnant (shown in the figure as 92.828), but the on-chain mark price (Mark Price, shown in the figure as 92.685) continues to rise due to buying pressure. At this moment, the price of WTI-USDT is no longer determined by spot traders in New York but is driven by pure supply and demand relations on-chain.

When the on-chain mark price deviates from the stagnant oracle price, smart contracts automatically adjust funding rates. Buyers need to pay very high rates to sellers. For quantitative arbitrageurs, if they judge that the price increase of crude oil in the traditional market after opening won’t match the on-chain premium, this presents an excellent short arbitrage opportunity; conversely, if the geopolitical situation severely deteriorates, buyers are willing to pay high funding rates to establish long exposures first.

In this process, DEX essentially replaced CME, becoming the only effective price discovery center for WTI crude oil during market closures. The depth of the on-chain order book, long-short ratio, and the trends of mark prices constitute the most authentic "forward guidance" before the traditional market opens on Monday.

The effective functioning of this mechanism marks the rise of decentralized pricing power. In the past, the crypto market passively accepted the pricing of real-world assets (RWA); now, within specific time windows and extreme liquidity demands, the crypto market is actively pricing real-world assets in reverse. This represents a qualitative change from "passive mapping" to "active market-making."

In recent years, "tokenization of everything" has been one of the grandest narratives in the crypto industry. However, in the past cycles, the main landing scenarios for RWAs have been limited to interest-bearing stablecoins and tokenized US Treasury bonds (like MakerDAO, Ondo Finance). These assets are characterized by low volatility and heavy compliance, essentially moving traditional financial yields onto the chain, classified as "static RWAs."

The explosive popularity of the WTI perpetual contracts on Hyperliquid unveils the second half of the RWA narrative: decentralized derivatives trading of high-frequency risky assets (dynamic RWAs).

The market is no longer fixated on the cumbersome and illiquid spot tokenization of "how to register a barrel of physical crude oil on the blockchain," but rather skips the spot confirmation to directly reconstruct commodity risk exposure on-chain using smart contracts, oracles, and margin systems.

For professional financial traders, buying WTI futures essentially buys the cash flow benefits from rising oil prices rather than a genuine intention to receive hundreds of barrels of crude oil on the delivery date. If this is the case, if a decentralized application chain can provide sufficiently deep liquidity, extremely low trading slippage (estimated slippage of 0%), and decentralized self-custody security, then trading synthetic WTI on-chain is financially indistinguishable from trading WTI futures on CME.

More importantly, this model breaks down geographical and access barriers. Whether institutional traders on Wall Street or independent quants in emerging markets can share the same liquefaction pool without obstacles and borders. This inclusivity and efficiency prove that the practical value of RWAs has thoroughly transcended the purely crypto-native narrative phase, entering the deep waters of macro finance.

The oil price war triggered by the geopolitical crisis in 2026 unexpectedly became an epic stress test for decentralized financial infrastructure. The 1.3 billion dollars of trading volume on Hyperliquid is not just a dazzling trading figure; it is the rallying call for crypto finance to march toward global macro pricing systems.

The ancient game of war and oil has found a new evolutionary field within the codes and smart contracts of blockchain. As the giants of traditional finance return to their desks on Monday morning, they may be surprised to find that the weekend's flames of war have not only altered the world map but also reshaped the trading landscape of global finance. The crypto market is no longer just a playground for tech geeks; it is undoubtedly becoming the "all-weather backup engine" for global risk pricing.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。