Written by: Bibi News

In 1999, Musk founded X.com, aiming to reshape the online payment landscape. A few years later, X.com merged with Confinity and eventually evolved into today's PayPal. Years have passed, and Musk returns to the origin with unfinished dreams.

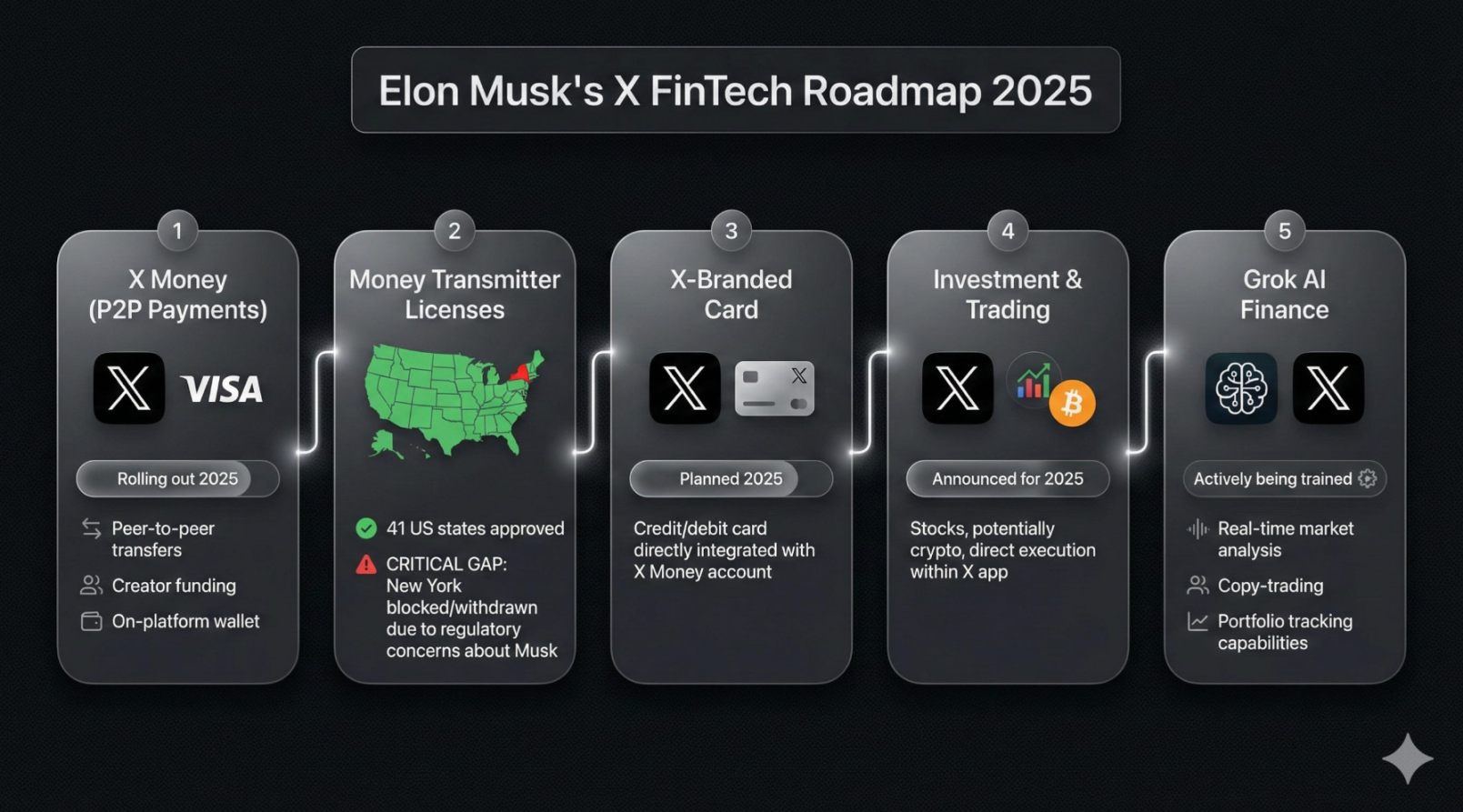

On March 10, 2026, Elon Musk personally announced on the X platform: X Money will begin early public access next month.

This brief post stirred ripples in the crypto community—Dogecoin surged in response, media outlets flocked to report, and the U.S. fintech industry began to reassess the competitive threat posed by this social media company.

X Money, a payment product that has been brewing internally for years, officially enters the final sprint phase for public visibility. However, behind the excitement, a more fundamental question remains unresolved: Is X Money a true financial revolution, or just another Musk-style narrative marketing?

Musk's Everything App Strategy

X Money did not come out of nowhere. Early in his acquisition of Twitter, Musk publicly stated his intention to create an "Everything App" (super app). The goal is to create a super platform that integrates social, payment, shopping, and travel, modeled after China's WeChat. Payment is at the core of this vision.

Musk aims to replicate this path in the United States. His logic is that X already has about 600 million monthly active users who spend a significant amount of time on the platform each day. If a payment feature can be embedded within this scenario, X would upgrade from an attention container to a true financial gateway, becoming the central node for all users' currency transactions, and thereby propelling monthly active users to 1 billion.

The Core Product Strength of X Money

From the disclosed features, X Money's positioning is clearly above traditional P2P tools like Venmo or PayPal.

One of the core highlights is the annualized yield of 6% (APY). Compared to the generally below 0.5% rates of traditional savings accounts in the U.S., X Money enters the market directly with a higher yield, which is likely to become an important tool to attract early users.

Additionally, the product offers P2P instant transfer, direct deposit, a metal debit card engraved with user names, cashback rewards, zero foreign exchange fees, and a $25 account opening bonus, among a range of financial services.

The interface has three main feature tabs: "Account, Rewards, Activities," and the overall design resembles a lightweight digital bank account rather than merely a transfer tool, indicating that it seeks to do more than just act as a payment tool; it aims to construct a social ecosystem around financial behavior.

Transaction settlements rely on the Visa Direct network, achieving almost instant fund arrival. In January 2025, X officially announced a partnership with Visa, which became X Money's first official payment partner.

The significance of this combination lies in: X provides traffic and scenarios, Visa offers a global clearing infrastructure, and the combination largely avoids the high barriers of building a payment system from scratch.

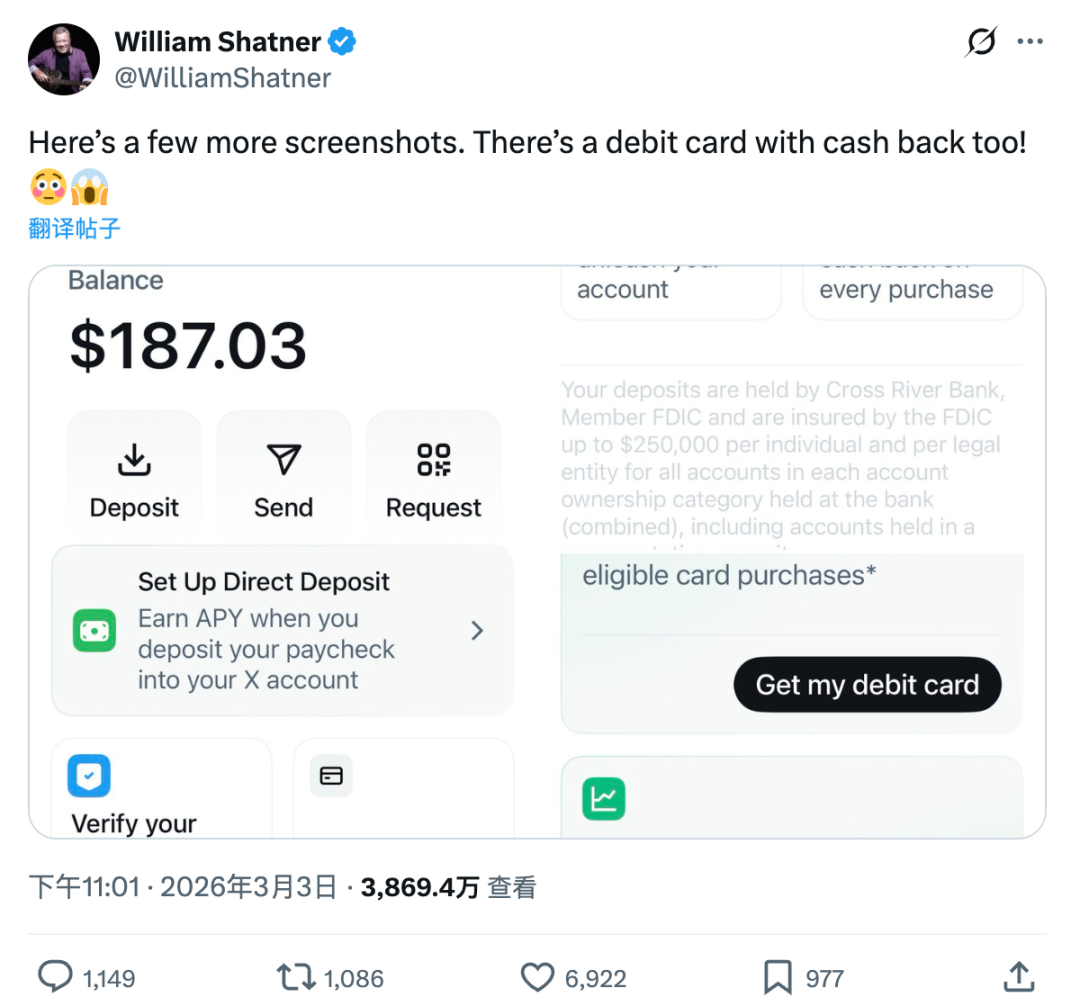

Currently, the product has completed internal closed testing. The external Beta phase is quite reminiscent of Musk's marketing style—X initiated a charity auction through actor William Shatner, allowing those who donate $1,000 or more to gain an invitation to X Money, with a total of 42 spots released. Shatner himself has already experienced the product first-hand and shared screenshots on social media.

Ambitions Compared to WeChat and the Reality Gap

Musk's reference point has always been WeChat.

WeChat Pay's rapid rise is largely due to China's unique ecological environment: an instant messaging tool used by almost everyone, a widely accessible merchant system, and a historical window when mobile payments were not fully established.

X faces a completely different battlefield. The U.S. payment market is highly mature, with Apple Pay, Venmo, PayPal, and Zelle each holding their ground, and credit card networks deeply embedded in daily consumption scenarios.

Although X has about 600 million monthly active users, most people are accustomed to viewing it as an information platform rather than a financial tool. Getting users to actually deposit money into a "social App" requires overcoming not just technological barriers, but also significant psychological barriers.

From a credit perspective, account suspensions on the X platform occur occasionally; if users worry about fund safety and account accessibility, no matter how high the interest rates, it will be difficult to convince them to migrate financial assets. Meanwhile, past controversies over data usage related to privacy issues will be further amplified in financial scenarios.

This concern has already appeared at the regulatory level. In 2025, a New York State senator issued an open letter, urging the state’s Department of Financial Services (DFS) to maintain caution in approving X Money-related permits, citing privacy protection and regulatory risk as reasons.

In fact, over the past few years, X has been quietly advancing its compliance layout. Currently, X has obtained money transmitter licenses in over 40 U.S. states and Washington D.C. and has registered with the Financial Crimes Enforcement Network (FinCEN). Applications in a few markets like New York State are still in progress, but the overall compliance framework has basically taken shape. Users' funds are held by Cross River Bank, which has FDIC insurance coverage, with a limit of $250,000.

The Potential Role of Cryptocurrency

In all discussions about X Money, one topic consistently lingers at the edge—cryptocurrency. On this issue, Musk has chosen silence, at least for now.

Musk's relationship with the crypto world is well-known. Over the past few years, he has repeatedly expressed support for Dogecoin and is also a well-known supporter of Bitcoin. For this reason, when the news of X Money broke, the crypto community immediately began to speculate whether the platform would integrate Dogecoin, XRP, or some stablecoin.

From the currently disclosed information, X Money will initially operate on a pure fiat currency system, prioritizing the dollar, and has never officially confirmed support for Dogecoin or other crypto assets.

But the market clearly does not see it this way: after Musk announced the launch date of X Money, the price of Dogecoin immediately surged, and various speculations about the "$" symbol button have continuously circulated in the community, with rumors about XRP and the Ripple stablecoin RLUSD also spreading among the community.

This ambiguity may be Musk's cleverness. For Musk, cryptocurrency integration seems more like a card that can be played at the right moment. Starting with fiat can bypass additional regulatory complexities while first building a user base and financial data, leaving space for future possibilities.

User Trust and Habitual Barriers

The real challenge may not necessarily stem from the crypto assets themselves. For X Money, the pressure comes not only from direct competitors like PayPal or Venmo, but more deeply from users' entrenched habits of use. Putting funds into a social platform account creates a higher psychological barrier than technical barrier for most American users.

From a favorable perspective, X has extremely low distribution costs. Reaching 600 million users without additional customer acquisition investment is a significant advantage that Venmo could only aspire to when starting from scratch. A 6% annualized yield may become a powerful user acquisition tool during a declining interest rate cycle. The metal debit card with engraved usernames also reinforces a sense of identity for the product on a material level.

From another angle, the logic of the "super app" has its cultural limitations in America. American users are accustomed to using multiple dedicated apps to address different needs rather than relying on a single super entrance. Previous failures such as Bakkt's setbacks and Kraken's application for a Federal Reserve account remind us that fintech in the U.S. faces dual obstacles of regulation and user habits that are not always smooth sailing.

Tests of Scale and Global Expansion

If X Money successfully completes its early public access in April, the real test is just beginning.

First, can it achieve large-scale adoption? A 6% APY is an enticing hook, but whether it can lock in users' long-term financial behavior depends on the coherence and reliability of the entire product experience.

Second, the timeline for global expansion. X plans to extend to international markets by the end of 2026, but the EU GDPR, various countries' AML/KYC compliance requirements, and local competition dynamics are all variables that cannot be underestimated.

Third, the profit model. X Money waives many fees for users, but where will the revenue come from? If relying on deposit interest margins, it will face pressure in a declining interest cycle; if shifting towards value-added services, it will need to build a more complete financial product matrix.

Historically, U.S. internet giants entering finance have often ended in setbacks—Facebook Pay's failure, Bakkt's growth stagnation, Google Pay's repeated restructuring. The path chosen by X Money is closer to that of banks rather than tech companies, which is both its advantage and burden.

Real financial ambitions can never be replicated overnight. WeChat's success was a product of timing, location, and collaboration, and whether X Money can replicate this miracle in the U.S. or even globally remains to be seen. The early public access in April will be the first real answer to this ambitious experiment.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。