Written by: ConvexDispatch

Translated by: AididiaoJP, Foresight News

Introduction

This is not a conservative investment; this is a convex investment (an asymmetric structure where risks are limited, and returns are unlimited).

If you believe that Ethereum's price has peaked, that it will always be a niche player in global finance, or that blockchain adoption has fundamentally stalled, then the story of BitMine Immersion Technologies (NYSE: BMNR) may hold no significance for you. But if you think it is possible for Ethereum to increase tenfold in the next decade, or even that it will eventually become a foundational financial network with a value far exceeding its current valuation, then a more important question arises:

Which investment tools are structurally best positioned to benefit from such an outcome?

My answer is BitMine.

In less than a year, BitMine has transformed from an unremarkable cryptocurrency miner into what I consider the "Berkshire Hathaway of the blockchain"—a company that prioritizes its balance sheet and seeks to achieve compounding value growth through scale, patience, and bold capital allocation. Berkshire relies on stocks and insurance float, while BitMine relies on Ethereum ownership, staking yields, and long-term options related to the Ethereum monetary base.

The emphasis on Ethereum here is not to treat it as a trading asset, but to see it as infrastructure. It serves as the dominant execution and settlement layer for on-chain finance, asset tokenization, stablecoins, and smart contract activities. If Ethereum continues to expand its role within the global financial system, then owning it, having sufficient scale, and demonstrating patience will become decisive advantages. BitMine is clearly optimizing for these variables.

As of today, BitMine controls over 4.167 million ETH, making it the largest public company holding Ethereum in the world, along with nearly $1 billion in cash. At the current price, the company holds approximately $13-14 billion in assets, yet its market capitalization is equal to or slightly below this asset value. In plain terms, buying BitMine shares right now is akin to purchasing Ethereum at nearly spot prices while receiving the added benefits of staking yields, the management team’s capital allocation ability, and strategic options.

This is not betting on next quarter's earnings report. It is betting on who can dominate the balance sheet, who can demonstrate patience, and who can execute in a world where Ethereum increasingly resembles financial infrastructure. The following article will delve into BitMine's strategy, financial condition, various valuation possibilities, and potential risks. Please consider it as a long-term, asymmetric investment story rather than a reference for short-term trading.

A Bold Vision: Holding 5% of Total Ethereum Supply

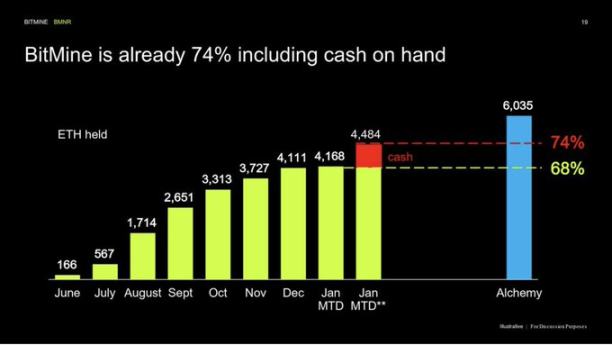

BitMine's chairman, Tom Lee (@funstrat), speaks of "the alchemy of 5%"—holding 5% of Ethereum's total supply. As of January 11, 2026, BitMine holds 4,167,768 ETH, approximately 3.45% of total ETH supply (with a circulating supply of about 120.7 million). Within just six months of execution, BitMine has achieved nearly 70% of this goal. This immense reserve has made BMNR the clear leader as the largest public Ethereum holder. To put it bluntly, BitMine now possesses more ETH than most leading DeFi protocols, surpassing top holders like the Ethereum Foundation, and leaving other publicly traded cryptocurrency companies far behind. The only company holding more in the cryptocurrency space is MicroStrategy's Bitcoin reserve (approximately 672,000 BTC), but in the Ethereum arena, BitMine stands alone as a giant whale. The goal of reaching a complete 5% (approximately 6 million + ETH) is still the endpoint, and management does not appear to have any plans to stop; in recent weeks, they have been increasing cash reserves while continuing to buy tens of thousands of ETH. This scale evokes memories of Berkshire's heavy positions in Coca-Cola or Apple stock, only this time it involves digital assets. BitMine's strongly held bet is that Ethereum is the future financial network, and owning a substantial share will yield significant strategic and economic benefits.

A crucial point is that BitMine's ETH accumulation strategy focuses on how much value each share can bring to shareholders rather than just how impressive the total looks. The company only issues new shares when they can add value—meaning when they can raise money at a price higher than the current net asset value per share—and then uses that money to buy even more ETH. This approach allows BitMine to increase its ETH reserves while avoiding the dilution of existing shareholders' proportional holdings in those reserves. For instance, in September 2025, BitMine sold $365 million worth of stock at a price of $70 per share, 14% higher than the market price at that time. Management immediately used the proceeds to buy ETH, increasing both total ETH and each share's ETH. Tom Lee explained, "Selling stock at $70… is a substantial value increase… because the money raised is primarily used to buy ETH." This is similar to how Berkshire only issues stock during high-value acquisitions—BitMine is using its stock to "acquire" more ETH, provided that doing so enriches existing shareholders more. The result is a rapid growth in net asset value while maintaining or even increasing net asset value per share. Since pivoting to this Ethereum-centric strategy in mid-2025, BitMine's per-share crypto asset value has risen significantly, proving that this dilution-free growth strategy is effective.

Financial Pillars: Massive Crypto Reserves and Strong Balance Sheet

Like Berkshire, BitMine's balance sheet is central. The company's entire philosophy revolves around expanding its asset pool. According to the latest data (January 11, 2026), BitMine's total assets (crypto + cash + equity) amount to $14 billion, specifically including:

- Ethereum (ETH): 4.168 million, valued at approximately $3,119 each at the time of the announcement (totaling about $13 billion). This is the core reserve and constitutes the vast majority of BitMine's net asset value.

- Bitcoin (BTC): 193, a relatively small holding (with BTC valued at approximately $90,000, about $17 million).

- Cash and equivalents: $988 million in cash, providing the company with flexibility to buy during market downturns or sustain operations without selling ETH. Although buying ETH costs a lot, BitMine's cash actually increased by $73 million in the first week of 2026, indicating they either secured additional financing or realized some profits.

- "Moonshot" investments: Approximately $23 million invested in Eightco Holdings (NASDAQ: ORBS), a small strategic investment. (This will be discussed later, as BitMine recently made a larger "moonshot" bet on MrBeast's company.)

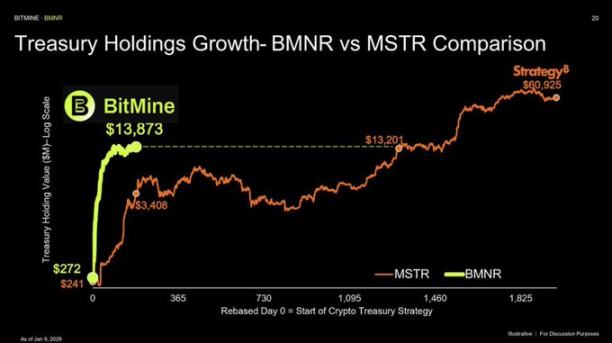

- There is little debt or liabilities accompanying these assets—BitMine's strategy is to grow through equity financing rather than high leverage. Therefore, the book value (shareholders' equity) is roughly equal to these $14 billion in assets. It is worth noting that BMNR's market value (stock price × total shares) is still slightly below its asset value, implying that the stock is being sold at a discount relative to what it holds. At the recent closing price of about $30.87 (January 15, 2026), BMNR's market cap was around $13.3-13.8 billion—approximately 5% less than the roughly $14 billion net asset value. This 0.95 times price-to-book ratio is reminiscent of early Berkshire, where its stock often traded below its steadily growing book value until the market eventually caught up. Just weeks ago, BMNR's price-to-book ratio was only 0.8 times (an 80% discount to net asset value); at that time, the stock price was around $25-28, with BitMine holding approximately $12 billion in ETH. As the BMNR stock price rose above $30, this gap narrowed somewhat, but the market still has not fully recognized the value of BitMine's assets. In other words, today's investors buying BMNR stock are effectively purchasing Ethereum (and other assets) at $0.95 on the dollar—similar to Warren Buffett's famous "cigar butt" investment approach (where asset value exceeds market price). BitMine's management frequently mentions this undervaluation, and indeed, insiders and institutional investors are supportive: look at the shareholder list, which includes prominent visionaries (Cathie Wood of Ark Invest, the Founder's Fund, Bill Miller III, Pantera, Galaxy Digital, and Tom Lee of Fundstrat himself), all advocating for BitMine's 5% ETH goal.

It's also worth noting that BitMine is already profitable under generally accepted accounting principles, unlike many crypto companies which are still burning cash. In fiscal year 2025, BitMine reported a net profit of $328.2 million (with earnings per share of $13.39). This was achieved even with minimal revenue (derived from traditional mining and services that brought in $6-7 million), with the profit primarily coming from the appreciation of crypto assets and financial prudence, along with some one-time projects (such as fair value adjustments). BitMine even announced a symbolic annual dividend of $0.01 per share at the end of 2025, becoming the first large crypto company to pay dividends. The dividend is symbolic, but it signifies the management's confidence in future cash flows. With nearly $1 billion in cash and substantial crypto assets, BitMine's balance sheet is solid as a fortress, able to withstand volatility in the crypto market. It doesn't need to sell ETH to sustain operations in the short term, meaning it can hold indefinitely, weathering various fluctuations—this is a critical advantage. In fact, BitMine's corporate creed is to never proactively sell Ethereum; instead, it aims to generate returns through lending, staking, or utilizing ETH for something else (much like Berkshire using its insurance float or other people's money to invest without needing to sell its core assets).

From Passive to Yielding: Ethereum Staking and Sources of Income

A common critique of companies holding vast amounts of crypto assets is that these assets are passive, resting like digital gold in cold wallets. BitMine aims to prove otherwise; it wants to turn its ETH into a laying hen that produces eggs. Starting from the first quarter of 2026, the company launched MAVAN (Maker American Validator Network), its self-built Ethereum staking platform. Simply put, BitMine will stake a significant portion of ETH (likely the majority) to help validate transactions on the Ethereum network, thereby earning staking rewards (yields). This move transforms BitMine's treasury into an income-generating asset, akin to how Berkshire uses cash to buy bonds or companies that generate cash flow.

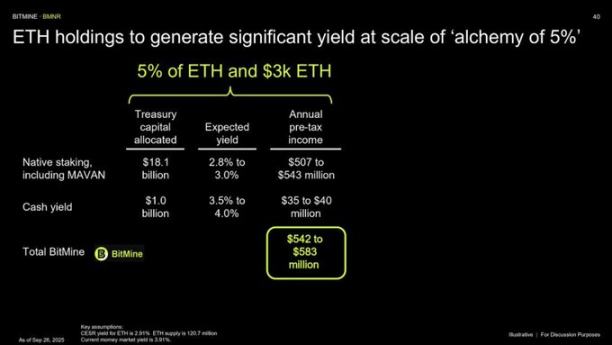

Progress has been remarkable. As of January 11, 2026, BitMine has already staked 1,256,083 ETH (around 30% of its ETH holdings, valued at approximately $3.9 billion at the time). This staking volume surged by about 596,000 ETH in just the previous week, indicating that BitMine is rapidly placing tokens into staking contracts. The current network staking yield (overall Ethereum staking rate) is about 2.81% per year. At this rate, the portion BitMine has staked can earn approximately $110 million in new ETH annually. But BitMine's plan is to eventually stake almost all ETH as MAVAN ramps up. Once BitMine's approximately 4.17 million ETH are fully staked (which is expected to occur in the coming months as MAVAN rolls out), the company anticipates earning over $374 million in staking income annually—translating to over $1 million per day. Tom Lee mentioned at the shareholder meeting on January 15 that, at the current ETH price, the company could receive more than $400 million in pre-tax income from its approximately $13 billion in ETH reserves annually. In fact, BitMine is evolving into something that could be termed a decentralized bank, collecting interest from its digital deposits. Importantly, these rewards will allow the treasury to compound: BitMine will not convert them into fiat currency; instead, it can accumulate these earnings of ETH to further increase its holdings. This mirrors Berkshire's strategy of using insurance float to invest, earning money, and expanding its float—a self-reinforcing cycle of compounding.

In addition to direct staking, BitMine has also hinted at exploring other revenue opportunities at the protocol level in the future (like DeFi lending, providing liquidity, etc.), but staking is clearly the lowest-hanging fruit at this moment. Launching MAVAN at the beginning of 2026 is a key step. By establishing its top-tier validator network domestically, BitMine's goal is to ensure the highest level of security, compliance, and efficiency for staking its assets (and potentially for charging others in the future). This could position BitMine not just as a participant, but as a leader in Ethereum consensus infrastructure, much like some banks have become primary dealers in financial markets. If successful, BMNR will evolve from a pure holding company into a hybrid of an asset management company and a revenue generator, enjoying significant recurring income. Analysts suggest this could support future dividends or stock buybacks—management has even indicated that once the growth phase concludes, a portion of the staking income could be returned to shareholders. Regardless of the path, moving from idle ETH to staked ETH is a game-changing move: BitMine is poised to generate substantial cash flow (in ETH terms) to increase returns. This makes the company's valuation metrics more attractive—investors can look at not just asset net value but also revenue (like price-to-earnings ratios). Earning $374-400 million against a $13 billion ETH reserve implies an annualized return of about 2.8-3%; if ETH appreciates (which BitMine expects), the dollar-denominated earnings will rise too (since staking yields are generally a percentage of the staked asset's value). BitMine likes to point out that $400 million in annual staking income is higher than dividends from a comparable $13 billion stock portfolio—further solidifying the analogy of BitMine as an index fund or holding company, only this time tracking Ethereum.

Strategic Moonshot Plan: Beyond ETH, Expanding Blockchain Horizons

While Ethereum is BitMine's core business, the company does not merely lock coins in the treasury. The management team clearly enjoys making strategic investments (what they call moonshots), leveraging BitMine's crypto expertise and community influence to seek out excess returns. This is somewhat akin to Berkshire buying high-growth businesses to complement its core assets. The latest and currently largest example occurred this week: BitMine announced a $200 million investment in Beast Industries, the parent company of YouTube sensation MrBeast. This deal was announced on January 15, 2026, and is expected to close on January 19. As a result, BitMine acquired a stake in MrBeast's private company (rumored to be significant but non-controlling), which covers YouTube content, consumer brands (Feastables snacks), and upcoming financial services. Why would an Ethereum treasury invest in a YouTuber? Tom Lee explained that this is to connect with future finance and Generation Z. @MrBeast has over 450 million subscribers across platforms and 500 million young fans. BitMine sees this as an opportunity to tap into the attention of the next generation—essentially laying a distribution channel for any blockchain products or educational content it may promote in the future. In the announcement, Lee stated that MrBeast is the leading creator in our generation… possessing unparalleled coverage and engagement among Generation Z and Generation Alpha, adding that BitMine's values align with Beast Industries' spirit of innovation. Furthermore, Beast Industries has hinted at launching MrBeast financial services (potentially including a crypto trading platform). Therefore, if MrBeast later develops crypto applications or tokenization experiences, BitMine's investment could result in a synergistic effect—BitMine stands as both investor and potential backend liquidity provider in Ethereum for these projects.

From a financial perspective, BitMine clearly believes this $200 million has the potential to yield exponential returns. Tom Lee boldly stated he thinks achieving a 10-fold return could be possible. If it does return 10 times, that stake would be worth $2 billion—which is a considerable gain relative to BitMine's current size. Of course, this is speculative and will take years to validate, but it illustrates that BitMine is willing to step outside the pure crypto circle to invest in high-growth areas that can amplify its core mission (media, consumer). This is similar to Berkshire's acquisition of Geico or Apple—these deals aren't directly related to insurance or textiles (Berkshire's original trade) but are highly profitable and complementary to the portfolio. Similarly, BitMine also had a smaller moonshot position in Eightco/ORBS (a company in blockchain and retail tech). These moonshots leverage a small portion of BitMine's treasury to bet on innovation, even if they fail, the core ETH reserve remains intact. If successful, they can provide additional upside and diversification to BitMine's story, making it more than just a means to hold ETH.

It must be clear that BitMine's primary capital use remains to buy ETH; management has explicitly stated that such equity investments will be rare and always based on opportunities. For instance, the MrBeast transaction was carefully considered for its potential to expand BitMine's influence. This transaction highlights that BitMine's current impact is indeed increasing: being invited to co-invest in a company like MrBeast alongside top VCs shows that BitMine is regarded as a credible long-term partner, rather than just an oddball in the crypto world. This could open up more avenues for entry into blockchain media, gaming, or Web3 consumption—areas where a substantial ETH treasury can be an advantage (like providing liquidity for content tokenization or nurturing a creator economy on Ethereum). In summary, while buying ETH is the foundation for BitMine, its Berkshire-like capital allocation approach means that if there’s a chance to safely acquire equity in the next big event, it will take action. These moonshot plans provide an additional layer of growth potential beyond ETH's price appreciation and staking income to investors.

Reframing the MrBeast Deal: More than Speculation, It's Smart Marketing Investment

At this point, it’s natural to question:

Why not buy ETH directly? Why go through BitMine Immersion Technologies stock?

My logic is quite simple:

If you couldn't tell from my username, there's a reason I operate under the name Convex. I like options, I appreciate convexity, and I favor a strong management team. This framework guides how I allocate money across various assets.

Here’s my comparison of BitMine versus ETH.

As long as I can buy at a price close to BitMine's balance sheet value, essentially buying its existing ETH at spot-like prices, BitMine already serves as a clean substitute for ETH.

At this stage, does it matter whether it’s ETH or BitMine? This choice largely disappears. If BitMine's price is close to net asset value, then economically, I achieve the same exposure to Ethereum regardless of which I choose.

Now to the second step, which is a more crucial question.

What else do I gain in addition to ETH exposure?

The answer is options and convexity. If I solely buy ETH, I acquire just one thing: the volatility of ETH prices.

If I buy BitMine, under similar entry costs, I gain:

- ETH exposure +

- No balance sheet leverage

- No forced selling risk

- A highly capable management team aligned with shareholder interests

- Proactive capital allocation

- Staking income

- Strategic moonshot investments

- And non-linear upside potential relative to ETH

That is convexity.

If I buy near net asset value, BitMine doesn’t introduce additional downside risks compared to ETH.

But it does introduce additional upside opportunities.

This potential upside may not fully materialize, but structurally, it exists.

In my framework, this equates to acquiring a free call option, with options on:

- Ethereum becoming global financial infrastructure

- Scaling of staking economics

- Widespread adoption of tokenization

- Ease of entry for consumers and institutions

- Management's ability to seize opportunities over time

This is why I frequently compare it to Berkshire.

Like Berkshire:

- You own underlying assets

- You don’t have to pay for leverage

- You benefit from long-term smart capital allocation

- You gain exposure to some investment opportunities that are difficult for you to replicate

This is how it simplifies my crypto investment strategy.

For me, there's also a very practical consideration.

After buying BitMine, I feel I no longer need to:

- Chase various altcoins

- Rotate through different speculative narratives

- Try to guess which protocol or token will perform best in the next cycle

I essentially outsource this decision-making to a team that:

- Has more information

- Has better channels

- Is larger in scale

- Aligns interests with shareholders

This allows me to focus my attention elsewhere, without having to constantly manage the emerging risks in crypto.

Position and Discipline

Currently, BitMine occupies about 10% of my investment portfolio.

This is not a casual decision.

I have a strict discipline: no single position can exceed 10% regardless of how optimistic I feel.

If ETH weakens and BitMine follows suit, would I add to my position? Possibly, especially through rebalancing.

Conclusion

BitMine has told a captivating story in a short amount of time: it combines characteristics of a crypto ETF, a yield-generating bank, and a venture capital fund. With over $14 billion in assets at hand, aggressively pursuing Ethereum, BMNR lets you invest directly in the second-largest cryptocurrency—but through its accumulation and staking strategies, it also adds a layer of leverage. We have already seen that by January 2026, BitMine had reached critical scale (holding 3.45% of ETH) and is about to start generating considerable income from staking. Its stock price is still slightly below asset value; if you believe there is little room for Ethereum to drop and that the market will eventually realize BMNR's value (just as Berkshire's stock eventually appreciated above its book value during its growth phase), this represents a margin of safety.

Is BitMine truly the Berkshire Hathaway of the blockchain? This analogy is not perfect—no crypto company can fully replicate Warren Buffett's insurance float and decades of compound stock selection. But the similarities are strong: BitMine emphasizes intrinsic value (ETH reserves), long-term growth, opportunistic financing (similar to Buffett's insurance capital), and side investments in promising projects (such as Beast Industries). Tom Lee, as BitMine's visionary capital allocator, draws comparisons to a modern-day Buffett in the crypto world—although considering Lee's public image and the hype surrounding the crypto market, he may be a bit more flamboyant. If Ethereum indeed becomes the next valuable internet, owning a substantial piece of it could be as game-changing as owning a significant stake in foundational internet companies in their early days. BitMine is positioning itself for that possibility.

For investors, BMNR represents a high-conviction, high-volatility choice. In a portfolio, it can serve as a leveraged Ethereum position while providing some downside protection (due to the stock price currently being below net asset value) and also upward thrust (the management's value-add and other bets). One must control positioning accordingly and be aware of those risks. But as of January 2026, BitMine's story is one of execution—currently, everything looks good: net asset value is rising, each share in ETH is increasing, and new catalysts (staking income, share authorizations for continued purchases, the MrBeast collaboration) are on the horizon. The next 12-24 months are critical to see if BitMine can continue growing without diluting shareholders and whether it can begin converting its substantial assets into meaningful revenue.

Ultimately, BitMine Immersion provides a rare case: traditional investment principles fused with cutting-edge digital assets. It bets on disciplined financial engineering conquering the chaos of the crypto market. If BitMine succeeds, shareholders looking back may declare it the Berkshire Hathaway of the blockchain era—transforming a misjudged asset (ETH, somewhat like Berkshire's early textile mills or insurance float) into an empire. If it fails, this experiment will nonetheless teach us much about how corporate finance and decentralized finance interact. Right now, BitMine is absolutely worth paying attention to—or for those willing to take risks, it could be a tool that accelerates Ethereum's wave. As always, do your own research and consider your risk tolerance—but keep an eye on BMNR, as it is making history at the intersection of crypto and Wall Street.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。