Author: CryptoSlate

Translated by: Deep Tide TechFlow

Deep Tide Summary: This article is not merely a simple report on Justin Sun's settlement with the SEC, but places this $10 million settlement within a larger policy context—since Trump's administration, the SEC's enforcement pressure on crypto giants has systematically receded, and the biggest beneficiaries of this retreat are Trump’s own token and stablecoin projects. The article outlines the transmission mechanism between policy and private benefits using quantifiable data ($802 million in revenue, $4.4 billion USD1 circulation), and is worth a close read by anyone interested in the direction of crypto regulation in the U.S.

The full text is as follows:

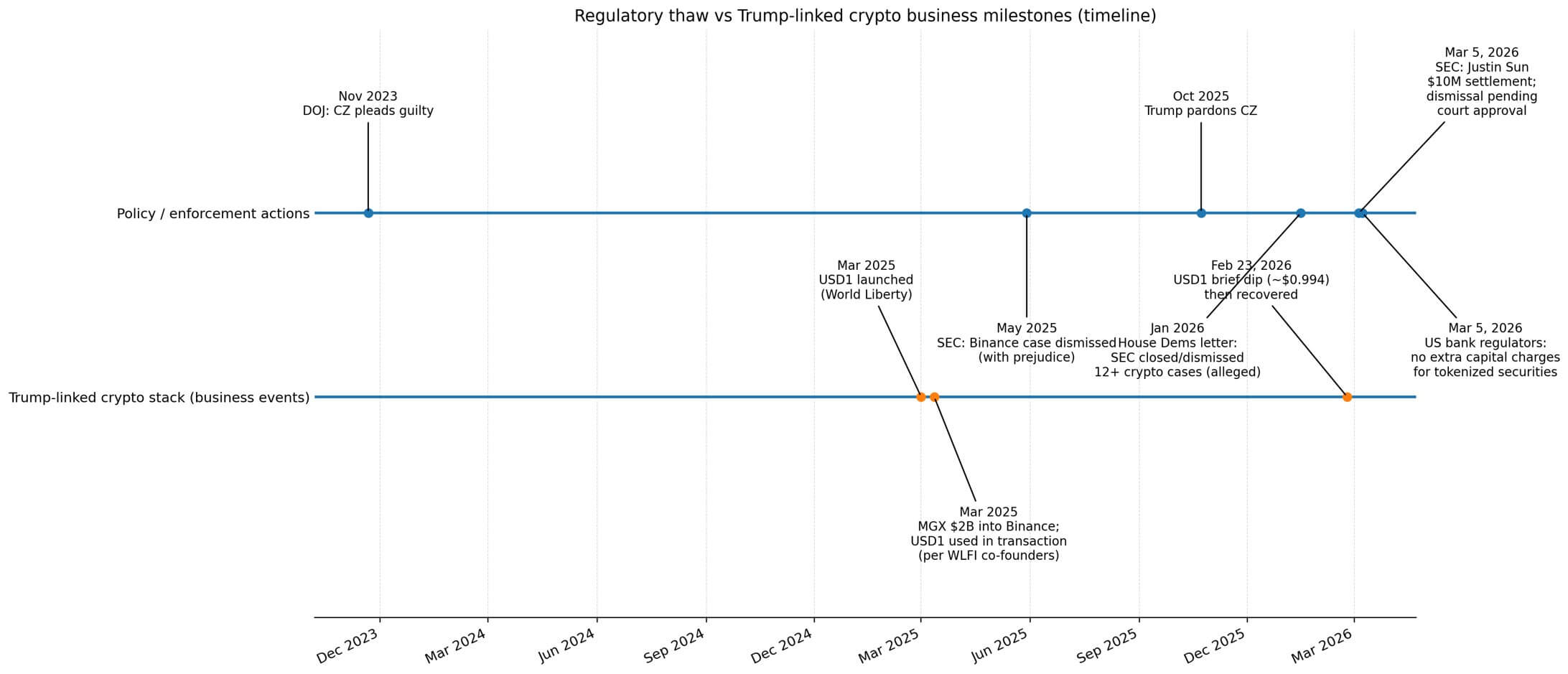

On March 5, Justin Sun reached a $10 million settlement with the SEC, resolving a civil fraud lawsuit. The case alleged that he profited $31 million through operations similar to wash trading and undisclosed celebrity promotions.

The settlement requires court approval and does not include any finding of illegality, leading to the case being dismissed.

On the same day, U.S. banking regulators announced that banks holding tokenized securities and traditional securities would not face additional capital requirements. This technology-neutral qualitative characterization represents another brick being removed from the walls of crypto regulation.

The settlement for Justin Sun coincidentally occurred on the anniversary of the Trump administration’s regulatory contraction.

By May 2025, the SEC's civil lawsuit against Binance was dismissed without leave to refile. In October 2025, Trump pardoned Binance founder Changpeng Zhao (CZ)—who pleaded guilty to money laundering and unlicensed remittance charges in November 2023, paid billions in fines, and served four months in jail.

In January 2026, members of the House Financial Services Committee issued a joint letter noting that the SEC has withdrawn or terminated at least twelve crypto-related cases since January 2025.

The beneficiaries are not only the overall U.S. crypto market. Trump’s own crypto network has quietly taken a position, ready to reap excess private benefits from these entrepreneurs' distribution channels and business relationships.

Token Economics Up Close with the President

In less than a year, two globally recognized crypto entrepreneurs have managed to free themselves from major legal constraints in the U.S.

Justin Sun’s settlement ended the civil fraud case, but it was not a finding of innocence. The SEC's civil lawsuit against Binance was dismissed in a way that does not allow re-filing. CZ’s pardon is a judicial clemency, not a reversal of the facts of his guilty plea.

Meanwhile, crypto projects associated with the Trump family have become direct beneficiaries of the renewed activity in the crypto market.

Reuters calculated that the Trump Organization generated $802 million from crypto operations alone in the first half of 2025, far surpassing other business lines, with the largest share coming from World Liberty Financial’s token economy.

World Liberty's golden document stipulates that 75% of token sale revenue flows to entities associated with the Trump family after deducting operating expenses. The stablecoin component USD1, launched in March 2025, adds another revenue stream through reserve income, with Reuters estimating that it could generate tens of millions of dollars annually once scaled.

Justin Sun became one of the most prominent buyers of the World Liberty token, investing at least $75 million in the WLFI token pre-sale and joining as an advisor.

He also participated in the TRUMP Memecoin ecosystem, with reports linking a "SUN" wallet and HTX-related activities to a large holding, though the specifics remain controversial.

The intersection of Binance and the Trump crypto ecosystem is linked through another channel: Abu Dhabi-supported MGX invested $2 billion in Binance in March 2025, marking the largest institutional transaction in crypto history.

World Liberty co-founders confirmed that USD1 was used in this MGX-Binance transaction.

Reports found that when the total circulation of USD1 was only about $2.1 billion, a single wallet held about $2 billion USD1, illustrating how a single channel dominated the early supply.

By February 2026, according to Artemis data, USD1 had grown to the sixth largest stablecoin, with a circulation of about $4.4 billion.

On February 23, USD1 briefly fell to about $0.994, which World Liberty attributed to a "coordinated attack" on its X account, but the pegged price quickly recovered.

The early supply of USD1 was highly concentrated in the MGX-Binance channel, and then the growth achieved created a distribution advantage that allowed World Liberty's revenue structure to be directly monetized.

Feedback Loop from Policy to Profit

This business design implies that the retreat of enforcement and the gradual guidance from regulatory agencies are reducing friction.

Reduced friction leads to increased activities, and increased activities allow the tokens and stablecoin economies associated with Trump to be monetized.

Trump does not need to personally orchestrate regulatory outcomes to become his biggest private beneficiary. This overlap is mechanical: when the legal pressures on participants controlling the distribution channels are lifted—such as Binance's ability to list on exchanges or Justin Sun's investment capacity—projects capturing the reactivated participants benefit, with the token and stablecoin structure of World Liberty placing itself at these critical nodes.

Stablecoins have evolved from niche crypto infrastructure to macro-level collateral. A working paper from the Bank for International Settlements in February 2026 found that net inflows of U.S. dollar stablecoins by two standard deviations could lower the yield on three-month treasury bills by about 2.5 to 3.5 basis points, with the effect rising to 5 to 8 basis points during times of treasury scarcity.

The growth of stablecoins has now generated measurable demand for safe assets, embedding these tools into interest rate and treasury pipelines.

A working paper from the European Central Bank recorded a "deposit replacement mechanism": the popularity of stablecoins has reduced retail deposits, limiting intermediary banking activity.

Evidence from the Eurozone provides a strict analytical framework for the U.S. banking industry's opposition to the interest-bearing function of stablecoins (concerned about accelerated outflows of deposits), and the ethical norms and anti-money laundering clauses involving Trump-related projects are still contentious.

According to DeFiLlama data, the total market cap of stablecoins is about $313 billion, with a 30-day growth of 3.7%. Even without new legislation, the U.S. is effectively lowering the operational costs of crypto businesses, while Trump's crypto ecosystem has positioned itself as a "toll booth" for distribution growth.

Secondary Beneficiaries and Structural Constraints

The first-tier private beneficiaries are Trump's crypto network. The second-tier public beneficiaries are the overall U.S. crypto market—reduced enforcement risk premiums, accelerated product launches, and more U.S.-focused projects going live.

This distinction is important because it separates correlation from causation without overlooking observable flows of benefit. The settlement is not a finding of innocence; the dismissal was done in a way that does not allow re-filing, and the pardon is clemency rather than a reversal of the facts of the guilty plea.

Even if a direct link between enforcement results and private business connections cannot be proven, the distribution and revenue outcomes remain visible and quantifiable.

SEC Chairman Paul Atkins stated in February 2026 that after previous White House-led layoffs, the agency was in the process of re-hiring, responding to external accusations that the SEC's dismissal of crypto cases was politically motivated, and pointed out that many decisions were made before his tenure.

The thaw extends beyond individuals. U.S. regulators now tend to grant "exemptive relief" for tokenized securities experiments, while the U.K. leans towards a sandbox approach, creating cross-border friction even as U.S. policy overall favors inclusivity.

The next constraint may not be at the legal level, but rather at the legislative and political levels.

Banks view stablecoins as a threat to deposit substitutes. The ethical clauses in proposed legislation could structurally limit the scale of Trump-associated projects, even as the market continues to grow; they could also turn out ineffective, allowing for faster expansion.

Entrepreneurs who have already obtained exoneration at the civil level or received clemency at the criminal level may still face reputational and market access constraints if future enforcement agencies take a tougher stance.

Regulatory pressure can reemerge in the form of policy risk rather than purely legal risk.

Why This Matters

The concentration of benefits gained by Trump’s crypto project raises issues of conflicts of interest, without needing to prove the existence of quid pro quo.

Revenue sharing, stablecoin reserve income, and distribution touchpoints are all reflected in public documents and reports. Policy shifts—decreased enforcement intensity, gradual guidance, civil dismissals, and pardons—have reduced friction.

The private capture of this reduction in friction is most evident in projects where token economics and stablecoin growth directly translate into income associated with the President.

Trump does not need to be the biggest beneficiary of regulatory retreat. The beneficiary status is observable.

As the regulatory agencies of the Trump era lift the legal pressures on crypto leaders, the clearest private upside benefits land in Trump's own token and stablecoin systems, while the broader U.S. market is the second-tier beneficiary. This model holds whether or not the motivations are considered, and the numbers make it clearly discernible.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。