Written by: Ignas

Translated by: Chopper, Foresight News

In the past two months, at least 10 crypto protocols have announced shutdowns. Not exits, but a lack of users, a lack of money, or both.

Not to mention companies like BlockFills and lending platforms freezing withdrawals. Just yesterday, Angle also announced (https://x.com/AngleProtocol/status/2029161525580112263) the gradual shutdown of EURA and USDA stablecoins, despite having a total locked value (TVL) of $250 million and good business partnerships.

Angle stated in its announcement, "The decentralized stablecoin track has changed completely. Stablecoins that offer yields are essentially just repackaged versions of existing treasury and lending protocols, there is no need to maintain a separate set of infrastructure."

These shutting down projects almost all had functioning products:

- Polynomial had a total transaction volume of $4 billion, covering over 70 markets

- MilkyWay's TVL once reached $250 million

- Step Finance's monthly active users peaked at 300,000

I have used these products, or at least experienced them. The technology isn't the problem, but no one is willing to pay fees to keep the projects alive.

MilkyWay is a typical example: four transformations in less than two years. It started with Celestia liquid staking, then shifted to re-staking, RWA tokenization, and a crypto debit card for paying rent... Each transformation chased the trends of the time.

Their description of re-staking is quite moving, "We recognized the re-staking opportunity early, designed the system, TVL soared to $250 million, security audits were completed, and we were ready to launch. But the market abandoned re-staking faster than anyone expected."

In the end, we could only admit that the funds wouldn't last until we found product-market fit.

The Polynomial team bluntly stated the reasons for failure, giving a lesson to all perpetual contract projects: "In the derivatives space, having good technology is useless. We improved execution speed, optimized user experience, and built innovative infrastructure, but it all amounted to nothing. Traders only go to places with liquidity, and we didn't have any. The rest are just flashy features."

The conclusion is harsher: "Liquidity is the only moat in derivatives. You can't beat liquidity with innovation, you can't beat liquidity with marketing, you can't beat liquidity with development."

The closure of ZeroLend serves as a wake-up call for those attempting to launch decentralized applications across multiple blockchains. They placed bets on niche blockchain-supported projects like Manta, Zircuit, and Xlayer, but when the market turned bearish, these chains lost liquidity, and oracle service providers stopped their services.

Ultimately, long-term operating losses made it unsustainable.

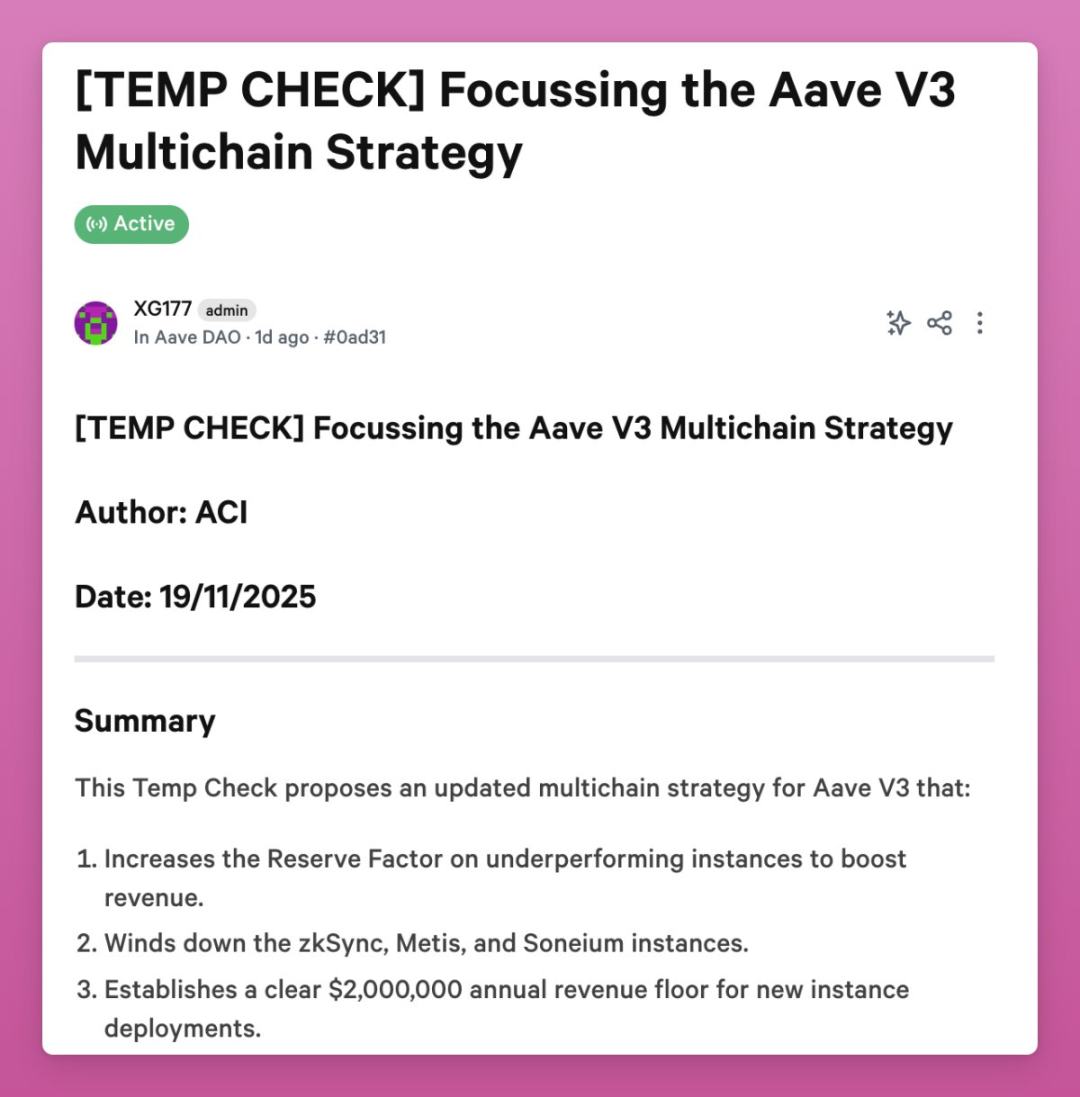

Aave recently also voted to shut down services on several chains, citing the same reason of operating at a loss.

Then there’s Parsec, once a legendary tool in the industry that tracked decouplings of Terra, 3AC, and stETH. But the team admitted, "After the FTX crisis, DeFi spot, lending, and leverage never returned to the way they were. The market has changed, on-chain behavior has changed, and we haven't truly understood it."

In simple terms, the market has shifted, while we remained stagnant. The market is very harsh.

Slingshot was completely shut down after its acquisition. Eden cut 80% of its unprofitable products, leaving only the core business.

As they said, "The 80/20 rule has become a reality; the products for which we incur 80% of costs only bring in 20% of income."

Finally, Step Finance has a more unusual case: it was stolen $26 million on January 31, declaring its death. "Tried raising funds, attempted acquisition, but none of it worked."

What do these dead projects have in common? They failed to adapt to the ever-changing market and lacked the funds to transform again.

Every team bet on a particular ecosystem experiencing explosive growth, but the results either had insufficient growth speed or saw no growth at all. Celestia DeFi never really developed, and on-chain derivatives struggled to compete with Hyperliquid, even well-established platforms like dydx and GMX found it tough to thrive.

Expanding into new chains and realms comes with high costs.

For players like me, transferring money from one platform to another is easy and inexpensive. But applications need to invest significantly more time and resources to prepare for potential new user bases.

The good news is that these are all "decent deaths". All projects gave users time to withdraw funds, the teams did not exit or irresponsibly issue tokens for harvesting. Compared to direct exit schemes in 2022, the industry has indeed learned to die responsibly.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。