Author: Nancy, PANews

After a five-year regulatory marathon, Kraken has finally received authorization for a master account from the Federal Reserve, becoming the first cryptocurrency-native company permitted access. This achievement is not only the result of Kraken's compliance efforts but also an important milestone in the history of cryptocurrency development, further intensifying the heated competition between new and old financial forces.

Securing the Federal Reserve's "ticket", innovative banking license key to breakthrough

On March 4th, Kraken announced that its bank, Kraken Financial, has officially been granted permission to open a master account with the Federal Reserve, becoming the first digital asset bank in U.S. history to directly access the Federal Reserve's payment infrastructure.

This historic breakthrough marks an important step for cryptocurrency-native companies and is finally a valuable "ticket" obtained by Kraken after over five years of effort.

Since submitting its application to the Kansas City Federal Reserve in October 2020, the process has undergone strict regulatory reviews, detailed communications, and comprehensive operational audits, ultimately receiving approval. This grant allows Kraken Financial to settle funds directly through the Federal Reserve’s core payment system, Fedwire, which processes over $40 trillion in fund flows daily.

Prior to this, cryptocurrency platforms like Kraken needed to conduct fiat transfers through intermediary banks, facing challenges such as high costs, long delays, and operational complexities. Now, with the Federal Reserve master account, Kraken will be able to settle directly like traditional banks, significantly improving transaction efficiency and reducing operational costs.

Kraken co-CEO Arjun Sethi stated, “With the master account from the Federal Reserve, we are no longer marginal participants in the banking industry, but a directly connected financial institution.”

However, while Kraken Financial has received the master account authorization, its account permissions are not entirely identical to those of traditional banks; rather, they are a streamlined version of the master account proposed by the Federal Reserve (Skinny Master Account). These accounts only provide basic payment service functions, and Kraken Financial cannot earn interest on reserves from the Federal Reserve, nor can it utilize emergency loans (i.e., discount window) from the Federal Reserve. Currently, this account model is still in a pilot phase, with the Federal Reserve Governor Waller recently disclosing plans to roll it out by the end of this year.

Initially, the authorization period for Kraken Financial's master account is one year, with related services being phased in, initially focusing on supporting activities for institutional clients on the platform. Institutional clients are one of Kraken's important growth engines, and the goal is for their revenue share to reach one-third. With the master account authorization, Kraken can provide these institutional clients with quicker and more efficient fiat fund transfers while significantly reducing operational complexity, costs, and reliance on intermediary banks, laying the groundwork for further expansion of institutional business.

Kraken Financial’s successful acquisition of this authorization is not only beneficial due to the relatively friendly regulatory environment in the U.S., but is also closely related to its designation as a Special Purpose Depository Institution (SPDI).

Arjun Sethi also acknowledged that SPDI created a unique and solid foundation that enables Kraken to settle directly on Fedwire, reducing dependency on correspondent banks and directly integrating regulated fiat liquidity into the digital asset market.

In fact, as early as the second half of 2020, Kraken announced that Wyoming had approved its application to become an SPDI, making it the first compliant bank in the U.S. able to offer clients cryptocurrency deposits, custodial, and trust services.

SPDI is an innovative banking license introduced by Wyoming in 2019, specifically targeting cryptocurrency and blockchain businesses, providing a legitimate channel for crypto firms to access the traditional financial system. The regulatory requirements for SPDI are quite stringent, including the need to hold highly liquid assets equal to 100% of customer fiat deposits, a prohibition on using customer deposits for lending, and requirements for sufficient capital and surplus funds. These strict conditions ensure the soundness and compliance of SPDI banks, enabling Kraken Financial to smoothly meet the Federal Reserve's master account requirements.

It is noteworthy that Kraken Financial's successful navigation through this process will also provide a demonstration effect for more crypto institutions, potentially attracting more companies to join the ranks of SPDI license applications in Wyoming.

Although the Federal Reserve master account permission obtained is still limited in scope, this advancement is undoubtedly an important step for crypto institutions entering the mainstream financial system. Over time, Kraken Financial plans to continue communicating with the Federal Reserve to seek more comprehensive permissions in the future and further expand service functions.

May trigger a wave of applications from crypto institutions, Wall Street is on alert

For an industry that has long been excluded from the traditional banking system, Kraken's approval for a master account from the Federal Reserve is undoubtedly a milestone. This not only opens the door to the mainstream financial market for Kraken but may also provide a model for other crypto platforms to follow.

Public data shows that several crypto companies, including Custodia Bank, Anchorage Digital, and Ripple, have applied for a master account with the Federal Reserve. As the Federal Reserve may open streamlined master accounts to more crypto companies in the future, the trend of applications from crypto institutions is expected to accelerate.

However, the Federal Reserve's shift in attitude has also raised concerns and opposition from the banking industry in the U.S.

The Bank Policy Institute (BPI), representing Wall Street giants like JPMorgan Chase, Bank of America, Wells Fargo, and Goldman Sachs, pointed out that the approval of Kraken has "deeply concerned" them, as it occurred before the Federal Reserve has definitively clarified the policy framework for the streamlined master account. BPI criticized the approval process for its lack of transparency and failure to detail mitigating measures for potential significant risks. Compared to traditional insured deposit-taking institutions, unregulated deposit institutions like SPDI pose greater risks to the payment system due to their weaker regulatory and supervisory intensity.

Rebeca Romero Rainey, president of the Independent Community Bankers of America (ICBA), also expressed similar concerns, pointing out that opening master account access to non-bank entities and crypto institutions grants traditionally heavily regulated privileges to these institutions, potentially posing risks to the banking system. The American Bankers Association (ABA) also criticized that this move bypasses regulatory rules, allowing crypto companies to "free ride" on the Federal Reserve's infrastructure without bearing equivalent regulatory burdens.

In fact, this opposition has existed since the Federal Reserve first proposed the concept of a streamlined master account. At the time, there were opinions that master accounts should be limited to insured, low-risk institutions to avoid unfair competition and systemic risk.

Now, with Kraken's approval, this controversy has once again been pushed into the public spotlight.

Regulatory green lights intensify the old and new competition, the era of big banks is fading

Currently, as U.S. regulatory agencies frequently "green light" crypto institutions, crypto payments are increasingly integrating into mainstream finance, leading to an intensifying struggle between traditional banks and crypto companies.

Recently, the Office of the Comptroller of the Currency (OCC) has continued to approve several crypto-related companies for national trust bank status, including Ripple, Circle, Crypto.com, Paxos, BitGo, Bridge, among others, and the Trump's family project WLFI also made related applications. The licenses granted to these companies allow them to offer financial activities like digital asset custody, stablecoin services, and staking under federal regulation. This trend not only signifies further integration of crypto business with traditional finance but also indicates that crypto payments are challenging the banking system.

In response to this trend, the U.S. banking lobby promptly urged the OCC to slow down the issuance of national trust bank licenses to crypto companies and emphasized that the GENIUS Act's regulatory framework has not been fully clarified, and the existing regulatory environment carries uncertainties, with unregulated digital asset trusts still facing unresolved risks regarding asset segregation, conflicts of interest, and cybersecurity.

It is noteworthy that Trump initiated a de-banking campaign at the end of last year that prompted the OCC to issue a new report. This report reviewed the nine largest national banks in the U.S., stating that during 2020 to 2023, these banks restricted certain industries from accessing banking services when formulating public and non-public policies, particularly placing higher entry thresholds for controversial or environmentally sensitive businesses. The OCC warned that these banks may face legal consequences. This action reflects that the U.S. government is attempting to create more development space for the crypto industry.

Meanwhile, the CLARITY Act being promoted in the U.S. Congress has become a focal point for the crypto industry, but due to conflicts of interest between banks and the crypto industry, it has stagnated at times. The controversial issue revolves around whether to allow stablecoin holders to earn interest or rewards. The banking industry believes such practices make stablecoins substitutes for deposits, attracting significant bank deposits, threatening the stability of community banking systems, and potentially triggering bank run risks. To protect their interests, banks have lobbied to include provisions in the CLARITY Act that prohibit stablecoin earnings. The crypto industry strongly opposes this, arguing that such practices are essentially bank protectionism, stifling innovation, limiting user choices, and undermining the dollar's position in global digital finance.

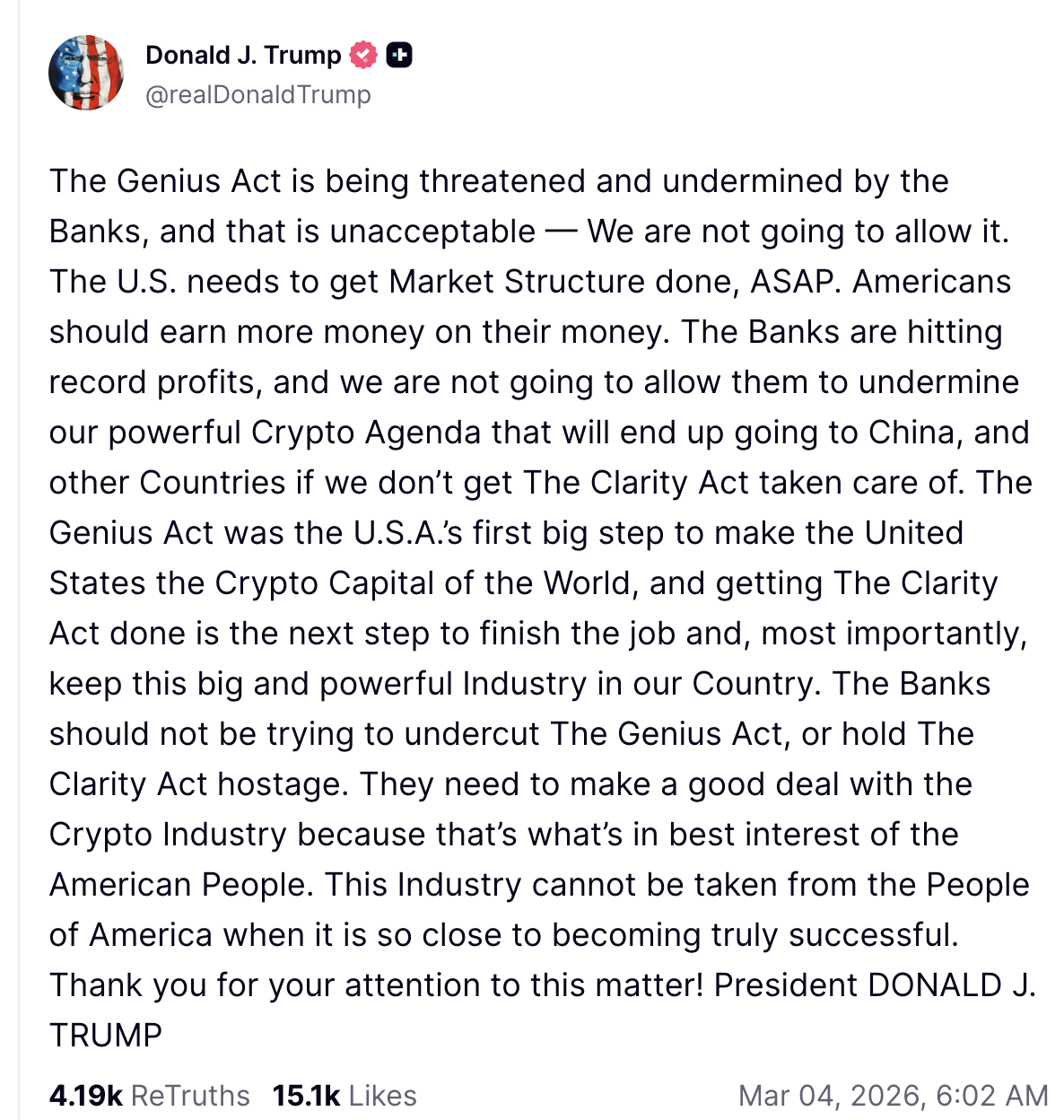

Both sides hold firm, neither willing to yield. Meanwhile, Trump posted on his social media platform Truth Social, strongly criticizing banking institutions for trying to undermine the GENIUS Act and obstruct the passage of the CLARITY Act. He stated that these acts are crucial for ensuring the U.S. becomes the "cryptocurrency capital" and warned that without action, the industry may shift to other countries. Trump urged banks and the cryptocurrency industry to reach an agreement, emphasizing it is in the best interest of the American people, and called for swift market structure reforms to allow "Americans to get more returns from their funds."

Currently, Mike Selig, chairman of the U.S. Commodity Futures Trading Commission (CFTC), has also expressed support for promoting the CLARITY Act, believing it is a key part of ensuring the U.S. maintains its leadership in global innovation. He emphasized, "Now is the time to take action," and is ready to implement the act during Trump's term. At the same time, Trump's decision to appoint Paul Atkins as chairman of the U.S. Securities and Exchange Commission (SEC) is also interpreted as a means to provide regulatory clarity for the crypto industry through executive action, as the SEC has the authority to establish necessary crypto industry rules without waiting for congressional legislation.

Trump's son, Eric Trump, also recently publicly criticized that large banks (such as JPMorgan Chase, Bank of America, and Wells Fargo) are rushing to lobby against providing Americans with higher savings yields while attempting to block any rewards or incentives for customers. The American Bankers Association and other lobbying groups have spent millions attempting to ban or limit these yields through legislation like the CLARITY Act while claiming to promote "fairness" and "stability," in reality, it is to protect their monopoly on low-interest rates and prevent deposit outflows.

As the regulatory environment becomes increasingly clear, crypto companies are moving from the margins to the mainstream, and the competition between them and traditional banks will only grow fiercer. As Eric Trump stated, as customers gradually awaken and realize more efficient asset return paths, the era of big banks profiting by relying on barriers is fading.

In the contest between new and old financial forces, driven by technological innovation and user demand, this financial power redistribution movement is undoubtedly heading toward a heated climax.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。