Author: Jae, PANews

On March 4, as the situation in the Middle East suddenly deteriorated, the global financial markets instantly entered a "wartime state." For global investors, this was a trading day that would go down in history.

The blockage of shipping in the Strait of Hormuz, a global energy chokepoint, triggered a significant surge in international oil prices, and panic quickly swept through traditional capital markets, with the Asia-Pacific stock markets facing an epic wave of sell-offs.

The South Korean KOSPI plummeted 12% in a single day, marking the largest drop in history; the Nikkei 225 fell sharply by 3.7%, recording its worst performance in five months; local stock markets in the Middle East experienced a nearly 5% dive during corrections; major stock indices in Europe and the United States all closed lower.

However, an unusual phenomenon quietly emerged amidst this sell-off.

The cryptocurrency market, typically regarded as "high-risk, high-volatility" and the first asset class to collapse during any geopolitical crisis, surprisingly held steady this time.

Bitcoin quickly rebounded after a brief panic sell-off, once surpassing $74,000, reaching a two-week high. On the very same day, Seoul investors witnessed the KOSPI fall through the circuit breaker line.

This is no longer a simple dichotomy of "safe-haven" versus "risk," but a deep reassessment of asset nature, pricing logic, and market structure.

Asia-Pacific stock markets become disaster zones, South Korean KOSPI plunges 12%

Following the outbreak of hostilities, global stock markets entered a "misery competition." The Asia-Pacific market, due to its high dependence on external energy, became the hardest hit.

The South Korean stock market suffered the worst.

The South Korean Composite Stock Price Index (KOSPI) closed down over 12%, marking the largest single-day drop in history. The day before (March 3), it had already declined by 7%. Over the two trading days, the cumulative drop approached 20%, evaporating approximately $430 billion in total market value, the most severe two-day consecutive decline since the 2008 global financial crisis.

The Korean KOSDAQ index fared even worse, plummeting 14% and triggering circuit breakers multiple times during the session.

Why Korea?

South Korea is the eighth-largest oil consumer in the world, with about 70% of its oil imports coming from the Middle East, and net oil imports accounting for 2.7% of GDP. The economic structure is primarily manufacturing-based and extremely sensitive to energy prices.

The closure of the Strait of Hormuz leading to soaring oil prices implies rising corporate costs, declining profit expectations, and heightened inflationary pressures. For this export-oriented economy, the missiles of the Middle East war are not distant news, but numbers directly impacting financial reports.

Even more lethal is the market structure. Foreign capital accounts for over 30% of positions in the South Korean stock market, and retail investors engage in leveraged trading amounting to nearly 80%. When panic strikes, foreign capital withdraws, leverage collapses, and quantitative stop-losses occur simultaneously, leading to a stampede sell-off.

Japan closely followed.

The Nikkei 225 index closed down 3.7%, marking the largest single-day drop in nearly five months; the Tokyo Stock Exchange index saw an even greater decline, closing down 4%.

Japan is also a major energy importer. Trump's statement about "potentially taking larger-scale military action against Iran" was enough to scare Tokyo traders.

The Middle East region, meanwhile, is in the eye of the storm.

The UAE stock market reopened after two days of closure, with the main indices in Dubai's financial market experiencing a drop of 4.7% in early trading, a rarely seen decline in recent years. The Saudi benchmark index plunged nearly 5% at the onset of the conflict. The Kuwait Stock Exchange even suspended trading to avoid a collapse-like sell-off.

For Gulf countries, war means uncertainty in oil revenues, stagnation in tourism and aviation sectors, and accelerated capital outflows.

The aftershocks of the Middle East conflict quickly transmitted to global financial markets, causing European and American stock markets to weaken collectively. Although the declines eased somewhat, major stock indices still ended lower.

Global stock markets continue to fall, cryptocurrency market rebounds "in a sprint"

While global stock markets were in disarray, the performance of the cryptocurrency market astonished many.

After the initial panic selling, Bitcoin quickly stabilized and rebounded, on March 5, surpassing $74,000 to reach a two-week high.

This divergence is not coincidental. It results from a combination of pricing efficiency, valuation misalignment, inflation risks, anchoring mechanisms, and participant structures.

When war broke out on the weekend, the cryptocurrency market was the only market that could trade.

No market closures, no circuit breakers, no delays. From the first explosion in Tehran, global investors could express their judgments in the cryptocurrency market.

This means that by the time the Asia-Pacific stock markets opened on Monday morning, the cryptocurrency market had completed several rounds of price discovery, having digested and priced in most risks in advance. Bitcoin's price fluctuation of "initial suppression followed by rise" is a reflection of this pricing efficiency.

At certain specific moments, the most sensitive cryptocurrency markets may be becoming leading indicators for all assets.

Moreover, before this "black swan" outbreak, the stock market and the cryptocurrency market were in different valuation cycles.

Major global stock markets continued to rise early this year, with the Nikkei 225 repeatedly hitting historic highs, the South Korean KOSPI at near five-year highs, and the three major US stock indices oscillating near historic peaks. Major global stock markets had accumulated a significant amount of profit, and valuation bubbles were building.

When a "black swan" occurs, profit-taking concentrates, and stop-loss orders flood in, resulting in a drastic decline.

In contrast, the cryptocurrency market has undergone several phases of deep corrections since October 2025. The valuations and leverage levels of mainstream assets have returned to reasonable ranges, and profit-taking has been fully realized, leading to early risk release.

When panic strikes, a market with bubble high leverage and a market with squeezed-out valuations react quite differently.

The macro risk variable brought by the Middle East war is inflation.

Soaring energy prices will increase inflation stickiness, forcing global central banks to delay interest rate cuts and even maintain high rates. For stocks, this represents a "valuation + profit" double whammy. Rate hikes suppress valuations, while cost pressures squeeze profits.

For Bitcoin, the logic of inflation is precisely the opposite. With a fixed total supply of 21 million coins, it is viewed as "digital gold" in an environment of excessive fiat currency issuance and high inflation.

Against the backdrop of geopolitical conflicts exacerbating fluctuations in fiat currency credibility, more and more investors are using it as a hedge against inflation and fiat currency devaluation.

Meanwhile, local capital in the Middle East is facing a triple dilemma of fiat currency devaluation, stock market crashes, and increased geopolitical risks. They need to find borderless, geographically unconstrained safe-haven assets, and cryptocurrencies have become one of the major flows. This incremental capital also offsets some of the risk-off selling pressure.

The pricing in the stock market anchors the real economy and corporate earnings, while the cryptocurrency market's pricing anchors global liquidity and decentralization attributes.

For export-oriented, energy-import-dependent economies like Japan and South Korea, the Middle East war directly impacts their economic fundamentals. The surge in crude oil prices raises production costs, and amid weak global demand, companies find it difficult to fully pass on these cost pressures, leading to a significant compression of profit margins.

In contrast, the devaluation of fiat currency and capital controls triggered by the Middle East conflict highlight the decentralized attributes of crypto assets, making them a viable option for global capital to hedge against geopolitical risks.

This is the fundamental reason for the divergent responses of the stock market and the cryptocurrency market to the same geopolitical risks.

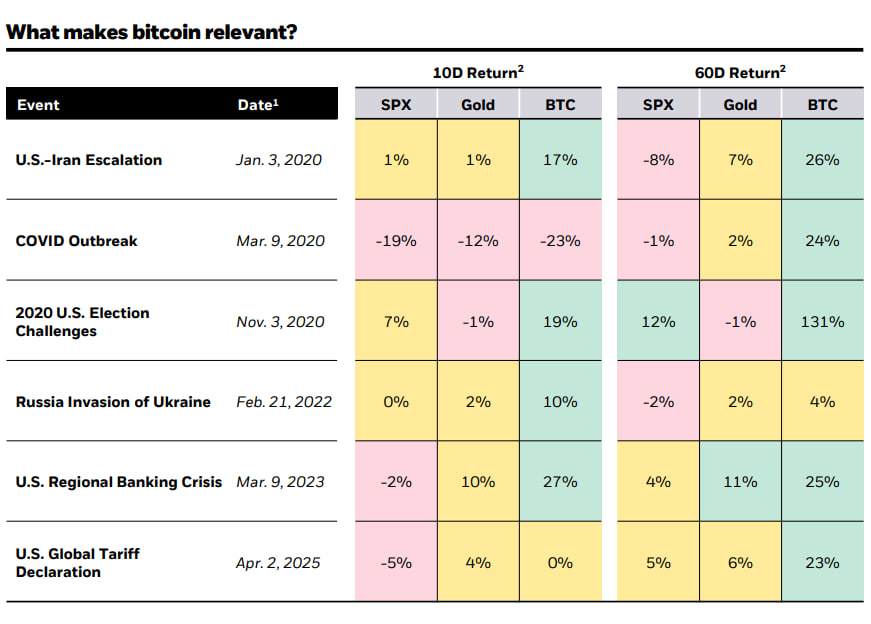

Research from BlackRock has pointed out that Bitcoin outperforms gold and stocks when facing geopolitical shocks. To date, this conclusion remains valid.

The structure of market participants determines volatility.

The dramatic drop in the South Korean stock market revealed its market structure's fragility: a high proportion of foreign capital, crowded leveraged trading, and dominance by algorithmic trading.

When panic hits, these three elements resonate, directly triggering a stampede and circuit breakers.

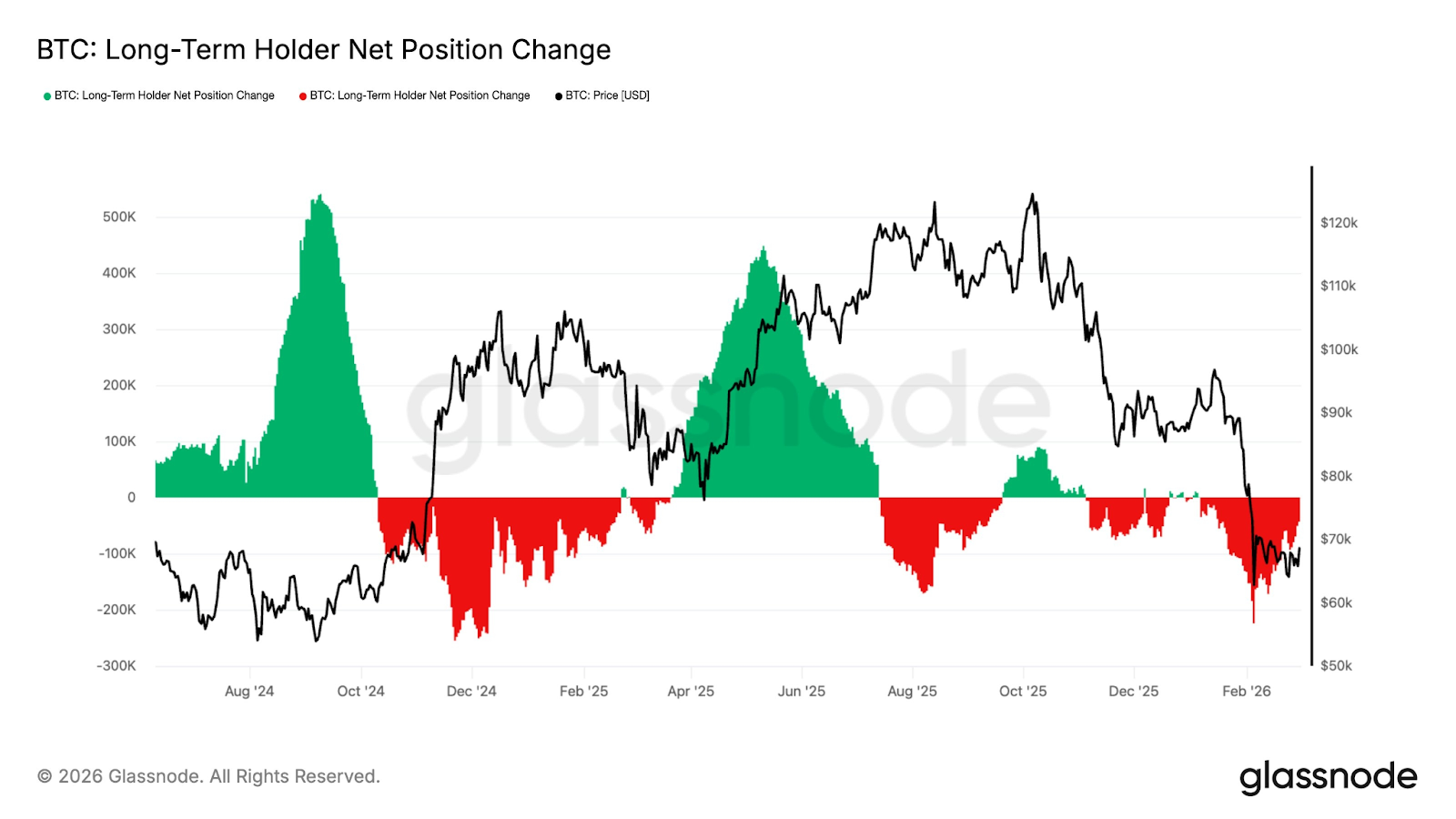

In contrast, the participant structure of the cryptocurrency market has undergone fundamental changes. Data from Glassnode indicates that the net position changes of long-term Bitcoin holders have tended to stabilize, suggesting a reduction in the intensity of sell-offs.

The US spot Bitcoin ETF has also brought stable institutional capital, transferring part of the pricing power into institutional hands, which typically possess more specialized risk management capabilities and long-term investment perspectives, forming underlying liquidity support.

More importantly, the cryptocurrency market had already completed multiple rounds of deleveraging before this "black swan" outbreak, and there were no large-scale chain liquidation events in the derivatives market, further reducing volatility.

War is a tragedy for humanity and a test of market resilience.

Yesterday's global sell-off taught all investors a lesson.

"High risk" is not necessarily truly high risk. While the cryptocurrency market stabilizes amidst volatility, the traditionally "relatively stable" stock market is experiencing plummeting and circuit breaker events.

Whether this is a temporary misalignment or a profound shift in logic and the rewriting of asset labels will require time to verify.

But in an era of normalized geopolitical risks, the anchor for asset pricing is shifting. Assets tethered to a single economy will become increasingly fragile, while assets anchored in global liquidity will grow ever more resilient.

The divergence between stock markets and the cryptocurrency market during this US-Iran war once again proves that crypto assets are gradually becoming an alternative medium that cannot be ignored in the global geopolitical game.

For many countries, the Middle East war is an unavoidable economic shock. For the cryptocurrency market, however, the same war serves as a confirmation of value logic.

When the storm comes, what matters is not where you stand, but what your anchor is tied to.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。