Author: Chloe, ChainCatcher

Opinion officially announced the token economics and roadmap of its native token OPN yesterday, while Binance also officially announced that Opinion will be the 72nd Launchpool project. According to the official roadmap, Opinion will conduct its Token Generation Event (TGE) in the first quarter of this year, with a focus on promoting ecological growth and decentralized governance in the second quarter.

However, the announcement did not receive widespread applause, as there are many data points that raised market doubts, complaints about the "anti-pullback" airdrop ratio, and criticisms regarding its "fast-track to Binance" approach.

Why now? The factors behind the shift from user growth to token issuance

In the global prediction market sector, Polymarket is undoubtedly the current acknowledged leader, but despite its high traffic during global elections and sporting events, it has not issued a token. With the demand for prediction markets reaching a peak this year, Opinion has jumped ahead to Binance, clearly intending to capture the spillover attention and liquidity from the prediction market boom initiated by PolyMarket, and also to establish a significant competitive advantage through user expectations of airdrops.

Additionally, for many retail investors, obtaining the endorsement of Binance for OPN has become the preferred gamble in this narrative. As the first prediction market token listed on a centralized exchange (CEX), the scarcity of OPN has ignited a spark of interest in today's cryptocurrency industry.

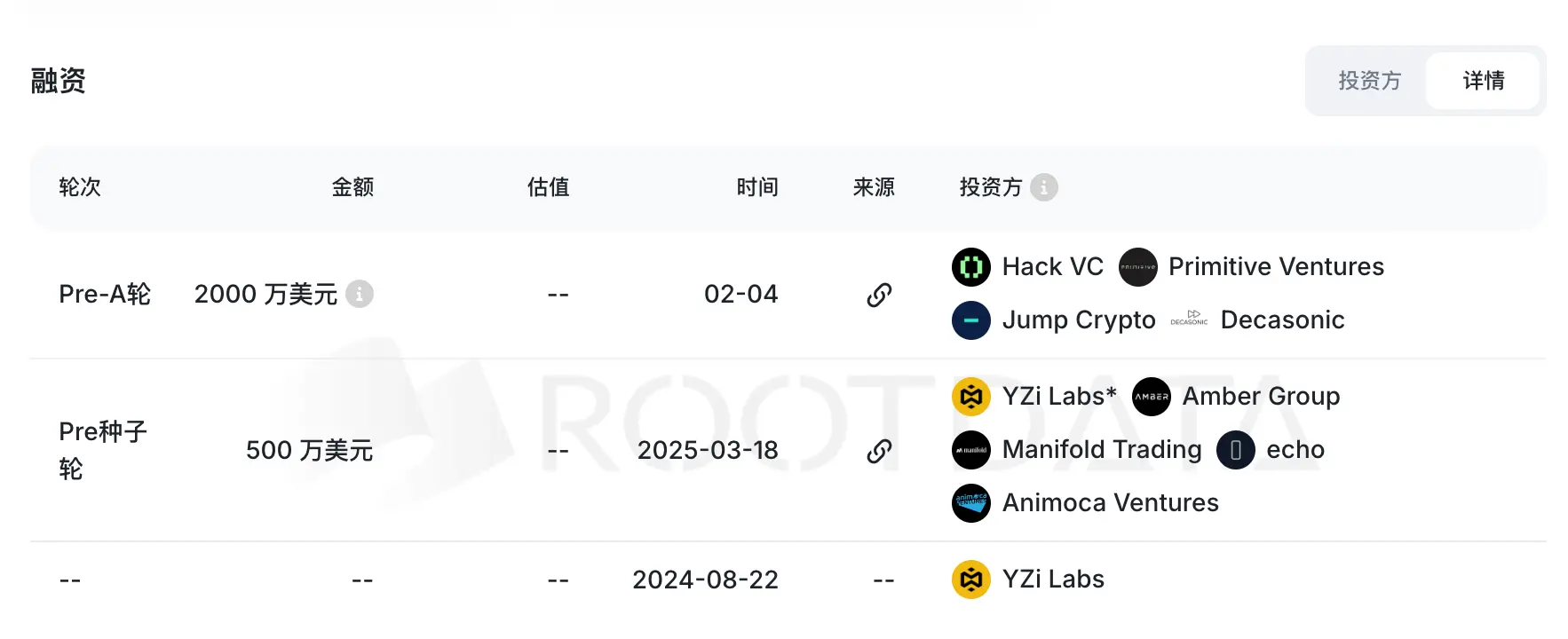

Moreover, according to RootData, on February 4, Opinion announced that it completed a $20 million Series A financing round, with participation from Hack VC, Jump Crypto, Primitive Ventures, Decasonic, among others. However, @cryptobraveHQ pointed out that insiders disclosed that the majority of the participating parties have refund rights or principal protection agreements, which is similar in nature to BeraChain's principal-protected financing, essentially being a "pricing round" or a "listing round."

According to interactions with VC同行 and listing personnel from the exchanges, the feedback generally indicates that it is a typical hype round, pricing round, or pay-to-list round. For VCs, instead of gambling on an unknown future, it is better to take advantage of the current peak of AI + prediction market narratives to achieve a streamlined exit.

Massive data questioned, huge discrepancies between transaction counts and transaction volumes

Perhaps in an attempt to become the “first project to issue a prediction market token,” Opinion's impressive data has raised market suspicions from the outset.

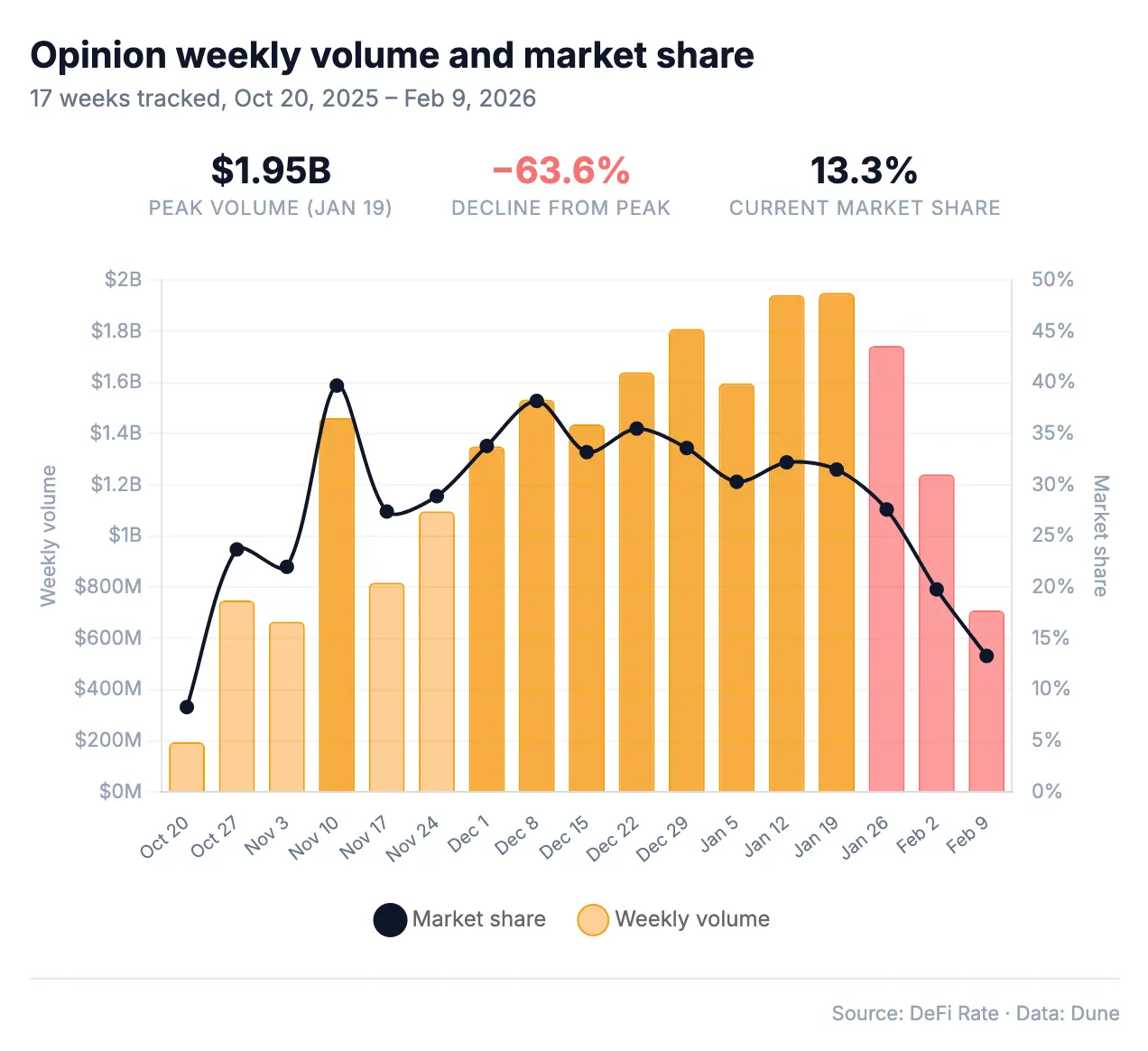

From Opinion's publicly available data, the trading volume for January 2026 reached $8.08 billion, accounting for 31% of the entire prediction market industry. A platform that only went live in October 2025 managed to exceed the trading volume of the well-established Kalshi and Polymarket within a few months, earning the title of “the fastest-expanding platform in the history of prediction markets.” In response, DeFiRate meticulously analyzed Dune Analytics' on-chain data over 17 weeks (from last October to this February) and discovered many anomalies that could not be explained by typical platform growth logic.

1. Huge discrepancies between transaction counts and transaction volumes:

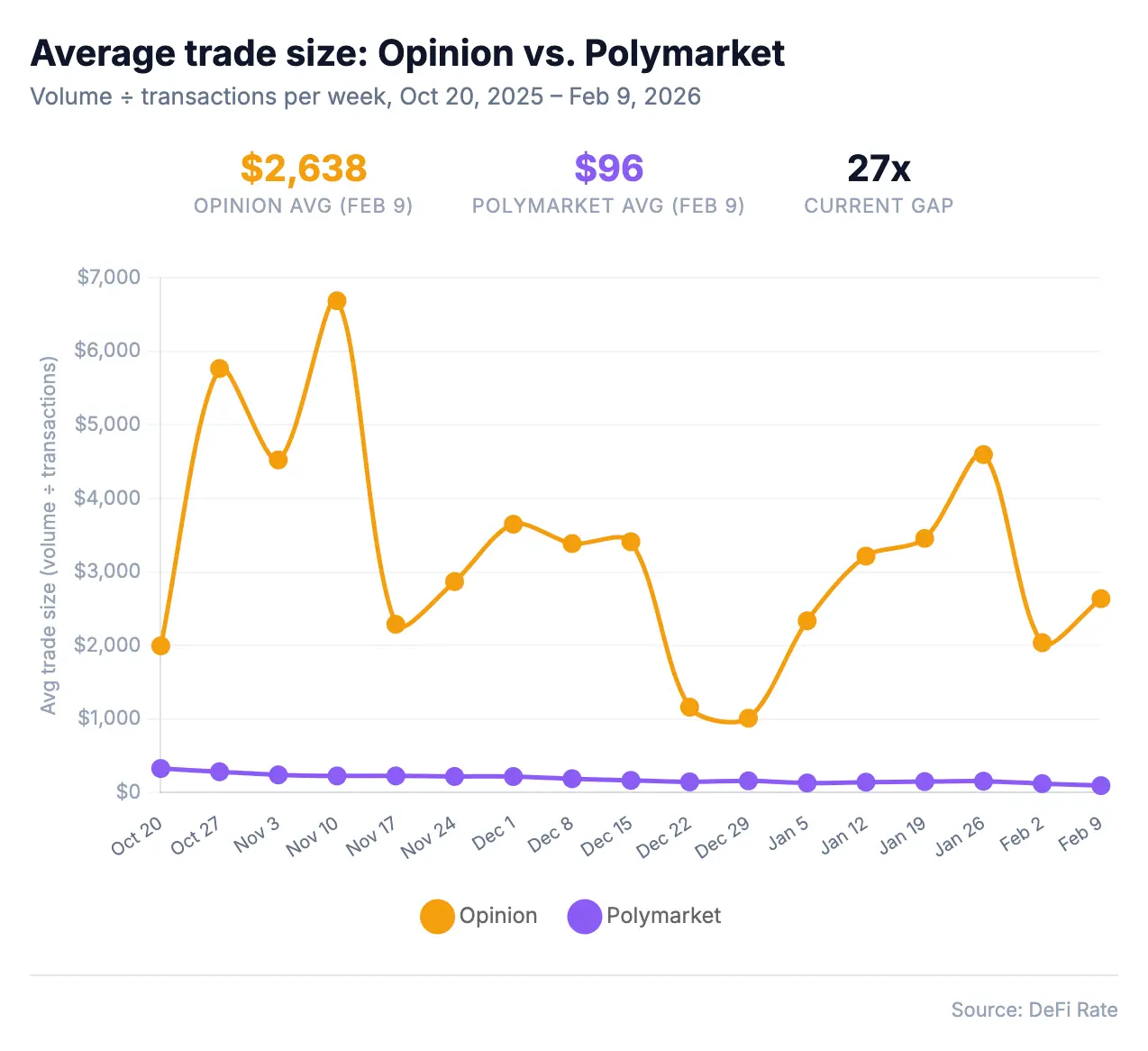

The core issue is not the size of the trading volume, but the ratio between trading volume and transaction counts. In January 2026, Opinion's $8.08 billion trading volume came from 3.2 million transactions, averaging about $2,525 per transaction. During the same period, Kalshi achieved $9.55 billion from 54.5 million transactions, averaging $175 per transaction; Polymarket generated $7.66 billion from 52 million transactions, averaging $147 per transaction. In simple terms, Opinion achieved 31% of the industry trading volume with less than 3% of the industry transaction counts.

This ratio has never normalized over consecutive weeks of data. The most extreme week was November 10: Opinion produced $1.46 billion in trading volume from 218,582 transactions, averaging $6,688 per transaction; during the same week, Polymarket produced $952 million from 4.19 million transactions, averaging $228 per transaction. Opinion's transaction counts were one-nineteenth that of Polymarket, yet its trading volume exceeded by 53%.

By February 9, Opinion accounted for 13.2% of the industry's trading volume but only contributed about 0.7% of the transaction counts; this 19:1 ratio has never been approached by any prediction platform.

2. Abnormal per capita trading volume: Are new users actually raising the platform's average trading volume?

The normal growth logic for platforms is that as the user base expands, the average trading volume decreases with the influx of new retail investors. However, Opinion's trajectory is precisely the opposite. According to DeFiRate data, when it launched in October, 20,534 users generated an average monthly trading volume of $38,537 per person; by January, the user base expanded to 101,954 people, and the average trading volume doubled to $79,241, with the platform's scale growing fivefold.

Typically, new users decrease the platform's average trading volume. Yet on Opinion, the trading volume from each batch of new users appears to be increasing? This starkly contrasts with the natural growth seen on platforms like Polymarket, where average trading volume per user gradually grows at a stable but slow rate (from $4,852/user in August to $11,817/user in January, with user counts increasing 2.9 times and trading volume growing 2.4 times).

3. Dramatic fluctuations in user numbers, only appearing normal during holidays?

The user base of Opinion itself represents another red flag. Within 17 weeks, the number of weekly active users surged from 11,124 to 67,913 and then plummeted back to 18,098, with a fluctuation range of 6 times. The period of greatest fluctuation occurred between February 2 and February 9: in just one week, the user count dropped from 67,804 to 18,098, a weekly decline of 73%. In contrast, during the 17 weeks, Polymarket's user base fluctuated only 1.5 times, showing a stable upward trend.

Interestingly, there is an anomalous return to normal values in the data: during the holiday period from December 22 to January 4. In these two weeks, Opinion’s transaction counts suddenly surged from the usual 300,000 to 600,000 to between 1.4 million and 1.8 million, while the average transaction size simultaneously dropped to between $1,000 and $1,163. This was the only instance where Opinion's data profile resembled that of a typical prediction market, but once the holidays ended, the data immediately reverted to its original anomalous state.

These anomalies did not arise without reason. Opinion's points system clearly states that trading volume is one of the weightings for obtaining points, explicitly encouraging users to place larger bets. Coupled with the airdrop expectations before TGE and a no KYC environment, a strong incentive to inflate volume was created.

It is worth noting that researchers at Columbia University estimated in November 2025 that about 25% of Polymarket's total trading volume over three years came from wash trading, with the sports market reaching as high as 45%, and Polymarket does not even have a points system or a clear method of calculating rewards based on trading volume. With Opinion's existing conditions, which reward large trades with points mechanisms, the incentive to inflate volume is significantly present.

Extremely low airdrop ratio, faced criticism from users for being anti-pullback

Additionally, the airdrop distribution announced yesterday sparked a strong backlash from the community. Although the officials claimed the total airdrop amounts to 23.5%, and the initial circulating supply at TGE is expected to be 19.85%, only 3.5% (approximately 8.2 million tokens) is unleashed initially, with the remainder released linearly over seven months. The rest is either insider trading or directly supplied to Binance.

Compared to Opinion’s high fees and complex point system, many users experienced months of real trading and high costs, only to receive a very meager allocation, leading a large number of deeply involved participants to declare that they were subjected to anti-pullback by the officials.

This ratio's implications reach far beyond just community sentiment. It also continuously affects the prediction market projects within the Binance ecosystem, as users watching PredictFun and Probable cannot help but question whether there is really any return expected from prediction markets within the Binance ecosystem?

Opinion's proactive listing should endorse the later comers in this sector, but the 3% airdrop ratio and data suspicions could very well deter potential users of PredictFun and Probable.

Lastly, it is undeniable that Opinion has technical innovations; traditional prediction markets require manual review and manually set settlement conditions to open a market, while Opinion utilizes AI oracles to accomplish this process almost instantaneously. This means it can cover scenarios far beyond just elections and sporting events; the changes in TVL of a DeFi protocol or the listing time of a token can all become a liquid prediction market within minutes.

Additionally, independent researcher Haotian also pointed out that even if Opinion's trading volume must contain significant wash trading for earning OPN points, “disregarding the wash trading, a platform where the user profile heavily includes institutions and arbitrageurs is actually indirectly validating the underlying infrastructure's capacity.”

“The future goal of prediction markets 2.0 is to allow large funds to engage in precise hedging in prediction markets just like they do in derivatives, rather than merely gambling on the retail level.”

It can be said that after the TGE, Opinion will face a brutal retention test: after the incentive for points is removed, how many people will be willing to stay and truly use this platform? Can the macro prediction market attract a sufficient scale of institutional users to support organic trading volume?

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。