Author: Zhongjin Insights

The military strike by the United States and Israel on Iran triggers global attention

According to Xinhua News Agency, on February 28, the United States and Israel jointly launched a "preemptive" military strike against Iran, which retaliated against multiple targets in Israel and the Middle East [1], further escalating the geopolitical situation in the Middle East. That evening, the Islamic Revolutionary Guard Corps of Iran announced a ban on any vessels passing through the Strait of Hormuz. The Strait of Hormuz is a crucial route for crude oil exports from oil-producing countries in the Middle East, accounting for about one-fifth of global oil transportation through this strait [2]. The rapid escalation of this conflict impacts global risk tolerance. This article briefly analyzes the potential impact on Chinese assets, particularly the A-share market, based on a review of the performance of major asset classes following 14 significant geopolitical conflicts since 2000, combined with the current global energy and trade background.

How have geopolitical conflicts historically affected equity market prices?

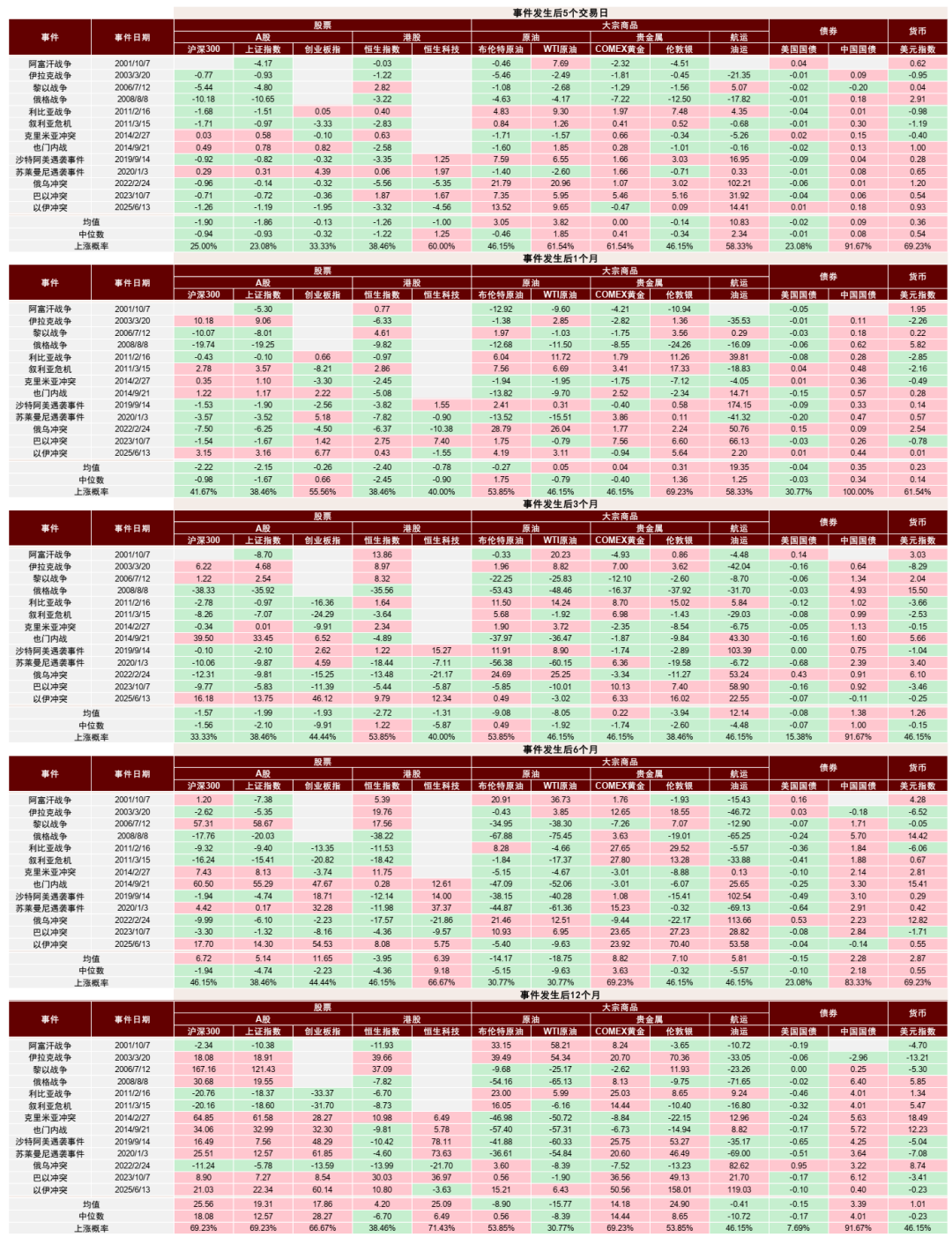

In the short term, the initial impact of geopolitical shocks on the stock market usually manifests as an emotional shock and a jump in risk premiums, reflected in rising volatility and capital reallocation. In an environment of significant uncertainty, capital tends to shift from equity assets to safe-haven assets such as gold and U.S. Treasury bonds; recent geopolitical conflicts have often been related to oil-producing countries, and energy prices, affected by supply shocks, tend to rise synchronously. The stock market faces cyclical downward pressure. Historical data shows that in the first week following the outbreak or escalation of a conflict, the median increase in WTI crude oil and COMEX gold prices is about 1.9% and 0.4%, respectively, with an upward probability of approximately 61.5%; during the same period, the median increase of the A-share CSI 300 and Shanghai Composite Index is about -1%, with upward probabilities of only 25% and 23%.

Chart: Historical performance of major asset classes after geopolitical military actions

Data Source: Wind, Research Department of Zhongjin Company

In the medium term, as uncertainty gradually dissipates, risk tolerance usually shows signs of recovery, with market focus returning to fundamentals and policy lines. After the retreat of emotional shocks, the subsequent factors affecting asset performance are the substantial changes brought about by geopolitical conflicts to global supply chains and macro environments. Taking recent conflicts in the Middle East as an example, events affecting the supply of oil-producing countries, key infrastructure, or strategic waterways (such as the Strait of Hormuz), cause crude oil prices and shipping costs to often spike rapidly. If supply disruptions are quickly repaired, the shock is typically limited to the short term; if disruptions persist, cascading reactions may occur. Specifically, 1) cost shocks and profit differentiation. China is a typical net energy importer, and rising energy prices put direct or indirect cost pressure on most domestic industries. Industries directly affected mainly include aviation transportation and shipping logistics, where fuel costs and freight charges erode profits; downstream enterprises in the petrochemical industry chain, such as basic chemicals, plastics, and chemical fibers, also face squeezed profit margins. If the impacts expand globally, they may also affect China's export demand. 2) The linkage effect between macro inflation and interest rates. High oil prices raise inflation expectations or may force major economies to adopt tighter policy options in interest rates and fiscal space. For example, if rising energy prices cause U.S. inflation data to rise again, the Federal Reserve's previous expectations for rate cuts may be disrupted, leading to an early end to the global liquidity easing cycle, which suppresses equity market performance.

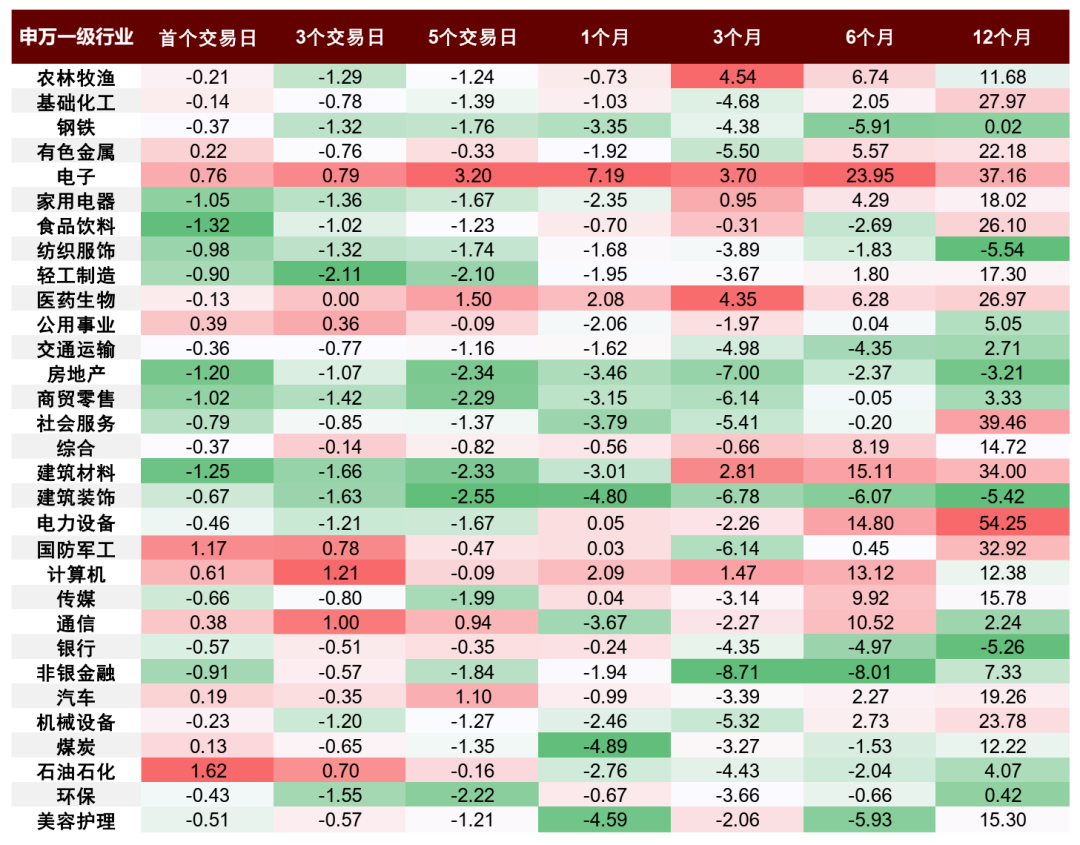

From an industry perspective, most sectors are influenced or have short-term adjustments due to emotions at the early stages of geopolitical conflicts, while sectors such as oil and petrochemicals, defense, and non-ferrous metals tend to resist downturns; medium to long-term impacts are very limited. In the short term, due to rising risk premiums and supply expectation disruptions, sectors such as oil and petrochemicals, defense, and non-ferrous metals often outperform and even achieve absolute gains; however, historical experience shows that this kind of excess performance is often characterized by phases. As emotional shocks fade and supply expectations are corrected, industry performance typically returns to fundamental lines, and the impact of geopolitical conflicts on long-term trends in our industries is limited.

Chart: Sector performance following the last four geopolitical conflicts in the Middle East

Note: Data represents the median price increases across various sectors following the last four geopolitical military conflicts in the Middle East (2019 Saudi Aramco attack, 2020 Soleimani attack, 2023 Gaza conflict, 2025 Israel-Iran conflict)

Data Source: Wind, Research Department of Zhongjin Company

How does the escalation of this conflict affect Chinese assets?

Chinese assets, including A-shares, may experience short-term risk tolerance disturbances but are expected to display relative resilience, without altering the mid-term positive trend. After the Spring Festival, the A-share market achieved a "good start," with trading volume significantly rebounding compared to the week before the holiday. Structurally, fueled by geopolitical concerns and expectations of policy reinforcement during the "Two Sessions," cyclical sectors supported by pricing logic in steel, non-ferrous metals, and chemicals led the gains; previously high-interest sectors such as AI applications have seen corrections. From the perspective of short-term driving factors, a relatively ample liquidity environment, marginal reduction in U.S. tariff disturbances, warming expectations in U.S.-China relations, profit recovery, and strengthening trends in the technology industry together support a moderate upward trajectory for the market. This round of escalation in the Middle East conflict requires attention, based on past patterns of Middle Eastern geopolitical events: a very short-term elevation of risk premiums, but A-shares may show relative resilience. Moving forward, it's important to monitor the scope and duration of the geopolitical conflict, the progress of the blockade in the Strait of Hormuz, changes in oil prices, and their impact on inflation. In the medium to long term, as pointed out in our report "A Share Market Outlook for 2026: Seizing the Momentum," the reconstruction of international order resonating with China's industrial innovation trend is the core driver of the current rise in A-shares and the re-evaluation of Chinese assets. We believe that the short-term shocks caused by the Middle Eastern conflict have not shaken the aforementioned mid-term logic. If changes in the geopolitical landscape further accelerate the reconstruction process of the international monetary order, it may actually strengthen the logic of re-evaluating Chinese assets. In addition, against the backdrop of continuous macro paradigm shifts and the ongoing reform of the capital market system, the underlying environment for A-shares is experiencing structural improvements. The evolution of market operating mechanisms and investor structures makes it more conducive to forming a "steady and progressive" pattern compared to the past; A-shares are still expected to continue a steady upward trend in the medium to long term.

In terms of asset allocation, in the short term, influenced by the geopolitical conflict, it is advisable to focus on the energy, non-ferrous, military, and oil transportation sectors, while high-dividend sectors may also show relative performance amidst rising risk sentiments; aviation and certain chemical sectors may be impacted by expected cost increases. In the medium term, attention should be given to the following areas: first, growth in prosperity, as AI is expected to gradually enter the industrial application stage, investments can be made around basic infrastructure aspects such as computing power, semiconductors, and cloud computing, as well as in applications like robotics and autonomous driving; areas like commercial aerospace and energy storage batteries are also entering a prosperous cycle; second, breakthroughs in external demand, as overseas expansion expectations have short-term impacts but remain a current certainty for growth opportunities, such as mechanical engineering, commercial buses, grid equipment, and relatively successful fields like gaming; third, opportunities for rising prices and performance improvements in non-ferrous metals and oil and gas resources affected by the geopolitical environment; fourth, high dividends, while it may be difficult to achieve excess returns in a growth-dominated environment, they still have good foundational value in a low interest rate context, with a positive outlook for the insurance sector in finance and companies with high free cash flow and consistent dividends in the non-financial sector.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。