The "Super Bowl" of earnings season has just concluded. Nvidia (NVDA) delivered a report that met expectations, yet its stock price during after-hours trading felt stuck at the critical psychological level of $200, unable to move significantly in either direction. Meanwhile, the VIX index, which measures market fear (also known as the "fear index"), saw its 1-day volatility spike after the earnings announcement far below many traders' expectations, subsequently plunging to around 9 at the market open. It feels like a highly anticipated concert where the lead singer performs steadily, but the audience remains unusually calm, with some even yawning.

Behind this calm, there may be brewing an important shift in market structure. After the most heavyweight "shoe" has dropped, the market's focus is shifting from the extreme performances of individual stocks to a more macro and monotonous theme: "Dispersion Unwind."

The Options Dilemma of "Buy the Expectation, Sell the Fact"

First, let's look at Nvidia itself. Ahead of the earnings report, market sentiment was exceptionally high, and the options market was particularly active. A lot of capital was betting on the stock price breaking through the $200-$205 range after the earnings announcement. However, reality is stark. After the earnings, the stock price hovered around $200, causing a rapid erosion in the value of many out-of-the-money options, especially the call options at $200 and $195.

I recall a similar scenario during the earnings season for tech stocks in 2023. At that time, a star company's earnings exceeded expectations, yet the stock price gapped up and then fell because of the reverse effect of option gamma squeeze—when the stock price fails to breach the critical strike price, market makers engage in selling operations to hedge, which in turn exacerbates the downward pressure on the stock price. The situation with Nvidia's options chain seems quite similar. When the most optimistic expectations are not met, the options market shifts from a "booster" to a "speed bump."

The Intermission After the Market's "Grand Play": The Arrival of Dispersion Convergence

Why does the entire market seem a bit "boring" after Nvidia's earnings? This may be because the main logic driving the market over the past period—the extreme divergence in individual stock performances—is nearing a turning point.

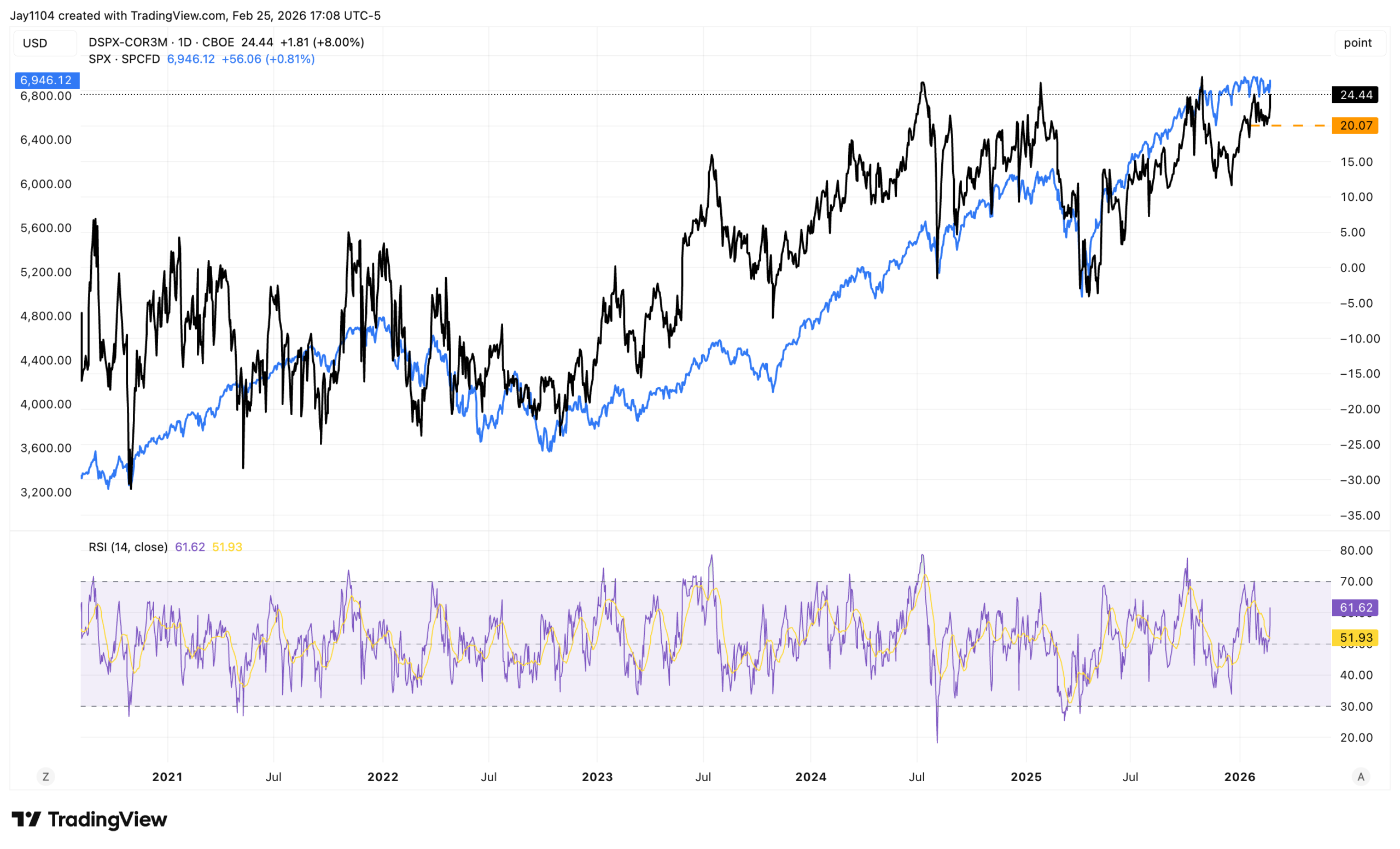

Dispersion, simply put, is the difference between the volatility of individual stocks and the overall market volatility. In the AI frenzy, we saw a few giants like Nvidia and AMD galloping ahead with severe volatility, while many other stocks performed blandly. This high-dispersion market is a paradise for active stock pickers and quantitative hedge funds. However, this state is unlikely to persist indefinitely.

A key observation indicator currently is the 3-month dispersion and correlation spread (DSPX-COR3M). When this spread is high, it means that stock movements are severely divergent (high dispersion), while the inter-stock correlation is low. Historical experience shows that this state tends to revert to the mean. In other words, the implied volatility of individual stocks will gradually converge with the market index's volatility, leading to a decrease in dispersion and an increase in the correlation between individual stocks.

To put it more plainly: the "star solo" may soon take a pause, and what follows might be "group singing" time. If dispersion begins to converge, the "long-short strategies" that have profited by going long on strong AI stocks and shorting weak stocks over the past few months may see a deteriorating environment for profits. Funds might re-evaluate sector rotation or return to trades that focus more on macro beta (the overall movement of the market).

Unmissable "Background Sound": Massive Treasury Settlements

As the market ponders a style switch, a technical factor is buzzing quietly in the background—a massive settlement of U.S. Treasury securities.

According to the published settlement schedule, approximately $137 billion in Treasuries will be settled over the next few trading days (including $22 billion on the day of the earnings report, $37 billion the following day, and so on). Although massive fund transfers do not directly represent outflows from the stock market, they can influence liquidity in the financial system in the short term, potentially exacerbating short-term market volatility. It’s like a swimming pool where water is simultaneously being drained and replenished; beneath the calm surface, strong currents are at play.

I recall during a "rebalancing week" at the end of a certain quarter last year, we encountered similar liquidity disturbances. At that time, U.S. stocks saw several days of low-volume declines at the close without any negative fundamentals, largely due to the joint effects of institutional rebalancing and bond settlements. For short-term traders, these dates represent additional "calendar risk" worth paying attention to.

What Will the Market Do Next?

Overall, Nvidia's earnings may signify a temporary adjustment of a micro driving force. The market needs new catalysts. These catalysts may come from:

- Further clarity on macro policies: The monetary policy paths of major global central banks, especially the Federal Reserve, will refocus attention. Any hints regarding the timing and pace of interest rate cuts could trigger a repricing of market styles.

- Validation of performance dispersion: The AI narrative cannot rely solely on Nvidia. The market needs to see more companies (whether tech giants or traditional industries) presenting concrete AI capital expenditure plans and revenue contributions during earnings calls to prove the breadth and depth of this wave.

- Self-fulfilling Dispersion Convergence: Once more and more investors begin to expect and trade on "dispersion convergence," the process itself will accelerate. Funds withdrawing from the crowded AI track to seek other valuation troughs may promote a healthy sector rotation.

For investors, current strategies may require some adjustments. Chasing after those single star stocks that are already fully priced and have overly crowded options presents changing risk-reward ratios. Instead, attention can be shifted to two aspects: one is sectors that might benefit from dispersion convergence (for example, cyclicals or financials that are more sensitive to macro conditions and have lagged previously); the second is to monitor changes in overall market volatility; if the VIX is at low levels, it may be a good time to purchase some "insurance" (such as index put options) for the portfolio.

The market will never stay at a peak indefinitely; a "calm period" like the present is a window to observe fund flows and adjust positions. After all, when the choir starts tuning, the next song is not far off. Of course, any judgment must consider real-time market dynamics, and being flexible at nodes of liquidity changes and style transitions is more important than sticking stubbornly to one view.

Related Read: A Comprehensive Analysis of Nvidia's 20-Year Rise: From Two Graphics Cards to a $50 Trillion Empire

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。