Written by: Charlie Little Sun

Hello everyone, today we are discussing a very important event from last week: the CLARITY Act, which the Senate Banking Committee was originally set to advance, was shelved on the eve of the markup and entered a pause for negotiations.

It made headlines and revealed many industry divisions that had previously gone unnoticed: Coinbase publicly clashed with most other players in the industry; the conflict between the crypto industry and the banking system, as well as traditional Wall Street interests, came to light; at the same time, an alternative route emerged within Congress—the Senate Agriculture Committee is preparing to advance its own market structure proposal, and their timeline is very fast.

What is the Clarity Act and its important development milestones

First, let's talk about what the CLARITY Act is. In a nutshell: it is a comprehensive framework for the digital asset market structure. It aims to answer questions such as: is a token considered a security or a commodity? Should it be regulated by the SEC or the CFTC? How should obligations related to brokerage, custody, disclosure, and investor protection on trading platforms be implemented?

The industry has been looking forward to it for a long time because, for many years, U.S. regulation has primarily relied on enforcement. For startups and public companies, whether new products can be developed and how far they can go often depends on guesswork. Everyone hopes to end this uncertainty with a set of clear rules.

On important milestones, the House version was passed last July with bipartisan support. In today's U.S. political environment, there are not many bills that can achieve consensus between the two parties, so the market had expectations for the Senate to continue advancing.

However, last year, the momentum was not capitalized on; on one hand, the government shutdown affected many project timelines; on the other hand, the banking system, after the legislative push related to stablecoins, became increasingly aware of a key issue: if stablecoins can provide yields, it will directly impact deposits and sources of funds.

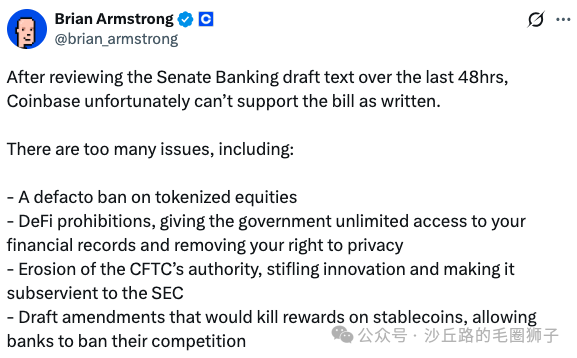

Last Monday evening, the Banking Committee introduced a revised draft, giving the industry only two or three days to analyze it before preparing to enter the markup session on Thursday. However, just a few hours before the markup was set to begin, Coinbase CEO Brian Armstrong publicly stated that Coinbase could not support this version, even saying, "I would rather have no bill than a bad bill." Ultimately, the markup was postponed; the bill is not dead but has entered a pause for negotiations.

Why Coinbase flipped at the last moment

Coinbase's "flip" or "threat to overturn the table" can be understood as their belief that the draft would lock in the future business space in three key areas.

The first is the de facto ban on stablecoin rewards/yields. Coinbase's concern is that this would kill the platform's ability to offer stablecoin yields and rewards to users. This is not just a minor feature; it is a crucial weapon for attracting new users, increasing balance retention, and enhancing user retention. Especially during market downturns, exchanges will rely heavily on this "balance-based, interest-based" income and product leverage.

The second is the "de facto ban" on tokenized equities. Coinbase argues that this is a de facto ban: while it does not explicitly state a prohibition, it sets the bar so high that it effectively prevents crypto-native platforms from participating. This is not a technical issue but a matter of control—who can legally become the entry point for "U.S. stocks on-chain" trading and distribution.

The third is the regulatory power tilt and DeFi penetration. Coinbase believes the draft expands SEC authority while weakening the CFTC, and that it forces some DeFi protocols into the compliance path of BSA/AML, which would impose unbearable compliance costs on many teams focused on coding and protocol development, stifling domestic DeFi innovation and productization in the U.S.

When you put these three points together, you can understand Coinbase's logic: they would rather delay negotiations to make these terms acceptable because they believe these terms will determine the space for the next decade, not just a compromise for the current quarter.

Crypto factionalization, the stance of the other side, and the legislative window before the midterm elections

Interestingly, the only company that has publicly come out strongly against the draft is Coinbase. However, there is another faction in the industry that is quite vocal and representative: Kraken, Chris Dixon from a16z crypto, Ripple, and David Sacks, who has significant political influence.

Their common point is not to say "the draft is perfect," but to emphasize a reality: there is a brief and rare legislative window right now. We have entered the election season, and the uncertainty of the upcoming midterm elections will narrow the significant legislative window. For them, an imperfect bill is better than the entire industry continuing to live in a regulatory vacuum and enforcement-based regulation.

This also reflects differences in business models.

Coinbase hopes the bill will strengthen its "everything exchange" narrative: all assets on-chain, all transactions completed in one account, while allowing the dollar balances on the platform to generate yields. In contrast, some other players care more about "legalizing first, getting a clear framework," so they can launch more products under the rules and promote broader institutional cooperation and market expansion.

Core reason one: Competing with banks for stablecoin yields (the deposit war)

Next, let's discuss the crux of the matter: the debate over stablecoin rewards/yields.

Why are banks so concerned? Because this is direct competition for deposits. If users can convert dollars into fully-reserved stablecoins and then earn nearly risk-free interest rates of 4%-5% on the platform, bank deposits will flow out, funding costs will change, and lending capacity will be affected. Furthermore, banks will emphasize systemic risk: if stablecoins experience a run, will the pressure be transmitted to the banking system and even the broader financial system?

I can also understand the banks' sensitivity to the term "run." When Silicon Valley Bank had its issues, my own startup's funds were also with SVB, and that weekend many people experienced several sleepless nights.

However, Coinbase's narrative is also very direct: stablecoin reserves are invested in short-term government bonds, which are essentially close to risk-free rates. Passing the yields on to users is market competition and does not inherently constitute systemic risk. Conversely, banks keep interest rates on demand deposits very low, making money through interest rate spreads, while also using legislation to eliminate competitors' interest rate weapons, which feels more like protectionism.

Thus, the real question behind the rewards debate is whether stablecoins in the U.S. will only serve as payment/transaction mediums or will become savings vehicles. It is redefining what a "dollar account" means.

For this reason, we see Armstrong in an interview with CNBC, on one hand, continuing to point fingers at banks, believing they should not suppress savings competition through regulation; on the other hand, he also expresses willingness and is currently communicating with bank CEOs, hoping to engage in more comprehensive discussions at Davos to reach some form of industry consensus.

Core reason two: Competing with Wall Street for dominance in RWA

The second point of contention is RWA, especially tokenized equities, or "U.S. stocks on-chain."

The key here is not "can tokenization happen," but "who can legally dominate this path in the U.S." Coinbase's concern is that certain language in the CLARITY Act could lock the secondary market trading path for tokenized securities within the traditional securities system—only allowing licenses to be issued through existing exchanges, brokers, and clearing systems.

For example, on Monday, the New York Stock Exchange announced a major initiative: to develop a platform for tokenized securities. This is very similar to the direction previously indicated by Nasdaq. This action itself is a statement: traditional exchanges want to bring tokenization into the securities compliance track, and they are more likely to obtain regulatory approval and connect with clearing and custody systems.

Adding to this is the phenomenon we see: traditional asset management institutions like BlackRock and Franklin Templeton are advancing tokenized money market funds, indicating that traditional Wall Street has organizational, systematic, and resource advantages in tokenization.

So will this be disadvantageous for consumer-facing, crypto-native companies like Coinbase or Robinhood in the future? One possibility is that with the home field advantage on Wall Street, their opportunities may become more about being distribution channels, custody, and settlement partners, rather than leading a new market structure. This would compress their imaginative space for "native product innovation."

Core reason three: Overregulation of DeFi could stifle innovative products

The third point of contention, which has received relatively little external discussion but is more fatal to the underlying nature of crypto, is the regulatory penetration of DeFi.

The logic of traditional financial compliance is that the responsible parties are clear: who does KYC? Who reports suspicious transactions? Who bears AML obligations? However, DeFi is often just a set of code, a decentralized governance structure, and may not even have a traditional operational entity. Who do you punish— the code, the developers, the initiators, or those providing the front end and entry points? This is vastly different from the logic of traditional institutions.

Coinbase's concern is that if certain DeFi protocols are forcibly included under BSA/AML obligations, it will push developers into a position of extremely high costs, even contrary to the underlying operational logic, stifling the legalization and productization of domestic DeFi in the U.S.

For Coinbase itself, this also directly impacts its "everything exchange" strategy—it is promoting a more open product line, including a more decentralized trading experience. If DeFi is subjected to excessive regulatory penetration, its new product line will face substantial constraints.

Possible future scenarios and their impact on COIN / HOOD / CRCL

Now let's conduct a scenario analysis.

Scenario one: The bill advances and passes in a more conservative version.

This would put the most pressure on Coinbase: the product capability of stablecoin rewards would be weakened, the imaginative space for tokenized equities would be compressed, and regulatory penetration of DeFi would burden its innovation path.

For Robinhood, the situation is more nuanced: a clearer framework would help it develop more products in compliance; at the same time, its cash interest payments come more from traditional partner banks, which may mean it faces less competition from crypto apps using stablecoin rates to attract users, potentially benefiting it in terms of competition.

For Circle, my intuition leans towards "bad news being fully priced in." Circle's distribution and market share are certainly important, but as a publicly traded company, if its revenue structure overly relies on interest rate-driven income, it essentially becomes a model that profits from interest rate spreads. Investors will price it like a bank, and its valuation imagination will be constrained. In the short term, reduced pressure to pass on benefits may lead to more stability; in the long term, being forced to accelerate revenue diversification and develop a more platform-based payment network and B2B infrastructure revenue may not necessarily be a bad thing.

Scenario two: A compromise is reached, forming a "win-win version."

For example, stablecoin rewards could be conditionally relaxed, tokenized equities could be given a more feasible path, and the responsibility chain for DeFi could be written more intelligently—this would advance regulatory clarity while not locking down key product spaces. This would be more positive for COIN, HOOD, and CRCL.

Scenario three: Talks break down, and legislation fails.

This would not be good for the industry, as everyone would continue to live under enforcement-based regulation, and all products would carry a discount due to compliance uncertainty. Moreover, it could benefit traditional Wall Street: asset management firms, exchanges, and investment banks would find it easier to lock the role of tokenization within the traditional system, shrinking the profit space for crypto-native players in RWA.

Alternative Senate Bill and Next Steps

Finally, let's talk about the alternative route emerging within Congress: the market structure draft from the Senate Agriculture Committee.

This line focuses more on the regulatory authority for the spot market of digital commodities, essentially establishing the CFTC's regulatory territory first, creating a smaller but actionable regulatory anchor, and then negotiating a more complex overall structure based on that. It is not a complete replacement for CLARITY but more like "putting together half of the puzzle first."

However, its timeline is indeed very fast: they stated that the legislative text would be released on January 21 and the committee markup would take place on January 27. This means there is not much time left for negotiations on CLARITY.

So my own judgment is that after the discussions in Davos this week, the market will see the next indicators more quickly. Whether CLARITY finds a compromise, or Senate Ag pushes forward a portion first, or whether one side takes a harder stance, we need to continue tracking. If the probabilities of these scenarios change, I will update everyone.

Alright, that's it for today. Feel free to leave comments and continue the discussion. Our written transcript will be released on our public account later. See you next time, bye!

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。