Author: Zhao Ying, Wall Street Insights

Bank of America Chief Investment Strategist Hartnett believes that Trump is driving global fiscal expansion, giving rise to the pattern of "New World Order = New World Bull Market." Within this framework, the bull market for gold and silver will continue, while the biggest risk currently lies in the rapid appreciation of the yen, won, and new Taiwan dollar, which could trigger a global liquidity tightening.

The yen is currently close to 160, nearing its historically weakest level, with the exchange rate against the renminbi hitting the lowest since 1992. Hartnett warns that if these extremely weak East Asian currencies experience rapid appreciation, it will lead to a reversal of capital outflows from Asia, threatening the liquidity environment of global markets.

In terms of asset allocation, Hartnett recommends going long on international stocks and "economic recovery" related assets, while maintaining a positive long-term outlook for gold. He believes China is his most favored market, as the end of deflation in China will act as a catalyst for bull markets in Japan and Europe.

Gold is expected to break through the historical high of $6,000, while small-cap and mid-cap stocks will benefit from policies of interest rate, tax, and tariff reductions. However, the sustainability of this optimistic outlook depends on whether the U.S. unemployment rate can remain low and whether Trump can improve his approval ratings by lowering the cost of living.

1. New World Order Fuels Global Bull Market

Assuming the yen will not collapse in the short term, Hartnett believes the market is entering the "New World Order = New World Bull Market" phase. Trump is driving global fiscal expansion, succeeding Biden's previous approach.

In this context, Hartnett suggests going long on international stocks, as the positioning of American exceptionalism is rebalancing globally. Data shows that U.S. stock funds saw inflows of $1.6 trillion in the 2020s, while global funds only saw inflows of $0.4 trillion, indicating a potential correction of this imbalance.

China is Hartnett's most favored market. He believes that the end of deflation in China will act as a catalyst for bull markets in Japan and Europe.

From a geopolitical perspective, the Tehran Stock Exchange has risen 65% since last August, while the markets in Saudi Arabia and Dubai remain stable, indicating that there will be no revolution in the region. This is good news for the market, as Iran accounts for 5% of global oil supply and 12% of oil reserves.

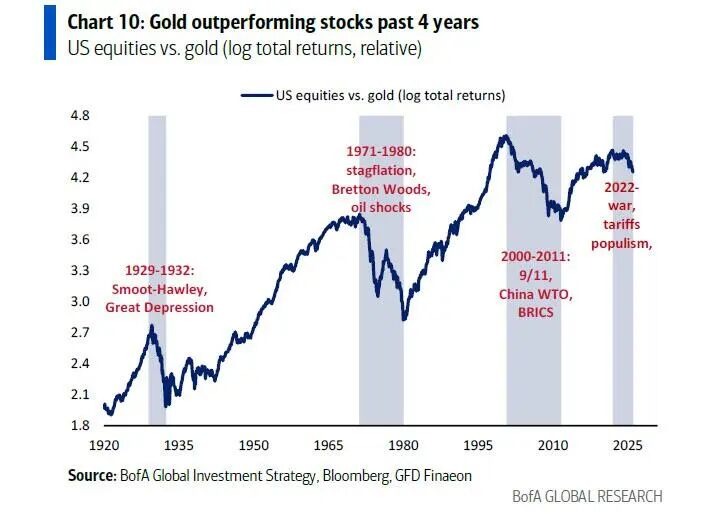

2. The Gold Bull Market is Far from Over

Hartnett emphasizes that the New World Order not only fuels a stock bull market but also a gold bull market.

Although gold, especially silver, is currently overbought in the short term—silver prices are 104% above the 200-day moving average, the highest level of overbought since 1980—the long-term logic for gold's rise remains valid.

Gold was the best-performing asset in 2020, driven by factors including war, populism, the end of globalization, excessive fiscal expansion, and debt devaluation.

The Federal Reserve and the Trump administration are expected to increase quantitative easing liquidity by $600 billion through the purchase of government bonds and mortgage-backed securities by 2026.

Over the past four years, gold has outperformed bonds and U.S. stocks, and there are no signs of this trend reversing. While overbought bull markets always experience strong corrections, a higher allocation ratio for gold still seems reasonable.

Currently, the gold allocation ratio for Bank of America’s high-net-worth clients is only 0.6%. Considering that the average increase in the four gold bull markets over the past century is about 300%, gold prices are expected to break through $6,000.

3. Small-Cap Stocks and Economic Recovery-Related Assets Benefit

In addition to gold, other assets are also benefiting in the new world bull market.

Hartnett believes that interest rate, tax, and tariff reductions, along with the "put option protection" provided by the Federal Reserve, the Trump administration, and Generation Z, are the reasons for the market's rotation to "devaluation" trades (such as gold and the Nikkei index) and "liquidity" trades (such as space and robotics) following the Fed's rate cut on October 29 and Trump's victory on November 4.

Hartnett recommends going long on "economic recovery" related assets, including mid-cap stocks, small-cap stocks, home builders, retail, and transportation sectors, while shorting large tech stocks until the following conditions occur:

First, the U.S. unemployment rate rises to 5%. This could be driven by companies cutting costs, the application of artificial intelligence, and immigration restrictions failing to prevent the unemployment rate from rising. Notably, the youth unemployment rate has risen from 4.5% to 8%, while Canadian immigration has significantly decreased, yet the unemployment rate has risen from 4.8% to 6.8% over the past three years. If tax cuts are saved rather than spent, it will be detrimental to cyclical sectors.

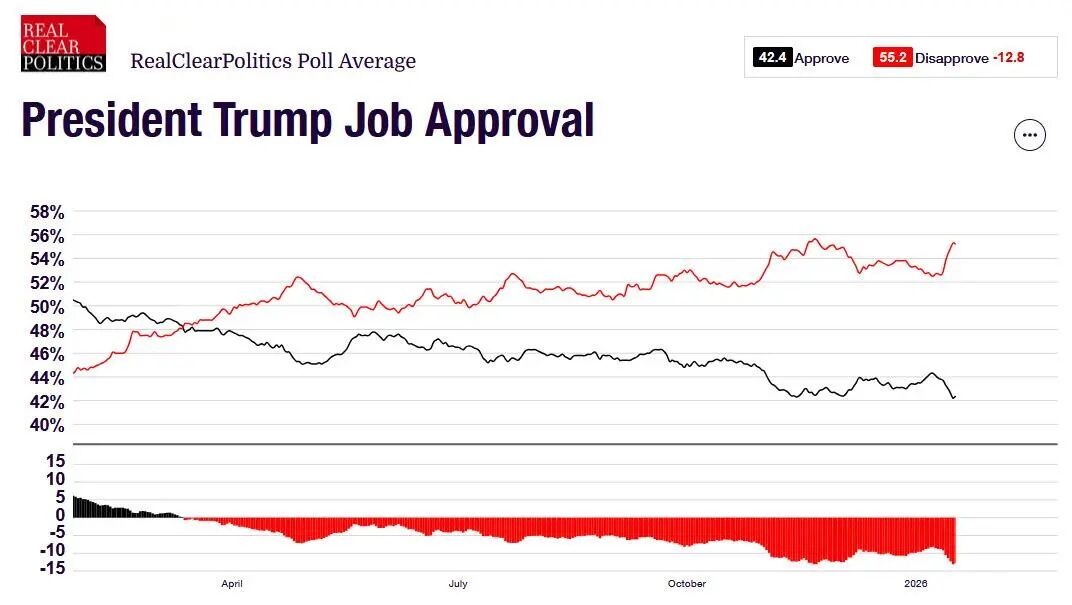

Second, Trump's policies fail to lower the cost of living through large-scale intervention. Main Street interest rates remain high, and if energy, insurance, healthcare, and electricity prices driven up by artificial intelligence do not decrease, Trump's low approval ratings will be hard to improve. Currently, Trump's overall approval rating is 42%, with economic policy approval at 41% and inflation policy approval at only 36%.

Historically, Nixon's freezing of prices and wages in August 1971 to improve living costs did work—Nixon's approval rating rose from 49% in August 1971 to 62% when he was re-elected in November 1972.

However, if Trump's approval ratings do not improve by the end of the first quarter, the risks of the midterm elections will rise, making it more difficult for investors to continue going long on "Trump prosperity" cyclical assets.

4. Appreciation of East Asian Currencies Poses the Biggest Risk

Hartnett points out that the current market consensus for the first quarter is extremely bullish, while the biggest risk comes from the rapid appreciation of the yen, won, and new Taiwan dollar. The yen is currently trading near 160, at its weakest position against the renminbi since 1992.

The rapid appreciation of these currencies could be triggered by factors such as interest rate hikes by the Bank of Japan, U.S. quantitative easing, geopolitical tensions between Japan and China, or hedging errors.

If this occurs, it will trigger a global liquidity tightening, as the capital flowing into the U.S., Europe, and emerging markets to recover the $1.2 trillion current account surplus from Asian countries will reverse.

Hartnett's warning signal is the risk-averse combination of "yen appreciation and rising MOVE index." Investors need to closely monitor this indicator to determine when to exit the market.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。