Author: Brian, Guatian Laboratory W Labs

(Continuing from Part One) "The Storm of RWA in Hong Kong (Part One): From Frenzy to Reconstruction, Analysis of the Strength of Nine Major Factions"

7. AlloyX — The "Hybrid Aggregator" Connecting DeFi Liquidity and Real-World Assets

In the grand narrative of RWA in Hong Kong, if HashKey and OSL are building "heavy asset" infrastructures akin to Nasdaq or bank vaults, then AlloyX represents another agile force in the RWA market — the "DeFi Native Aggregator."

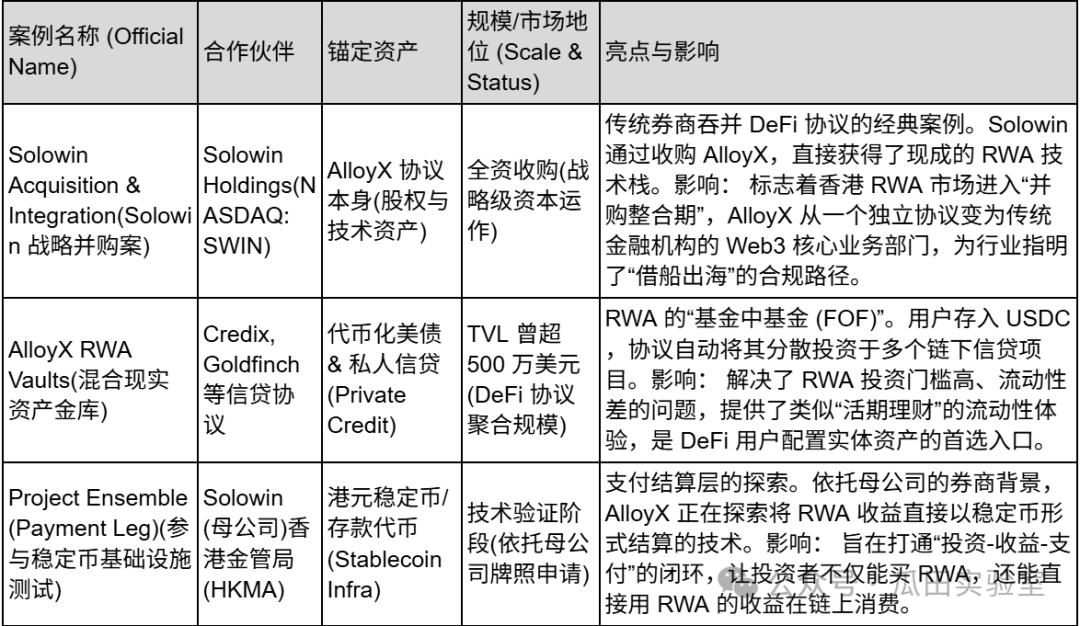

Originating from San Francisco, USA, and later fully acquired by the Hong Kong-listed brokerage Solowin Holdings (NASDAQ: SWIN), AlloyX plays a unique role in the Hong Kong RWA landscape as a "CeDeFi (Centralized and Decentralized Hybrid Finance Connector)." It does not directly hold heavy physical assets but instead uses smart contract technology to "package" credit assets scattered across different chains and protocols into highly liquid financial products, directly delivering them to investors in the crypto world.

AlloyX's business logic is fundamentally different from traditional exchanges. It is essentially an Aggregator Protocol for RWA assets.

In the early RWA market, assets were fragmented: investors wanting to buy U.S. Treasuries might have to go to one platform, while those looking to invest in private credit would need another, with extremely high thresholds. The emergence of AlloyX addresses this pain point. It has built a modular "Vault" system that can connect to multiple upstream credit protocols such as Centrifuge, Goldfinch, and Credix. By standardizing these into unified tokenized products, AlloyX allows users to easily allocate stablecoins like USDC into real-world credit assets, much like depositing into a money market fund.

With its official integration into Solowin Holdings in 2025, AlloyX has completed a stunning transformation from a "pure DeFi protocol" to a "compliant fintech flagship." Today, AlloyX resembles a tentacle of Solowin, a traditional brokerage, reaching into the Web3 world, leveraging Hong Kong's regulatory license advantages to distribute traditional securities, funds, and other assets through AlloyX's technological pipeline in token form to global investors, achieving true "Asset rights in the traditional world, liquidity released in the blockchain world."

In the fiercely competitive Hong Kong market, AlloyX's moat primarily lies in the unique combination of its shareholder background and technological architecture.

First, the endorsement and resource injection from a listed company is its greatest differentiating advantage. As a wholly-owned subsidiary of Nasdaq-listed Solowin, AlloyX has stepped out of the compliance dilemmas faced by ordinary DeFi projects. It can directly utilize the resources of the Hong Kong Securities and Futures Commission (SFC) Class 1, 4, and 9 licenses held by its parent company to legally design and distribute tokenized products involving securities. This "front-end DeFi experience + back-end licensed brokerage risk control" model perfectly aligns with the CeDeFi regulatory direction promoted in Hong Kong.

Secondly, AlloyX possesses strong "composability" technical capabilities. Unlike single asset issuers, AlloyX excels at algorithmically mixing and packaging RWA assets of different risk levels (such as low-risk U.S. Treasuries and high-risk trade finance) to create on-chain products similar to structured notes. This capability allows institutional investors to customize RWA investment portfolios on-chain according to their risk preferences, greatly enriching the profit strategies in the RWA market.

AlloyX's business practices mainly focus on "asset aggregation" and "compliant issuance," with the following being its most representative business cases:

Looking back at AlloyX's development path, we can clearly see that it does not pursue a large and comprehensive platform traffic but instead focuses on refined operations on the asset side. Through Solowin's acquisition, AlloyX has effectively become the "technical engine" for traditional financial institutions to undergo digital transformation in RWA. For the market, AlloyX has proven that RWA is not just a game for giants; technical protocols can also find a core ecological niche within the high walls of compliance through deep binding with licensed institutions.

8. Asseto — The RWA "Asset Packaging Factory" Built for Institutions

In the Hong Kong RWA industry chain, Asseto plays a key role as the "source of assets." It is positioned at the very top of the industry chain, directly connecting with the real economy.

As the flagship RWA infrastructure project strategically invested by HashKey Group, Asseto boasts a strong "noble lineage." It does not deal directly with retail investors but focuses on solving the most challenging "first-mile" problem of RWA: how to "transform" a building or a fund into a compliant token from legal structure, technical standards, and compliance processes?

Asseto's business model is highly vertical and has high barriers to entry, primarily serving TradFi giants with billions in assets:

RWA Asset Issuance Gateway: Asseto provides a standardized technology stack that allows institutions to "one-click" put cash management products, real estate, private credit, and other assets on-chain. It not only offers smart contracts but, more importantly, provides "legal packaging" services to ensure that the tokens on-chain have real claims to the underlying assets under Hong Kong law.

Asset Conveyor Belt of the HashKey Ecosystem: As a portfolio company of HashKey, Asseto is an important source of potential RWA assets for HashKey Exchange. Asseto is responsible for organizing assets off-chain (cleaning, rights confirmation, tokenization) and then distributing them to secondary market investors through HashKey's compliance channels.

Application Scenario Provider for Stablecoin Sandbox: Asseto collaborates closely with several institutions applying for Hong Kong stablecoin licenses, aiming to use RWA assets as reserve assets for stablecoins and exploring high-end strategies like "issuing stablecoins with tokenized government bonds/cash."

Asseto's core advantage in the Hong Kong market lies in the top-tier resources brought by its shareholder structure:

HashKey's technical and channel support: HashKey not only provides funding but also opens up HashKey Chain (L2 public chain) to Asseto as the preferred issuance platform. This means that the assets issued by Asseto inherently possess the largest compliant liquidity exit in Hong Kong.

Asset injection from DL Holdings: Hong Kong main board-listed company DL Holdings (1709.HK) has not only invested in Asseto but also signed a strategic agreement to plan to tokenize its managed family office assets (such as commercial real estate, fund shares) through Asseto. This addresses the most pressing "asset scarcity" issue faced by RWA projects — Asseto started with high-quality assets from a listed company.

The case of Asseto is highly "institutionally customized," primarily revolving around real estate and cash management:

Asseto is the "asset alchemist" of the Hong Kong RWA market. It does not directly shout to retail investors but hides behind the scenes, using precise legal and technical molds to melt down the large and cumbersome assets of traditional financial institutions into gold coins suitable for circulation in the Web3 world.

9. FireX — The "Industrial-Grade" RWA Platform for Releasing Computing Power Liquidity

In the Hong Kong RWA market, the vast majority of platforms deal with "paper assets" (such as bonds and equities), while FireX focuses on "productive assets."

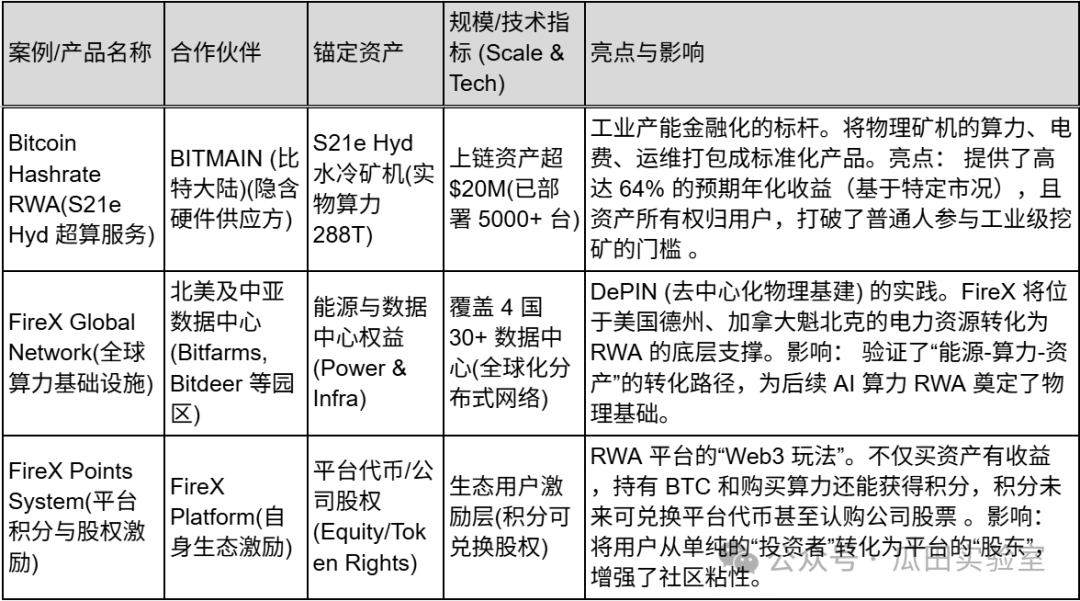

FireX is an institutional-level RWA trading platform, with its core narrative centered on "financializing the source production capacity (computing power) of Bitcoin." By collaborating with top infrastructure providers like Bitmain, it encapsulates data centers and mining entities located globally (in the U.S., Canada, Kazakhstan, etc.) into on-chain tradable RWA tokens. For investors, purchasing FireX's RWA products essentially means acquiring the "future cash flow rights" of a running supercomputer.

FireX's business logic is very vertical; it addresses the mismatch between traditional mining's "poor liquidity" and Web3 funding's "lack of stable physical returns":

Assetization of Computing Power: FireX transforms the "S21e Hyd mining machine" and its generated computing power (288 TH/s), which originally belonged only to the physical world, into on-chain assets. This means users do not need to build their own mining farms or maintain machines to hold computing power and earn Bitcoin mining rewards.

Global Energy Arbitrage Network: FireX is not just a trading platform; it is backed by a vast network of physical infrastructure. It owns or collaborates with over 30 data centers in locations like Texas, Canada, and Ethiopia. It is essentially engaging in global energy arbitrage — seeking the cheapest electricity, converting it into Bitcoin, and then distributing the profits through RWA.

Diverse Asset Allocation Entry: In addition to core Bitcoin computing power, FireX's vision also includes RWA-izing global quality stocks (like NVDA, MSFT), Pre-IPO equities, and AI computing power assets. It aims to create a comprehensive asset allocation basket that encompasses both the digital and physical worlds.

Unlike pure software protocols, FireX's moat is built on heavy "hardware" and "ecological relationships":

Verifiable Physical Scale: FireX has currently deployed over 5,000 supercomputing servers, managing computing power exceeding 1,000 PH/s, with on-chain assets valued at over $20 million. This "tangible and visible" physical scale provides the most fundamental credit endorsement for RWA — ownership belongs to the clients, and the assets operate genuinely.

Top-tier Ecological Network: According to disclosures, FireX's partner network includes mining giants BITMAIN, mining pool Antpool, and leading institutions such as Binance, Coinbase, and Tether. This resource integration capability that spans the entire industry chain of "mining machine production - mining - exchanges - stablecoins" ensures the stability and low-cost advantages of its asset supply (such as zero machine fees and zero service fees).

High Yield Expectation Product Design: During the Bitcoin bull market cycle, FireX's computing power RWA demonstrates extremely high yield elasticity. According to calculations for its S21e Hyd product, under the optimistic assumption that Bitcoin prices reach $150,000, the ROI (Return on Investment) could even approach 100%. This is more attractive than traditional government bond RWAs.

FireX's business is extremely focused on "financializing computing power" and "global asset allocation":

FireX is the "hardcore industrial faction" in the RWA track. It moves beyond the simple "old wine in new bottles" model of traditional financial assets (like government bonds) and instead provides a foundational income layer supported by the real sounds of machines and energy consumption through the "securitization packaging" of Bitcoin computing power, a native digital asset.

Bipolar Narrative: Deep Benchmarking of Hong Kong and U.S. RWA Markets

If 2024 is the year of concept validation for RWA, then 2025 will be the year of "bipolarization" in the global RWA market landscape. In the global RWA map, the U.S. and Hong Kong represent two distinctly different yet mirror-like evolutionary paths.

The U.S. relies on its native DeFi innovation and dollar hegemony to become the "super factory" of RWA assets; meanwhile, Hong Kong, leveraging its unique institutional advantages and geopolitical positioning, has become the "super boutique" and "distribution hub" for RWA assets.

1. Regulatory Philosophy: "Enforcement-driven Tolerance" vs. "Sandbox-style Access"

U.S.: Bottom-up Jungle Rules

The U.S. RWA market has grown wildly in the cracks of regulation. Although the regulatory environment softened after the Trump administration took office in 2025, its core logic remains a game of "Regulation by Enforcement" and "DeFi First."

Characteristics: U.S. projects (like Ondo, Centrifuge) often start as DAOs or decentralized protocols, initially pursuing scale and technological innovation, then using complex legal structures (like SPV offshore isolation) to evade SEC's securities classification.

Advantages: Innovation is rapid, allowing asset combinations to be realized through smart contracts without license approval, easily giving rise to phenomenon-level products with strong scale effects like BlackRock BUIDL.

Disadvantages: There is significant legal gray area; once cross-border distribution or non-qualified investors (retail) are involved, there is a high compliance risk.

Hong Kong: Top-down Design

Hong Kong has taken a completely opposite path — "Licensing Regime." From obtaining exchange licenses from HashKey to Star Road (Star Road Technology) relying on the 1, 4, and 9 licenses held by Fosun Wealth, every step of Hong Kong RWA is within the visible range of the SFC and HKMA.

Characteristics: "No license, no RWA." All projects (like OSL, HashKey) must operate within the Project Ensemble sandbox or existing securities framework. Regulators are not only referees but also "product managers" (like guiding the design of tokenized deposits).

Advantages: Extremely high certainty. Once a product is approved (like the tokenized products from Huaxia Fund), it can legally connect to the banking system and retail funds, possessing the trust endorsement of traditional financial institutions.

Disadvantages: High entry barriers and compliance costs (over $800,000 per project) suppress grassroots innovation, leading to market participants mostly being "noble families" or "consortia."

2. Market Structure: "Fundamentalist DeFi" vs. "Traditional Consortium"

U.S.: The Home of DeFi Native Capital

The market structure of the U.S. RWA is "DeFi downward compatible with TradFi." The main funding sources come from on-chain USDC/USDT whales, DAO treasuries, and crypto hedge funds. Project teams are usually led by tech geeks who disdain cumbersome offline processes, aiming to turn everything (including government bonds) into ERC-20 tokens and then deposit them into Uniswap or Aave for collateralized lending.

- Typical Profile: Protocols like MakerDAO or Compound purchase U.S. Treasuries through RWA modules to provide yield support for stablecoins.

Hong Kong: Digital Transformation of Traditional Consortiums

The market structure of Hong Kong's RWA is "TradFi upward adapting to Web3." The main funding sources come from family offices, high-net-worth individuals (HNWI), and enterprises seeking diversification in financial management. Project teams often have deep industrial backgrounds (like the mining power resources behind FireX, the industrial capital behind Star Road, and the real estate funds behind Asseto).

- Typical Profile: The "Web5" strategy proposed by Star Road Technology is the most typical — utilizing Web3 technology to serve existing Web2 customers. Hong Kong RWA is not about creating new assets but about making "old money" feel trendy and secure.

3. Asset and Project Spectrum: "Standardized Treasuries" vs. "Non-standard Structured Assets"

U.S.: The Unilateral Hegemony of U.S. Treasuries

About 80% of the TVL in the U.S. RWA market is concentrated in "tokenized U.S. Treasuries." This is the most standardized, liquid, and easily accepted collateral by DeFi protocols. Most U.S. RWA projects operate on roll rates and T+0 settlements.

Hong Kong: A Testing Ground for Diverse Assets

Limited by market size, Hong Kong cannot compete with the U.S. purely on the U.S. Treasury track, thus moving towards "differentiation" and "physicalization."

Physical and Industrial RWA: FireX packages Bitcoin computing power and energy into RWA, a unique "hardcore industrial" innovation in Hong Kong that leverages Asia's advantages in the global mining supply chain.

Real Estate and Alternative Assets: Mantra (though headquartered in Dubai, it focuses on Asia) and Asseto specialize in structuring non-standard assets like real estate and private credit. Hong Kong is better at handling complex offline rights confirmation (like the assets managed by Star Road).

Infrastructure: OSL and HashKey are not just dealing with assets; they are building a complete infrastructure of "exchanges + custody + SaaS," reflecting Hong Kong's service provider gene as a financial center.

Recommendations for Mainland Assets and Enterprises Issuing RWA in Hong Kong

Given the recent layers of regulatory tightening, for enterprises with a mainland background (shareholders, teams, operating entities), the window for issuing RWA through the "Mainland Assets/Team + Hong Kong Shell" model has essentially closed. This is not just an issue of increased compliance difficulty but a shift from a "gray area" to a "high-risk criminal involvement."

On November 28, 2025, in a meeting of 13 departments including the central bank, it was clearly stated that stablecoins are virtual currencies and do not possess legal compensation, and related businesses are considered illegal financial activities. This essentially cuts off the most critical "payment settlement" leg of RWA. RWA yields are typically settled in stablecoins (USDT/USDC), which have been classified as illegal. On December 5, 2025, seven major industry associations issued risk warnings, explicitly listing RWA financing as illegal activities, akin to illegal public financing.

In this policy environment, mainland enterprises face three dimensions of blockage when issuing RWA in Hong Kong:

A. The "Long Arm" Extension of Legal Jurisdiction (Penetrative Regulation)

The past operational model was to establish an SPV (Special Purpose Vehicle) in Hong Kong, with the mainland parent company only providing technical support or consulting. Now, this "isolation wall" has become ineffective.

Personal Jurisdiction: Even if the issuing entity is in Hong Kong, if the actual controllers, executives, or technical teams are in mainland China, they are considered to be "cooperating with illegal financial activities" under the new regulations.

Accomplice Risk: The December policy particularly emphasized a crackdown on the entire industry chain. Mainland entities (and individuals) providing technical development, marketing, payment settlement, or even market-making services for overseas RWA projects may violate illegal business operation laws or aiding information network crime laws (aiding crime).

B. "Supply Cut-off" on the Asset Side

The Hong Kong RWA market is most eager for high-quality physical assets from the mainland (such as photovoltaic power station revenue rights, commercial real estate rents).

Asset Exit Lockdown: Since RWA has been classified as illegal financial activity, packaging domestic assets for financing through RWA is suspected of illegal foreign exchange trading and capital flight.

Rights Confirmation Dilemma: Domestic laws do not recognize on-chain tokens as ownership of domestic assets. If a project defaults, foreign investors holding tokens to sue in mainland courts for asset enforcement will not be supported (due to violations of public order and mandatory regulations).

C. "Blockade" on the Funding Side

Obstruction of Fund Repatriation: Even if you raise USDT/USDC in Hong Kong, these funds cannot flow back to mainland entities through formal banking channels for real economic construction (as banks will refuse to accept funds related to "virtual currency businesses").

Marketing Red Lines for Mainland Investors: Strictly prohibited from marketing to Chinese citizens. If your RWA product brochure (PPM) has a Chinese version, or if your roadshow activities involve mainland IP, it will directly trigger regulatory red lines.

According to market feedback, since November 28, the Hong Kong RWA market has experienced a severe reaction. Approximately 90% of RWA consulting projects with mainland backgrounds have been suspended or canceled, and the stock prices of Hong Kong-listed companies related to the RWA concept (especially those with parent companies in mainland China, such as Meitu, New Huo Technology, and Boyaa Interactive) have seen significant declines.

Therefore, for purely mainland background enterprises (Team in China, Assets in China) that still wish to participate in RWA token issuance, the risks are extremely high. Not only is compliance impossible, but they also face criminal liability. It is recommended to abandon the RWA tokenization narrative and return to traditional ABS (Asset-Backed Securities) or issue traditional bonds in Hong Kong.

For enterprises that are completely overseas (Global Team, Global Assets), it is theoretically still feasible, but they need to implement separation, including physical and legal separation, such as:

Personnel Separation: Core team members and private key controllers cannot be located within mainland China.

Asset Separation: The underlying assets must be overseas assets (such as U.S. Treasuries, overseas real estate) and cannot be domestic assets.

Market Separation: Strict KYC, using technical means to block mainland IPs, and not conducting any promotion in the Simplified Chinese internet.

Conclusion and Outlook: The Path of Hong Kong from "Fervor" Back to "Essence"

Looking back at 2025, the Hong Kong RWA market underwent a nearly brutal stress test. From the attention garnered at the beginning of the year with the launch of Project Ensemble, to the frenzy of capital inflow mid-year, and then to the freezing and restructuring triggered by tightening regulations from the mainland at year-end, this painful process has completed a deep reshuffling of the market.

After the waves have washed away the sand, the naked swimmers have exited, leaving behind the seven pillars we have deeply analyzed in this article:

HashKey and OSL have maintained the baseline of compliant trading and custody, becoming the "water, electricity, and gas" of Hong Kong Web3;

Star Road and Asseto have proven the feasibility of traditional consortiums revitalizing existing assets using RWA;

FireX has showcased Hong Kong's unique ability to connect physical industries (computing power/energy) with digital finance;

Mantra and AlloyX have provided the necessary underlying public chain infrastructure and DeFi aggregated liquidity for the market.

Looking ahead to 2026, the Hong Kong RWA market will present the following three major trends:

Transition from "Internal Circulation" to "External Circulation": With the tightening of capital channels from the mainland, Hong Kong will completely bid farewell to the gray fantasy of "helping mainland capital go overseas." Future increments will mainly come from "global assets, Hong Kong distribution." This means utilizing Hong Kong's compliant channels to package U.S. Treasuries, Dubai real estate (as in the Mantra case), or global computing power (as in the FireX case) and sell them to institutional investors in Southeast Asia, the Middle East, and Japan and South Korea. Hong Kong will become a true "offshore financial router."

Dissolution of Boundaries between RWA and DeFi (CeDeFi): Simply "putting assets on-chain" is no longer profitable. The core of competition in the next phase will be "composability." We will see more aggregators like AlloyX using tokenized funds issued by Star Road as collateral to generate stablecoins or conduct leveraged operations on-chain. Compliant CeFi assets will become the highest quality underlying "LEGO bricks" for DeFi protocols.

Stablecoins as the Final Battlefield for RWA: All transactions and settlements of RWA ultimately point to currency. With the implementation of stablecoin regulations in Hong Kong, "yield-bearing stablecoins" (stablecoins backed by RWA assets) will become the largest RWA single product. Whoever can master the issuance scenarios of RWA (such as FireX's mining revenue settlement, Asseto's real estate rent distribution) will hold the minting rights for HKD/USD stablecoins.

The story of Hong Kong RWA is not over; it has just turned the page on the "grassroots entrepreneurship" prologue and entered the main text of "institutional games." In this new phase, compliance is no longer a burden but the greatest asset; technology is no longer a gimmick but a carrier of credit. Hong Kong, a city that continually evolves in crisis, is redefining the financial center of the digital age.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。