Author:RootData Research

01. Market & Financing

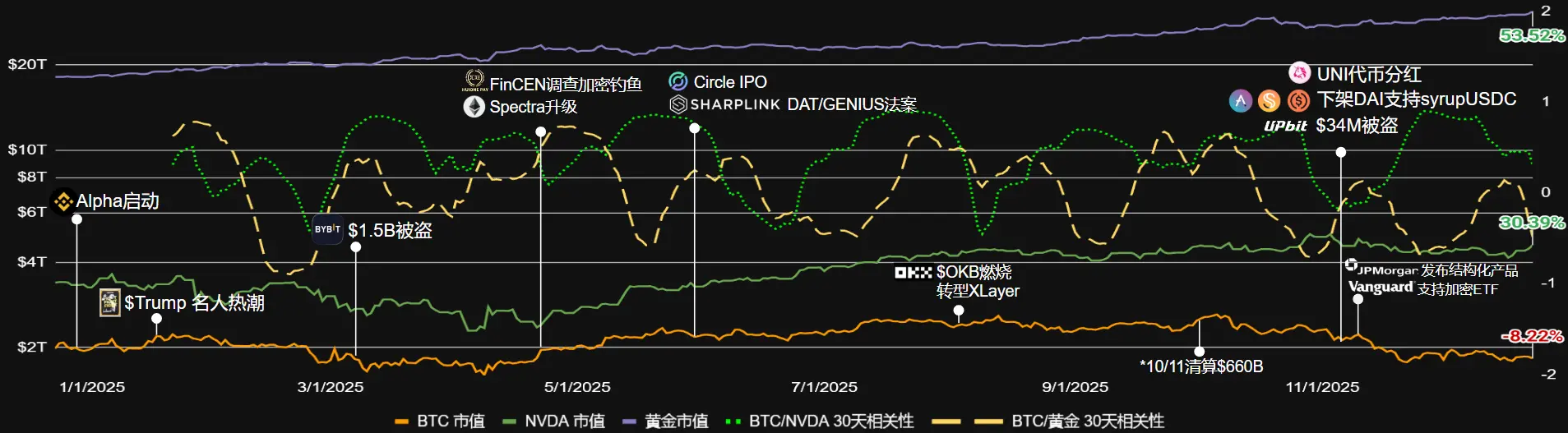

From Optimism to Correction, BTC Underperforms Gold and Tech Stocks

The cryptocurrency industry in 2025 was influenced by multiple factors such as macroeconomics, geopolitics, and technological innovation, experiencing a key year of transition from extreme volatility to institutional transformation. Bitcoin's market value fell by 8% in 2025, underperforming gold (+53%) and NVDA (+30%), with an annual market value volatility of 63% (peaking at $2.62T and dropping to a low of $1.60T). Overall, investors in 2025 need to be wary of geopolitical and hacking risks, prioritizing compliant and transparent crypto assets to capture long-term value.

At the beginning of the year, Trump's inauguration sparked a brief optimism, leading to the launch of celebrity meme coins like $TRUMP, driving social trends and entertainment waves, but also exacerbating asset bubbles. The rise of the DAT concept became a model for corporate Bitcoin treasury management (e.g., MicroStrategy holding over 3% of supply). The "1011 crash" magnified the supply issues in the crypto space, with leveraged liquidations exceeding $19 billion, as Bitcoin fell from a peak of $126,000 to a low of about $90,000, impacted by tariffs and other macro shocks.

The compliance theme ran throughout the year: Circle's successful IPO pushed stablecoins closer to traditional finance; institutions accelerated their entry, with JPMorgan exploring crypto trading products and Vanguard allowing retail purchases of BTC, positioning Bitcoin as a safe-haven asset. However, BTC reached historical highs throughout the year but did not outperform gold and silver, revealing limitations under inflationary pressures.

DeFi's older protocols optimized governance: Aave/Uniswap improved risk adjustments and fee mechanisms to enhance sustainability; Ethereum's Pectra (May) and Fusaka (December) upgrades significantly improved scalability and security. The integration of AI shifted from meme/agent narratives to infrastructure and multi-agent applications, marking a transition from speculation to practicality.

Structural Differentiation in Primary Financing Market: Large Financing Drives New Highs, but Early Projects Continue to Clear Out

Web3 Primary Market Financing Overview

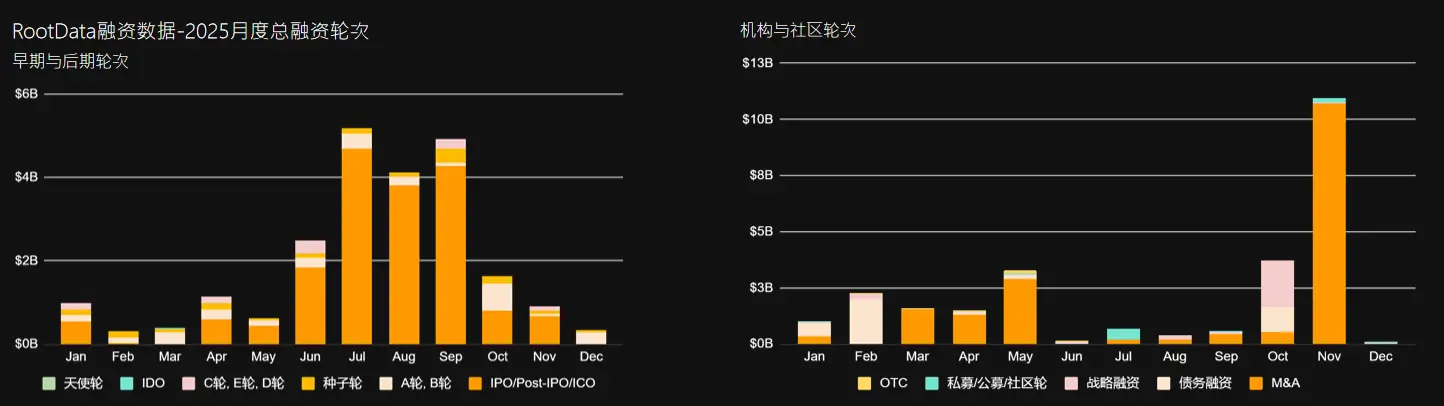

According to RootData statistics, the cryptocurrency primary market completed a total of $22.73 billion in financing in 2025 (excluding Post-IPO and debt financing), a 120.6% increase from 2024. The average financing amount reached $30.6 million, up 234.7% year-on-year. The median financing amount was $6.1 million, an increase of 46.5% year-on-year. In terms of the number of financing events, there were a total of 933 financing events throughout the year, a decrease of 40.3% from last year, averaging 77 events per month. Notably, merger and acquisition events reached 173, a 57.2% increase from 2024, setting a new historical high.

Overall, while the financing amount reached a three-year high, this growth does not indicate a comprehensive market recovery. The increase in financing scale throughout the year was primarily driven by a few leading projects like Polymarket and Binance with large financing rounds, with capital highly concentrated in projects with strong certainty and high scalability.

At the same time, the number of financing projects continued to decline, reaching a five-year low, and the monthly financing event count showed a nearly one-sided downward trend, indicating a continued deterioration in the financing environment for early and small to medium-sized projects. The structural characteristic of capital "converging to the head and shrinking at the tail" became increasingly evident, with the primary market still in a deep clearing phase, showing no widespread cyclical recovery signals.

Financing Events Over $1 Billion

IPO Window Concentrated in Q3, November M&A Wave Signals Accelerated Industry Consolidation in 2026

Looking at the monthly timeline, 2025 exhibited a clear rhythm of "IPO concentration in Q3, M&A explosion in Q4," reflecting the strategic path of crypto companies: "first go public to raise funds, then integrate and expand":

IPO/Post-IPO activities peaked from July to September, accounting for 72% of the year: July, August, and September saw peaks of $4.7 billion, $3.8 billion, and $4.27 billion, respectively, totaling $12.77 billion in Q3, during which BTC prices surged, and market KOL rounds and investment sentiment were high. In contrast, the first half of the year was relatively stable (approximately $4.67 billion from January to June), indicating that the IPO window concentrated in the second half of the year.

M&A saw explosive growth in November, accounting for 59% of the year's total: November alone accounted for $10.7 billion (59% of the total $18.11 billion in M&A for the year), triggered by South Korean search engine giant Naver's acquisition of Upbit's holding company Dunamu. In contrast, M&A steadily grew in the first half of the year (approximately $6.07 billion from January to June), with the November surge reflecting accelerated industry consolidation in 2026, as leading companies rapidly expanded market share through acquisitions.

Private/public/community rounds peaked at $500 million in July, coinciding with the IPO window.

IPO/Pre-IPO/ICO project teams completed large OTC trades in Q2-Q3 to pave the way for subsequent listings/market making/exits. Combined with OTC market data, the active institutional M&A/debt/strategic financing throughout the year suggests that the consolidation trend will continue in the first half of 2026, with leading industry capital operations creating a moat, small and medium projects face the choice of "either being acquired or being eliminated," as the crypto market enters a consolidation cycle of "big fish eating small fish."

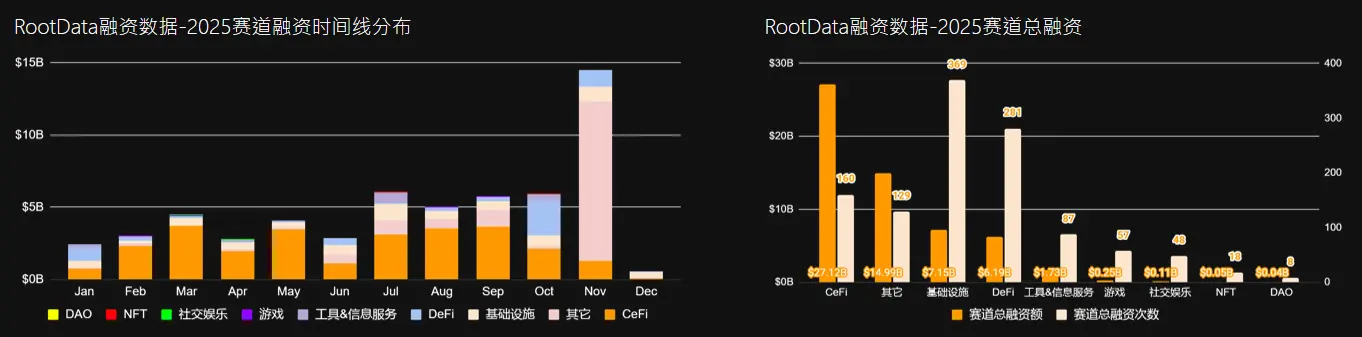

CeFi Leads Strongly with $27.12 Billion, Average Single Financing is 8.7 Times That of Infrastructure

In 2025, financing in the sector was extremely polarized, with CeFi capturing nearly half of the market, while Web3 native sectors became collectively marginalized:

CeFi: $27.12 billion (160 deals, average single deal $169.5 million), with a gap of 8.7 times compared to the average single financing in infrastructure, indicating that CeFi continued to absorb capital flows both inside and outside the market under the influence of ETF compliance and the U.S. "Big and Beautiful" Act, favoring cash flow-friendly CeFi and RWA.

Infrastructure: $7.15 billion (369 deals, average single deal $19.4 million) had the highest number of transactions (32.1%) but only accounted for 12.4% of the financing amount, indicating that native funds in the market are still concentrated on early-stage investment in infrastructure.

DeFi: $6.19 billion (281 deals, average single deal $22 million) remained stable but growth slowed, positioned between CeFi and infrastructure.

Tools & Information Services: $1.73 billion (87 deals), showing fatigue in investment enthusiasm and total amount.

Marginalized Sectors: Gaming $247 million, NFT + DAO + Social Entertainment only $200 million (totaling 0.5%).

The timeline distribution reveals CeFi's steady growth throughout the year, while infrastructure and DeFi entered a mature phase:

CeFi maintained stable output throughout the year, with total financing of $13.8 billion in H2 (50.9% of the second half), with financing windows open throughout the year, unaffected by seasonal factors.

Infrastructure and DeFi entered a mature phase: monthly averages of approximately $6 million and $5 million, respectively, with even distribution throughout the year and no significant peaks, making financing rhythms predictable.

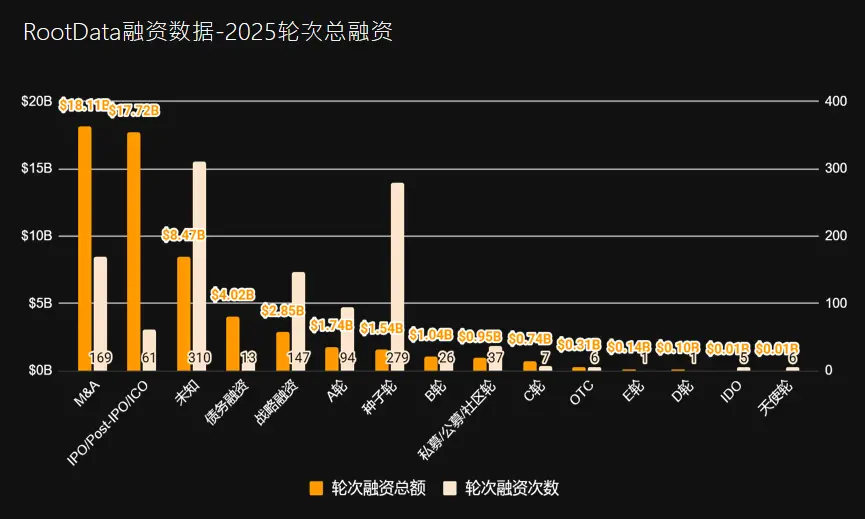

Institutional Activity Dominates 2025, Traditional VC Rounds Shrink in Proportion

*Rootdata's website statistics do not include M&A/Post-IPO data, which may lead to discrepancies in this data.

Market funds are concentrating towards institutionalization and scaling, with the ratio of institutional activity to traditional VC reaching 8.4 times, with significant differentiation among various rounds:

Traditional Institutions/Exchanges/Strategic/Whale Market (M&A/IPO/Debt/Strategic) totaled $42.7 billion, accounting for 74.3%.

M&A: $18.11 billion (169 deals, average $107 million).

IPO/Post-IPO/ICO: $17.72 billion (61 deals, average $290 million).

Debt Financing: $4.02 billion (13 deals, average $309 million).

Crypto Native VC (Seed to C Round) only accounted for $5.07 billion, or 8.8%.

Seed Round: $1.54 billion (279 deals, average $5.5 million).

A Round: $1.74 billion (94 deals, average $18.6 million).

B Round and above: $1.82 billion (34 deals).

Early-stage investment in the industry continues to shrink, with the DAT boom catalyzing debt financing as a new path for large funds, as mining companies and DAT firms expand major crypto assets like BTC/ETH strategies recognized by traditional securities markets through bond financing.

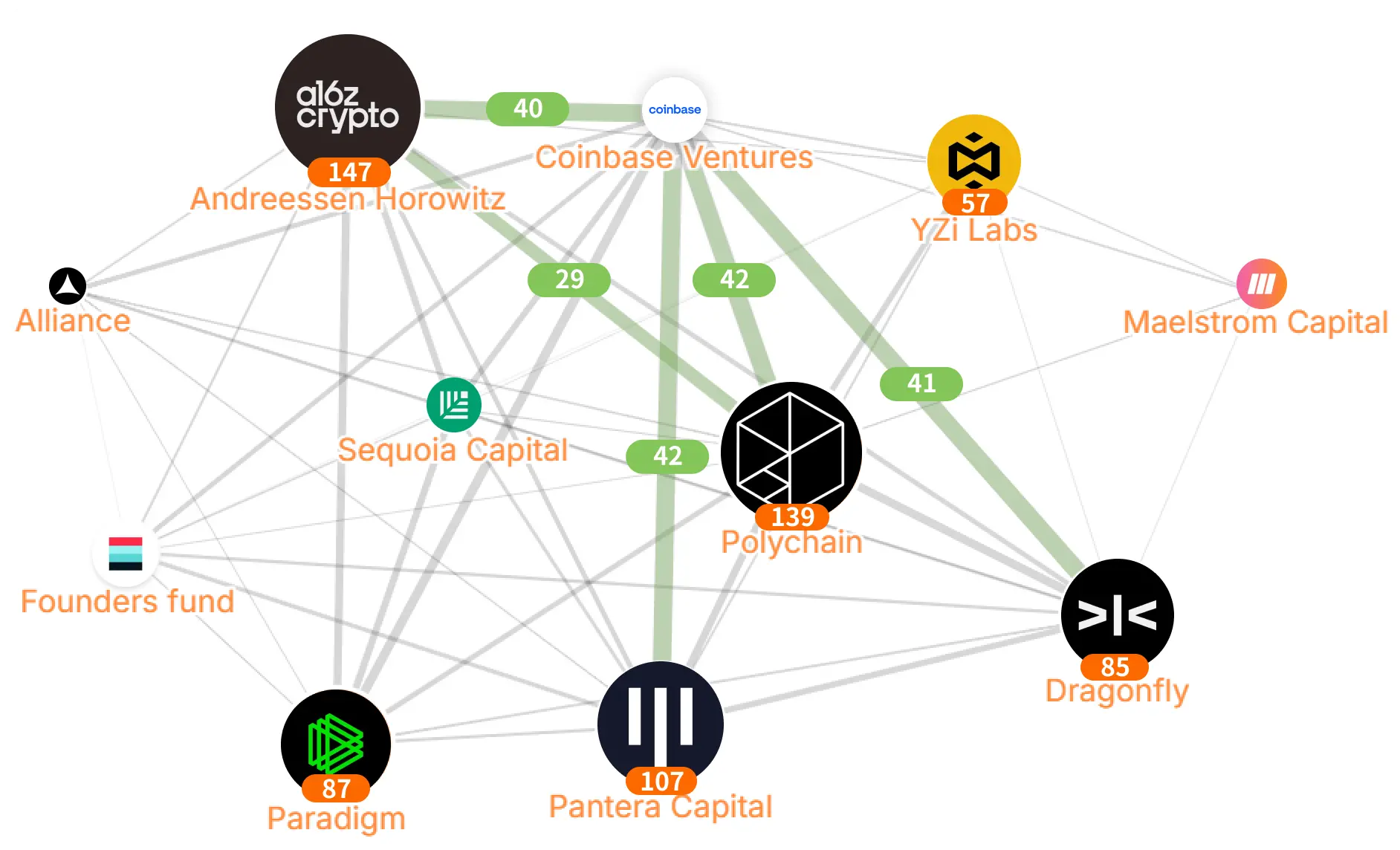

Crypto VC Landscape: Analysis of Top Institutions' Joint Investment Networks and Leading Investment Capabilities

Top VC's Joint Investment and Leading Investment Situation

Throughout the year, VC investment focus shifted towards AI blockchain, DeFi, and institutional-level applications and infrastructure (primarily through M&A), rather than early-stage speculation. Key characteristics are as follows:

Highly Collaborative Investment: Coinbase Ventures has jointly invested 40, 41, and 42 times with a16z, Dragonfly, Polychain, and Pantera, while Polychain and a16z have collaborated 29 times. This indicates that risk-sharing and resource-sharing have become mainstream, with top VCs preferring to form "alliances" to avoid single exposure. Late-stage investments in 2025 accounted for over 50%, and collaboration helps facilitate large rounds (such as infrastructure projects like Berachain and Tempo).

Divergence in Leading Investment Capabilities: a16z led the most rounds (147), reflecting its strong position and high-conviction investment style. Emerging/specialized firms like Alliance and Maelstrom led fewer rounds (4), relying on collaboration.

Core Cluster Formation: Polychain, Coinbase Ventures, a16z, Dragonfly, and Pantera form a tight network, often collaborating. A few giants dominate the flow, while small and medium VCs (like YZi Labs and Founders Fund) enter quality deals through collaboration.

The dominance of leading institutions like a16z, Polychain, and Paradigm in leading investments further reinforces the trend of industry resources skewing towards a few specialized players. This is highly synchronized with the market's shift from meme speculation to practical value, as improved regulatory environments and institutional capital influx prompt VCs to abandon retail-style strategies in favor of deep collaboration to support DeFi optimization and AI agent applications. Ultimately, this professional alliance model not only buffers market volatility but also paves the way for a wave of AI-DeFi innovation under the backdrop of Federal Reserve easing in 2026, driving the crypto ecosystem towards a more robust institutional phase.

02. Compliance & Transparency

The Transparency Revolution in the Crypto Industry: From Concept Discussion to Systematic Practice Stage

In recent years, compliance and transparency have become the most prominent themes in the crypto industry. The industry has officially transitioned from early discussions on "why transparency is important" to the practical stage of "how to systematically achieve financial-grade transparency."

Since April 2025, RootData has taken the lead in rigorously verifying and publicly disclosing the core financing data of platforms on a monthly basis, having disclosed over 20 instances of false financing information, including well-known projects and institutions such as Balance, ACM+, and influencers related to Web3Port. This action not only exposes the long-standing issue of "false financing" in the industry but also provides investors with verifiable reference standards, greatly enhancing the credibility of financing information.

In unlocking data transparency, RootData has mobilized the community and professional researchers to tackle the industry's most stubborn data opacity issues through high-reward activities and USDT incentive mechanisms, successfully promoting the public disclosure and standardization of several key on-chain and off-chain data.

In terms of calendar event transparency, the platform fully leverages the power of community users, using collective supervision and feedback mechanisms to compel project parties to timely and accurately disclose milestone progress and key events, significantly reducing the phenomena of "empty promises" and delays.

RootData's exchange rankings aim to collaborate with exchanges to build a compliant and trustworthy trading ecosystem.

In the future, RootData will launch more innovative initiatives focused on transparency, including deeper on-chain data verification tools, project governance information disclosure standards, and cross-platform information sharing mechanisms. We believe that only by establishing compliance and transparency as the foundation can the crypto industry truly gain mainstream recognition and achieve the leap from marginal innovation to global financial infrastructure.

Research on Exchange Leadership Adjustments: Strategic Shift from Regulatory Compliance to Global Expansion

The personnel changes in exchanges in 2025 mark the crypto industry's transition from "barbaric growth" to maturity, influenced by regulatory easing and market recovery. The reasons for these changes are primarily compliance policies and business expansion, rather than large-scale restructuring. Major platforms like Coinbase and OKX experienced the most changes, indicating their consolidation of industry-leading positions.

Strengthening of Regulatory Compliance and Legal Roles: This is the most significant trend in 2025, influenced by changes in the global regulatory environment (such as the Trump administration easing crypto regulations, CFTC authority expansion, and new SEC rules). OKX replaced its chief legal officer and appointed a vice president for global government relations; Coinbase appointed a global head of regulatory affairs and general counsel; Binance's legal head departed. This indicates that exchanges prioritize hiring or adjusting compliance experts to address policy uncertainties and prepare for potential litigation or compliance audits.

Geographical and Market Expansion Orientation: Several exchanges are promoting internationalization through regional leadership appointments, particularly in North America and Latin America. Kraken appointed a general manager for North America, OKX established a CEO for its U.S. branch, and Bybit hired a country manager for Latin America. At the same time, the roles for institutional business have increased (such as Gemini's head of institutional business and OKX's U.S. institutional head), indicating that exchanges are targeting high-value institutional clients.

Marketing, Product, and Operational Optimization: Frequent changes related to marketing have occurred, with Coinbase, Kraken, and Bitget appointing chief marketing officers or vice presidents of marketing to enhance brand exposure and user growth. Internal promotions and acquisitions (such as Coinbase acquiring talent through Opyn) are also common, reflecting improved operational efficiency. The departure of Kraken's institutional executive, accompanied by layoffs, points to cost control and IPO preparations (planned for 2026).

Leadership Stabilization and Diversification: The appointment of He Yi as co-CEO of Binance is a landmark event, possibly aimed at diversifying risk and strengthening the founding team's influence. Overall, there has been a slight increase in the representation of women and diversity in executive positions, such as Coinbase's COO Emilie Choi and CMO Catherine Ferdon.

Looking ahead to 2026, as potential policies are further implemented (such as the comprehensive implementation of MiCA and U.S. market structure legislation), it is expected that the compliance role will continue to dominate changes.

03. Ecosystem & Sectors

CeFi Ecosystem Accounts for 61.6%, Crypto Market Splits into "TradFi" and "Crypto Native"

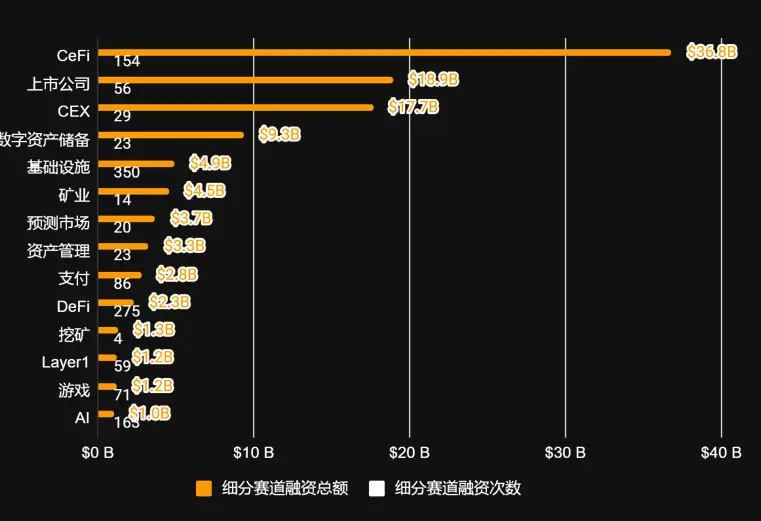

Financing in segmented sectors is concentrating towards the top, with 14 sectors raising over $1 billion attracting $108.9 billion, where the top three—CeFi, public companies, and CEX—monopolize 63.2% of the total financing amount, while 24 sectors raising over $1 billion but under $100 million only attracted $7.3 billion, resulting in an average financing gap of 25.6 times between the top and bottom. The data shows that the influx of hot money continues to flow towards regulatory-friendly, cash-flow-clear TradFi projects, showing little concern for the financing difficulties of crypto-native innovations.

The acceleration of "TradFi" sees CeFi, CEX, digital asset services, and asset management monopolizing $67.1 billion, which is 29 times that of DeFi. At the same time, the BTC reserve strategy of Strategy is being continuously replicated, with mining companies shifting from "mining and selling coins" to "holding coins for listing," reconstructing valuation logic. Public companies rank second with $18.9 billion, with 56 financing rounds confirming the new trend of "Nasdaq exit > token exit," and the crypto IPO window is expected to synchronize with the securities bull market.

The prediction market has surged to $3.7 billion, ranking seventh, rapidly capturing the market combining compliant gambling and RWA under the catalyst of the "presidential election." Polymarket has proven the successful path of "on-chain + regulatory arbitrage."

RootData's segmented sector financing data - 2025 greater than total financing of $1 billion

Crypto Native Sector Innovation and Financing Severely Disconnected:

DeFi ranks tenth with only $2.3 billion, a 16-fold gap compared to CeFi, and the divergence between TVL and financing—DeFi's locked value remains high, but VCs are no longer buying into the narrative of "pure on-chain" and "nested" projects.

Layer 1 ranks twelfth with only $1.2 billion, signaling the end of the public chain narrative.

AI shows "high heat, low concentration": tagged at $1.0 billion, ranking fourteenth, but its distribution combines with multiple tags, indicating that AI is primarily focused on "function enhancement," with investors betting on yet-to-be-realized AI + X applications.

Infrastructure, despite having 369 transactions (the highest frequency), only amounts to $4.9 billion, ranking fifth, with a single deal average of $19 million reflecting the "high-frequency small amount" characteristic, showing that early projects are still laying out but lack significant follow-up financing.

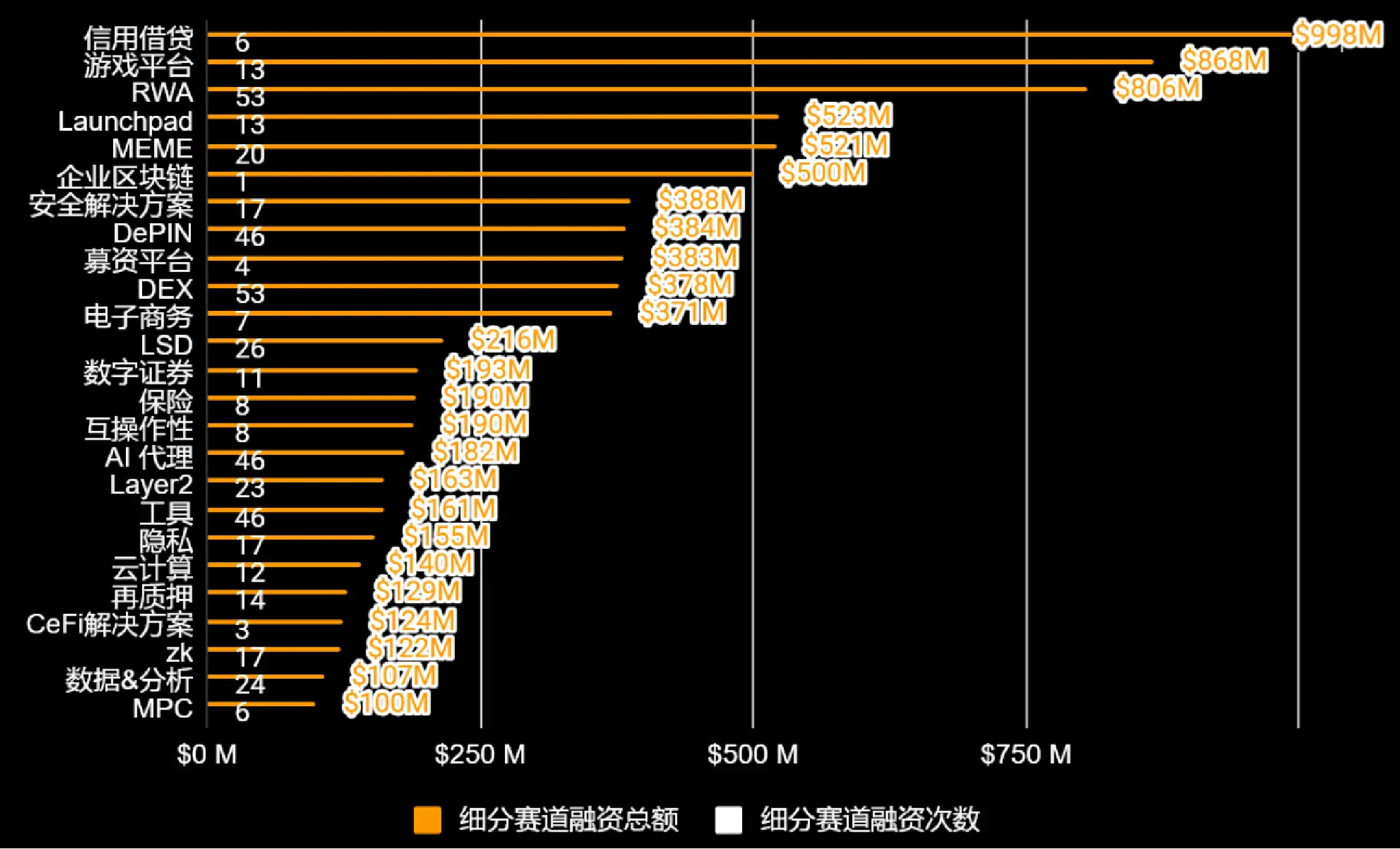

"Cash Flow" Becomes the Dominant Narrative, Pragmatism Rises in Mid-Tier Sectors of $100 Million to $1 Billion

The "pragmatism" of mid-tier sectors with total financing between $100 million and $1 billion is noteworthy.

Financial Infrastructure:

Credit lending $0.87 billion, RWA $0.81 billion, DEX $0.38 billion, totaling $2.05 billion, with the on-chainization of traditional financial tools continuing to gain traction alongside the supply of stablecoins on-chain.

Meme surpassed Layer 2 ($0.16 billion) with $1.04 billion (Launchpad $0.52 billion + MEME $0.52 billion), showing that the crypto-native community's speculative demand outweighs technological innovation, as well as anxiety over CeFi's entry. Among them, Pump.fun and the celebrity coin wave triggered by President Trump are worth pondering.

Privacy & Security totaled $0.77 billion, with compliance demands under regulatory pressure driving funding support for technologies like zk and MPC.

In summary, this indicates that the crypto industry is splitting into two parallel universes:

Investment logic shifts from "decentralization premium" to "compliance premium," from "technology narrative" to "cash flow narrative," and from "single token economy" to "equity + token dual benefits."

TradFi-oriented CeFi/public companies dominate capital, while crypto-native DeFi/Layer 1/NFTs have become "technology testing grounds," requiring constant stitching of new concepts (such as RWA, compliant DeFi, prediction markets, AI + Crypto) to secure ongoing financing.

The pragmatism shift in mid-tier sectors indicates that investments in 2026 will further concentrate on "implementable, revenue-generating, and compliant" projects.

RootData 2025 segmented sector financing data - ($100M < total financing < $1B)

Catalyzed by the U.S. Elections, the Prediction Market Sector Explodes

2025 segmented sector financing rounds - Prediction Market

12 projects raised $3.69 billion, with Polymarket and Kalshi monopolizing 98.5% of the financing share.

Polymarket: $2.15B, accounting for 58.3% of the total

Kalshi: $1.485B, accounting for 40.2% of the total

The top players form an absolute monopoly, with a clear gap:

The 3rd place TCC only raised $15M, the 4th place Limitless $14M, and the other 8 projects raised less than $10M.

According to Rootdata's comparison feature:

Polymarket is backed by General Catalyst, Polychain, and Blockchain Capital, with an FDV of $322.72M and an RD growth index of 1,893 (+0.08%), ranking first.

Kalshi is backed by Sequoia Capital, Capital G, and Coinbase Ventures, with undisclosed FDV and an RD growth index of 1,601 (-0.04%).

Limitless is backed by 1confirmation, WAGMI Ventures, and Coinbase Ventures, with an FDV of $589.69K and the fastest growth index of 666 (+5.74%).

The prediction market has seen explosive trading volumes for Polymarket and Kalshi driven by the 2024 U.S. elections, with a combined financing of $3.635 billion primarily occurring between 2024-2025. The prediction market, as a model of "compliant gambling + RWA," has gained mainstream capital recognition, with regulatory compliance serving as a moat:

Polymarket (implicitly approved by U.S. regulators) and Kalshi (CFTC approved) hold absolute advantages.

The breakout effect of the sector provides trading/arbitrage liquidity for the crypto community.

As the 2024 elections conclude, prediction market trading volumes will return to normal, and binary options and competitive events in 2026 will become opportunities for "emerging players."

Currently, under the evident top effect, PM and Kalshi are also actively improving product experience, market depth, and cross-platform integration, while founders of related ecosystem trading and data monitoring and analysis tools are eager to participate.

PerpDex Sector Financing Reaches $460 Million, Flying Tulip Dominates with $200 Million

2025 segmented sector financing rounds - PerpDex

The perpetual DEX (PerpDex) sector has gained popularity due to the success of Hyperliquid and CZ's Aster, with a total of 33 projects raising $460 million, showing a concentrated top pattern:

Flying Tulip: $200M seed round (accounting for 43.2% of the total, 2.9 times that of the second place)

The top 5 account for 70.6%: Flying Tulip $200M, Lighter $68M, Ostium $20M, GRVT $19M, and Roxom $17.9M.

Tail projects face financing difficulties: 75.8% of projects raised less than $10M, with an average of $14M vs. a median of $5M.

According to Rootdata's comparison feature, the performance of PerpDex is severely disconnected from financing disclosure. From RootData's multi-dimensional comparative data, the RD growth index for Lighter is +1.15% over 7 days, while Hyperliquid is -0.35%. The RD heat index for Lighter is 379 (+139.87%), far exceeding Hyperliquid's 195 (+18.90%), indicating that VC-backed projects are beginning to catch up in market attention compared to purely community-driven projects.

Lighter raised $89M and is backed by VCs such as Haun Ventures and Ribbit Capital, with financing information fully disclosed.

Hyperliquid's financing is undisclosed, but it has generated $66.04M (+20.48%) in revenue over the past 30 days, consistently leading the market in trading volume.

Aster's financing amount is undisclosed but has the support of YZi Labs and Binance founder CZ.

The PerpDex sector exhibits three main characteristics: "low financing, intense competition, and technological differentiation."

The unusual financing of Flying Tulip may reflect market trust in DeFi pioneer Andre Cronje.

Hyperliquid's lack of financing disclosure but standout performance indirectly confirms that "community-first + zero financing" may be viable in the PerpDex sector.

Over 90% of projects raised less than $20M, indicating that the sector is still in its early stages, and the barrier effect of top projects may further amplify in 2026.

As more VC-backed projects like Lighter accelerate product iteration, perpetual DEXs will differentiate into "community-driven high trading volume" and "institutionally subsidized high growth," requiring investors to pay attention to multi-dimensional indicators such as recent revenue and RD growth index to assess project potential.

The AI Sector Blooms with a Decentralized Competitive Landscape, Ready to Distinguish the Genuine from the False

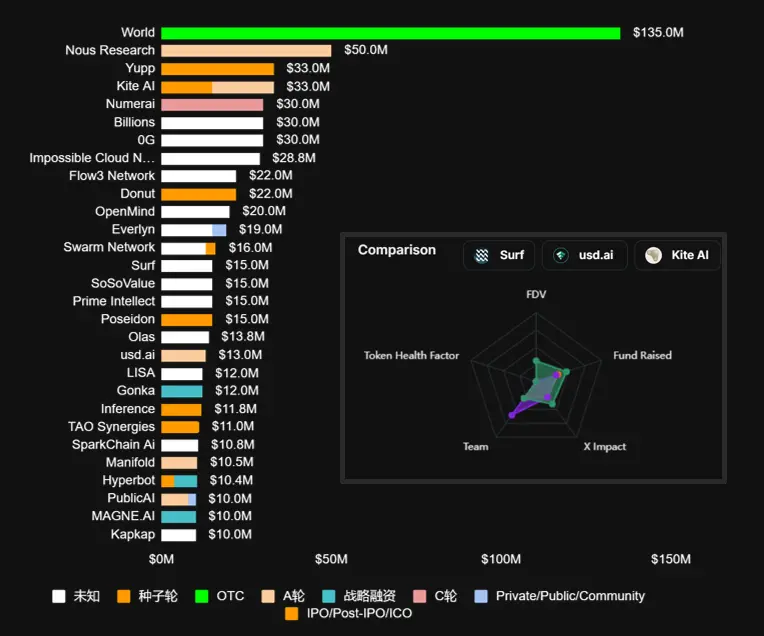

2025 segmented sector financing rounds - Top 30 AI

Compared to PerpDex, the top five in the AI sector have a concentration of only 28% vs. 70% in PerpDex. AI competition is more dispersed, with 88% of projects raising less than $20M, and an average financing of $10M > median of $6M.

The AI sector showcases diverse technical routes and verticals, with a "hundred schools of thought contending," indicating that its business models have yet to be validated. Investors need to focus on the technical feasibility, token economic models, and practical application scenarios of projects, rather than judging value solely based on the "AI" label.

According to Rootdata's data combined with comparison features:

Nous Research, driven by research, has received the most financing.

Kite AI raised $33M, backed by General Catalyst and PayPal Ventures, focusing on AI + Layer 1 + payments.

Surf secured $15M in financing, backed by Pantera Capital and Coinbase Ventures, with an RD growth index of 869 (+0.92%) and an RD heat index of 131 (+32.47%).

usd.ai raised $13M, backed by Framework Ventures and YZi Labs, but its RD growth index is 1,100 (-6.17%), possibly affected by market conditions.

"AI + X" has become mainstream, with few pure AI infrastructure projects. As Web2 giants like OpenAI and Google accelerate AI product iterations, Web3 AI projects face the question of whether "decentralized AI training/inference" can establish a viable token economy. 88% of projects raised less than $20M, with most financing rounds being "unknown," indicating that investors hold a cautiously optimistic attitude towards AI + Crypto. From the distribution of financing rounds:

Seed rounds dominate, with 22 projects in the $10-20M range.

64 projects raised less than $10M, showing a significant deviation in quantity.

The $30-50M range is concentrated with Yupp, Kite AI, Numerai, Billions, and 0G, all focused on AI infrastructure or decentralized training directions, reflecting VCs' continued investment in "AI + Crypto" infrastructure.

World’s OTC financing is exceptionally prominent, possibly benefiting from Sam Altman's endorsement.

In summary, 2026 and beyond will be the year of "distinguishing the genuine from the false" in the AI sector, with projects that can prove the feasibility of "decentralized AI training/inference" token economies or achieve PMF standing out.

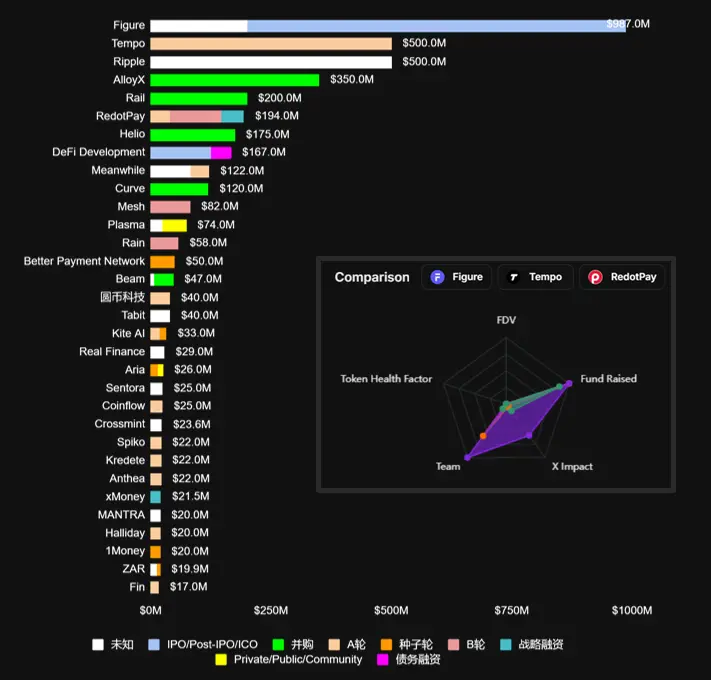

2025 Payment/RWA Sector Accelerates TradFi Integration, Figure Leads the Way

2025 segmented sector financing rounds - Payment/RWA

According to Rootdata's comparison feature, the Payment/RWA sector shows a deep integration trend between TradFi and Crypto, with the top three financings including Ripple, along with:

Figure: Raised a maximum of $987M, with a total financing of $1.4B, supported by traditional tech venture capital and crypto-native VCs, focusing on blockchain financial services + CeFi + lending (CeFi) + real estate.

Tempo: $500M backed by well-known VCs such as Greenoaks Capital and Sequoia Capital, with an RD heat index of 91 (+43.48%) indicating a rapid increase in market attention, possibly due to its Layer 1 attributes and its CEO Matt also serving as a co-founder of Paradigm and a board member of Stripe. Notably, Stripe acquired Bridge for $11B at the end of 2024 as its stablecoin issuance platform and payment API interface.

RedotPay: $194M backed by Goodwater Capital and Pantera Capital, focusing on wallet + payment digital packaging solutions, leading with an RD heat index of 108. Its founder Michael previously served as Vice President of Institutional Banking at DBS Bank and Vice President of Energy and Offshore at HSBC.

The Payment/RWA sector exhibits characteristics of "TradFi giants dominating, active mergers and acquisitions, and regulatory compliance driving":

The top 5 in Payment/RWA have a concentration of 57.5%, positioned between Perpdex and AI, showing both a top effect and maintaining competitive vitality.

The entry of traditional financial giants is evident: Traditional banks, electronic payment, and Web3 payment giants like Ripple, Stripe, and Paradigm are actively acquiring, indicating that the Payment/RWA sector has become the main battleground for traditional finance to embrace blockchain.

Mergers and acquisitions have become the mainstream exit path: Among the top 10, 5 have completed large financings through acquisitions, reflecting the development logic of "acquiring technology + integrating licenses" in the RWA/payment sector.

In 2026, the Payment/RWA sector will shift from "technology validation" to "scalable implementation," and projects without compliance licenses, TradFi resources, and large financings will face elimination. Investors in 2026 need to focus on the compliance progress of projects, TradFi partnerships, and the actual scale of payment/assets on-chain, as purely technical concept projects will be marginalized.

04. Rankings

Top 50 VCs & Top 100 Project Rankings

RootData's Top 50 VCs list as of October 1, 2025

RootData's Top 100 Projects list as of October 1, 2025

As the industry's most transparent data barometer, the rankings are based on multi-dimensional indicators such as investment activity, market reputation, and on-chain performance, deeply reflecting the capital landscape and innovation highlands during the "institutional transformation" process. This list not only pays tribute to the annual outstanding contributors but also serves as a core reference for capturing certainty in industry value in 2026. For details, refer to https://rootdata.com/rootdatalist

About RootData

RootData is a Web3 asset data platform dedicated to making Web3 investment simpler, having recorded over 19,000 projects, 2,800 investment institutions, 18,000 individuals, and 9,200 financing events, presenting data in a highly visual and structured manner, and has become an essential data platform for over 3 million Web3 users to discover early alpha projects and make investment decisions.

Download this issue's PDF research report | Download this issue's PDF research report

Disclaimer

This report is produced by RootData Research, and the information or opinions expressed in this report do not constitute investment strategies or advice for any individual. The materials, opinions, and speculations contained in this report reflect the judgment of RootData Research as of the date of publication, and past performance should not be used as a basis for future performance. At different times, RootData Research may issue reports that are inconsistent with the materials, opinions, and speculations contained in this report. RootData Research does not guarantee that the information contained in this report remains up to date, and reliance on the information in this material is at the reader's own discretion; this material is for reference only.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。