According to a summary by Bloomberg, experts from six major international investment banks generally believe that the US dollar will continue to weaken against major currencies, with the dollar index expected to drop by about 3% by the end of 2026.

Author: Ba Jiuling, Wu Xiaobo Channel

The suspense itself is not great, just a step away from the goal.

After nearly a month of speculation that the "renminbi is about to break 7," analysts from Goldman Sachs provided a key assist.

Recently, Goldman Sachs released its "2026 Global Stock Market Outlook," which mentioned the renminbi. Based on its dynamic equilibrium exchange rate model (GSDEER), Goldman Sachs calculated the fair value of the renminbi, indicating that it is undervalued against the US dollar by nearly 30%.

However, slogans are more attractive than numbers, and the report stated:

The degree of undervaluation of the renminbi against the US dollar is comparable to that in the mid-2000s.

In 2000, the average annual exchange rate of the US dollar against the renminbi was about 8.28. Subsequently, the renminbi entered a nearly decade-long appreciation cycle, rising to around 6.1 against the US dollar.

Goldman Sachs' calculations gave the market more confidence in a bullish outlook, causing the offshore renminbi, which was already in an appreciation channel, to suddenly gain momentum.

On the morning of December 25, the exchange rate of the US dollar against the offshore renminbi quickly broke through the 7.0 mark, reaching a new high in 15 months and officially re-entering the "6 era."

USD/CNY Trend from 2005 to 2025

Source: Juheng.com

At the same time, the onshore renminbi exchange rate hit a low of 7.0053, just a step away from "breaking 7." The People's Bank of China also raised the renminbi's midpoint rate against the US dollar by 79 basis points. Now, with the "shoe dropping," we can finally ask a few questions:

Why can the renminbi have an independent trend in 2025? What does entering the "6" era mean for our business operations and personal asset allocation?

Is "breaking 7" a short-term or long-term phenomenon?

Looking back over the year, the renminbi exchange rate has been quite unusual.

In April this year, the renminbi exchange rate hit a low of 7.429, and the market was still worried about the risk of renminbi depreciation. Unexpectedly, as the year-end approached, the trend of the renminbi exchange rate reversed.

This is influenced by seasonal factors.

As is customary, approaching the end of the year, domestic export companies need to settle accounts with suppliers, converting the US dollars earned over the year into renminbi for "closing accounts" and distributing year-end bonuses, which has triggered seasonal demand for currency conversion.

As more and more people "need" renminbi, starting from the end of November, the "price" of the renminbi has risen, aligning with the timeline.

On December 24, foreign trade container terminals were busy at work.

Additionally, due to the recent "impressive rise" of the renminbi, export companies that had previously hoarded US dollars to avoid potential losses began to rush to "settle" their currency, further boosting the renminbi's appreciation.

It is worth mentioning that this wave of demand is evidently larger than in previous years.

According to data released by the General Administration of Customs, in the first 11 months of this year, China's goods trade maintained growth, with a total import and export value of 41.21 trillion yuan, a year-on-year increase of 3.6%. In the first 11 months, China's trade surplus exceeded 1 trillion US dollars for the first time.

This means that some export companies have more foreign exchange income than in previous years.

Wang Qing, chief macro analyst at Dongfang Jincheng, believes that as the year-end approaches, the increase in corporate currency conversion demand is also driving the seasonal strengthening of the renminbi; especially after the recent continuous appreciation of the renminbi against the US dollar, the accumulated demand for currency conversion from previous high export growth may be accelerating its release.

However, Huatai Futures wrote in its "Huatai Futures - Forex Annual Report: Gradually Improving, Renminbi Enters Appreciation Channel" that due to the impact of inverted interest rate differentials between China and the US, the cost-effectiveness of currency conversion and holding is becoming more balanced, leading to a divergence in corporate currency conversion strategies. Therefore, although this year's year-end "currency conversion wave" will provide marginal support for the renminbi, it does not constitute a dominant trend.

The appreciation of the renminbi also has some geographical advantages.

In 2025, the Federal Reserve implemented three interest rate cuts, directly leading to a weakening of the dollar index. As of December 25, the dollar index has fallen by 9.69% this year, not only breaking below the 100 mark but also closing at 97.97, marking the largest annual decline in nearly eight years.

On December 10, the Federal Reserve cut interest rates for the third time.

Exchange rates are like a "seesaw." When the dollar weakens, it means that non-dollar currencies, including the renminbi, strengthen, resulting in a "passive appreciation" of the renminbi.

Another contributing factor is that after Trump took office, he initiated a global "tariff war," undermining the global trade system that had been operating for years based on existing rules.

When trade flows become uncertain, the costs of trade settlement and supply chain financing denominated in US dollars naturally rise, further shaking the foundation of the dollar as an ideal trade settlement currency.

Coupled with the 35-day government shutdown in the US and the downgrade of the US sovereign credit rating by one of the three major rating agencies, Moody's, global funds began to seek safe havens, leading to a large outflow of dollar assets from the US—thus, the renminbi and renminbi assets welcomed their own "value reassessment."

According to data from global fund flow monitoring agency EPFR Global, during the period from May to October 2025, foreign capital-focused stock funds investing in Hong Kong stocks saw a cumulative net inflow of 67.7 billion Hong Kong dollars, completely reversing the net outflow trend of the same period in 2024.

The appreciation of the renminbi is more importantly about people.

On December 11, the World Bank raised China's GDP growth forecast by 0.4% in its latest economic briefing, and the International Monetary Fund (IMF) raised this year's GDP growth forecast for China by 0.2%, expecting it to reach 5%.

The simultaneous upward revision of China's economic outlook by these two international institutions clearly reflects a strong affirmation of the current operation and long-term development potential of the Chinese economy.

Among them, the stability of exports provides the most fundamental support for the appreciation of the renminbi.

On one hand, the record trade surplus is a solid foundation for the renminbi exchange rate, and on the other hand, the value of exports has also increased.

Data from the General Administration of Customs shows that in the first 11 months of this year, China exported integrated circuits worth 1.29 trillion yuan, an increase of 25.6%; and automobiles worth 896.91 billion yuan, an increase of 17.6%. This means that the leading exports have shifted from traditional labor-intensive products to high-end manufacturing industries such as shipbuilding, integrated circuits, and new energy vehicles.

Export vehicles parked at the port

Guan Tao, chief global economist at Bank of China Securities, believes that the increased diversification of export markets, the accelerated transformation and upgrading of domestic manufacturing, and the enhanced competitiveness of export products have contributed to maintaining rapid growth in China's exports, providing important support for China's market share in global exports.

Renminbi Appreciation and Personal Investment

Next, let's address a question that everyone is most concerned about—what is the impact of this renminbi appreciation on A-shares, is it a positive or negative?

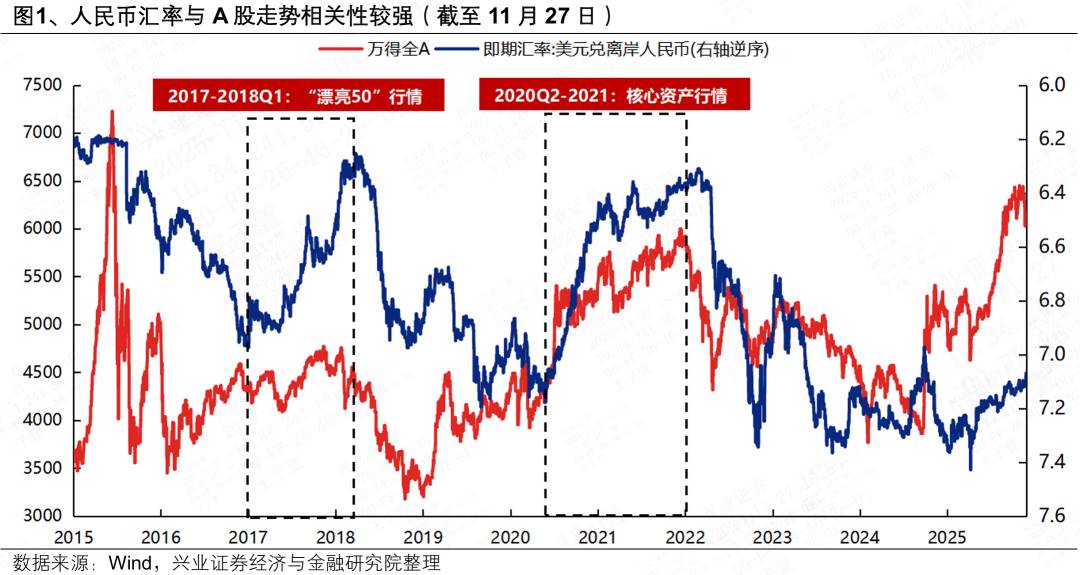

Over the years, there have been many studies on the impact of exchange rates on A-share trends. The team led by Zhang Qiyao at Xingzheng Strategy believes that since the exchange rate reform in 2015, there has been a significant positive correlation between the renminbi exchange rate and A-share trends.

From the correlation chart of the renminbi exchange rate and A-share trends, we can also see that since 2017, the correlation between the renminbi and A-share trends has become quite evident.

For example, during the "beautiful 50" period from 2017 to the first quarter of 2018, and during the renminbi appreciation trend from the second quarter of 2020 to 2021, A-shares operated within a bull market range. Correspondingly, foreign capital has become an important incremental driver of the upward trend in the Chinese stock market.

Additionally, Goldman Sachs has conducted a study on US stocks, concluding that: if the fundamentals do not diverge, a 0.1 percentage point increase in the exchange rate leads to a 3%-5% increase in stock valuations.

Of course, due to the complex mechanisms of influence between exchange rates and stock prices, we cannot assert that as long as the renminbi appreciates, individual stocks and the overall market will definitely rise. However, based on various assessments, this renminbi appreciation is expected to stimulate further increases in A-shares.

However, the appreciation of the renminbi will indeed have varying impacts on different industries, thereby affecting the stock prices of related listed companies.

The appreciation of the offshore renminbi means that the prices of Chinese goods priced in local currency will rise in the international market, making them more expensive for foreign buyers, which naturally weakens price competitiveness and may lead to a decrease in export orders.

Particularly for traditional export-oriented industries, such as home appliances and textiles, where profit margins are relatively thin and sensitive to exchange rate fluctuations, the profit impact on these industries will be quite significant.

Everything has its pros and cons; the appreciation of the renminbi is also a great benefit for certain industries. For example, domestic industries that rely heavily on imports can directly benefit from this appreciation.

According to import and export data from the National Bureau of Statistics, industries in China that are "net importers," including energy, agriculture, and materials, directly benefit from this appreciation.

At the same time, industries with significant dollar liabilities also benefit from the appreciation of the renminbi. For instance, within the scope of Hong Kong Stock Connect, industries with a high proportion of short-term liabilities in US dollar debt, such as internet, shipping, aviation, utilities, and energy, will benefit.

Moreover, the appreciation of the renminbi will also change the trading styles of individual investors.

Earlier this year, "US dollar deposits" and US Treasury bonds were very popular, and some investors exchanged a considerable amount of US dollars for investment. However, with the significant appreciation of the renminbi, US dollar deposits have become "negative yield," and even though US Treasury bonds enjoyed a 5% yield, accounting for exchange rate losses, they are only comparable to the interest rates of one-year fixed deposits.

Of course, some people ask, since the renminbi is now strong, can we take advantage of the renminbi appreciation to buy more US dollars for future use?

For individuals, if it is for cross-border shopping, it may be a good choice, as the appreciation of the renminbi equates to enjoying discounts when consuming abroad, and when paying in renminbi for overseas purchases, it will be 5%-10% cheaper than before.

However, if it is purely for speculation, it is better to be cautious. Because the probability of significant fluctuations in the renminbi exchange rate is low, one should not blindly chase after gains by converting renminbi into US dollar deposits.

Where to go after "breaking 7"?

It is worth noting that when we talk about appreciation now, we mainly refer to the renminbi appreciating against the US dollar, rather than a "comprehensive strengthening."

According to data from the China Foreign Exchange Trading Center, since the beginning of this year, the renminbi exchange rate against the CFETS renminbi exchange rate index, the BIS currency basket renminbi exchange rate index, and the SDR currency basket renminbi exchange rate index have all declined, with two major indices falling below 100.

These three indices are "average report cards" measuring the comprehensive value of the renminbi against a basket of foreign currencies.

The weakening of the index means that although the renminbi has appreciated significantly against the US dollar, its overall value level is declining against other currencies, such as the British pound, euro, and a basket of foreign currencies.

However, institutions including Goldman Sachs share a consensus that with the continued development of the Chinese economy and the deepening of the renminbi's internationalization, a "moderate appreciation" of the renminbi is expected to become a major trend.

For instance, Yuekai Securities believes that in the past two years, domestic prices have been sluggish while overseas inflation has been high, causing the central level of the CFETS renminbi exchange rate index to even decline, indicating that there is potential for the renminbi to catch up. The renminbi's exchange rate against the US dollar is expected to maintain strong momentum, with "6.8" possibly being a key level.

According to a summary by Bloomberg, experts from six major international investment banks generally believe that the US dollar will continue to weaken against major currencies, with the dollar index expected to drop by about 3% by the end of 2026—this will create a trend of passive strengthening for the renminbi.

However, regardless of whether the renminbi continues to appreciate or experiences fluctuations in the future, it is unlikely to exhibit overly surprising trends.

The recent Central Economic Work Conference has emphasized for four consecutive years the need to "maintain the basic stability of the renminbi exchange rate at a reasonable and balanced level."

Additionally, as stated by the central bank: "The medium- to long-term exchange rate of the renminbi has a solid foundation, and we will continue to uphold the decisive role of the market in exchange rate formation, maintain exchange rate flexibility, strengthen expectation guidance, prevent excessive exchange rate adjustments, and keep the renminbi exchange rate basically stable at a reasonable and balanced level."

Even Goldman Sachs has stated: "We expect the renminbi's appreciation to be gradual and managed, but even so, we believe it is still likely to outperform forward pricing."

For individual investors, we should not focus on predicting precise exchange rate points but rather on understanding trends, adapting to industrial upgrades, and effectively using hedging tools. We need to seize the opportunities brought by appreciation while also guarding against the risks posed by fluctuations.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。