Author: Tanay Ved, Coin Metrics

Translated by: GaryMa Wu Says Blockchain

Key Points Summary

The demand for major absorption channels such as ETFs and DAT has recently weakened, while the deleveraging event in October and the macro backdrop of declining risk appetite continue to pressure the crypto asset market.

Leverage in the futures and DeFi lending markets has been reset, resulting in lighter and cleaner positions, thereby reducing systemic risk.

Spot liquidity has not yet recovered, with both mainstream assets and altcoins remaining weak, making the market more fragile and susceptible to unexpected price fluctuations.

Introduction

"Uptober" started strong with Bitcoin hitting a new historical high. However, the optimism was quickly interrupted by the flash crash in October. Since then, BTC has dropped by about $40,000 (over 33%), with altcoins experiencing even greater impacts, bringing the total market capitalization close to $3 trillion. Despite positive fundamental developments this year, there has been a clear divergence between price performance and market sentiment.

Digital assets seem to be at the intersection of multiple external and internal forces. On a macro level, uncertainty regarding interest rate cuts in December and recent weakness in tech stocks have exacerbated the decline in risk appetite. Internally, core absorption channels such as ETFs and Digital Asset Treasuries (DAT) have seen capital outflows and increased cost pressures. Meanwhile, a wave of market-wide liquidations on October 10 triggered one of the most severe deleveraging events in recent years, with aftershocks still ongoing as market liquidity remains shallow.

This report will dissect the driving forces behind the recent weakness in the crypto asset market. We will delve into ETF fund flows, perpetual futures and DeFi leverage conditions, as well as order book liquidity, exploring how these changes reflect the current market state.

Macro Environment Shifts Towards Declining Risk Appetite

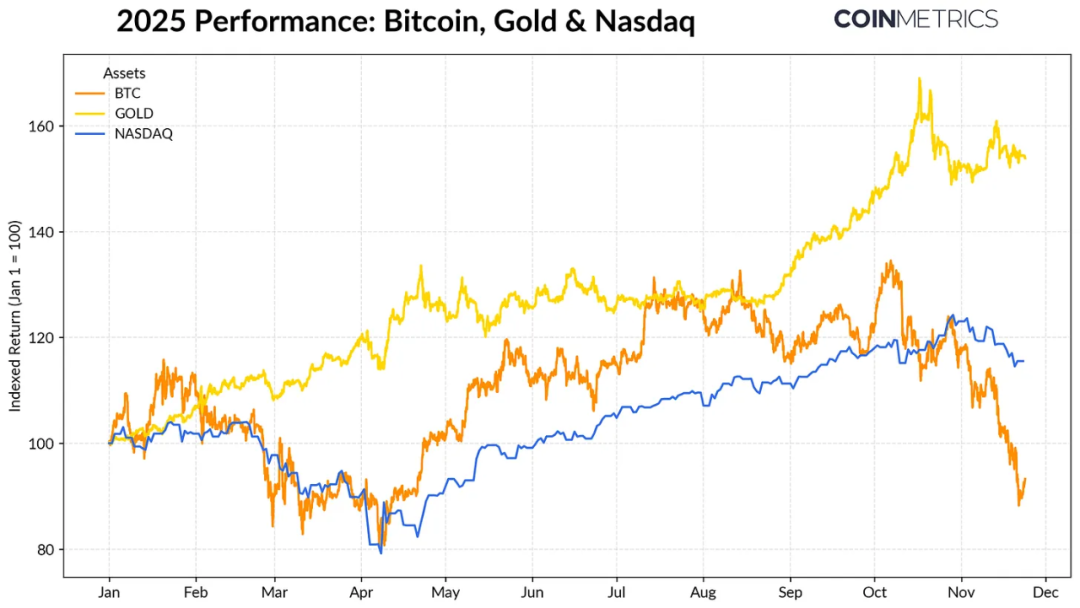

The performance gap between Bitcoin and major asset classes is widening. Gold has risen over 50% this year, driven by record central bank gold purchases and ongoing trade tensions. Meanwhile, tech stocks (NASDAQ) have lost momentum in the fourth quarter as the market reassesses the probability of Fed rate cuts and the sustainability of AI-driven valuations.

As shown in our previous research, the relationship between BTC and "risk assets" like tech stocks and "safe-haven assets" like gold tends to swing cyclically with the macro environment. This means it is particularly sensitive to sudden events or market shocks, such as the flash crash in October and the recent decline in risk appetite.

As the anchor of the entire crypto market, Bitcoin's pullback continues to transmit to other assets, although themes like privacy coins occasionally show brief performance, the overall trend remains synchronized with BTC.

ETFs and DAT: Weakening Absorption Demand

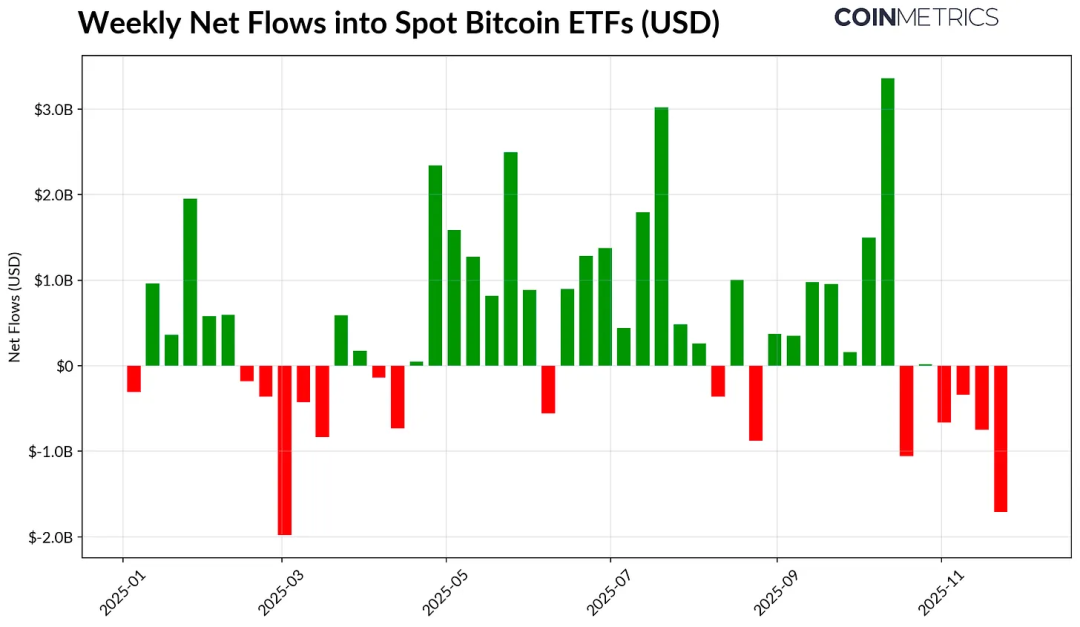

Part of the recent weakness in Bitcoin can be attributed to the softening of funding absorption channels that had supported the market for most of 2024-2025. Since mid-October, ETFs have seen several weeks of net outflows totaling $4.9 billion. This marks the largest redemption wave since April 2025, when Bitcoin fell to around $75,000 due to tariff expectations. Despite significant short-term outflows, on-chain holdings remain on an upward trend, with BlackRock's IBIT ETF alone holding 780,000 BTC, accounting for about 60% of the total supply of spot Bitcoin ETFs.

If funds return to sustained net inflows, it would indicate stabilization in this channel. Historically, ETF demand has been a key absorber of supply when risk appetite improves.

Digital Asset Treasuries (DAT) are also under pressure. As the market declines, their stock and crypto holdings' market value have been compressed, putting pressure on the net asset value premium that supports their growth mechanism. This will limit their ability to raise new capital through stock issuance or debt, thereby restricting their capacity to enhance "per share crypto asset" allocations. Smaller or newer DATs are particularly sensitive to these changes, becoming more cautious when their cost basis and equity pricing turn unfavorable.

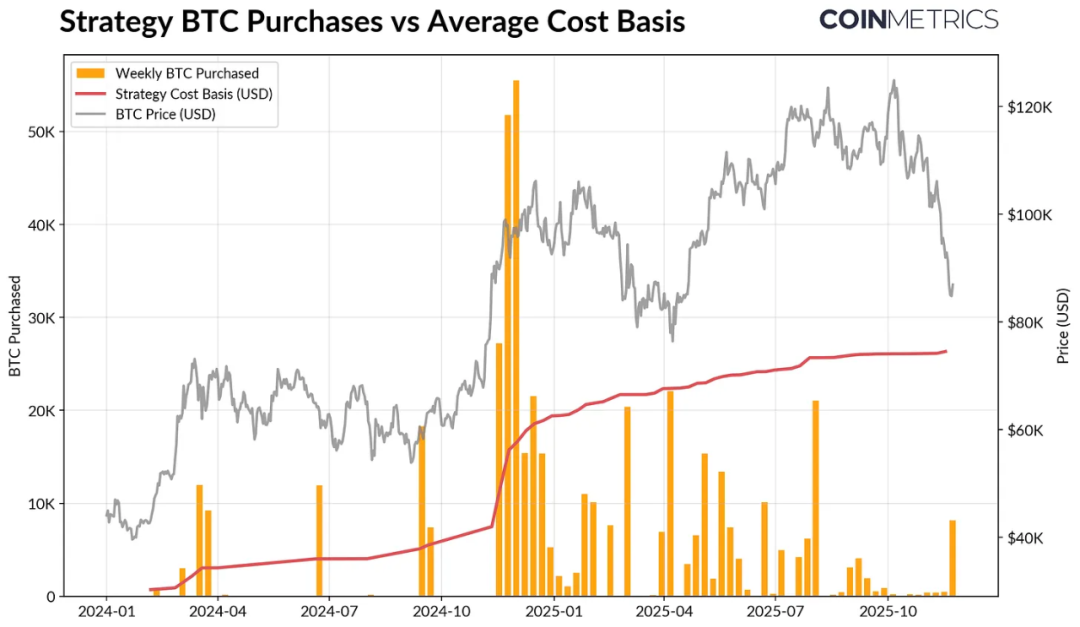

Strategy — the largest DAT currently — holds 649,870 BTC (about 3.2% of total supply) at an average cost of $74,333. As shown in the chart below, Strategy's accumulation accelerated significantly when BTC was rising and its stock price performed strongly, but has noticeably slowed recently without becoming a force for active selling. Even so, Strategy remains in a state of unrealized profit, with costs below the current price.

If BTC continues to decline or faces the risk of index removal, Strategy may come under pressure; however, if the market reverses and its balance sheet and valuation improve, it could restore a stronger accumulation pace.

On-chain profit metrics also reflect this situation. The Short-Term Holder SOPR (155 days) has fallen into a ~23% loss range, which typically indicates that the most sensitive holding group is experiencing "surrender" selling. Long-term holders remain on average profitable, but SOPR also shows a mild selling tendency. If the STH SOPR returns above 1.0 while LTH selling pressure eases, it would suggest that the market may stabilize.

Crypto Market Deleveraging: Perpetual Futures, DeFi Lending, and Liquidity

The liquidation wave on October 10 initiated a multi-layered deleveraging cycle across futures, DeFi, and stablecoin leverage, the effects of which have not yet fully dissipated.

Leverage Cleansing in Perpetual Futures

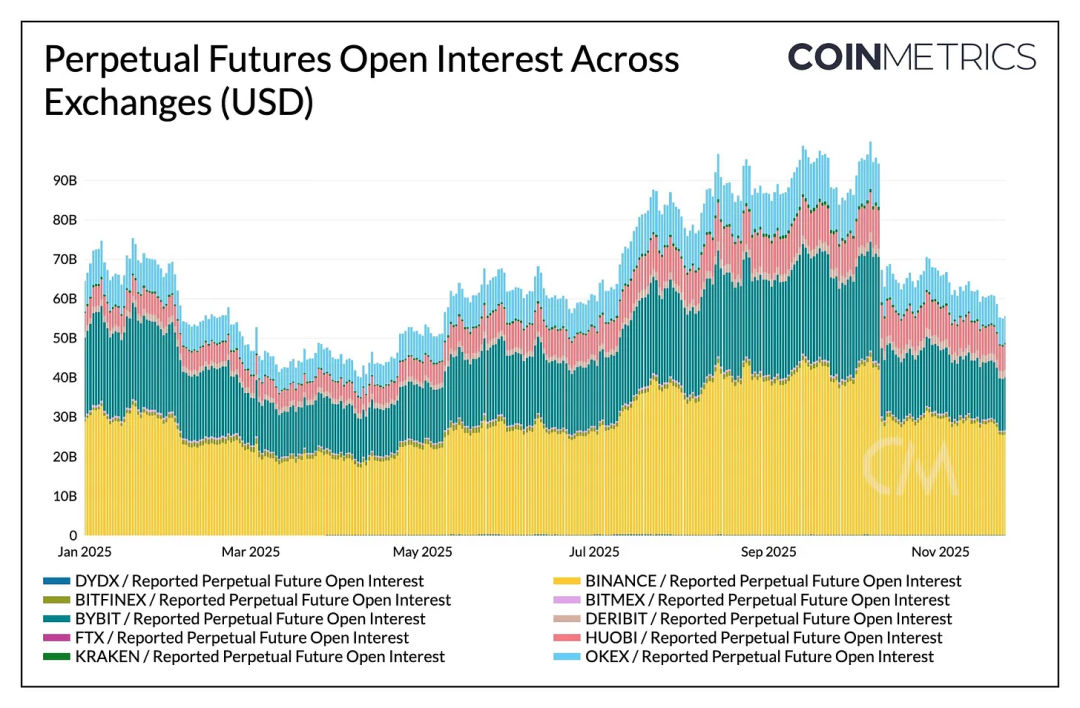

In just a few hours, perpetual futures experienced the largest forced deleveraging in history, wiping out over 30% of the open interest accumulated over months. Platforms with a high proportion of altcoins and retail (such as Hyperliquid, Binance, Bybit) saw the deepest declines, consistent with the aggressive leverage accumulated in these areas. As shown in the chart below, current open interest remains significantly below the pre-flash crash peak of over $90 billion and has since further declined slightly. This indicates that leverage within the system has been significantly cleansed, and the market has entered a phase of stabilization and repricing.

Funding rates have also declined in tandem, reflecting a reset in long positions' risk appetite. BTC funding rates have recently hovered around neutral or slightly negative, consistent with the market's lack of clear directional confidence.

DeFi Deleveraging

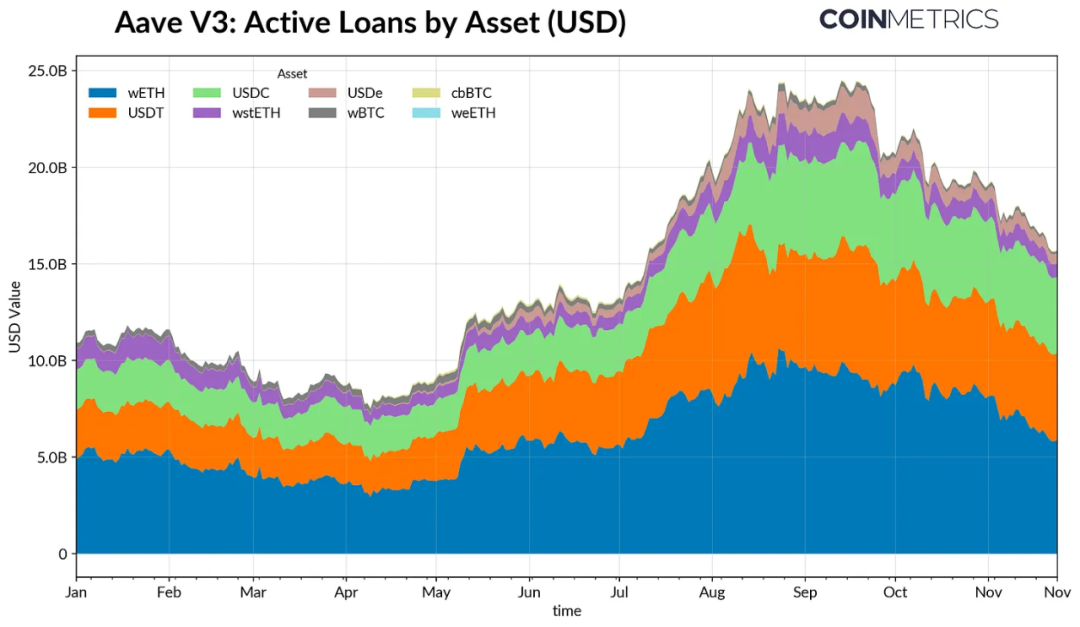

The DeFi lending market has also undergone a gradual deleveraging process. Active loans on Aave V3 have consistently declined since the peak at the end of September, as borrowers reduce leverage and repay debts. The contraction in stablecoin lending has been most pronounced, with USDe's depegging leading to a 65% decline in USDe lending, further triggering a liquidation chain for synthetic dollar leverage.

ETH-related lending has also contracted, with WETH and LST-related loans decreasing by 35-40%, indicating a significant exit from cyclical leverage and yield strategies.

Shallow Spot Liquidity

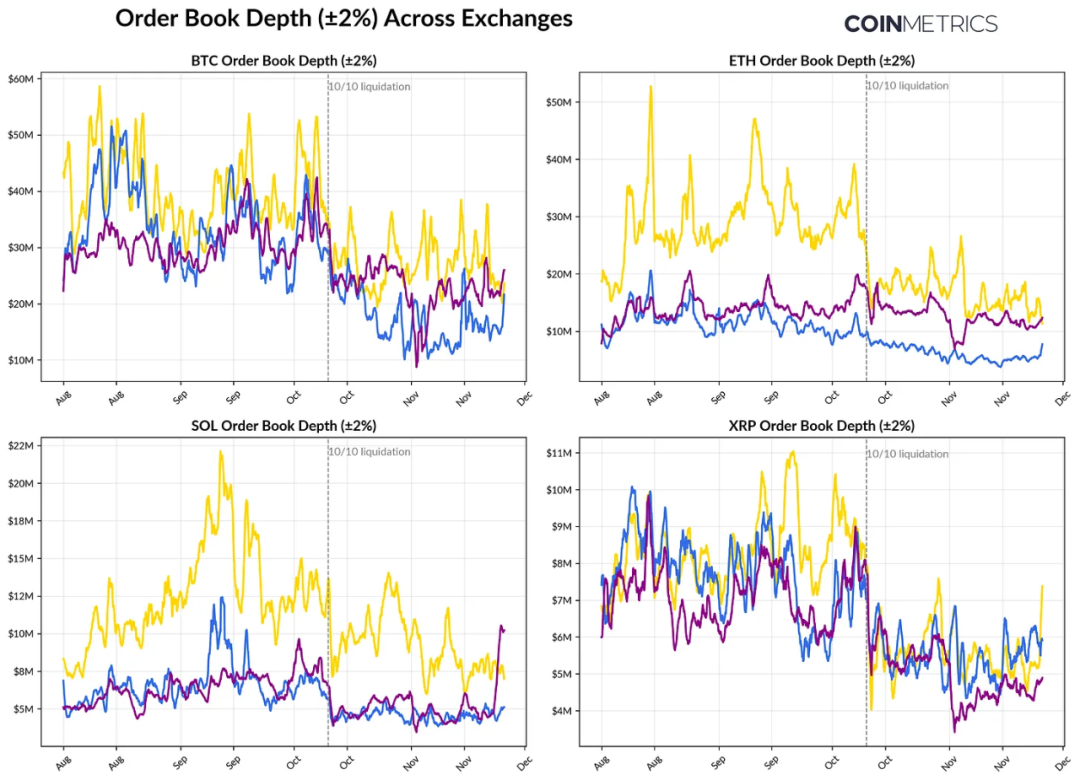

Spot market liquidity has failed to recover since the October 10 liquidation. The order book depth (±2%) on major exchanges remains 30-40% lower than early October, indicating that liquidity has not yet repaired as prices stabilize. With fewer orders, the market is more fragile, and minor trades can lead to excessive price shocks, exacerbating volatility and amplifying forced liquidation effects.

The liquidity situation for altcoins is even worse. The decline in order book depth outside of mainstream assets has been more significant and prolonged, indicating that the market continues to avoid risk and that market maker activity has decreased. If spot liquidity improves comprehensively, it could reduce price shocks and promote stability, but currently, the depth remains the most evident indicator that systemic pressure has not dissipated.

Conclusion

The digital asset market is undergoing a comprehensive recalibration, characterized by weak ETF and DAT demand, reset leverage in futures and DeFi, and shallow spot liquidity. These factors suppress prices but simultaneously make the system healthier: lower leverage, more neutral positions, and more important fundamentals.

Meanwhile, the macro environment remains a headwind: weakness in AI tech stocks, fluctuations in rate cut expectations, and declining risk appetite continue to suppress market sentiment. The market is only likely to stabilize and reverse when major demand channels (ETF fund flows, DAT accumulation, stablecoin supply growth) recover, along with a rebound in spot liquidity. Until then, the market will continue to be caught between the "macro environment of declining risk appetite" and "internal structural changes in the crypto market."

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。