The final results will be announced on January 15, 2026, and the market has already begun to vote with its feet.

Recently, Bitcoin has plummeted, and MicroStrategy is also facing tough times.

MSTR's stock price has dropped from a high of $474 to $177, a decline of 67%. During the same period, Bitcoin fell from $100,000 to $85,000, a drop of 15%.

What’s worse is the mNAV, which is the market value relative to the net asset value of Bitcoin.

At its peak, the market was willing to pay $2.5 for every $1 of Bitcoin held by MSTR; now that number is $1.1, with almost no premium left.

The previous model was: issue stock → buy Bitcoin → stock price rises (due to the premium) → issue more stock. Now that the premium has disappeared, issuing stock to buy Bitcoin has become a zero-sum game.

Why is this happening?

Of course, the recent sharp decline in Bitcoin is one reason. But MSTR's drop is much worse than BTC's, and there is a larger panic behind it:

MSTR may be kicked out of major global stock indices.

In simple terms, there are trillions of dollars in funds globally that are "passive investments." They do not pick stocks but mechanically buy all the components in the index.

If you are in the index, this money automatically buys you; if you are kicked out, this money must sell you, with no negotiation.

The decision-making power lies with a few large index companies, with MSCI being the most important one.

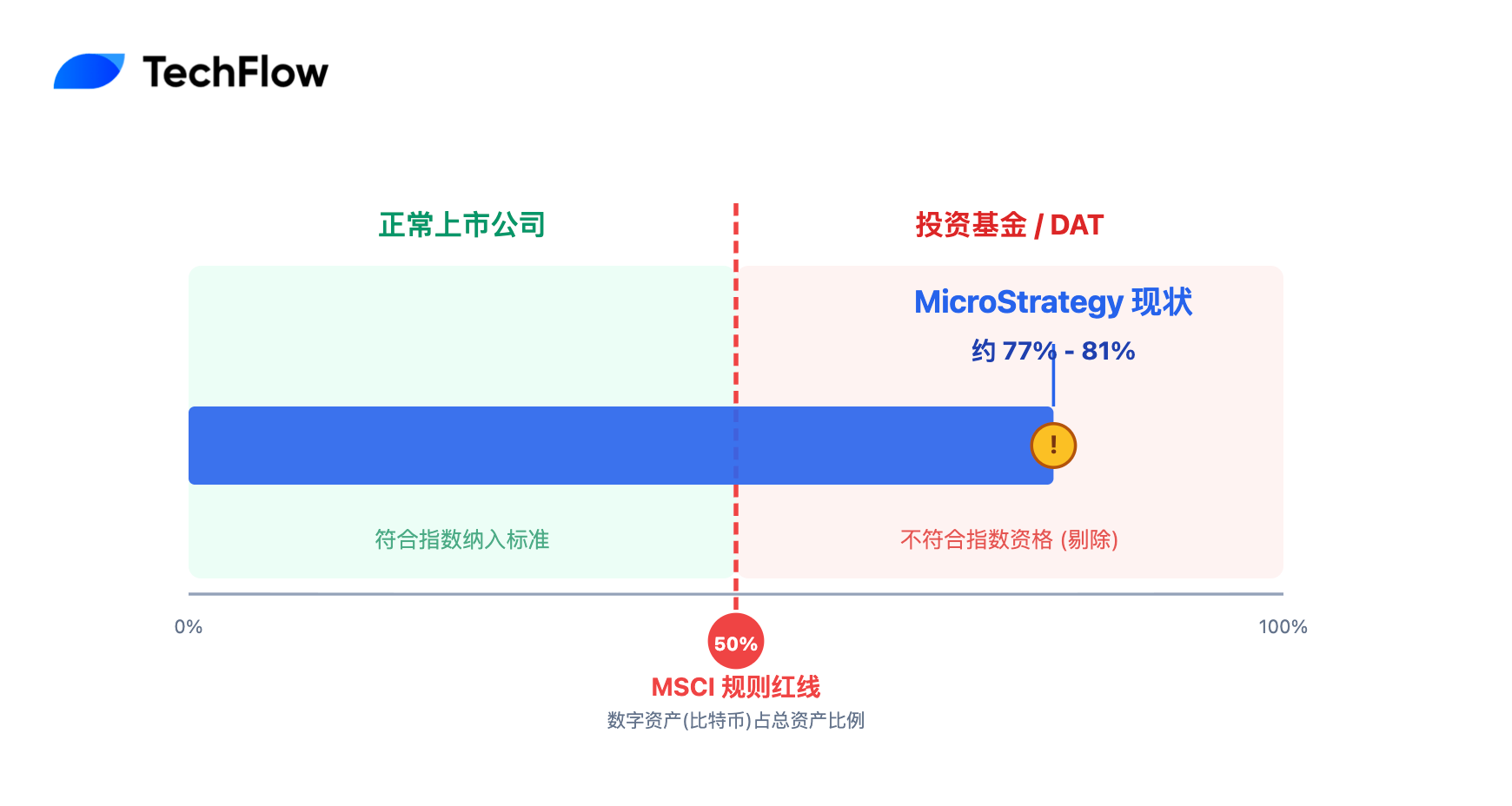

Currently, MSCI is considering a question: when a company has 77% of its assets in Bitcoin, can it still be considered a normal company? Or is it actually a Bitcoin fund disguised as a listed company?

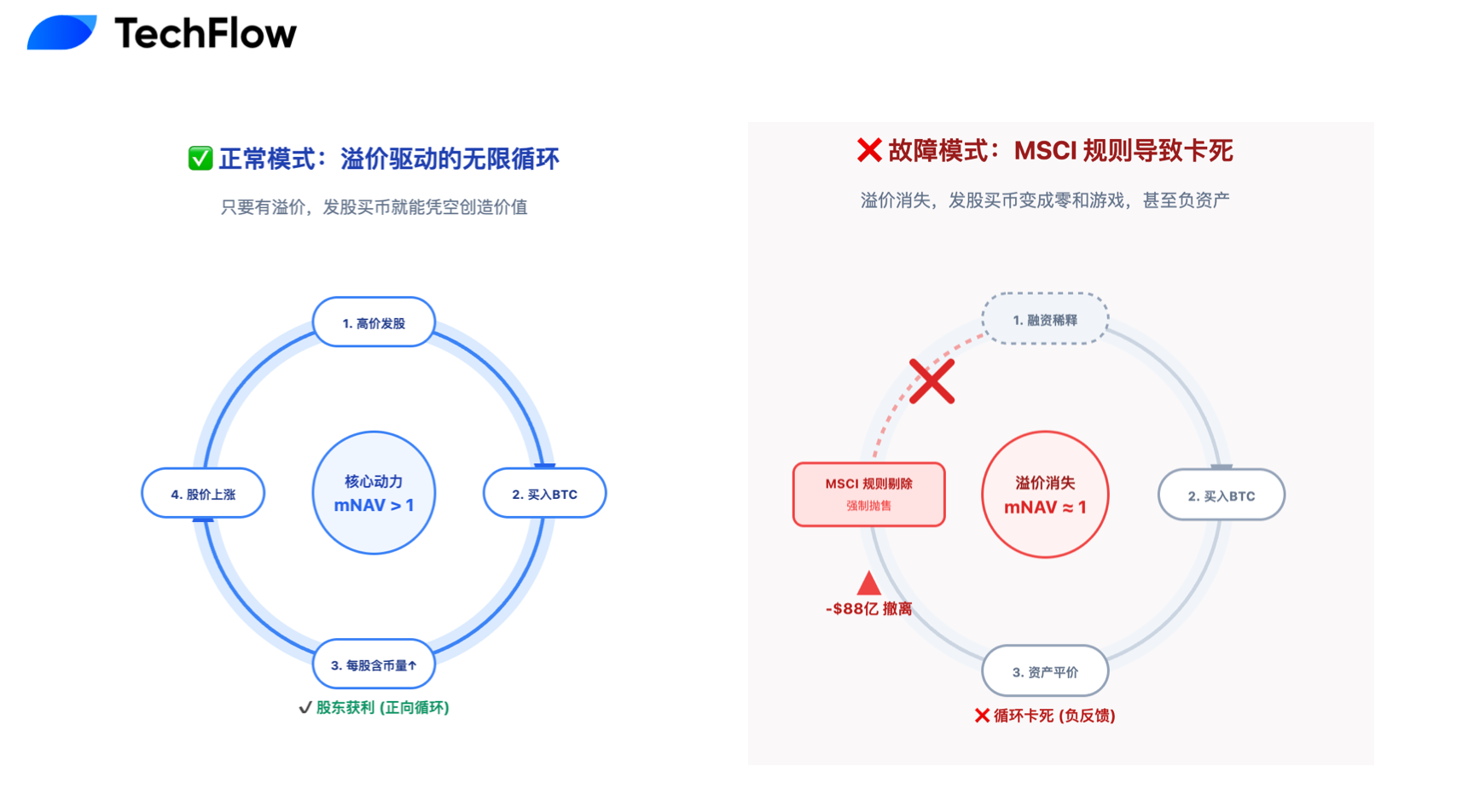

On January 15, 2026, the answer will be revealed. If MSTR is indeed kicked out, approximately $8.8 billion in passive funds will be forcibly withdrawn.

For a company that relies on issuing stock to buy Bitcoin, this is almost a death sentence.

When passive funds cannot buy MSTR

What is MSCI? Imagine it as the "college entrance examination question group" of the stock market.

Trillions of dollars in global pension funds, sovereign funds, and ETFs track indices compiled by MSCI. These funds do not conduct research or look at fundamentals; their task is to completely replicate the index—whatever is in the index, they buy; whatever is not in the index, they do not touch.

In September of this year, MSCI began discussing a question:

If a company's digital assets (mainly Bitcoin) exceed 50% of its total assets, can it still be considered a "normal listed company"?

On October 10, MSCI released a formal consultation document. The logic of the document is straightforward: companies holding large amounts of Bitcoin are more like investment funds rather than "operating enterprises." And investment funds are never allowed to enter stock indices, just as you wouldn't place a bond fund in a tech stock index.

What is MicroStrategy's current situation? As of November 21, the company holds 649,870 Bitcoins, worth approximately $56.7 billion at current prices. The company's total assets are about $73-78 billion. Bitcoin accounts for 77-81%.

This far exceeds the 50% red line.

Worse still, CEO Michael Saylor never hides his intentions.

He has stated in multiple public occasions that the quarterly revenue from the software business is only $116 million, and its main purpose is to "provide cash flow to service debt" and "provide regulatory legitimacy for the Bitcoin strategy."

What would happen if they were kicked out?

According to a research report from JPMorgan on November 20, if MSTR is only removed by MSCI, it will face about $2.8 billion in passive fund outflows. But if other major index providers (Nasdaq, Russell, FTSE, etc.) follow suit, the total outflow could reach $8.8 billion.

MSTR is currently included in several major indices: MSCI USA, Nasdaq 100, Russell 2000, etc. Passive funds tracking these indices hold approximately $9 billion worth of MSTR stock.

Once removed, these funds must sell. They have no choice; this is stipulated in the fund's charter.

What does $8.8 billion mean? MicroStrategy's average daily trading volume is about $3-5 billion, but this includes a lot of high-frequency trading. If $8.8 billion of one-way selling pressure is released in a short period, it would be equivalent to two or three consecutive days of only sell orders with no buy orders.

It is important to note that MSTR's average daily trading volume is $3-5 billion, but this includes high-frequency trading and liquidity provided by market makers. $8.8 billion of one-way selling pressure would mean that the total trading volume for 2-3 days would be all sell orders. The bid-ask spread would widen from the current 0.1-0.3% to 2-5%.

History tells us that index adjustments are ruthless.

When Tesla was added to the S&P 500 in 2020, the trading volume reached ten times its usual amount in one day. Conversely, when General Electric was kicked out of the Dow Jones index in 2018, its stock price fell by 30% within a month after the announcement.

The consultation period ends on December 31. On January 15 next year, the official ruling will be announced. Based on the current MSCI consultation document's rules, being kicked out seems almost certain.

The flywheel of issuing stock to buy Bitcoin is stuck

MicroStrategy's core strategy over the past five years can be simplified into a cycle: issue stock to raise money → buy Bitcoin → stock price rises → issue more stock.

The premise for this model to work is that the stock must have a premium. If the market is willing to pay $2.5 for every $1 of Bitcoin held by the company (mNAV = 2.5 times), then issuing new shares to buy Bitcoin can create value.

You dilute 10% of the shares, but the assets may increase by 15%, so shareholders overall still profit.

At its peak in 2024, MicroStrategy's mNAV did reach 2.5 times, even briefly touching 3 times. The market provided reasons for the premium, including Saylor's execution ability, first-mover advantage, and that this is a convenient channel for institutions to indirectly hold Bitcoin.

But now the mNAV has dropped to 1, essentially at par.

The market may have already begun to price in the possibility of MicroStrategy being removed from MSCI.

Once kicked out of the major indices, MicroStrategy would transition from a mainstream stock to a niche Bitcoin investment tool. A reference case is the Grayscale Bitcoin Trust (GBTC), which, after better Bitcoin ETFs emerged, went from a 40% premium to a long-term discount of 20-30%.

When the mNAV approaches 1, the flywheel stops turning.

Issuing $10 billion in new stock to buy $10 billion in Bitcoin means the company's total value remains unchanged. It’s just moving from one hand to the other, creating nothing except diluting existing shareholders.

The path of debt financing is still open; MicroStrategy has already issued $7 billion in convertible bonds. But debt must be repaid, and when the stock price falls, convertible bonds become a pure debt burden rather than quasi-equity.

Saylor's response and market views

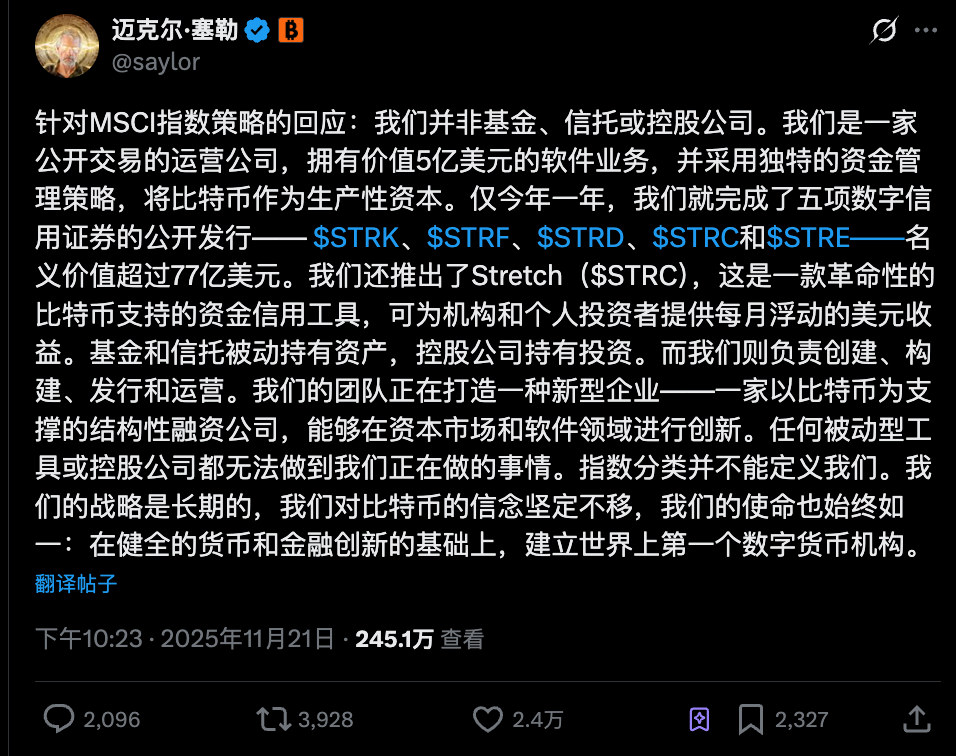

In response to the threat of potential removal by MSCI, Michael Saylor's response is very much in his style.

On November 21, he posted a lengthy article on X, with the core point being: MicroStrategy is not a fund, not a trust, and not a holding company. He used the art of language to evade MSCI's qualitative assessment:

"We are a publicly traded operating company with a $500 million software business that has adopted a unique Bitcoin capital strategy."

He emphasized that funds and trusts merely passively hold assets, while MicroStrategy is "creating, building, issuing, and operating." This year, the company completed five public offerings of digital credit securities: STRK, STRF, STRD, STRC, and STRE.

The implication is: we are not simply hoarding coins; we are engaging in complex financial operations.

But the market seems indifferent to these justifications.

MSTR's stock price trend has decoupled from Bitcoin; it is not that the correlation has decreased, but rather it has fallen even more sharply than Bitcoin. This likely reflects the market's concerns about its index status.

Cycle Capital partner Joy Lou posted pointing out that after being removed from the index, the average daily trading volume could plummet by 50-70% within 90 days.

What’s more concerning is the debt issue. MSTR has $7 billion in convertible bonds, with conversion prices ranging from $143 to $672. If the stock price falls to the $180-200 range, the debt pressure will increase dramatically.

Her conclusion is quite pessimistic. After liquidity dries up, the risk of MSTR falling below $150 will rise sharply.

Other community analyses also express pessimistic sentiments. For example, after MSTR is removed from the index, ETFs will automatically sell off, leading to a drop in stock prices that will drag down BTC, creating a vicious cycle of "Davis double kill."

The so-called "Davis double kill" refers to a sharp decline in stock prices caused by a drop in valuation and earnings per share.

Interestingly, these analysts all coincidentally mentioned one word: passive.

The passive selling by passive funds, passively triggering debt clauses, and passively losing liquidity. MSTR has transformed from an active Bitcoin pioneer into a passive victim of the rules.

The current consensus in the market is becoming clearer: this is not a matter of Bitcoin's rise or fall, but rather that the rules of the game have changed.

Saylor continues to insist on never selling coins in recent interviews. MSTR has proven that a company can go all-in on Bitcoin, but the MSCI index may be proving that the cost of doing so is being ostracized by the mainstream market.

Is DAT still a good business below the 50% red line?

MicroStrategy is not the only publicly traded company holding a large amount of Bitcoin. According to MSCI's preliminary list, there are 38 companies under observation, including Riot Platforms, Marathon Digital, Metaplanet, etc. They are all watching to see what happens on January 15.

The rules are clear: 50% is the red line. Exceeding it means you are a fund, not a company.

This draws a clear line for all DAT companies: either keep crypto holdings below 50% to remain in the mainstream market, or exceed 50% and accept the fate of being ostracized.

There is no middle ground. You cannot enjoy the passive buying from index funds while also turning yourself into a Bitcoin fund. MSCI's rules do not allow for such arbitrage.

This is a blow to the entire enterprise's approach to holding crypto assets.

Over the past few years, Saylor has been preaching, convincing other CEOs to add Bitcoin to their balance sheets. MSTR's success (with its stock price once rising tenfold) was the best advertisement, and now this advertisement is about to be taken down.

In the future, if companies want to hold large amounts of Bitcoin, they may need new structures. For example:

Establish independent Bitcoin trusts or funds

Hold indirectly by purchasing Bitcoin ETFs

Stay below the "safety line" of 49%

Of course, some believe this is a good thing. Bitcoin should not rely on the financial engineering of a single company. Let Bitcoin be Bitcoin, and let companies be companies, each to their own.

Five years ago, Saylor pioneered the corporate Bitcoin strategy. Five years later, this seems to be coming to an end with a boring financial document. But this may not be the end; rather, it forces the market to evolve into a new model.

Because of MSCI's 50% red line, MicroStrategy will not go bankrupt, and Bitcoin will not go to zero. But the era of unlimited "printing stock to buy Bitcoin" is over.

However, for investors still holding MSTR and various DAT company stocks, are you buying MSTR because you are optimistic about Bitcoin, or because you believe in Saylor as a person? If it's the former, why not just buy Bitcoin or ETFs directly?

After being kicked out of the index, MSTR will become a niche investment. Liquidity will decrease, and volatility will increase. Can you accept that?

The final results will be announced on January 15, 2026, and the market has already begun to vote with its feet.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。