If these were stocks, their trading prices would be at least 10 times higher, if not more.

Author: Jeff Dorman, CFA

Compiled by: Deep Tide TechFlow

Revealing the Discrepancy Between Fundamentals and Prices

In the crypto space, there are currently only three areas that consistently show growth: stablecoins, decentralized finance (DeFi), and real-world assets (RWAs). Moreover, these areas are not just growing; they are exhibiting explosive growth trends.

Take a look at the following charts:

- Growth of stablecoins (click to see more growth data):

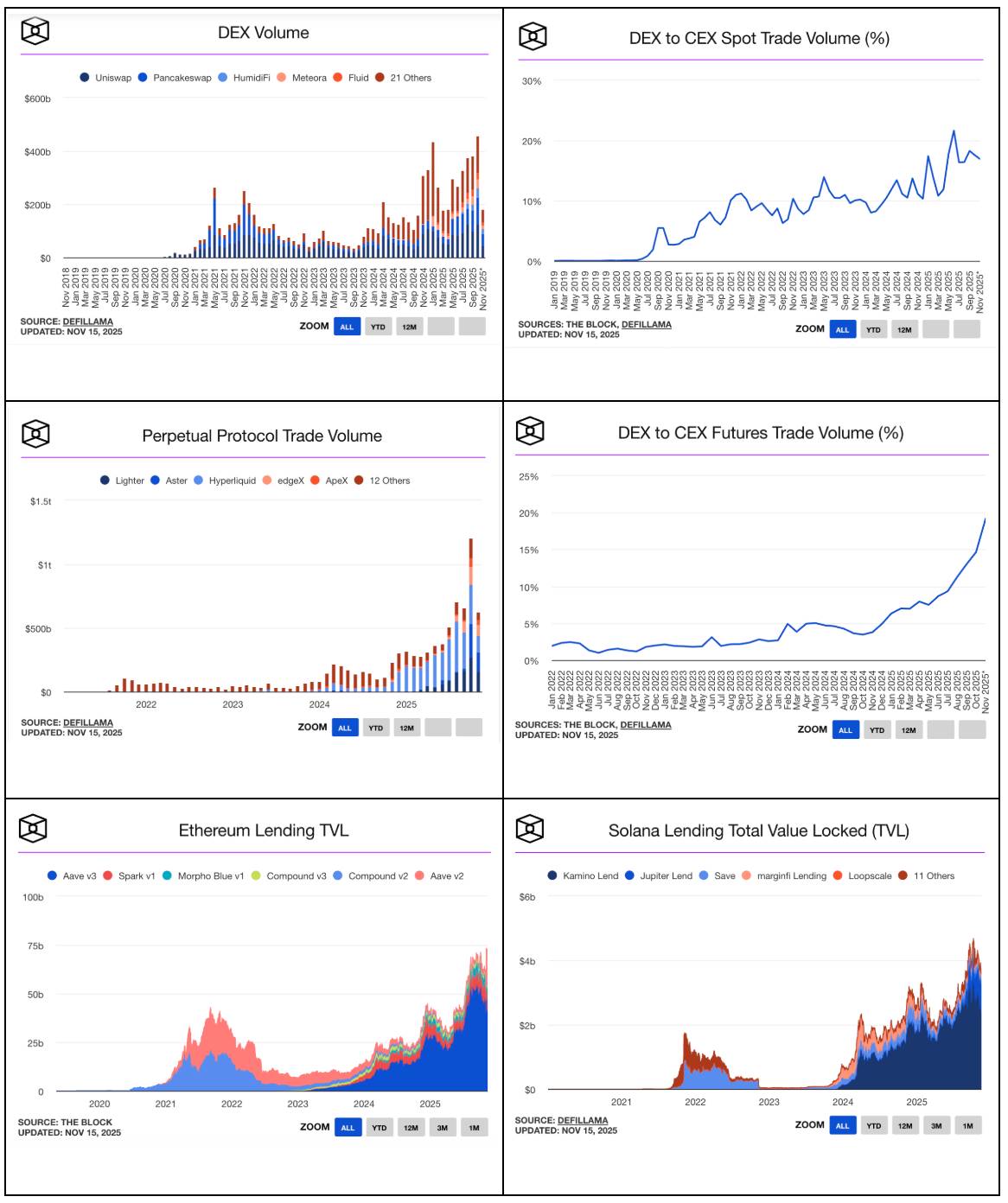

Growth of DeFi (click to see more data: here, here, and here):

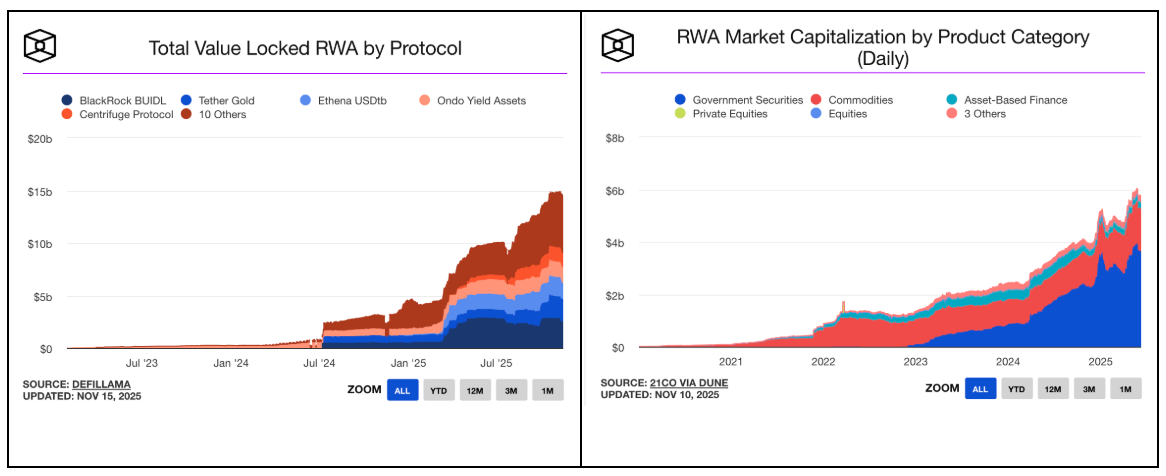

Growth of real-world assets (RWA) (click to see more data):

These are the applications that the crypto industry should be widely recognized for. The charts showing these growth trends should be featured on CNBC, The Wall Street Journal, and Wall Street research reports, and highlighted on every cryptocurrency exchange and crypto price page. Any objective growth-oriented investor seeing the growth in stablecoin assets under management (AUM) and trading volume, the expansion of RWAs, and the thriving data of DeFi would ask, “How should I invest in these areas?”

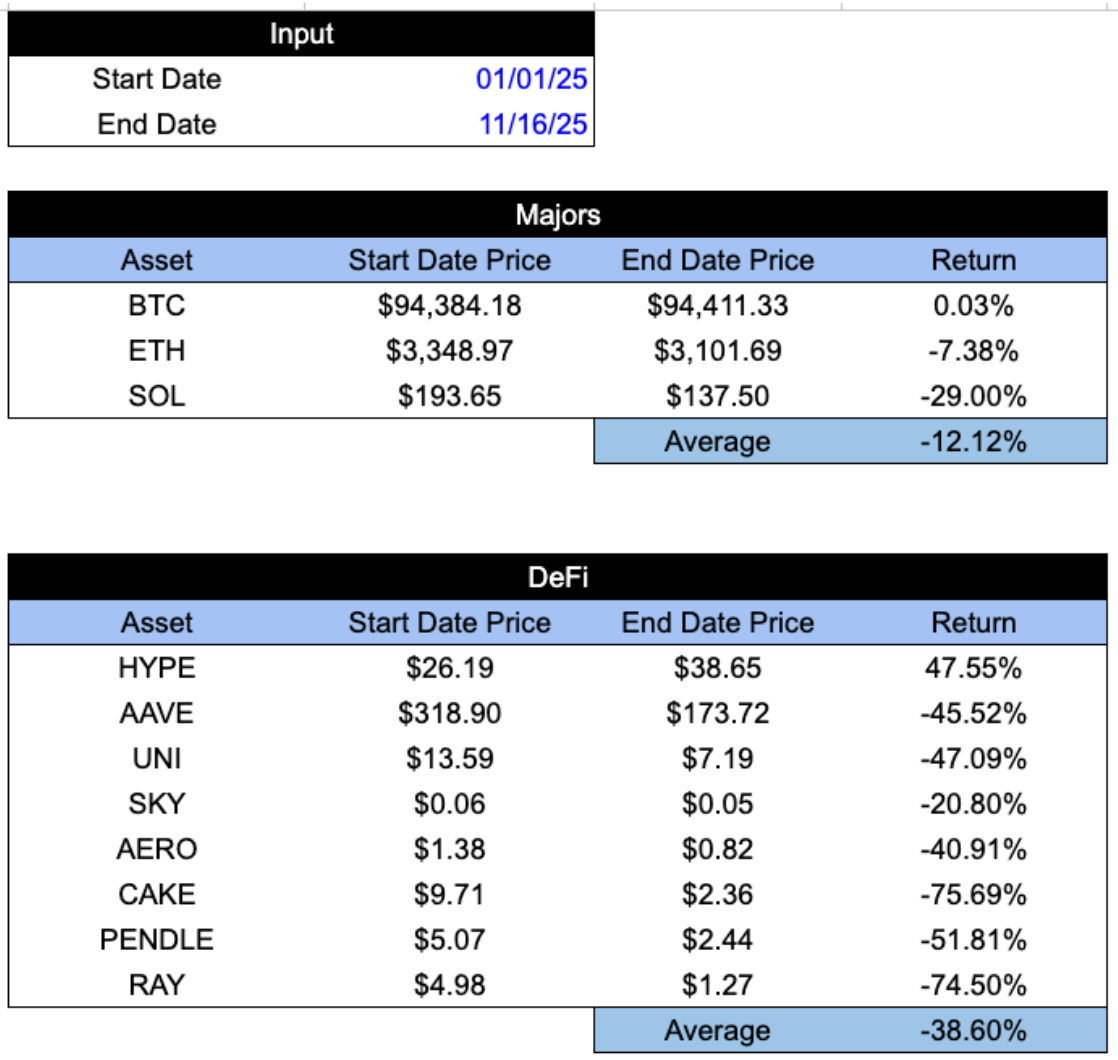

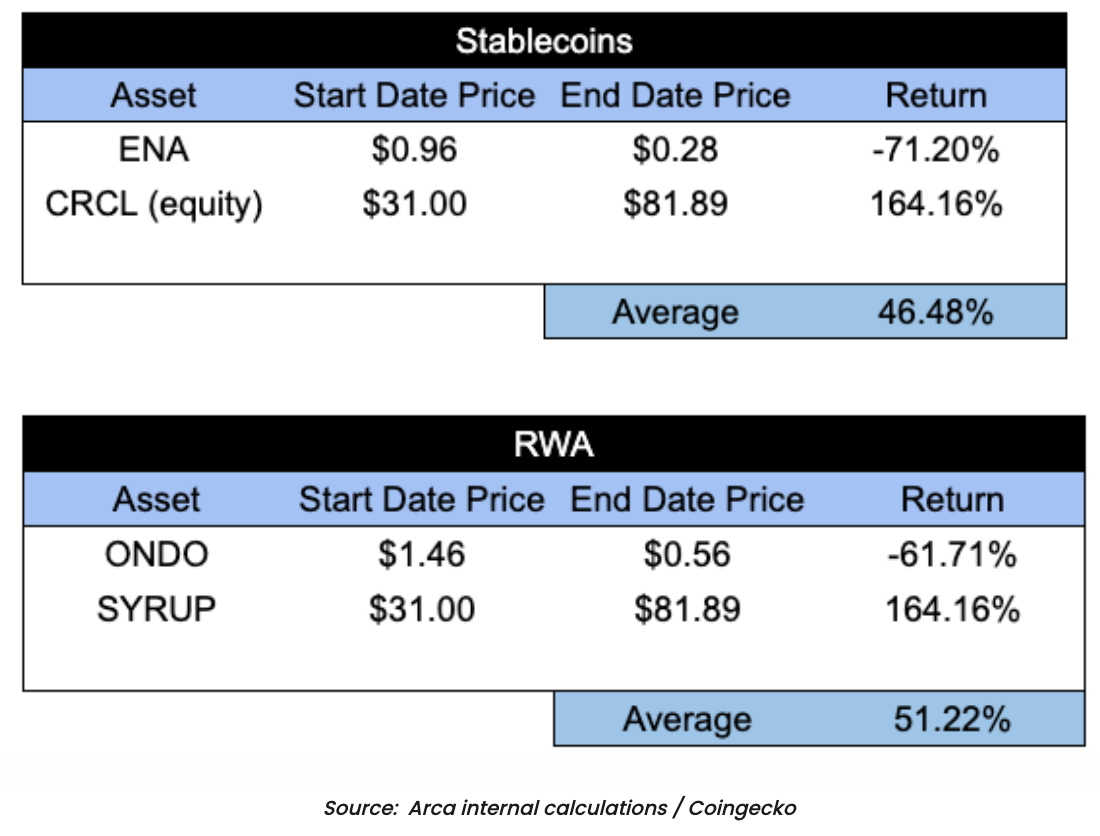

The growth trends in these industries are invariably “up and to the right.” And aside from stablecoins, all these areas can be easily invested in through tokens (e.g., HYPE, UNI, AAVE, AERO, SYRUP, PUMP, etc.). These decentralized applications (dApps) now account for over 60% of the total revenue in the crypto industry, yet the underlying tokens of these applications only make up 7% of the total market capitalization of crypto. Read that sentence again; it’s almost unbelievable.

Despite this, the media and exchanges continue to focus on Bitcoin and memecoins. Most investors still associate cryptocurrencies with Bitcoin (BTC), Layer-1 protocols (like ETH, SOL, and AVAX), and memecoins. However, the market has clearly shifted to focus on revenue and profits, yet many still fail to understand that tokens are actually excellent tools for capturing value and distributing profits.

Our industry has failed to attract those fundamental investors who value high cash flow and sustained growth, despite this investor group being the largest and most important globally. Instead, for some unknown reason, this industry has catered to the smallest and most irrelevant investor groups (like tech venture capital and fast-money macro/CTA funds).

Worse still, many people still believe that investing in stocks gives you some legal claim to the company's cash flow, while investing through tokens offers no ownership. I have pointed out this double standard between equity investors and crypto investors for over six years. As a shareholder, have you ever decided how the company spends its cash? Of course not. You cannot control how much the company pays its employees, how much it spends on R&D, whether it makes acquisitions, whether it buys back stock, or pays dividends. These decisions are entirely up to management. The only legal rights or protections you actually have as a shareholder are:

You have the right to receive corresponding proceeds when the company is sold (this is very important).

You have the right to receive the remaining assets after debts are deducted in the event of bankruptcy (but this is usually irrelevant, as creditors often receive all the equity post-restructuring, while shareholders get almost nothing).

You have the right to participate in proxy battles to overthrow management by joining the board (but this applies in crypto as well—over the past eight years, Arca has led three token activism campaigns, successfully forcing changes in crypto companies like Gnosis, Aragon, and Anchor).

Ultimately, whether as a shareholder or a token holder, you are subject to management's decisions on how to use cash flow. Whether stocks or tokens, aside from acquisitions, you always rely on management to decide how to utilize the company's cash flow, such as whether to buy back shares. There is no essential difference between the two.

Hyperliquid (HYPE) and Pump.Fun (PUMP) have already demonstrated the market appeal of capturing value based on real earnings and burn mechanisms. Many mature projects, such as Aave, Raydium, and PancakeSwap, have also integrated similar mechanisms. Last week, Uniswap (UNI) made headlines for finally launching its "fee-sharing" feature, allowing UNI holders to share in a portion of the protocol's revenue.

This further proves that the market is changing. In just 2025, crypto protocols and companies have conducted over $1.5 billion in token buybacks, with ten tokens accounting for 92% of the total buyback volume. (However, we believe the ZRO data in this article is incorrect, as the buyback amounts for HYPE and PUMP are far higher than the data indicates.)

To better understand this phenomenon, the total market capitalization of the entire liquidity crypto market (excluding Bitcoin and stablecoins) is only $1 trillion. The $1.5 billion in token buybacks accounts for just 0.15% of the total market value. But if we look solely at the tokens with the largest buyback amounts, their buyback amounts can account for as much as 10% of their market capitalization. In contrast, the total stock buybacks in the U.S. stock market this year are about $1 trillion, accounting for 1.5% of the $67 trillion market capitalization.

This cognitive gap regarding crypto investment and value capture is very significant. On one hand, it can be said that most tokens have no investment value at all; but on the other hand, the highest quality tokens are severely undervalued, likely due to being dragged down by inferior assets. The result is that in many cases, project growth and revenue metrics are on the rise, while token prices are on the decline. Among the three fastest-growing sectors contributing the most revenue and buybacks, many top tokens are performing exceptionally poorly.

The question remains: why haven’t more leaders in the crypto industry focused on promoting those areas that are truly achieving growth? Shouldn’t this industry showcase the tokens from these areas, highlight their excellent tokenomics, and explain to investors how to invest in them? Investors need to understand that there is logic and fundamentals behind crypto investments, so they will be willing to spend time researching these investments. If we want high-quality tokens to outperform low-quality tokens, we must start educating people on how to identify quality tokens.

A few years ago, there were almost no crypto products generating significant revenue. Today, many projects not only create substantial revenue but also use a large proportion of it (sometimes up to 99%) for token buybacks. Additionally, compared to traditional stocks, these tokens are trading at extremely low prices. In fact, these tokens are essentially stocks, just lacking an educated and committed buyer base.

So, if these assets were indeed stocks, what prices would they trade at? If investors could understand the difference between these income-generating and buyback tokens and “cryptocurrencies” or “smart contract protocols,” what prices would they trade at?

Let’s illustrate this with two of the best cases in the market:

Hyperliquid (HYPE) and Pumpfun (PUMP)

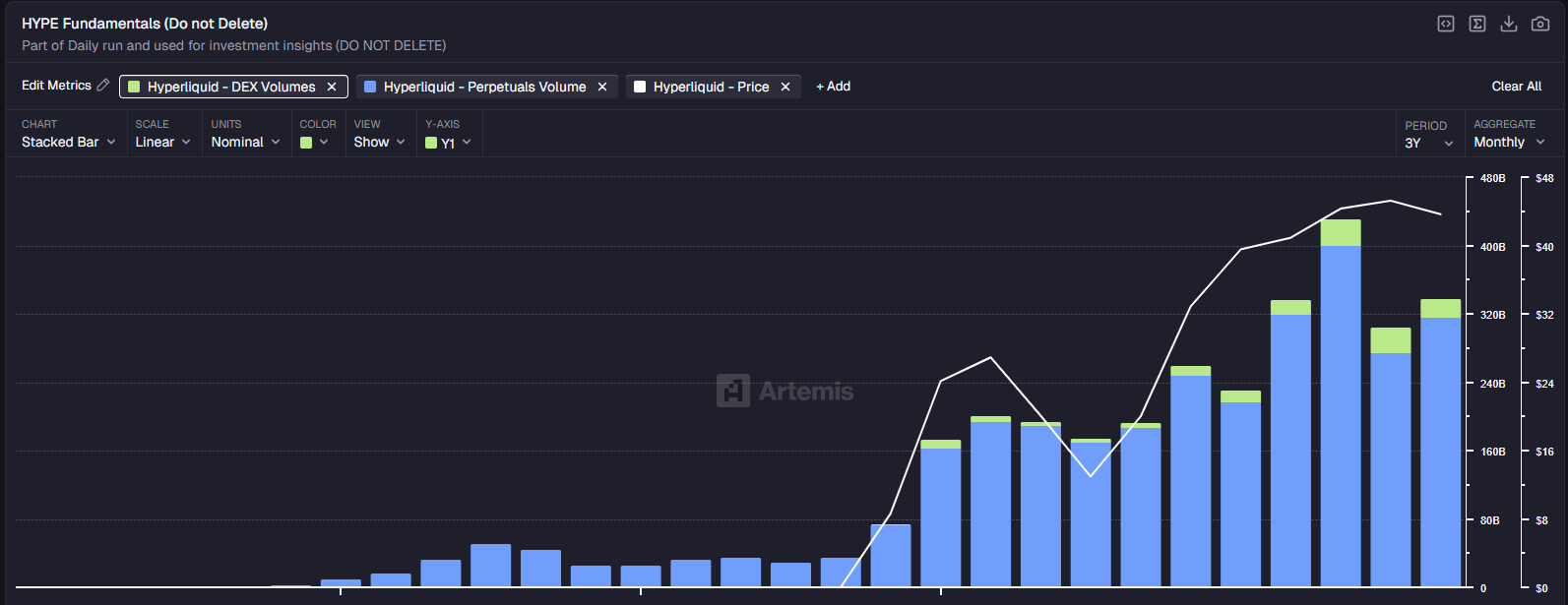

Hyperliquid has already become a leader in decentralized perpetual contract exchanges, with nearly all indicators showing that this company is growing rapidly and steadily.

Volume Growth:

Source: Artemis

Fees:

Source: Artemis

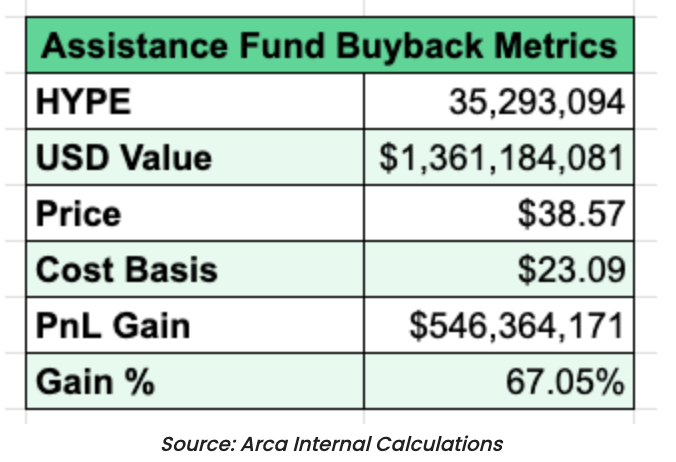

Due to the growth in volume and fees, Hyperliquid has become one of the cheapest tokens under traditional valuation models. HYPE has an annualized revenue of $1.28 billion (based on the past 90 days), with a price-to-earnings (P/E) ratio of only 16.40, and a year-on-year growth of 110%. More impressively, the project uses 99% of its revenue for token buybacks. To date, HYPE has repurchased over 10% of its circulating tokens (HYPE has repurchased tokens worth $1.36 billion). This is not only one of the most successful cases in crypto history but also in the history of the overall financial market.

In contrast, the S&P 500 has a P/E ratio of about 24, and the Nasdaq about 27. Coinbase has a P/E ratio of around 25, while Robinhood (HOOD) has a P/E ratio as high as 50, but its revenue is only twice that of HYPE (about $2 billion, while HYPE is $1 billion).

HYPE's year-to-date growth rate is even faster (110% compared to Robinhood's 65%).

Moreover, Hyperliquid is also a Layer-1 protocol, a feature that the market has not fully priced in. Currently, the market simply views HYPE as an exchange.

More importantly, every dollar of revenue from HYPE is distributed to token holders through buybacks, while Robinhood has neither a buyback plan nor a dividend policy.

This either means the market expects Hyperliquid's growth to significantly slow down and lose market share, or it means the market is overlooking some key factors. The valuation of HYPE being lower than that of Robinhood (HOOD) is somewhat reasonable: the HYPE token has only been launched for a year and faces fierce competition, while digital assets typically lack a clear moat. However, HOOD's P/E ratio is five times that of HYPE, while growing at a slower rate and having lower profit margins; this gap seems overly exaggerated and is more likely due to the maturity of stock investors being far higher than that of crypto investors, rather than an issue with the assets themselves.

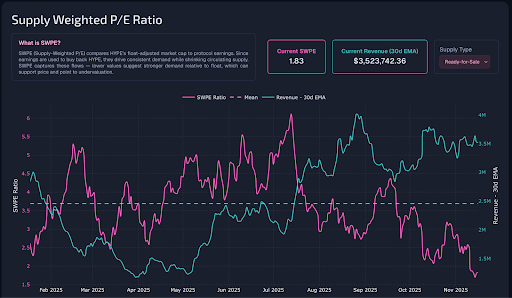

In any other industry, if you saw the situation depicted in the chart below—where earnings continue to grow while prices are falling—you would likely invest all your funds into that investment without hesitation.

Source: Skewga

Now let’s take a look at Pumpfun (PUMP). Similar to Hyperliquid, Pumpfun's business model is also very straightforward. Pumpfun helps token issuers launch tokens and charges fees through the issuance and subsequent trading of those tokens.

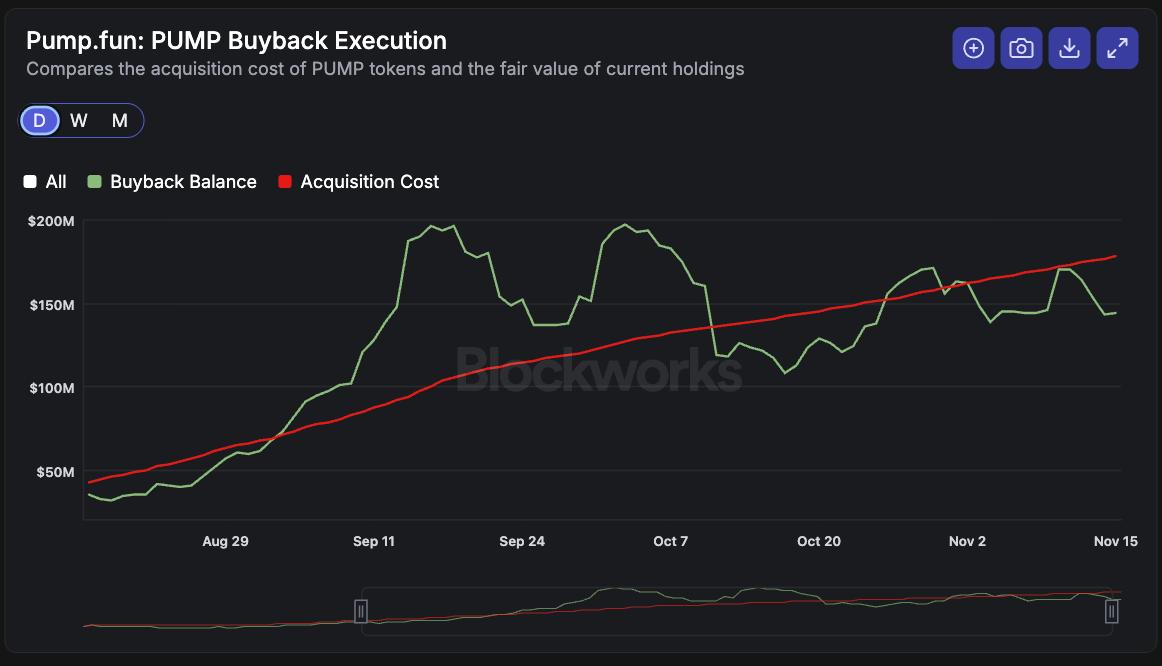

This is also one of the most successful cases in crypto history, with past revenues exceeding $1 billion.

Source: Blockworks

The PUMP token had its initial coin offering (ICO) earlier this year at a price of $0.004. Although the maximum supply is 1 trillion tokens, only 590 billion are currently in circulation. In less than four months, Pumpfun has already repurchased 3.97 billion PUMP tokens and used 99% of its revenue for token buybacks. Based on adjusted market capitalization, PUMP's P/E ratio is only 6.18 (with all earnings used for buybacks).

Source: Blockworks

Frankly, we have never seen companies like Pumpfun and Hyperliquid grow so rapidly, let alone that they return almost all of their free cash flow to investors. These are some of the most successful cases in investment history and the most outstanding tokens in crypto history.

If these were stocks, their trading prices would be at least 10 times higher, if not more. Unfortunately, the investor base has not matured yet. So, those who can recognize this value can only choose to wait. The issue does not lie with the assets themselves, nor with the mechanism of value transfer.

Education is the main problem.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。