Author: Zhou, ChainCatcher

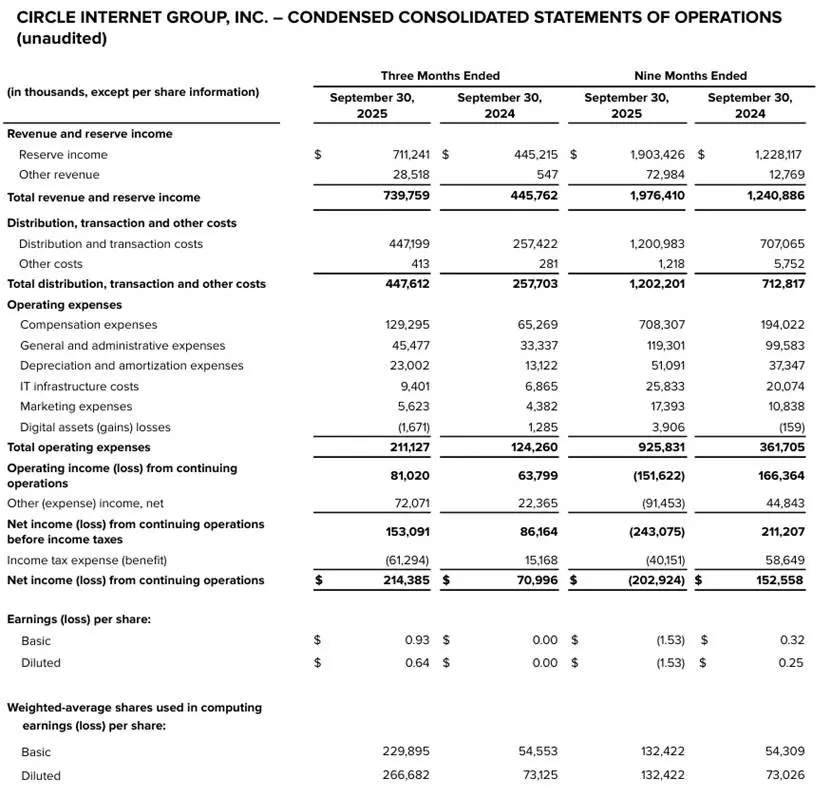

Circle released its Q3 2025 financial report on November 12, reporting total revenue of $740 million, a year-on-year increase of 66%; net profit reached $214 million, a year-on-year increase of 202%.

Previously, institutions expected revenue of $700 million and EBITDA of $31 million, and the financial report data significantly exceeded expectations. However, due to the company's update of its full-year expense guidance, raising the 2025 operating expense forecast to between $495 million and $510 million, this change raised market concerns about its cost control and future profitability, leading to a drop of about 12.21% in CRCL on the day, closing at $86.3, with a total market value of about $20 billion.

Since its IPO at a price of $31 in June 2025, Circle's stock price has experienced significant fluctuations, falling from a high of $298.99 to the current $86.3, with a total market value shrinking by over 70%.

Additionally, according to regulatory documents, the stock lock-up period for company executives and internal shareholders may end as early as this Friday. Typically, the lock-up period after an IPO is 180 days and should end in early December. This means that a large amount of stock held by insiders may soon flood the market, creating potential selling pressure.

Financial Report Breakdown: Reserve Income Up 60% Year-on-Year, Operating Expense Guidance Raised

Breaking down the financial report by business, Circle's main source of income is reserve income, which is the income from investing USDC reserve funds in short-term government bonds and other assets, so the growth of USDC circulation directly determines the revenue ceiling. By the end of Q3, the circulating USDC reached $73.7 billion, doubling year-on-year; reserve income reached $711 million, a year-on-year increase of 60% and a quarter-on-quarter increase of 12%, mainly due to a 97% increase in the average balance of circulating USDC, although this was partially offset by a 96 basis point decline in the return on reserve assets. Since short-term government bond yields are affected by interest rates, if interest rates continue to decline in Q4, it may weaken the elasticity of this interest income.

Despite this, Circle's Chief Financial Officer Jeremy Fox-Geen refuted the view that declining interest rates are unfavorable for the company. He stated that lower interest rates would lead to stronger economic activity, more risk-taking, and increased investment, which would benefit the company's business in the short term.

The second part of other income benefited from strong subscription and service revenue, driving other income to $29 million, a year-on-year increase of over 10 times.

Additionally, the company's new business layout may contribute to future performance growth. Among them:

- Circle announced the launch of the Arc public test network on October 28. Arc is a Layer-1 blockchain designed to help developers and enterprises leverage programmable financial infrastructure to bring more economic activities on-chain. The network has attracted over 100 companies to participate, and Circle is also exploring the possibility of issuing a native token on the Arc Network.

- The Circle Payment Network (CPN) enables cross-border payments through USDC/EURC, with 29 financial institutions already joined, another 55 under qualification review, and 500 more in preparation. Since its launch at the end of May this year, CPN's business activity has grown rapidly, with an annualized transaction volume reaching $3.4 billion as of November 7, 2025, based on the past 30 days of trading activity.

- Circle's tokenized money market fund USYC has grown by over 200% from June 30, 2025, to November 8, 2025, reaching approximately $1 billion.

These new business developments inject momentum into Circle's revenue diversification but also come with higher operational cost investments. The company has raised its full-year adjusted operating expense guidance range to $495 million to $510 million, increasing investment in platform construction, capability building, and global partnerships.

On the cost side, the company's distribution and trading costs in Q3 reached $448 million, a year-on-year increase of 74% and a quarter-on-quarter increase of 10%, mainly due to the increase in USDC circulating balance and the average USDC holdings on the Coinbase platform, driving distribution payments growth, which includes expenses related to other strategic partnerships.

Intense Competition in the Stablecoin Space, New Business Layout Breakthrough

In terms of competitive landscape, the total market value of stablecoins has surpassed $310 billion, with Tether holding nearly 60% market share, with a circulation of about $184 billion, dominating the market; Coinbase locks in Circle's revenue through a 50% revenue-sharing agreement while acquiring Deribit to expand its derivatives business; PayPal's PYUSD focuses on instant settlement scenarios, with merchant adoption increasing by 300%.

Additionally, traditional banks have also become a significant variable. JPMorgan launched the JPMD token, Fiserv issued FIUSD on Solana, and Mastercard initiated a stablecoin payment network. These players are rapidly capturing the enterprise market, leveraging low costs and existing trust, catalyzed by the GENIUS Act.

It is worth noting that the company has long viewed compliance as a core competitive advantage, with 20% of employees engaged in compliance-related work. However, this compliance advantage now faces dilution risks. As global regulatory frameworks mature, compliance is shifting from a moat for a few players to an industry standard. With the implementation of regulations like the EU's MiCA and the US's GENIUS Act, traditional banks and payment giants are accelerating their entry, making licenses no longer scarce.

Overall, Circle delivered a decent report for Q3, with both revenue and net profit significantly increasing, USDC scale and transaction volume reaching new highs, and progress in both Arc and the payment network. However, the short-term stock price pressure reflects the market's sensitivity to costs, lock-up releases, and competition. Additionally, Circle must face multiple risks from customer concentration, declining interest rates, and large institutions issuing stablecoins independently.

In the increasingly heated stablecoin space, the company's new business layout is not just an embellishment but a lifeline. Otherwise, USDC may only remain at the ceiling of high-interest deposits, with growth potential locked by the interest rate environment, and payment scenarios being divided by traditional banks and old players. In this view, Circle's transformation has entered deep waters.

Click to learn about job openings at ChainCatcher

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。