Unless multiple "black swan events" occur simultaneously, USDe remains safe.

Written by: The Smart Ape

Translated by: AididiaoJP, Foresight News

More and more people are beginning to worry about whether USDe is truly safe, especially after the recent decoupling.

The decoupling has triggered a lot of FUD sentiment, making it difficult to remain objective. The goal of this article is to clearly and factually examine @ethena_labs. With all the information at hand, you can form your own opinion rather than follow those who may have biases or hidden interests.

USDe Decoupling

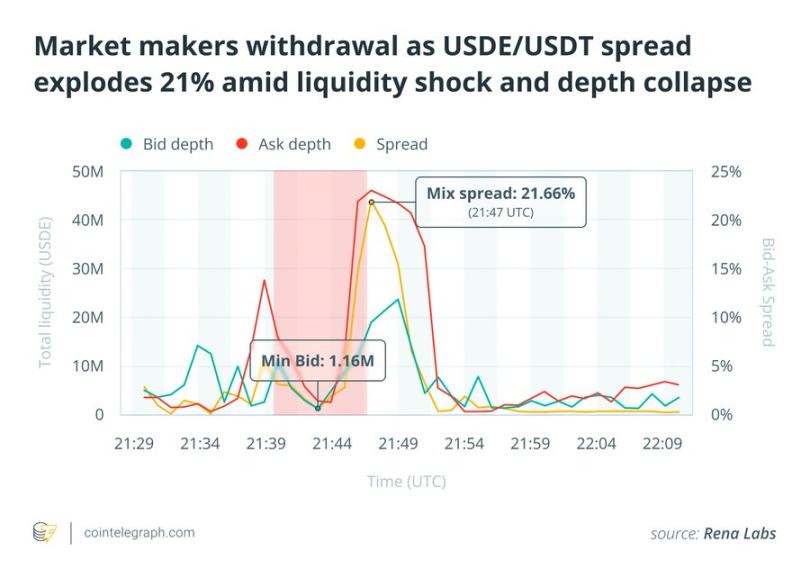

On the night of October 10, USDe severely decoupled, and I panicked when I saw it drop to $0.65.

However, the decoupling only occurred on @binance. In liquidity venues with better depth, such as Curve and Bybit, USDe hardly fluctuated for long, bottoming out around $0.93, and quickly recovered.

Why Binance?

Because Binance allows users to use USDe as collateral and uses its own internal order book (rather than external oracles) to assess the value of that collateral.

Some traders exploited this flaw, dumping $60 million to $90 million worth of USDe, driving the local price down to $0.65 and triggering $500 million to $1 billion in forced liquidations, as these assets were used as margin.

In short, the issue is not related to Ethena's fundamentals but rather to Binance's design. This situation could have been avoided with oracle-based price feedback.

Will USDe Collapse Like UST?

Many people compare Luna or UST with Ethena, but fundamentally, they are two completely different systems.

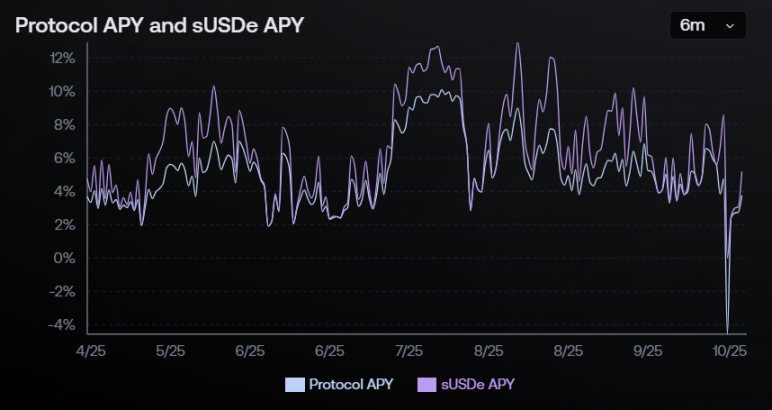

First, Luna had no real income, but Ethena does. It earns revenue through liquidity staking and perpetual funding rates.

Luna's UST was backed by its own token $LUNA, which means it had no real support. When LUNA collapsed, UST followed suit.

Ethena is supported by delta-neutral positions, not by ENA or any tokens related to Ethena.

Unlike Anchor's fixed 20% annualized rate, Ethena does not guarantee any yield; it fluctuates with the market.

Finally, Luna's growth was unlimited, with no mechanism to slow down expansion. Ethena's growth is limited by the total open contract volume on exchanges. The larger it becomes, the lower the yield, which helps maintain its scale.

So, Ethena and Luna are completely different. Ethena may fail, like any protocol, but it will not fail for the same reasons that Luna did.

What Are the Risks of Ethena?

Every stablecoin carries risks, even USDT and USDC have their own vulnerabilities. It is important to understand what these risks are and how severe you think they might be.

Ethena relies on delta-neutral strategies:

Long positions established through liquidity staking or lending protocols (BTC, ETH),

And short positions established through perpetual contracts on centralized exchanges.

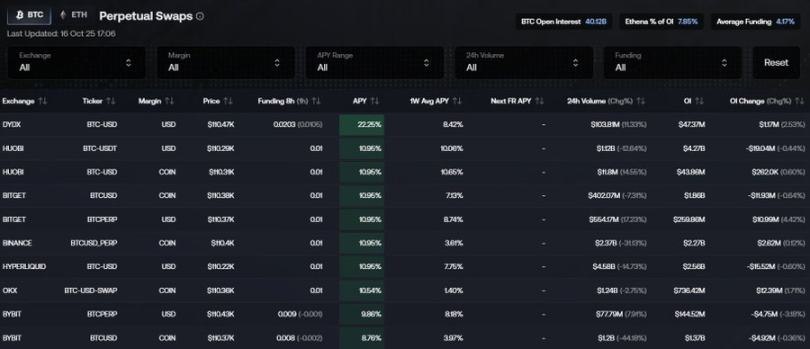

For me, the biggest risk is if major exchanges (Binance, Bybit, OKX, Bitget) crash or freeze withdrawals, Ethena will lose its hedge, leading to an instant decoupling.

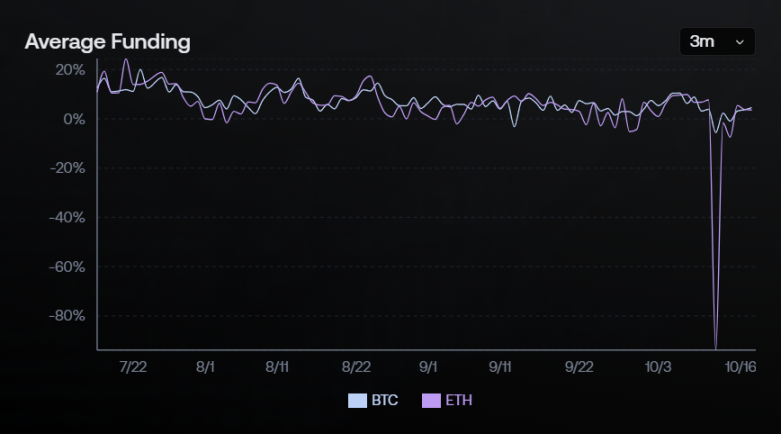

There is also funding rate risk. If the funding rate is negative for an extended period, Ethena will consume capital rather than earn revenue. Historically, the funding rate has been positive over 90% of the time, which can offset brief negative periods.

USDe will also undergo re-basing, minting new tokens when the protocol earns revenue, which could cause slight dilution if the market turns and the value of collateral decreases. So over time, this could lead to slight under-collateralization.

Ethena also operates in a high-leverage ecosystem. A large-scale deleveraging event (like the chain liquidations on October 10) could disrupt hedging or trigger forced liquidations.

Finally, all of Ethena's perpetual short positions are denominated in USDT, not USDe. If USDT decouples, USDe will also decouple. Ideally, perpetual contracts should be denominated in USDe, but convincing Binance to change the BTC/USDT trading pair to BTC/USDe seems impossible to me.

These are the main risks currently debated around Ethena.

Risk Assessment

The previous list may sound daunting, but the probability of these events occurring simultaneously is extremely low. You would need a long-term negative funding rate environment, simultaneous exchange crashes, and a complete liquidity freeze, which is statistically unlikely.

You can think of it like rolling dice: the probability of rolling a "1" is one in six, but the probability of rolling a "1" and then a "2" is one in thirty-six. This is how combinatorial probability works here.

Ethena was built after the Terra and FTX events, learning from those lessons. It has reserve funds, off-chain custody, floating yields, and is integrating oracle-based pricing.

In reality, the most likely outcome is not a collapse, but occasional anchoring fluctuations during periods of market stress, like what we saw on Binance, but without triggering broader contagion. Even in severe events, it will affect the entire perpetual and synthetic stablecoin market, not just USDe.

Remember, Ethena has already survived the largest liquidation event in cryptocurrency history without losing its peg, passing a real stress test.

Its collateral is on-chain and transparent, unlike many "mystery basket" stablecoins supported by obscure off-chain reserves.

Frankly, many of the stablecoins currently in circulation are much riskier than Ethena, and we hold Ethena to a higher standard simply because of its scale and visibility.

My Personal Opinion

Personally, I believe USDe does not face significant decoupling risks, which would require multiple disasters to occur simultaneously. And if it does happen, it will not drop alone.

There are still stablecoins in the market with much higher risks that maintain huge market capitalizations.

If USDe survived the record liquidation day in October unscathed, it speaks volumes about its resilience.

Therefore, I do not think Ethena is particularly dangerous, certainly not more dangerous than other stablecoins.

They are also one of the few projects innovating in the stablecoin space, and based on current results, this innovation is effective.

As always, do not put all your eggs in one basket. Diversify your stablecoin exposure, stay informed, and relax.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。