Chaebols dominate, rapidly advance, and prioritize practicality; South Korea has its own development model for the cryptocurrency industry.

Written by: Deep Tide TechFlow

Korea Blockchain Week (KBW) is in full swing in Seoul, and the eyes of cryptocurrency practitioners are focused on South Korea.

At this moment, according to a report by the Korean media Dong-A Ilbo on Thursday, South Korean internet giant Naver plans to swap shares with Dunamu, the parent company of Upbit, which will make Dunamu a subsidiary.

This means that South Korea's largest internet company will control the country's largest cryptocurrency exchange.

Currently, the South Korean cryptocurrency market is indeed experiencing an unprecedented period of activity.

The user accounts of the five major exchanges in South Korea have surpassed 9.6 million, accounting for about 18.7% of the total population. Upbit holds over 80% of the market share, with daily trading volumes often exceeding $10 billion. The Korean won has become the second-largest fiat currency for cryptocurrency trading globally, after the US dollar.

Earlier this month at the Upbit Developer Conference, Dunamu just launched its Web3-based blockchain GIWA Chain and GIWA Wallet; this Layer 2 solution based on OP Rollup technology showcases Upbit's technological ambitions.

(See related article: Upbit enters the public chain race; how ambitious is Giwa's on-chain vision?)

Now, this share swap transaction is not without warning.

In July, the two parties announced a collaboration to develop a Korean won stablecoin; in September, Naver acquired 70% of the shares in Dunamu's securities trading platform. In hindsight, these moves seem to be a prelude to a full acquisition.

Dunamu is currently valued at approximately 8.26 trillion won ($6 billion). If the transaction is completed, it will be the largest merger and acquisition in the history of South Korea's cryptocurrency industry.

Who is Naver? The Korean version of Google + Tencent

Naver is South Korea's largest internet company, with a market capitalization of about $50 billion.

In South Korea, Naver's status is comparable to that of Google and Tencent. It monopolizes 70% of the search engine market and has built a vast internet ecosystem through its various products.

Most Chinese-speaking users may not be familiar with the name Naver, but they must know LINE. LINE is a subsidiary of Naver, with over 200 million users in Japan and Southeast Asia, making it one of the largest instant messaging applications in Asia.

Naver's business scope extends far beyond this.

Naver Financial is its fintech subsidiary, and Naver Pay is South Korea's largest mobile payment platform, boasting 30 million users, covering more than half of the South Korean population. From online shopping to offline payments, from transfers to wealth management, Naver Pay has deeply integrated into the daily lives of South Koreans.

Like other global tech giants, Naver acquires users through its core platform (search engine) and then continuously expands its services, creating an ecosystem that is hard for users to leave.

In the financial sector, Naver has been accelerating its layout. It established Naver Financial in 2019, launched digital banking services in 2020, and obtained a securities brokerage license in 2024. In September of this year, Naver Pay acquired 70% of Dunamu's Securities Plus Unlisted for 68.6 billion won.

Now, acquiring Upbit is the final piece of the puzzle for Naver's financial landscape. Once completed, Naver will possess:

Payment tools (Naver Pay)

Securities trading (Securities Plus)

Cryptocurrency trading (Upbit)

Upcoming Korean won stablecoin

This vertical integration allows Naver to provide users with a full-chain financial service from fiat currency to cryptocurrency. More importantly, through LINE's 200 million overseas users, this system has the potential to expand beyond South Korea and cover the entire Asian market.

Korean Characteristics: When Chaebols Meet Web3

Naver's acquisition of Upbit is not an isolated case. It is one of the latest manifestations of large South Korean enterprises entering the cryptocurrency market.

Kakao started its layout earlier. In 2019, it launched the public chain Klaytn and promoted the Klip wallet through KakaoTalk's 50 million users. The KLAY token currently ranks among the top 50 in market capitalization globally. In September, Klaytn announced a merger with the Finschia chain developed by LINE to form a new Kaia chain.

Samsung has approached from the hardware angle. Since the Galaxy S10 in 2019, Samsung phones have included cryptocurrency wallet functionality. Samsung SDS also provides blockchain solutions for enterprise clients. Although Samsung does not directly operate an exchange, its infrastructure layout is quite evident.

Traditional financial institutions are also accelerating their entry. In August of this year, eight banks, including KB Financial and Shinhan Financial, announced a joint development project for a Korean won stablecoin. This timing coincided with Naver and Dunamu's announcement of their stablecoin collaboration a month earlier.

This chaebol-led pattern is not surprising in South Korea.

The South Korean economy has long been dominated by large corporate groups, with the top ten chaebols contributing a significant portion of South Korea's GDP. When new industries emerge, these large enterprises typically enter quickly and establish a dominant position.

Dunamu was founded in 2012 and launched Upbit in 2017. In a market environment like South Korea's, it is not easy for an independent company to grow to a valuation of 8.26 trillion won. Choosing to join the Naver system now may be a strategic choice in the face of increasingly fierce competition.

From past information, there are several characteristics of large South Korean enterprises entering the cryptocurrency market:

First, there is significant and rapid resource investment. Kakao took about a year from deciding to develop blockchain to launching the Klaytn mainnet. Naver took just over two months from announcing the stablecoin collaboration in July to preparing for the full acquisition of Dunamu.

Second, there is a high degree of coordination with government policies. The South Korean government suspended its central bank digital currency project this year and instead supported the private sector in developing stablecoins. This policy shift coincided with major enterprises accelerating their layout in the cryptocurrency business.

Third, each is building an independent ecosystem. Naver has its own payment system, Kakao has its own blockchain, and the banking alliance aims to promote its own stablecoin. Each group is constructing a relatively closed system, making it costly for users to migrate between different ecosystems.

The result of this model is an increasing concentration in the market.

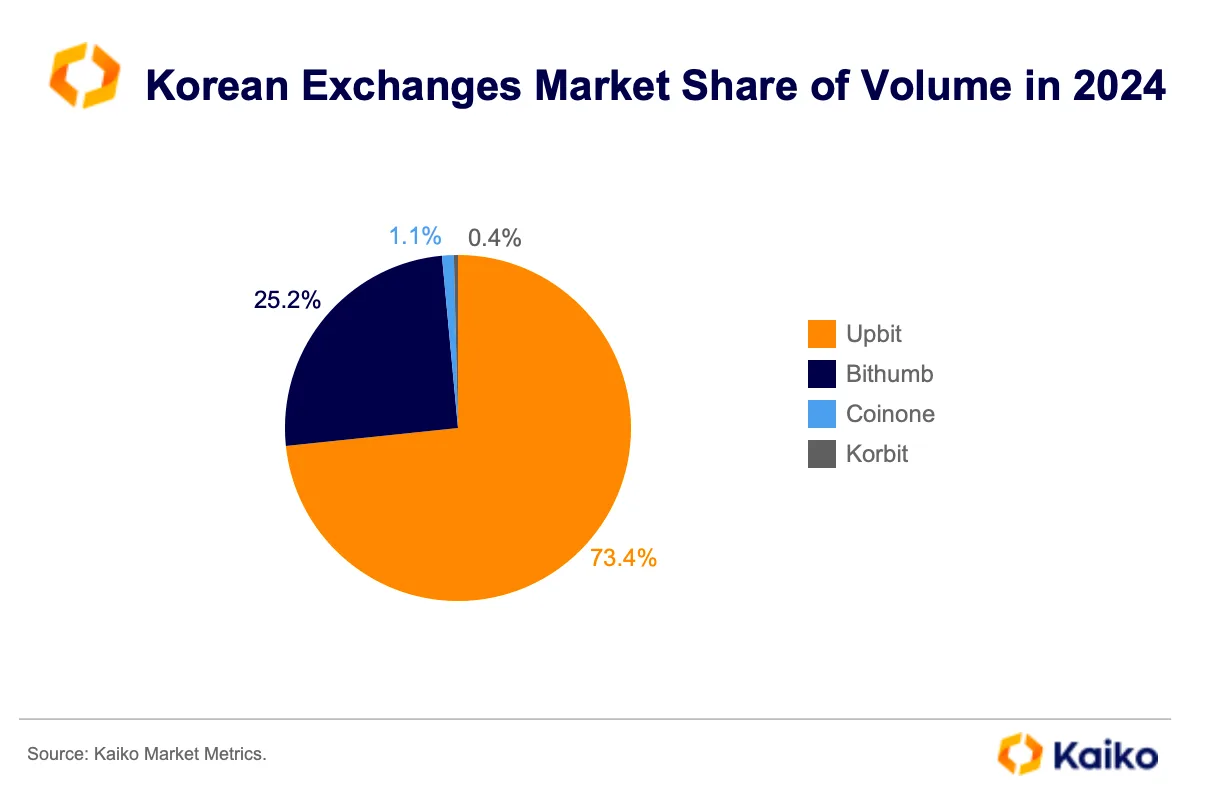

According to public data, Upbit once accounted for about 73% of trading volume in South Korea, while Bithumb accounted for about 25%, with the remaining market share divided among Coinone, Korbit, and others. With Upbit being acquired by Naver, market concentration may further increase.

Chaebols dominate, rapidly advance, and prioritize practicality; South Korea has its own development model for the cryptocurrency industry.

You might think this is somewhat centralized, but South Koreans seem unconcerned. Nearly 20% of South Koreans participate in cryptocurrency trading, and they care more about convenience and security.

The "New Chaebol Era" of the Global Cryptocurrency Market

Not just in South Korea, but globally, the current cryptocurrency market is undergoing a transformation from grassroots entrepreneurship to monopoly by giants.

First, let's look at the Middle East. Binance received investment from the Abu Dhabi sovereign wealth fund this year; although the specific amount has not been disclosed, market rumors suggest it could be in the billions. The Dubai royal family supports multiple cryptocurrency projects, aiming to make Dubai the "global cryptocurrency capital." Saudi Arabia's Public Investment Fund (PIF) is also actively investing in blockchain.

The United States is taking a different path: traditional finance is gradually swallowing the cryptocurrency market, ultimately turning it into another asset class.

As the government becomes increasingly friendly towards the cryptocurrency industry, major institutions on Wall Street are starting to pivot. BlackRock launched a Bitcoin ETF, Fidelity offers cryptocurrency custody, and Goldman Sachs has begun cryptocurrency trading…

Coinbase, while still relatively independent, is seeing its institutional business grow, with retail investors becoming less central to trading.

Japan's situation is more nuanced. Rakuten acquired a cryptocurrency exchange back in 2018, and SBI Holdings operates one of Japan's largest cryptocurrency platforms. However, unlike the aggressive approach of South Korean chaebols, Japanese large enterprises' cryptocurrency layouts are relatively conservative, resembling defensive investments.

These different models reflect varying understandings of cryptocurrency across regions, but the outcomes seem similar: independent cryptocurrency enterprises are finding it increasingly difficult to survive; attractive cryptocurrency assets are seeing a growing proportion of institutional holdings.

For instance, large centralized exchanges (CEX) and cryptocurrency infrastructure companies (like stablecoins), driven by compliance and the need to attract more incremental users, are either gradually accepting large investments from traditional capital or striving to go public in the capital markets.

BTC and ETH have become sought-after assets in corporate cryptocurrency treasury strategies.

Perhaps a more accurate description of this phenomenon is that the cryptocurrency market is becoming stratified.

The upper tier is an institution-led, compliant, centralized market. Here, there are ETFs, custody services, and licensed exchanges; the lower tier is a community-driven, experimental, decentralized market. Here, there are Perp DEX and Meme.

The mainstream market is controlled by large capital, serving ordinary users and institutions; the fringe market remains decentralized, continuing technological innovation and experimentation.

As for whether this phenomenon is good or bad, there may not be a simple answer.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。