Return 93% of trading fees directly to token holders, cash flow valuation shows $HYPE is severely undervalued

Author: G3ronimo

Translated by: Deep Tide TechFlow

HyperLiquid has evolved into a mature crypto-native exchange, with most of its net fees programmatically distributed directly to token holders through the "Assistance Fund" (AF). This design makes $HYPE one of the few tokens that can be valued based on cash flow. To date, most valuations of HyperLiquid still rely on traditional multiple methods, comparing it to established financial platforms like Coinbase and Robinhood, using EBITDA or revenue multiples as references.

Unlike traditional corporate stocks, where management typically retains and reinvests earnings based on their judgment, HyperLiquid systematically returns 93% of trading fees directly to token holders through the Assistance Fund. This model creates predictable and quantifiable cash flow, making it suitable for detailed discounted cash flow (DCF) analysis rather than static multiple comparisons.

Our approach first determines the cost of capital for $HYPE, then we reverse the current market price to determine the market's implied future earnings. Finally, we apply growth forecasts to these earnings streams and compare the resulting intrinsic value with today's market price, revealing the valuation gap between current pricing and fundamental value.

Why choose discounted cash flow (DCF) over multiple methods?

While other valuation methods compare HyperLiquid to Coinbase and Robinhood using EBITDA multiples, these methods have the following limitations:

Differences in corporate and token structures: Coinbase and Robinhood are corporate stocks, with capital allocation guided by a board of directors, and earnings retained and reinvested at management's discretion; whereas HyperLiquid systematically returns 93% of trading fees directly to token holders through the Assistance Fund.

Direct cash flow: HyperLiquid's design generates predictable cash flow, making it very suitable for DCF models rather than static multiple methods.

Growth and risk characteristics: DCF can explicitly model different growth scenarios and risk adjustments, while multiple methods may not fully reflect growth and risk dynamics.

Determining the appropriate discount rate

To determine our cost of equity, we start from publicly available market reference data and adjust for cryptocurrency-specific risks:

Cost of equity (r) ≈ Risk-free rate + β × Market risk premium + Crypto/illiquidity premium

Beta Analysis

Based on regression analysis with the S&P 500 index:

Robinhood (HOOD): Beta of 2.5, implied cost of equity of 15.6%;

Coinbase (COIN): Beta of 2.0, implied cost of equity of 13.6%;

HyperLiquid (HYPE): Beta of 1.38, implied cost of equity of 10.5%.

At first glance, $HYPE's lower Beta suggests its cost of equity is lower than that of Robinhood and Coinbase. However, the R² value reveals an important limitation:

HOOD: The S&P 500 explains 50% of its returns;

COIN: The S&P 500 explains 34% of its returns;

HYPE: The S&P 500 explains only 5% of its returns.

The low R² of $HYPE indicates that traditional stock market factors are insufficient to explain its price fluctuations, necessitating consideration of crypto-native risk factors.

Risk Assessment

Despite $HYPE's lower Beta, we adjust its discount rate from 10.5% to 13% (more conservative compared to COIN's 13.6% and HOOD's 15.6%) for the following reasons:

Lower governance risk: The direct programmed distribution of 93% of fees reduces concerns related to corporate governance. In contrast, COIN and HOOD do not return any earnings to shareholders, with capital allocation determined by management.

Higher market risk: $HYPE is a crypto-native asset, facing additional regulatory and technological uncertainties.

Liquidity considerations: The token market is generally less liquid than mature stock markets.

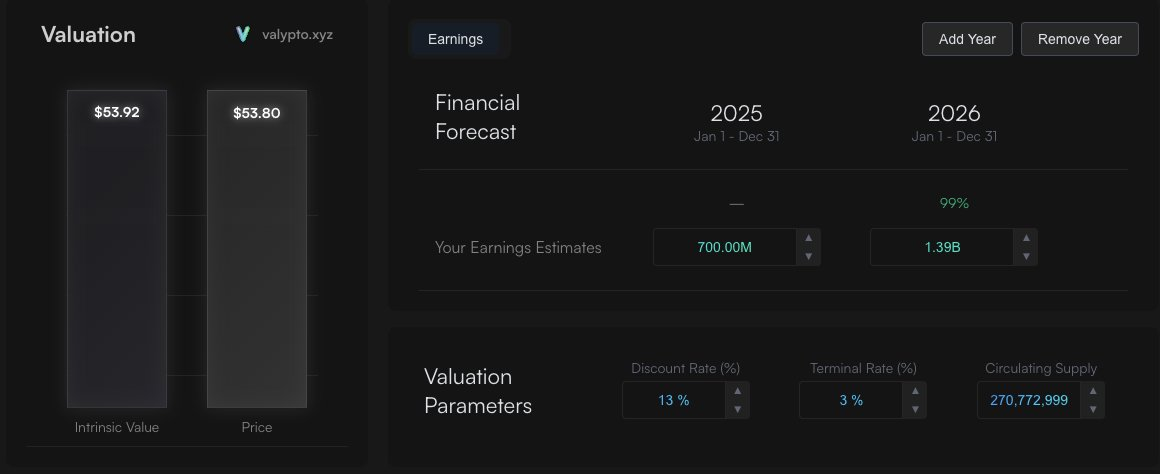

Obtaining Market Implied Price (MIP)

Using our established 13% discount rate, we can reverse-engineer the market's implied earnings expectations at the current price of approximately $54 for the $HYPE token:

Current market expectations:

2025: Total earnings of $700 million

2026: Total earnings of $1.4 billion

Terminal growth: Continuous growth of 3% per year thereafter

The intrinsic value derived from these assumptions is approximately $54, consistent with the current market price. This indicates that the market is pricing moderate growth based on current fee levels.

At this point, we need to ask a question: Does the market implied price (MIP) reflect future cash flows?

Alternative Growth Scenarios

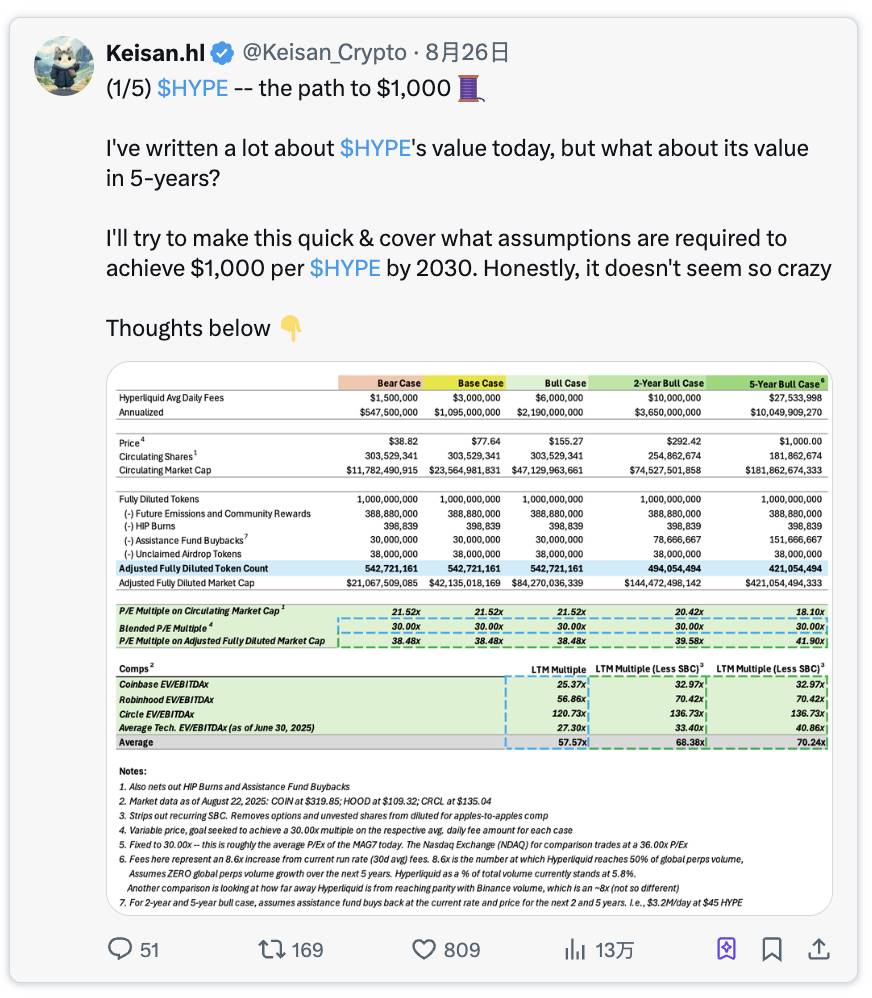

@Keisan_Crypto proposed an attractive bull market scenario for 2 and 5 years.

Original tweet link: Click here

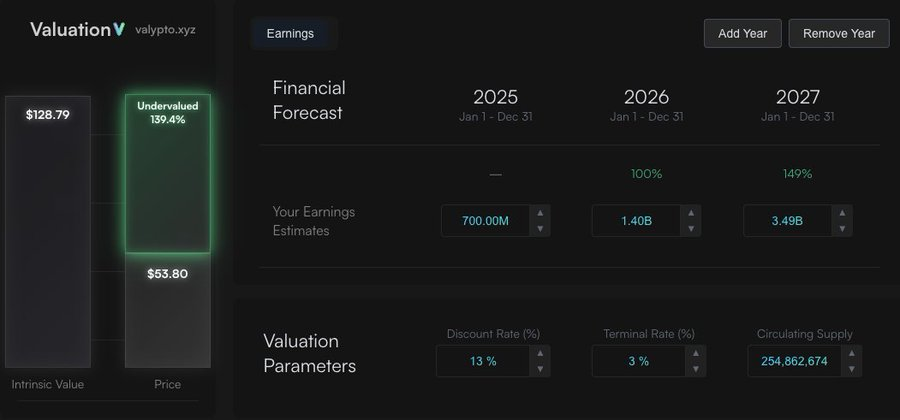

Two-Year Bull Market Forecast

According to @Keisan_Crypto's analysis, if HyperLiquid achieves the following targets:

Annual fees: $3.6 billion

Assistance Fund earnings: $3.35 billion (93% of fees)

Result: The intrinsic value of HYPE is $128 (undervalued by 140% based on current price)

Five-Year Bull Market Scenario

In the five-year bull market scenario (related link), he predicts that fees will reach $10 billion annually, with $9.3 billion attributable to $HYPE. He assumes HyperLiquid's global market share will grow from the current 5% to 50% by 2030. Even if it does not reach a 50% market share, these numbers could still be achieved with a smaller market share as global trading volume continues to grow.

Five-Year Bull Market Forecast

Annual fees: $10 billion

Assistance Fund earnings: $9.3 billion

Result: The intrinsic value of HYPE is $385 (undervalued by 600% based on current price)

Although this valuation is below Keisan's $1000 target, the difference arises from our assumption that earnings growth normalizes to 3% per year thereafter, while Keisan's model uses cash flow multiples. We believe there are issues with using cash flow multiples to forecast long-term value because market multiples are volatile and can change significantly over time. Additionally, multiples themselves contain assumptions about earnings growth, and using the same cash flow multiple five years later implies that the growth level from 2030 onward is consistent with the growth level from 2026/2027. Therefore, multiples are more suitable for short-term asset pricing. However, regardless of which model is used, $HYPE remains undervalued; this is merely a nuance.

Additional Value Drivers: USDH

Under the Native Market model, USDH will use 50% of stablecoin revenue for buybacks similar to the Assistance Fund. Therefore, $HYPE could add $100 million (50% of $200 million) in free cash flow annually.

Looking ahead five years, if USDH's market cap can reach $25 billion (currently still one-third of USDC, and even smaller in proportion to the total stablecoin market size five years later), its annual revenue is expected to reach $1 billion. Following the same 50% distribution model, this would bring an additional $500 million in free cash flow to the Assistance Fund annually. This would push the value of each token above $400.

Excluding Value Drivers: HIP-3 and HyperEVM

This DCF analysis intentionally excludes two significant potential value drivers that are not suitable for cash flow modeling. Clearly, they would provide additional incremental value and could be assessed separately using different valuation methods, then added to this valuation result.

Conclusion

Our DCF analysis indicates that if HyperLiquid can maintain its growth trajectory and market position, the value of the $HYPE token is significantly undervalued. The token's unique feature of programmed fee distribution makes it particularly suitable for cash flow-based valuation methods.

Methodology Note

This analysis is built on the research findings of @Keisan_Crypto and @GLC_Research.

The DCF model is open-source and can be modified at the following link:

https://valypto.xyz/project/hyperliquid/oNQraQIg

Market data and forecasts may change, and the model should be updated promptly based on the latest information.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。