Author: Frank, PANews

The hot on-chain derivatives trading platform Hyperliquid recently announced the issuance of its on-chain native stablecoin, named USDH. However, unlike the "pre-determined" or protocol-built stablecoins common in the industry, Hyperliquid has chosen an unprecedented path—publicly soliciting cooperative issuers through on-chain validator voting.

As soon as this news broke, giants in the stablecoin sector, such as Paxos, Frax Finance, and Agora, sprang into action, submitting highly competitive proposals. It is rumored that other stablecoin issuers are also planning to participate in the bidding, marking the beginning of an online bidding frenzy for Hyperliquid's "minting rights."

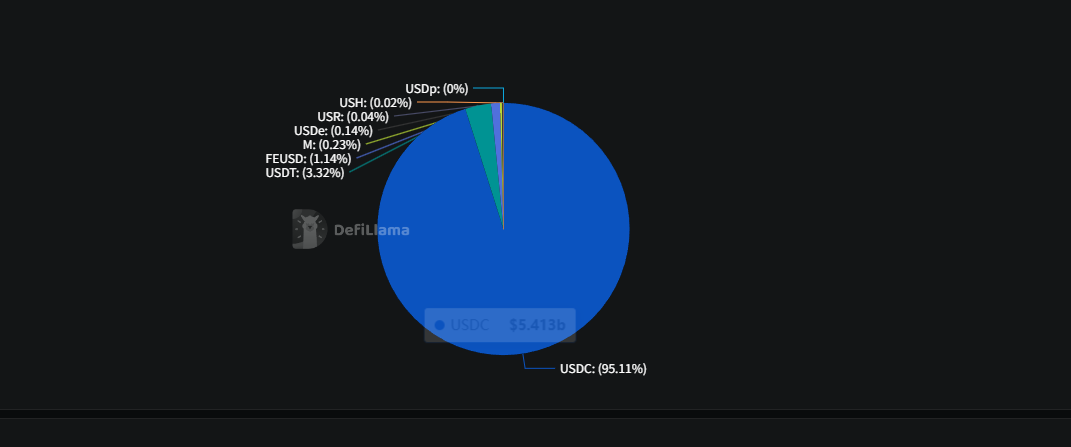

The focal point of this competition is the $5.6 billion in USDC deposited on the Hyperliquid platform. If successfully replaced with USDH, it is expected to generate over $220 million in annual treasury interest income. This substantial income will no longer flow to external issuers but will be reinvested into the Hyperliquid ecosystem. Following the announcement, the market reacted enthusiastically, with Hyperliquid's native token HYPE rising nearly 10%.

What interests lie behind this battle for stablecoin issuance rights? Why are major issuers willing to forgo easily obtainable massive profits? In this complex game, who will emerge as the ultimate winner? PANews will dissect these questions in this article.

A New Source of Income Exceeding the HPL Treasury

The most direct driving force behind Hyperliquid's issuance of the native stablecoin USDH is the enormous economic benefit.

Currently, there are approximately $5.6 billion in stablecoins on the Hyperliquid platform, with 95% being USDC. The reserves of this fund are managed by its issuer, Circle, which earns interest through investments in low-risk assets like U.S. Treasury bonds, capturing this value entirely externally. Hyperliquid, as the creator of the application scenario and demand for these funds, has not been able to share in the profits.

By issuing USDH, Hyperliquid aims to internalize this value. Based on the current short-term U.S. Treasury yield of about 4%, the $5.6 billion in reserves could generate approximately $220 million in annual income. This income would surpass the current annual revenue of the HPL treasury (approximately $75 million), becoming one of the largest sources of income on the Hyperliquid chain, undoubtedly providing greater incentives for the community.

In addition to economic benefits, stimulating the ecosystem may be another consideration. From the official announcement, the first reason given is: "To improve liquidity and reduce user friction, the spot trading pairs between two spot quote assets will reduce 80% of taker fees, maker rebates, and user trading volume contributions." For exchanges, lowering trading fees is a necessary option to directly enhance core competitiveness. Especially for Hyperliquid, the relatively low spot trading volume compared to contract trading is a pressing issue that needs to be addressed.

After all, increasing spot trading would provide Hyperliquid with better spot depth and could further help avoid incidents of price manipulation like those seen with tokens such as XPL in the past.

From the official announcement and bidding process, Hyperliquid's core requirements for issuers can be summarized in three points:

- A stablecoin pegged to the U.S. dollar and compliant.

- Suitable for Hyperliquid's native minting.

- A team prioritized by Hyperliquid.

Among these, compliance is a key focus for current stablecoin issuance and has become a necessary condition for stablecoins. The second point, emphasizing Hyperliquid's native minting, means that USDH will no longer need to enter the Hyperliquid chain through cross-chain bridges like USDC. This lays the foundation for various trading activities on-chain. Finally, the mention of a Hyperliquid-prioritized team suggests that teams familiar with the Hyperliquid chain will be given priority consideration.

It is worth noting that Circle co-founder Jeremy Allaire expressed on social media regarding this matter: "Glad to see competition, will enter the HYPE ecosystem in significant ways." However, from the link shared by Jeremy Allaire, it appears that Circle's focus remains on issuing the native USDC rather than participating in the competition for USDH.

Paxos, Frax Finance, and Other Bidders Each Have Their Strengths

This on-chain bidding has attracted several key stablecoin issuers to participate. As of September 8, the main participants include established compliant issuers such as Paxos, Frax Finance, and Agora, as well as native projects on the Hyperliquid chain like Native Markets and Hyperstable.

Among these, notable attention can be given to Paxos, Frax Finance, Agora, and Native Markets, which are quite representative.

Paxos and Agora, as representatives of compliance, have a strong background. Paxos is a trust company regulated by the New York Department of Financial Services (NYDFS) and has the compliance background and ecosystem advantages of PayPal. Paxos previously issued the stablecoin BUSD for Binance. In Paxos's proposal, it mentions that 95% of the reserve interest will be used to repurchase HYPE and promises to integrate HYPE into its brokerage infrastructure that serves giants like PayPal. Additionally, Paxos recently acquired Molecular Labs, the development team behind existing core components LHYPE and WHLP in the Hyperliquid ecosystem.

Agora also has advantages in compliance, with its reserves custodied by top financial institution State Street Bank and managed by VanEck. In terms of revenue distribution, Agora's proposal promises to share 100% of net income with the ecosystem. The key here is that "net income" may deduct custodial fees, operational costs, etc. However, in Paxos's proposal, the interest is used to repurchase HYPE, which ultimately does not count as a return to the community.

Frax Finance, as a giant in the DeFi space, has advantages in the DeFi ecosystem. Additionally, its proposal mentions that it will use the frxUSD stablecoin to support 1:1, which is also backed by tokenized treasury funds from BlackRock's BUIDL and other RWA assets, providing strong compliance and security. Furthermore, Frax Finance promises to directly and seamlessly pass 100% of the underlying treasury yield to Hyperliquid users through smart contracts, with Frax itself not charging any fees. Due to different mechanism designs, Frax's yields may also be higher than those of other stablecoins, although it may sacrifice some security ratings.

Native Markets has advantages in terms of native projects, being a native project on Hyperliquid. It also states that it will integrate the global compliance profile and fiat channels of the issuer Bridge (a company under Stripe). In terms of revenue return, Native Markets promises to contribute a significant portion of reserve income to the Assistance Fund (an automatic on-chain HYPE repurchase protocol). However, this does not equate to returning to the community, as they submitted a supplementary proposal on September 9, setting the return ratio at 50%.

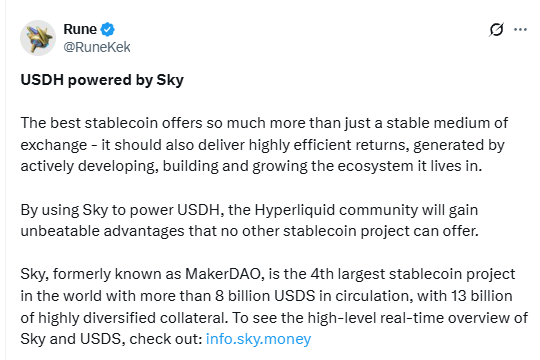

On September 9, another DeFi giant, Sky (formerly MakerDAO), also planned to participate in the issuance of the USDH stablecoin. Sky's feature lies in liquidity support, offering $2.2 billion in instant liquidity and providing a clear return rate of 4.85%, which could bring $250 million in annual income to Hyperliquid.

Overall, these participants each have their strengths in compliance, revenue return, and ecosystem native aspects. However, in terms of profit return, Frax Finance appears to be the most sincere.

Questioned or a Governance Show After Pre-Determination

For the community, the choice of USDH issuers is not just a simple ecological upgrade. It involves significant choices regarding HYPE token economics, the competitive landscape of the stablecoin market, and even the future of the entire DeFi sector.

For the HYPE token, as mentioned earlier, once this portion of treasury interest is returned, it will become one of the largest ecological income sources, further impacting the value expectations of HYPE. Indirectly, high-yield income-generating stablecoins can help the ecosystem absorb more funds, increasing Hyperliquid's trading depth and providing a continuous source of user conversion.

For the community, this decision is undoubtedly positive. In forums, supportive voices dominate. However, there are also voices questioning whether the official on-chain voting is essentially a show after pre-determination.

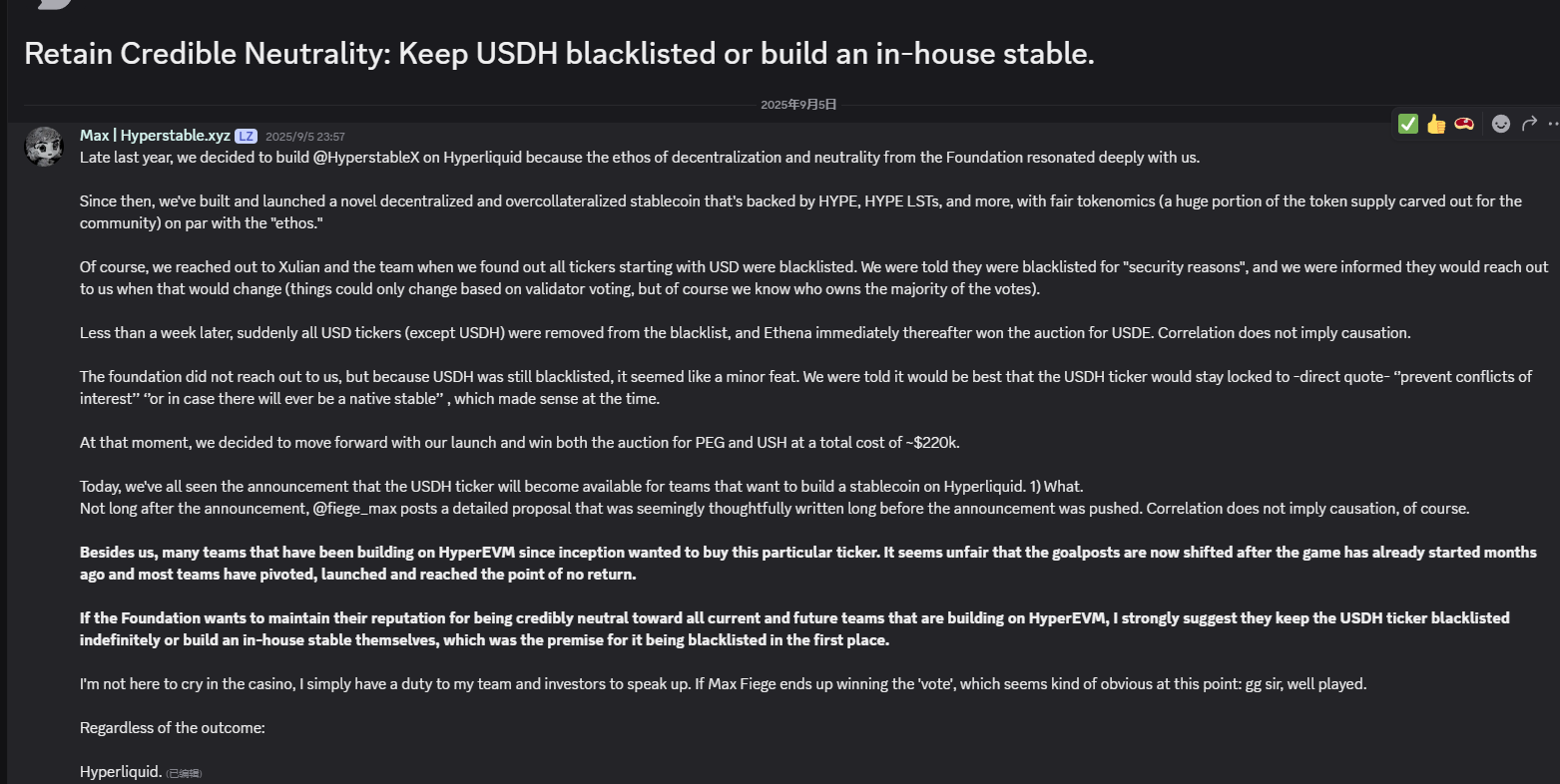

The biggest controversy was raised by another native stablecoin project on Hyperliquid, Hyperstable, which claimed that it had previously attempted to use the USDH code but was informed that the code had been blacklisted. In this on-chain proposal, another project, Native Markets, quickly released its proposal just one hour after the official announcement, suggesting possible prior information disclosure.

Additionally, some other community members expressed that the overall proposal content was too vague, raising questions about specific compliance details (such as federal or state licenses), technical details, and considerations of conflicts of interest regarding the stablecoin issuance. They felt puzzled that the official decision on an issuer was made based solely on these simple proposals, especially given that the proposal period was only five days.

Indeed, from the details of the proposals, those on Hyperliquid generally range from several hundred to over a thousand words, which may only cover the introduction or summary compared to proposals on other public chains. Furthermore, aside from Native Markets releasing its proposal within an hour, Frax's proposal was also published in about ten hours, which indeed far exceeds the average decision-making time of decentralized organizations, inevitably leading to speculation about whether the official had contacted alternative candidates in advance.

Conclusion

Regardless, this step taken by Hyperliquid is indeed a positive direction for the community. It reflects the official's consideration of the current issues of spot trading volume and depth on the platform, as well as maximizing community benefits. However, from another perspective, even if USDH can be issued quickly, it may not completely replace USDC in a short time, as USDC, being a more universal stablecoin, has demonstrated more tested performance in trading stability and depth. As for who will ultimately secure the rights, it will be an art of balance, and for the community, whether it is governance or merely advisory will also be a test of Hyperliquid's decentralized governance outcomes.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。