The altcoin season will come, but it will not be like the altcoin season of 2021.

Author | Jiawei @IOSG

Introduction

▲ Source: CMC

Over the past two years, the market's focus has been driven by one question: Will the altcoin season return?

In contrast to Bitcoin's strength and the advancement of institutionalization, the performance of the vast majority of altcoins has been lackluster, with most existing altcoins' market values shrinking by 95% compared to the last cycle, and many new coins that were once surrounded by hype are now mired in difficulties. Ethereum has also experienced a prolonged period of emotional downturn, only recently showing signs of recovery driven by trading structures like the "coin-stock model."

Even with Bitcoin reaching new highs and Ethereum recovering and stabilizing, the overall sentiment towards altcoins remains low. Every market participant is hoping for a repeat of the epic bull market of 2021.

I propose a core assertion: The macro environment and market structure that supported the "flooding" style of broad-based rallies for several months in 2021 no longer exist—this does not mean that an altcoin season will not come, but it is more likely to unfold in a slow bull pattern with more differentiated characteristics.

The Fleeting 2021

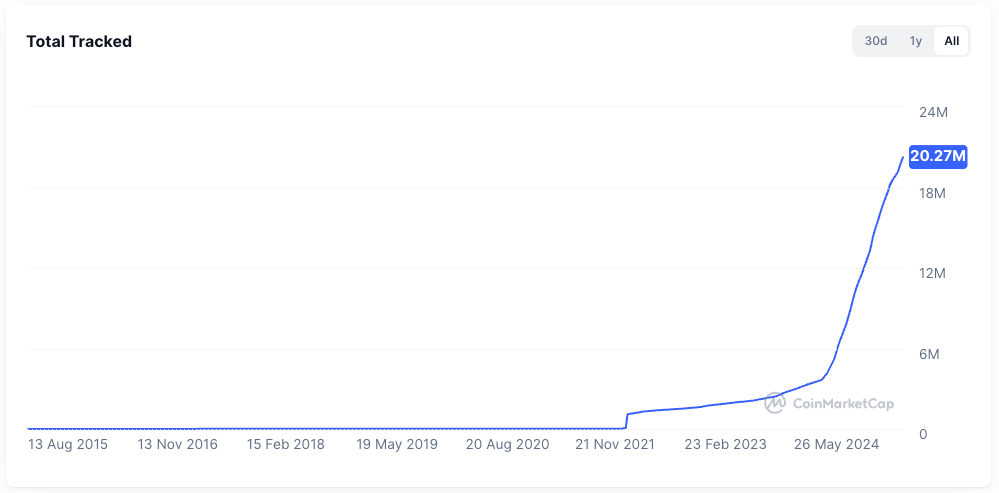

▲ Source: rwa.xyz

The external market environment in 2021 was quite unique. Amid the COVID-19 pandemic, central banks around the world were printing money at an unprecedented pace, injecting this cheap capital into the financial system, while the yields on traditional assets were suppressed, leading to a sudden influx of cash into people's hands.

Driven by the pursuit of high returns, funds began to flow into risk assets, with the crypto market becoming a significant recipient. The most direct indicator was the sharp expansion in the issuance of stablecoins, which skyrocketed from about $20 billion at the end of 2020 to over $150 billion by the end of 2021, an increase of more than seven times within the year.

Within the crypto industry, after DeFi Summer, the infrastructure for on-chain finance was being laid out, concepts like NFTs and the metaverse entered the public eye, and public chains and scaling tracks were also in a growth phase. At the same time, the supply of projects and tokens was relatively limited, with high concentration of attention.

For example, in DeFi, the number of blue-chip projects was limited at that time, with a few protocols like Uniswap, Aave, Compound, and Maker representing the entire sector. The difficulty of choice for investors was low, making it easier for funds to coalesce and drive the entire sector upward.

These two points provided the soil for the altcoin season of 2021.

Why "The Good Times Don't Last, and the Feast is Hard to Recreate"

Setting aside macro factors, I believe that the current market structure has undergone several significant changes compared to four years ago:

Rapid Expansion of Token Supply

▲ Source: CMC

The wealth effect of 2021 attracted a large influx of funds. Over the past four years, the booming venture capital landscape has invisibly raised the average valuation of projects, while the prevalence of airdrop economies and the viral spread of memecoins have collectively led to a rapid acceleration in the issuance of tokens, with valuations rising accordingly.

▲ Source: Tokenomist

Unlike most projects in 2021, which were in a state of high circulation, mainstream projects in the current market, aside from memecoins, are generally facing significant token unlocking pressures. According to TokenUnlocks, over $200 billion in market value of tokens will face unlocking between 2024 and 2025. This is also a criticism of the current cycle's "high FDV, low circulation" industry status.

Dispersed Attention and Liquidity

▲ Source: Kaito

In terms of attention, the above image randomly captures the mindshare of Pre-TGE projects on Kaito. Among the top 20 projects, we can identify at least 10 sub-sectors. If we were to summarize the main narratives in the 2021 market in a few words, most people would likely say "DeFi, NFT, GameFi/Metaverse." However, the market over the past two years seems difficult to describe immediately in just a few words.

In this context, funds quickly switch between different sectors, and the duration is very short. The crypto Twitter (CT) is flooded with overwhelming information, and various groups spend most of their time discussing different topics. This fragmentation of attention makes it difficult for funds to coalesce as they did in 2021. Even if a particular sector experiences a good market, it is hard to spread to other areas, let alone drive an overall rally.

In terms of liquidity, a fundamental basis for an altcoin season is the spillover effect of profit funds: liquidity first flows into mainstream assets like Bitcoin and Ethereum, and then begins to seek out altcoins with potentially higher returns. This spillover and rotation effect provides continuous buying support for long-tail assets.

This seemingly natural situation is something we have not seen in this cycle:

First, the institutions and ETFs driving the rise of Bitcoin and Ethereum are unlikely to further deploy funds into altcoins; these funds prefer custodial and compliant top assets and related products, which marginally reinforces the siphoning effect on top assets rather than raising the water level evenly across the board.

Second, most retail investors in the market may not even hold Bitcoin or Ethereum, but have been deeply trapped in altcoins over the past two years, leaving them with little liquidity.

Lack of Breakthrough Applications

Behind the frenzy of the 2021 market, there was actually some support. DeFi introduced fresh water to the long-term application exhaustion of blockchain; NFTs spread the creator and celebrity effects beyond the circle, with growth coming from new users and new use cases from outside the circle (at least that’s the narrative).

After four years of technological and product iteration, we find that infrastructure has been overbuilt, but truly breakthrough applications are few and far between. Meanwhile, the market is maturing, becoming more pragmatic and clear-headed—amid the aesthetic fatigue of overwhelming narratives, the market needs to see real user growth and sustainable business models.

Without a continuous influx of fresh blood to absorb the increasingly swollen token supply, the market can only fall into a zero-sum game of existing assets, which fundamentally cannot provide the basis needed for a broad rally.

Outlining and Imagining This Round of Altcoin Season

The altcoin season will come, but it will not be like the altcoin season of 2021.

First, the basic logic of profit fund circulation and sector rotation still exists. We can observe that after Bitcoin reaches $100,000, the short-term upward momentum has clearly weakened, and funds will begin to look for the next target. The same applies to Ethereum.

Second, in a market with long-term insufficient liquidity, altcoins are trapped, and capital needs to seek self-rescue methods. Ethereum is a good example: Has the fundamental situation of Ethereum changed in this round? The hottest applications, Hyperliquid and pump.fun, did not occur on Ethereum; the concept of the "world computer" is also a long-gone idea.

With insufficient internal liquidity, one can only seek external help. Driven by DAT, along with ETH's more than threefold increase, many stories about stablecoins and RWA have gained the most realistic foundation.

I envision the following scenarios:

Fundamentally Driven Certainty Market

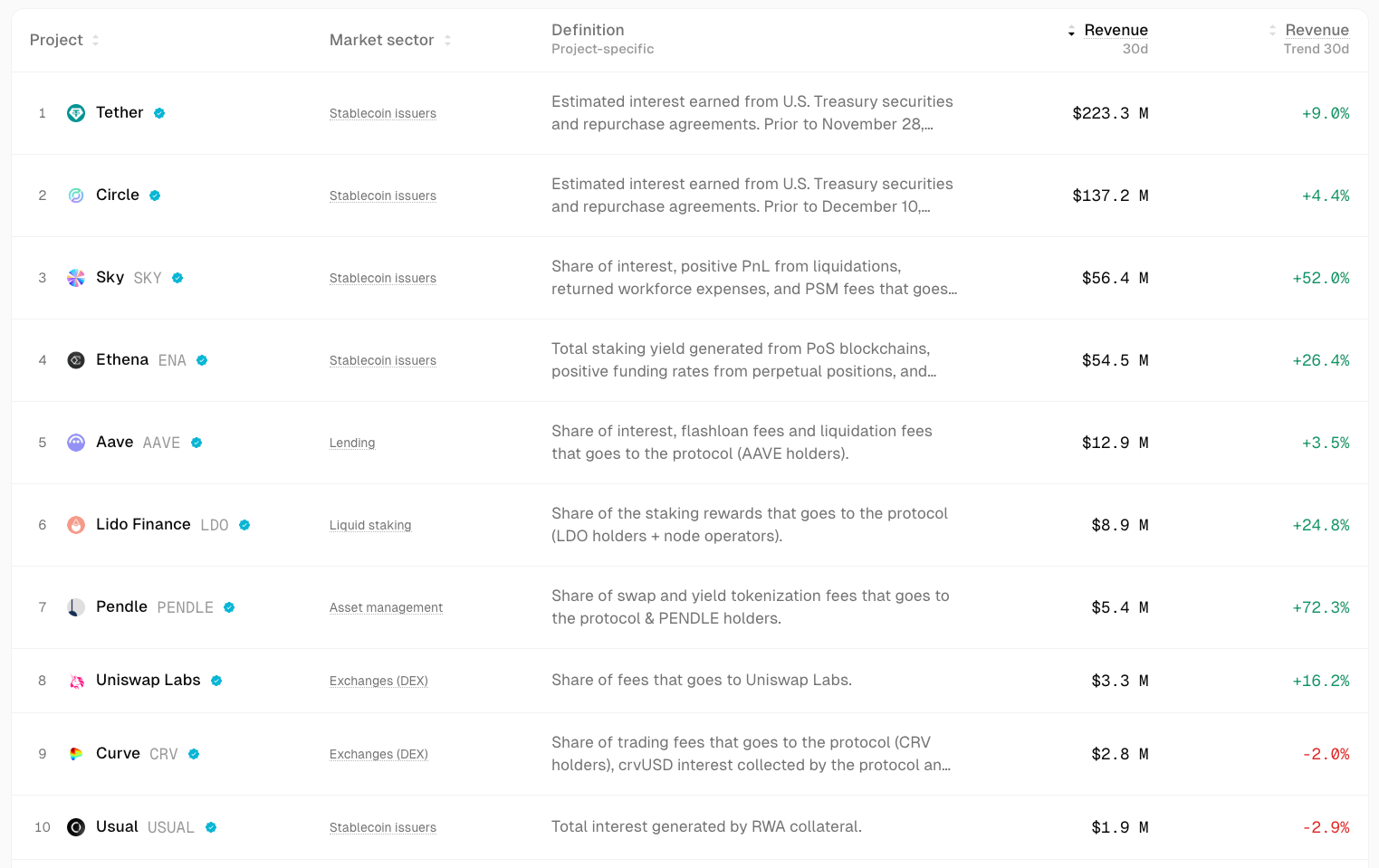

▲ Source: TokenTerminal

In an uncertain market, funds will instinctively seek certainty.

Funds will flow more towards projects with solid fundamentals and product-market fit (PMF); the price increases of these assets may be limited, but they are relatively more stable and certain. For example, DeFi blue chips like Uniswap and Aave maintain good resilience even during market downturns; Ethena, Hyperliquid, and Pendle have emerged as new stars in this cycle.

Potential catalysts could include actions like opening fee switches and other governance-level initiatives.

The commonality among these projects is that they can generate considerable cash flow, and their products have been fully validated by the market.

Beta Opportunities in Strong Assets

When a mainline market (like ETH) begins to rise, funds that miss this increase or seek higher leverage will look for highly correlated "proxy assets" to gain beta returns. For example, UNI, ETHFI, ENS, etc. They can amplify ETH's volatility, but their sustainability is relatively poorer.

Repricing of Old Sectors Under Mainstream Adoption

From institutional-level Bitcoin buying, ETFs, to the DAT model, the main narrative of this cycle is the adoption of traditional finance. If the growth of stablecoins accelerates, assuming a fourfold increase to reach $1 trillion, a portion of these funds will likely flow into the DeFi sector, driving a repricing of its value. Transitioning financial products from the crypto niche into the traditional financial view will reshape the valuation framework of DeFi blue chips.

Local Ecological Speculation

▲ Source: DeFiLlama

HyperEVM, due to its consistently high discussion heat, user stickiness, and the gathering of incremental funds, may experience weeks to months of wealth effect and alpha during the growth cycle of ecological projects.

Valuation Discrepancies Among Star Projects

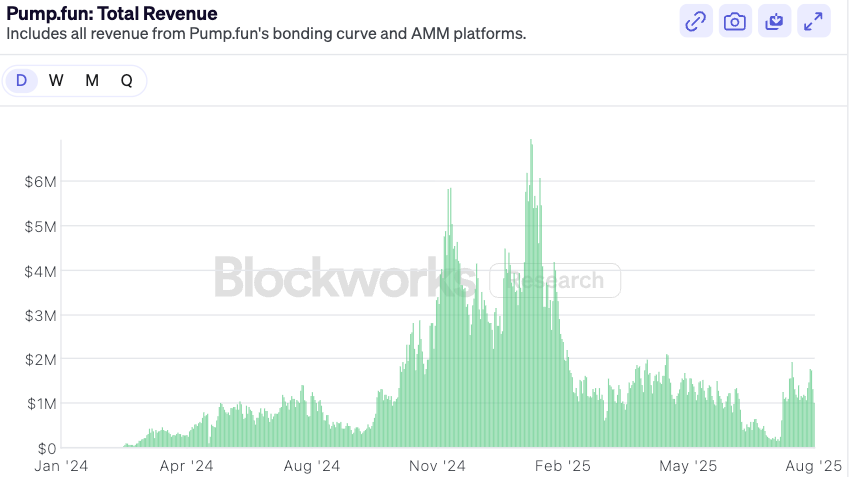

▲ Source: Blockworks

Taking pump.fun as an example, after the peak of sentiment in issuing tokens recedes, and valuations return to conservative ranges with market divergence, if the fundamentals remain strong, there may be opportunities for recovery. In the medium term, pump.fun, as a leader in the meme sector, while also having revenue as fundamental support and a buyback model, may outperform most top memecoins.

Conclusion

The "buying with closed eyes" altcoin season of 2021 has become history. The market environment is becoming relatively more mature and differentiated—markets are always right, and as investors, we can only continuously adapt to these changes.

In conjunction with the above, I would like to propose a few predictions as a conclusion:

After traditional financial institutions enter the crypto world, their capital allocation logic is entirely different from that of retail investors—they require explainable cash flows and benchmarkable valuation models. This allocation logic directly benefits the expansion and growth of DeFi in the next cycle. DeFi protocols will more actively initiate fee distribution, buyback, or dividend designs in the next 6–12 months to compete for institutional funds.

In the future, the valuation logic based purely on TVL will shift to cash flow distribution logic. We can see some recently launched institutional-grade DeFi products, such as Aave's Horizon, which allows collateralized tokenized U.S. Treasury bonds and institutional funds to borrow stablecoins.

As the macro interest rate environment becomes more complex and traditional finance's demand for on-chain yields increases, standardized and productized yield infrastructure will become a prized asset: interest rate derivatives (like Pendle), structured product platforms (like Ethena), and yield aggregators will benefit.

The risk faced by DeFi protocols is that traditional institutions may leverage their brand, compliance, and distribution advantages to issue their own regulated "walled garden" products, competing with existing DeFi. This can be seen in the collaboration between Paradigm and Stripe in launching the Tempo blockchain.

The future altcoin market may lean towards a "barbell" structure, with liquidity flowing to two extremes: one end being blue-chip DeFi and infrastructure. These projects possess cash flow, network effects, and institutional recognition, attracting the vast majority of funds seeking stable appreciation. The other end consists of purely high-risk speculative assets—memecoins and short-term narratives. This portion of assets does not carry any fundamental narrative but serves as high liquidity, low barrier speculative tools, satisfying the market's demand for extreme risk and return. Meanwhile, projects that fall in between, possessing certain products but lacking deep moats and having bland narratives, may find their market positioning awkward if liquidity structures do not improve.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。