Author: thetokendispatch

Translation: Blockchain in Plain Language

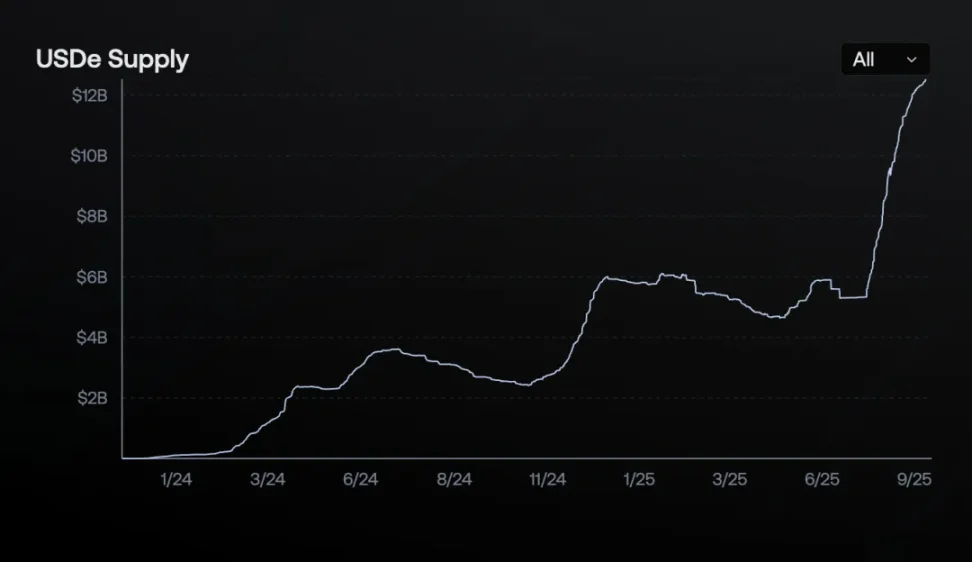

A cryptocurrency protocol launched just 18 months ago, USDe has already reached a circulating market value of $12.4 billion, setting the record for the fastest growth in the history of digital dollars. In comparison, USDT did not reach $12 billion until mid-2020 (after years of slow growth), and USDC only surpassed $10 billion in March 2021. Ethena's USDe seems to have completed a speed race in the financial arena.

How did they achieve this so quickly? What risks are behind it? Is this model sustainable, or is it just another Terra (Luna) that could collapse at any moment?

The World's Largest Arbitrage Trade

Ethena has found a way to turn the cryptocurrency market's endless thirst for leverage into a money-making machine. Simply put: hold cryptocurrency assets while simultaneously short hedging an equal amount in the futures market to earn the price difference. This creates a stable synthetic dollar while also generating returns from the most reliable "money printer" in the crypto market.

How does it work?

When someone wants to mint USDe, they need to deposit cryptocurrency assets like Ethereum (ETH) or Bitcoin. But Ethena does not just hold these assets (because they are too volatile); instead, it immediately opens an equal short position on a perpetual futures exchange.

- If ETH rises by $100, the spot position earns $100, but the short position loses $100.

- If ETH falls by $500, the spot position loses $500, but the short position earns $500.

The result? Regardless of price fluctuations, the dollar value remains stable. This is known as a "delta neutral" strategy; you won't make big money from price swings, nor will you lose big money.

Where does the 12-20% return come from? There are three sources:

- Staking rewards: Ethena stakes the deposited ETH to earn about 3-4% annualized staking rewards.

- Funding rates: They collect funding rates from the short positions. In the crypto perpetual futures market, traders pay funding fees every 8 hours to maintain their positions. When market sentiment is bullish (about 85% of the time), longs have to pay fees to shorts. Ethena always stands on the short side, collecting these fees. In 2024, the average funding rate for Bitcoin is 11%, and for Ethereum, it is 12.6%, which translates to real cash flow.

- Reserve asset returns: Ethena holds cash equivalents and treasury products, such as USDC loyalty rewards or BlackRock's BUIDL fund, generating additional returns.

In 2024, these sources provided an average annualized return of 19% for sUSDe holders. Over the past few years, the average funding rate in the crypto market has been around 8-11%, and combined with staking rewards and other income, the returns from USDe are enough to let one sleep soundly. Isn't that the goal we pursue?

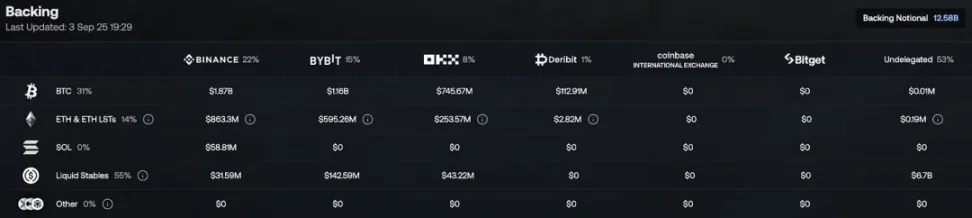

Image source: ethena.fi

Four Major Tokens in the Ethena Ecosystem

The Ethena ecosystem is supported by four tokens, each with different functions:

USDe: A synthetic dollar aimed at maintaining a stable value of $1 through delta neutral hedging. It does not generate returns unless staked, and only whitelisted participants can mint or redeem it.

Image source: ethena.fi/

sUSDe: A yield-bearing token obtained after staking USDe, stored in an ERC-4626 vault. All protocol revenue from Ethena is distributed to sUSDe holders, and its value grows with the protocol's revenue from regular deposits. Users can unstake after a cooling-off period and exchange it back for USDe.

ENA: A governance token that allows holders to vote on key protocol matters, such as acceptable collateral assets and risk parameters. ENA will also support the security model of the future ecosystem.

sENA: A token for staking ENA. The future "fee switch" mechanism will allocate a portion of protocol revenue to sENA holders, and currently, sENA can receive ecosystem allocations, such as the 15% token allocation proposed by Ethereal.

But there is a big problem: all of this relies on the market remaining bullish and willing to pay fees for long positions. If market sentiment reverses and funding rates turn negative, Ethena will need to pay fees instead of collecting them. This is a key risk that we will explore further later.

2025: The Year of Ethena's Explosion

USDe has become the fastest-growing digital dollar in history, driven by several forces:

Explosion of the perpetual futures market: By August 2025, the total open contracts for major altcoins reached $47 billion, while Bitcoin reached $81 billion. The surge in trading volume means more opportunities for funding rates, from which Ethena profits.

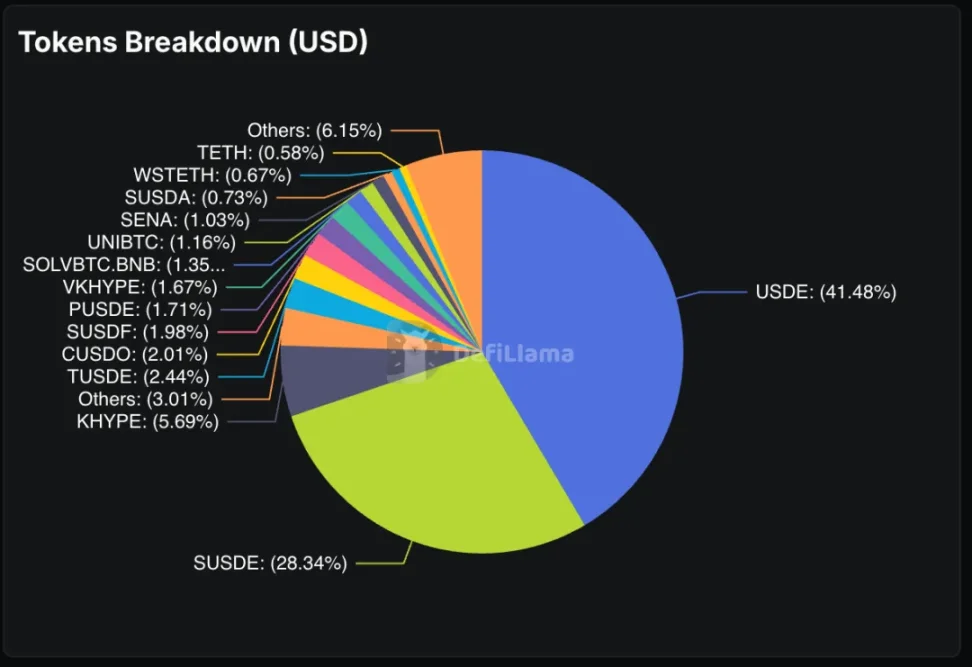

Source: defillama.com

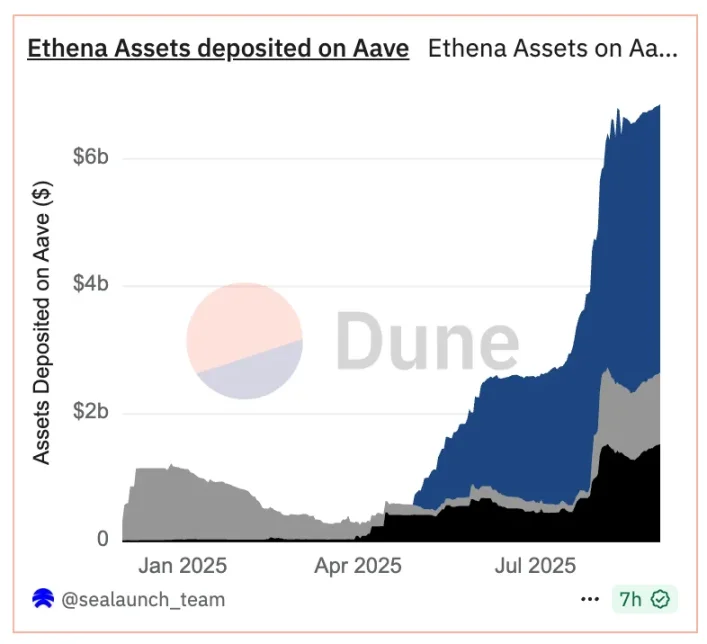

Frenzy of financial engineering: Users discovered they could stake USDe to obtain sUSDe (yield-bearing tokens), tokenize sUSDe on Pendle (a yield derivatives platform), and then use these tokens to collateralize and borrow more USDe on Aave (a lending protocol), creating a recursive cycle. This recursive yield loop has allowed savvy players to amplify their exposure to USDe returns. The result? 70% of Pendle's deposits are Ethena assets, and there are $6.6 billion in Ethena assets on Aave. This "leverage on leverage" play is chasing double-digit returns.

Image source: dune

SPAC Boost: A SPAC named StablecoinX plans to raise $360 million specifically to accumulate ENA tokens, creating a "permanent capital" buyer to reduce selling pressure and support decentralized governance.

Ethereal Perpetual DEX: Ethereal, designed specifically for USDe, has attracted $1 billion in total locked value (TVL) before its mainnet launch. Users deposit USDe to earn points for future token airdrops, creating huge demand for USDe.

Convergence Chain: Ethena's partnership with Securitize on a permissioned L2 chain uses USDe as the native gas token, attracting traditional financial institutions through KYC-compliant infrastructure, creating structural demand.

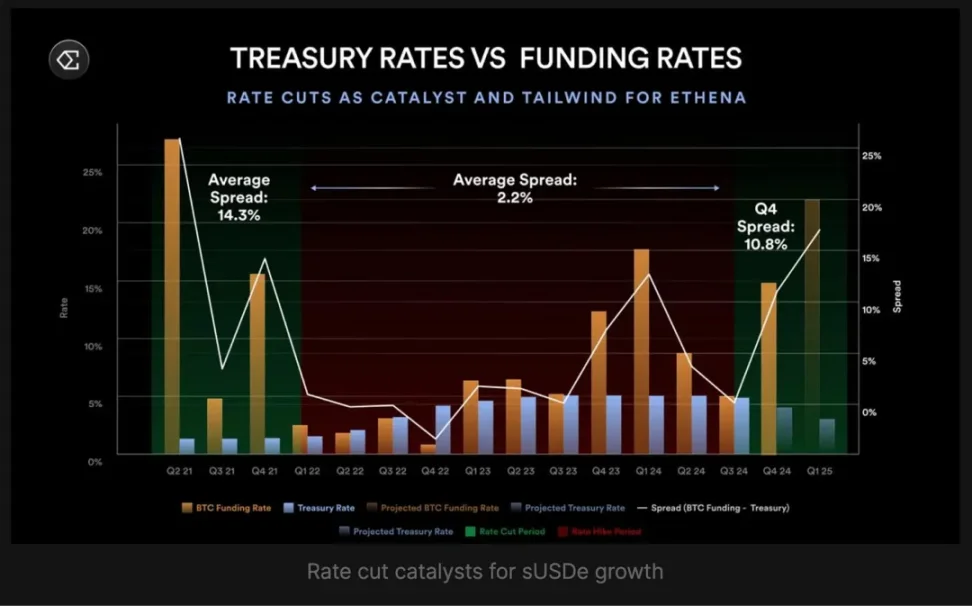

Federal Reserve Rate Cut Expectations: The market anticipates two rate cuts before the end of 2025, with an 80% probability of a cut in September. Rate cuts typically stimulate risk appetite, pushing funding rates up. The returns from USDe are negatively correlated with the federal funds rate, and rate cuts could significantly boost Ethena's income.

Image source: mirror.xyz

Fee Switch Proposal: Ethena's governance has passed a five-metric framework to allocate revenue to ENA holders. Four of the five metrics have been met: USDe supply exceeds $6 billion (currently $12.4 billion), protocol revenue exceeds $250 million (already over $500 million), Binance/OKX integration (completed), and sufficient reserve funds. The only unmet condition is that the yield of sUSDe must be at least 5% higher than that of sUSDtb, which is a key safeguard for the protocol and sENA holders.

Ethena has also established partnerships with traditional financial players and crypto exchanges, making USDe available across platforms from Coinbase to Telegram Wallet.

Institutional Frenzy

Unlike early stablecoins that relied solely on crypto-native use cases, USDe has attracted the attention of traditional financial institutions. Coinbase's institutional clients can directly access USDe, CoinList offers USDe with a 12% annualized return through its earn program, and major custodians like Copper and Cobo manage Ethena's reserve assets.

This institutional adoption model is similar to USDC and USDT, but the timeline is compressed. Traditional stablecoins took years to establish institutional relationships and compliance frameworks, while Ethena achieved this in just a few months. This is thanks to a mature regulatory environment and the allure of high yields.

Institutional adoption brings credibility, which attracts more capital, and more capital means greater funding rate capture, supporting higher yields and attracting more institutions. This is a continuously accelerating flywheel that can keep running as long as the underlying mechanisms do not fail.

However, it is important to note that the rapid growth of USDe has benefited from the groundwork laid by USDT and USDC, which have proven the utility, safety, and legitimacy of stablecoins.

The Square of Leverage

The high concentration of USDe on Pendle and Aave brings a "single point of failure" risk. If Ethena's model encounters issues, it will not only affect USDe holders but also impact the entire DeFi ecosystem that relies on Ethena's liquidity. 70% of Pendle's business and a significant amount of deposits on Aave are tied to Ethena. If USDe fails, it could trigger a liquidity crisis across the entire DeFi industry, not just a stablecoin decoupling.

Even more concerning is user behavior. The recursive lending cycles on Aave and Pendle amplify both returns and risks. Users stake USDe to obtain sUSDe, tokenize sUSDe on Pendle to receive PT tokens, and then use PT tokens to collateralize and borrow more USDe, creating a cycle. This leveraged multiplication of positions is reminiscent of the CDO square structure during the 2008 financial crisis—using one financial product to collateralize and borrow more of the same financial product, creating recursive leverage that is difficult to unwind quickly.

If funding rates remain negative, USDe may face redemption pressure, leveraged positions could trigger margin calls, and protocols relying on USDe's locked value may experience massive capital outflows, with the unwinding process potentially happening faster than any single protocol can handle.

Where Are the Risks?

Any high-yield strategy ultimately faces one question: what happens if it stops working? For Ethena, there are several potential risks:

- Sustained negative funding rates: If market sentiment remains bearish, Ethena will need to pay funding fees instead of collecting them. Their $60 million reserve fund provides a buffer, but it is not unlimited.

- Exchange counterparty risk: Although Ethena uses over-the-counter custody for spot assets, it still relies on major exchanges to maintain short positions. If an exchange goes bankrupt or is hacked, Ethena may need to quickly migrate positions, temporarily breaking delta neutral hedging.

- Liquidation risk of leveraged cycles: If USDe yields suddenly decline, recursive lending positions may become unprofitable, triggering a wave of deleveraging and selling pressure on USDe.

- Regulatory pressure: European regulators have forced Ethena to move from Germany to the British Virgin Islands. As yield-bearing stablecoins attract more attention, they may face stricter compliance requirements or restrictions.

Stablecoin Wars

Ethena marks a fundamental shift in the competition among stablecoins. In the past, competition revolved around stability, adoption rates, and regulatory compliance. USDC and USDT competed on transparency and regulation, while algorithmic stablecoins emphasized decentralization.

USDe changes the game with its yields. It is the first major stablecoin to offer double-digit returns to holders while maintaining a dollar peg. This puts pressure on traditional stablecoin issuers, who pocket all the treasury yields without sharing with users.

The market is responding. USDe's market share in stablecoins has surpassed 4%, second only to USDC (25%) and USDT (58%). More importantly, USDe's growth rate far exceeds both: in the past 12 months, USDT grew by 39.5%, USDC by 87%, while USDe grew by over 200%.

If this trend continues, the stablecoin market could undergo a fundamental reshaping. Users will shift from yieldless stablecoins to yield-bearing alternatives, forcing traditional issuers to either share yields or watch their market share erode.

Conclusion

Despite the risks, Ethena shows no signs of slowing down. The protocol has just approved BNB as a collateral asset, and XRP and HYPE tokens have also reached the inclusion threshold. This expands their market from ETH and Bitcoin to a broader range of assets.

The ultimate test is whether Ethena can maintain its yield advantage while managing systemic risks. If successful, they will create the first scalable and sustainable yield-bearing dollar in crypto history. If they fail, we will witness another dangerous tale of chasing high yields.

Regardless, USDe's achievement of reaching $12 billion in just 18 months proves that when innovation meets market demand, financial products can expand at an unimaginable pace.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。