Can Enterprises Leverage Ethereum to Replicate Strategy's Bitcoin Success?

Author: Terry Lee

Translation: Deep Tide TechFlow

A meme about companies holding cryptocurrency reserves.

Background

In August 2020, MicroStrategy (now renamed Strategy) shocked the financial world by investing millions of dollars of corporate treasury funds into Bitcoin. This strategy was once considered unbelievable, but it has now become a widespread choice for many publicly traded companies to combat inflation and unlock value. As Bitcoin solidified its position in corporate finance, a new question arose: can alternative coins like Ethereum provide enterprises with greater growth, innovation, or diversification opportunities? This article will explore why some companies choose to go beyond Bitcoin and adopt Ethereum as a treasury asset, and analyze whether this bold strategy can replicate MicroStrategy's success. By examining higher potential returns, access to an innovative blockchain ecosystem, and the long-term sustainability of this approach, I aim to reveal whether Ethereum can become a sustainable choice for corporate treasuries in 2025 and beyond.

Purpose of the Article

This article aims to explore whether publicly traded companies can successfully apply Strategy's Bitcoin leverage treasury strategy to Ethereum, focusing on a key metric called mNAV (market net asset value):

mNAV = Company Market Capitalization / Current Value of Token Holdings (mNAV = Market Capitalisation of Firm / Current value of token holdings)

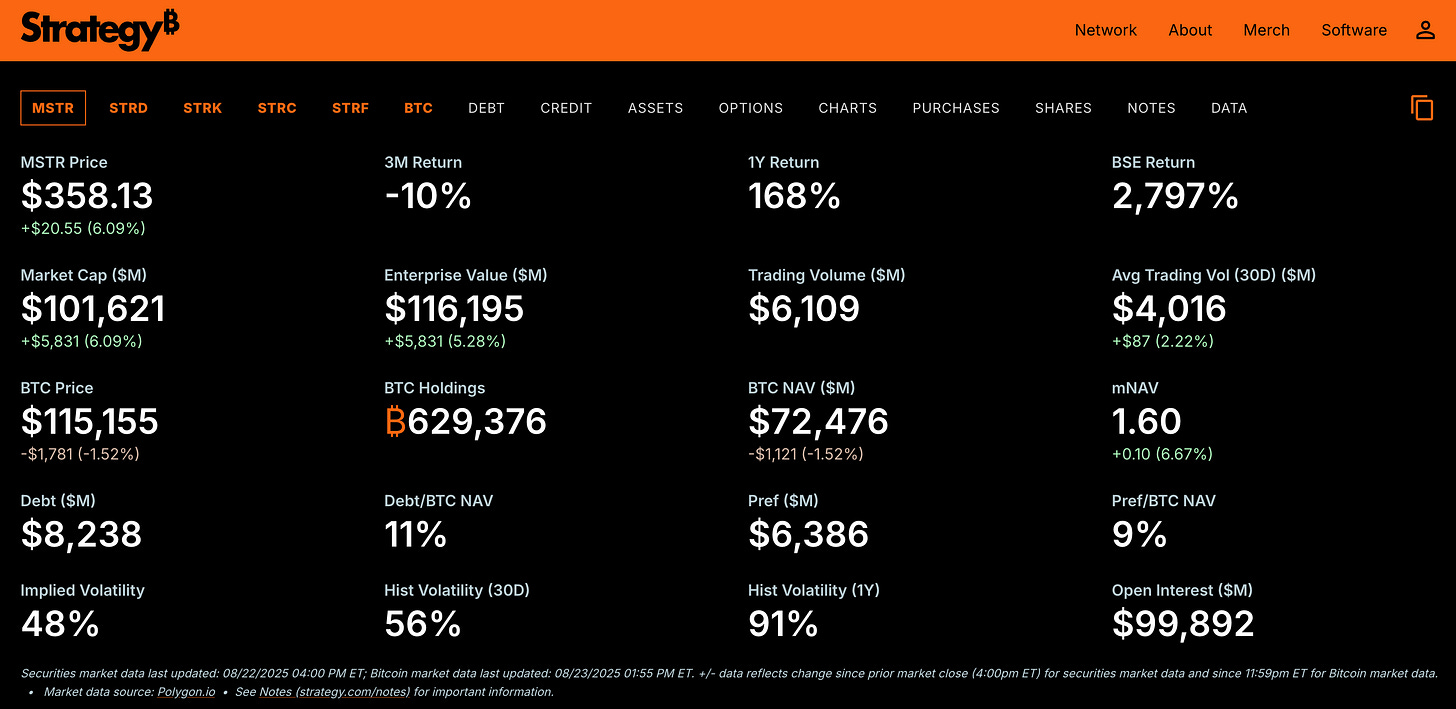

This metric is crucial as it helps readers understand why these treasury-holding companies are so fixated on it. The article will analyze why some companies choose Ethereum over Bitcoin, even though Strategy has proven its success with its holdings of 629,000 Bitcoins (valued at $72.5 billion in August 2025) and an mNAV of 1.6. The potential advantages of Ethereum include higher return rates (stemming from its growth potential), diversification beyond Bitcoin's "store of value" role, and participation in innovative blockchain ecosystems, such as Ethereum staking (locking ETH to support the network and earn rewards) and decentralized finance (DeFi) applications. Therefore, this article aims to reveal whether an Ethereum treasury strategy can provide better risk-adjusted returns or "alpha returns" while addressing higher uncertainties. To assess this, we will first analyze how Strategy's leveraged financing model drives its mNAV premium and provide a blueprint for companies considering Ethereum.

Financing Strategy

Strategy's Bitcoin treasury strategy was launched in 2020, driven by the need to protect corporate value from inflation and leverage Bitcoin's potential as a store of value. According to an article by BCB Group, Michael Saylor mentioned two main reasons for choosing Bitcoin:

Cost of Capital: Due to asset inflation triggered by stimulus policies and low yields on traditional assets (like bonds), the cost of capital soared to 25%. This rendered traditional assets unable to maintain their value storage function.

IRS Tax Guidance: The IRS treats Bitcoin as property rather than currency, making its tax treatment simpler compared to holding currency.

As Bitcoin prices rose, Michael Saylor achieved significant gains by raising funds from investors. The fundraising process can be simply divided into two parts: (1) equity financing; (2) debt financing;

(1) Equity Financing:

At-the-Market (ATM) Stock Sales: Strategy directly sold MSTR Class A common stock into the capital markets, a straightforward operation.

Preferred Stock: Buyers of convertible bonds receive a fixed "X"% dividend but do not have voting rights like common stock. Examples of such preferred stock include STRF or STRD, which have a face value of $100 and offer a 10% dividend.

(2) Debt Financing:

- Convertible Bonds: This is a debt instrument with a fixed maturity date but includes an option allowing bondholders to convert the bonds into MicroStrategy's Class A common stock at a predetermined conversion price. For example, Strategy's $3 billion zero-interest convertible senior bonds will mature in 2029, and investors can convert their bonds into common stock at a price of $672.40 per share. This price represents a 55% premium over the stock price at issuance, thereby delaying equity dilution.

Source: Strategy (https://www.strategy.com/)

Through equity and debt financing, Strategy expanded its Bitcoin reserves to nearly 630,000 BTC, valued at approximately $7.25 billion as of August 2025, while maintaining a market valuation premium, reflected in its mNAV of 1.6.

Notably, when mNAV is at a premium (mNAV > 1), Strategy issues new shares to sell at a price above the current net asset value (NAV) per share. For example, if mNAV is 1.6 and each share NAV is $100, new shares are sold at $160. The additional $60 raised will increase the company's cash reserves for purchasing more Bitcoin, thereby increasing total NAV (assets minus liabilities). Since the increase in the number of shares does not fully proportionately increase, the NAV per share rises, further enhancing investor confidence and creating a positive flywheel effect.

This leveraged financing strategy allows Strategy to purchase Bitcoin far beyond what its cash reserves would allow, achieving an mNAV range of 1.6 to 2.1 by 2025. During this period, its enterprise value (market capitalization + debt + preferred stock - cash reserves) exceeded the market value of its 630,000 Bitcoin holdings of $7.25 billion. As of August 2025, Strategy's enterprise value was approximately $11.6 billion, with its mNAV of about 1.6 reflecting investor confidence in its ability to increase per-share Bitcoin holdings through low-cost financing (such as zero-interest convertible bonds and ATM sales).

This financing method is more cost-effective than traditional bank loans, which typically come with higher interest rates. Additionally, by structuring the debt as non-recourse debt, this strategy protects Strategy's Bitcoin treasury in the event of a significant drop in Bitcoin prices, limiting creditors' claims to the bond terms rather than the company's Bitcoin or other assets. For investors, this leveraged strategy can amplify returns. For instance, a 10% increase in Bitcoin prices could lead to a stock price increase for Strategy exceeding 10% due to the mNAV premium. However, this also introduces risks: if Bitcoin prices fall, losses will be further magnified.

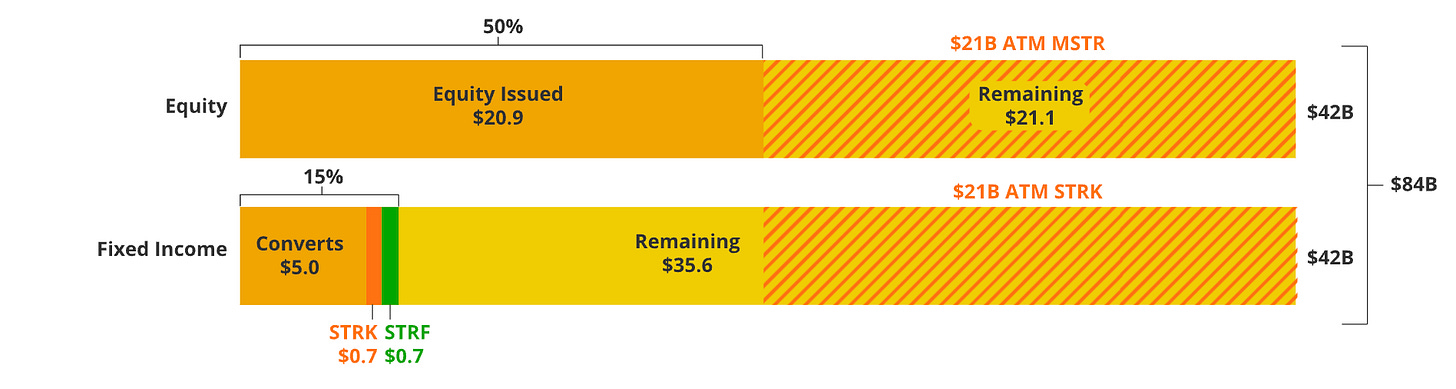

Source: VanEck - The chart shows the details of the $84 billion funding plan proposed by MicroStrategy.

Strategy's financing model, as outlined in VanEck's proposed $84 billion financing plan, demonstrates how leverage can maintain a high mNAV and provide a reference blueprint for altcoin treasury strategies. The next section will explore why publicly traded companies are beginning to choose Ethereum (Ether) and whether its leveraged strategy is feasible, as well as how to balance higher return potential with greater risk. The key to this shift towards Ethereum lies in execution, with specific details to be elaborated below.

Why Choose Ethereum (Ether)?

Having clarified how Strategy's leveraged financing model supports its Bitcoin treasury, the next question is whether this approach can be adapted for other altcoins like Ethereum.

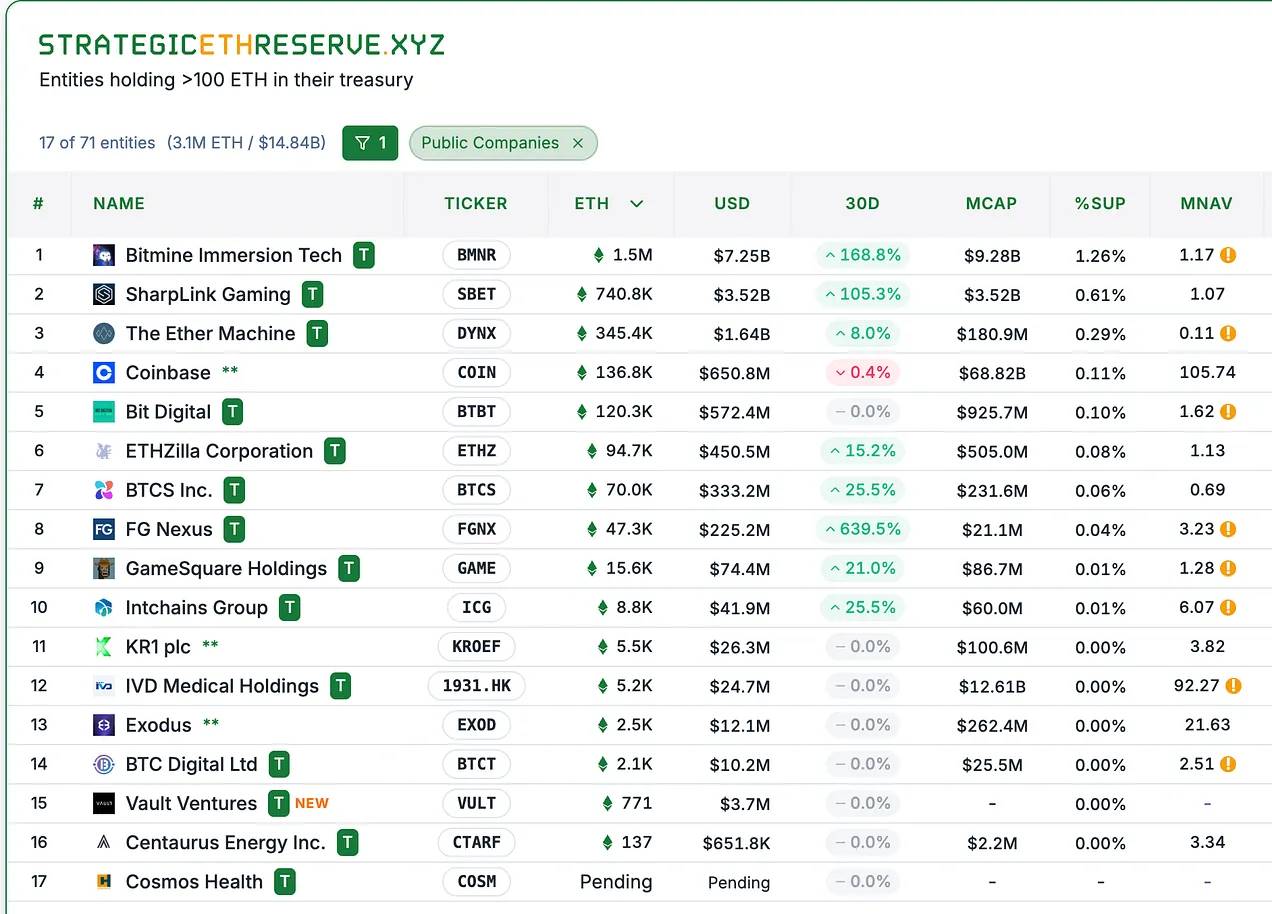

Source: StrategicETHReserve.xyz

Source: StrategicETHReserve.xyz and GameSquareHoldings (each website's mNAV adjusted to 0.84).

The above list shows eight publicly traded companies (excluding centralized exchanges like Coinbase). These companies either use cryptocurrency as a primary source of business, such as BTCS Inc, which engages in Bitcoin mining, or have ventured into the crypto space due to management decisions. For example, SBET hired Joseph Chalom, who previously drove Blackrock's digital asset initiative, as co-CEO.

According to my research, the overall reasons these companies explore holding Ethereum primarily include the following:

Growth Potential — Ethereum's market size is smaller compared to Bitcoin, which may lead to higher returns due to its growth trajectory, providing shareholders with better risk-adjusted returns than Bitcoin. For example, as of 2020, Ethereum's compound annual growth rate (CAGR) over the past five years was approximately 62.8%. However, it is important to note that past performance does not guarantee future results.

Staking Rewards — Ethereum offers staking rewards, meaning companies can earn additional premiums by staking their Ethereum assets. For instance, suppose a company plans to permanently hold $100 worth of Ethereum and sets a discount rate of 20% (assuming investors expect a 20% annual return on cryptocurrency). If the staking yield is 5%, the company can achieve a 25% premium on its mNAV just through staking.

Innovation-Driven — Companies holding Ethereum and other cryptocurrencies often actively participate in and support the development of the ecosystem, such as Ethereum staking, decentralized finance (DeFi), or scalable decentralized applications (dApps). These activities provide companies with richer added value than Bitcoin's "store of value" role.

First-Mover Advantage — Companies that choose Ethereum can position themselves as pioneers in holding ETH treasuries, similar to Strategy's breakthrough in 2020, attracting investor attention, especially as Ethereum gradually gains institutional recognition. This positioning offers a favorable risk-return ratio, as the demand for Ethereum is expected to increase with more institutional investors participating. Additionally, some companies even attempt to seize the opportunity to become the largest holders of Ethereum. This initiative sends a signal to the market that they are leading in capital raising and executing Ethereum purchases. This scale and efficient asset acquisition also enhance the company's credibility, attracting more capital inflow.

Success Factors

On the surface, one might think that the success of these treasury companies lies in their complex and often opaque models, which promise exponential growth and claim that "certain" tokens could grow 100 times in "N" years. However, I believe the core of these advantages lies in execution, particularly in the momentum of accumulation and efficient capital raising, which are crucial for maintaining altcoin (other cryptocurrencies) treasuries.

(1) Accumulation Momentum — The ability of companies to raise capital and their proactiveness in executing Ethereum purchase strategies play a key role.

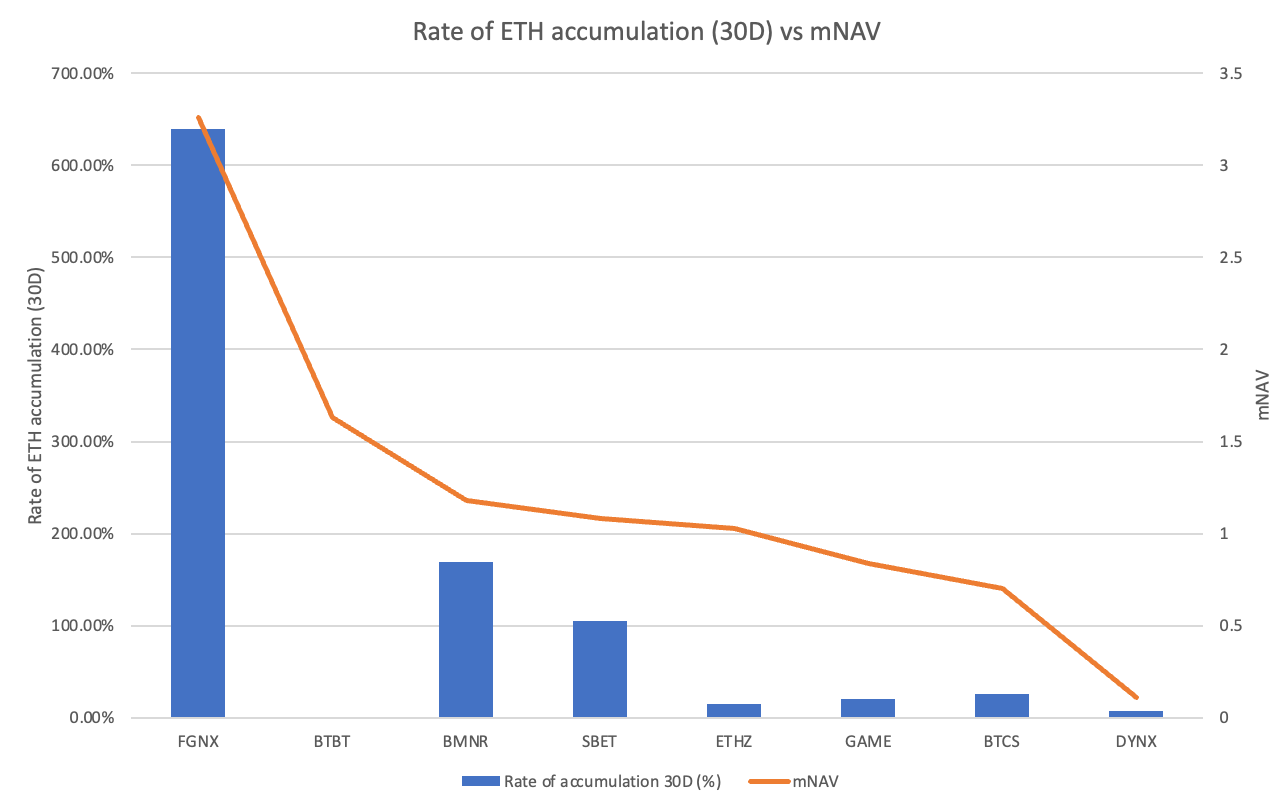

The relationship between Ethereum accumulation speed and mNAV

FGNX stands out with a 639% accumulation rate over 30 days. This figure far exceeds that of other companies, primarily due to FGNX's recent $200 million purchase of Ethereum and plans to announce the acquisition of 10% of the current Ethereum supply by July 2025. BMNR and SBET are also noteworthy, with accumulation rates of 169% and 105%, respectively, and they are still actively increasing their reserves. Other companies like GAME, BTCS, and DYNX have more moderate growth (below 30%), while BTBT's accumulation rate is 0%, indicating no recent Ethereum acquisition activity.

Clearly, except for BTBT, the companies with the highest accumulation rates (FGNX, BMNR, SBET) typically maintain high mNAV multiples (>1), but BTBT is an exception. This may be related to BTBT gradually scaling back its mining operations; due to declining revenues, the company is shifting towards an Ethereum treasury strategy, which may receive positive market recognition.

It is worth discussing that high accumulation funds continue to achieve higher net asset value premiums. For example, BMNR solidified its position as the world's largest ETH holder, holding 1.52 million ETH, primarily due to its aggressive ATM (at-the-market) equity issuance, and plans to raise up to $20 billion for further Ethereum purchases. SBET has also maintained a steady accumulation pace through a similar mechanism. In contrast, companies like DYNX (holding about 345,000 ETH post-SPAC merger) and BTCS (about 70,000 ETH) have limited net increases due to slower accumulation, with BTCS focusing more on Ethereum dividends rather than pure asset accumulation.

Data indicates that companies like FGNX, BMNR, and SBET, which continuously and actively accumulate Ethereum reserves, are viewed as reliable ETH asset management institutions, with their mNAV (adjusted net asset value) remaining above 1. In contrast, companies with slower accumulation struggle to achieve premiums (mNAV < 1), indicating that investors are not only focused on the Ethereum holdings on financial statements but also value the momentum of accumulation.

This model reveals a self-reinforcing mechanism: to survive, these companies need to excel at raising capital through premium stock issuances. This will enhance the net asset value per share, attract more investment, and ultimately achieve sustainable growth for the treasury. Conversely, low accumulation momentum may trigger a "death spiral."

When mNAV approaches or falls below 1, financing becomes more difficult, and issuing low-priced shares reduces the per-share value, creating a vicious cycle that may lead to stagnation or further discounts due to short sellers or capital outflows. This also explains why companies like DYNX and BTCS, facing post-merger challenges or adopting a conservative Ethereum dividend strategy, struggle to maintain mNAV premiums.

In contrast, the trend for Bitcoin treasuries is different, with over 79 publicly traded companies holding more than 4.5% of the Bitcoin supply, pioneering this trend, but their accumulation speed is slowing down. Additionally, about one-third of these companies trade below their net asset value, and premiums are shrinking. For example, MSTR's mNAV once reached 4 times, but now it is only about 1.61 times, despite Bitcoin prices hitting all-time highs.

This reduction in premium may be related to the market's excessive concentration on Bitcoin holding leaders (like MSTR, whose Bitcoin reserves are 12 times that of the second-place MARA), limiting growth opportunities for other companies. In contrast, Ethereum treasuries are still in a relatively early stage, with BMNR's Ethereum reserves only twice that of SBET, making the competitive landscape more open.

(2) Financing Strategy

I believe a secondary aspect is how these operators efficiently raise funds from investors. The case of BMNR is particularly typical, as it plans to raise up to $24.5 billion ($4.5 billion already raised + $20 billion target). Although this operation inevitably dilutes existing shareholder equity, under mNAV premiums (>1x), capital raising can translate into net gains in net asset value (NAV) per share, achieved through premium stock issuance.

When BMNR issues shares at an mNAV premium (e.g., 1.18) and sells at a price above NAV (e.g., selling $100 NAV shares at $118), it can achieve this. The additional $18 per share can increase the funds available for purchasing Ethereum, thereby increasing total NAV (assets minus liabilities) and raising NAV per share with limited dilution.

This strategy is particularly evident in BMNR's ATM stock sale plan, which launched on July 9 with a target of $250 million, increasing to $2 billion by July 24. As of the most recent date, August 12, this total target commitment has further increased to $24.5 billion. BMNR plans to purchase 5% of the Ethereum supply (approximately 6 million ETH), a bolder move than Strategy's use of $84 billion to purchase a smaller proportion of Bitcoin supply.

Through its $10.8 billion market capitalization, BMNR seeks to achieve disproportionate treasury growth. This strategy may further enhance its current mNAV premium (1.2), creating a positive flywheel effect: increased investor confidence leads to more capital raising, further increasing Ethereum holdings and enhancing NAV per share.

On the other hand, if mNAV falls below 1 (e.g., DYNX's mNAV is 0.11), they are effectively issuing shares at a discount (e.g., $11 per share for $100 shares), raising only $11 million for every million shares, which will only add limited Ethereum reserves while diluting NAV per share to about $90. This situation erodes company value, triggering a "death spiral," further exacerbating discounts and being extremely detrimental to shareholders. Therefore, when a company's mNAV approaches or falls below 1, it may prioritize share buybacks over continued Ethereum purchases to stabilize stock prices and shareholder equity.

Conclusion

In summary, while Strategy's Bitcoin treasury model has set a precedent by consistently maintaining mNAV above 1, Ethereum offers an attractive alternative for companies seeking higher growth, returns, and systemic innovation.

Companies like BMNR, SBET, and FGNX demonstrate the potential for sustainable treasury holding models by actively accumulating Ethereum and efficiently raising capital under mNAV premiums (>1x), similar to Strategy's success.

However, as more companies adopt this strategy, competition intensifies, and those failing to meet expectations, like DYNX and BTCS, will face challenges unless new driving factors emerge.

With the growth of institutional adoption, the number of Ethereum held in treasuries is expected to exceed 3 million by 2025, making Ethereum a potentially sustainable alternative asset that offers better risk-adjusted returns, provided they can successfully avoid the pitfalls of the "death spiral."

Ultimately, the future of Ethereum treasuries depends on execution, and 2025 will be a critical moment to test whether this strategy can surpass Bitcoin's mature path.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。