Priority fees are the main source of revenue for Base, accounting for 86% of its total earnings.

Written by: Zack Pokorny

Translated by: Luffy, Foresight News

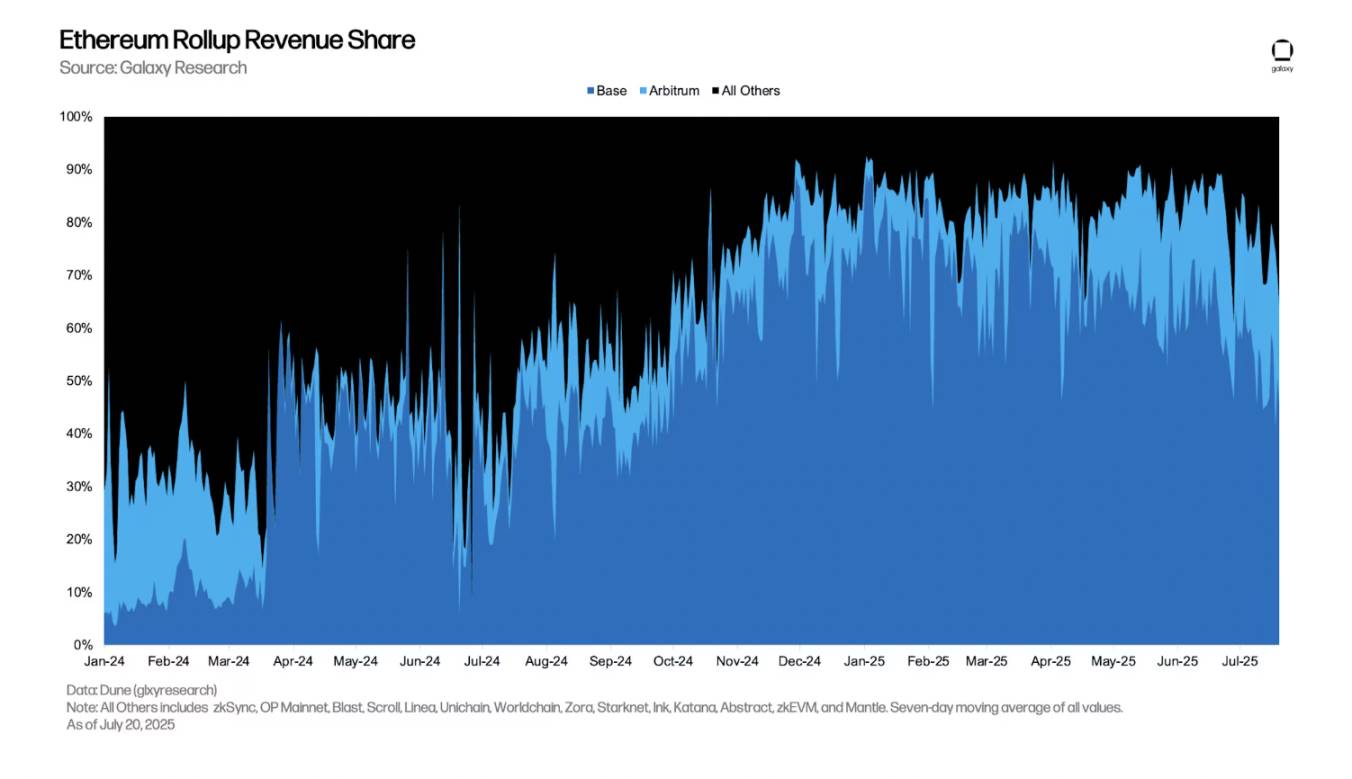

Base, created by the cryptocurrency exchange Coinbase, is the most revenue-generating platform in the Ethereum Layer 2 (L2) network, with daily earnings often exceeding the total of all other top Rollup projects. In the past 180 days, Base's average daily earnings reached $185,291, far surpassing the $55,025 of the second-ranked Arbitrum.

Clearly, Base has become a platform with consistently high revenue, but what drives its economic activity? What advantages does Base have over other leading L2s that allow it to create such high value?

This report will explore Base's fee structure and highlight the activities driving its revenue growth. We find that Base's sorting mechanism and decentralized exchange (DEX) activities are key drivers.

Base's Transaction Sorting Mechanism

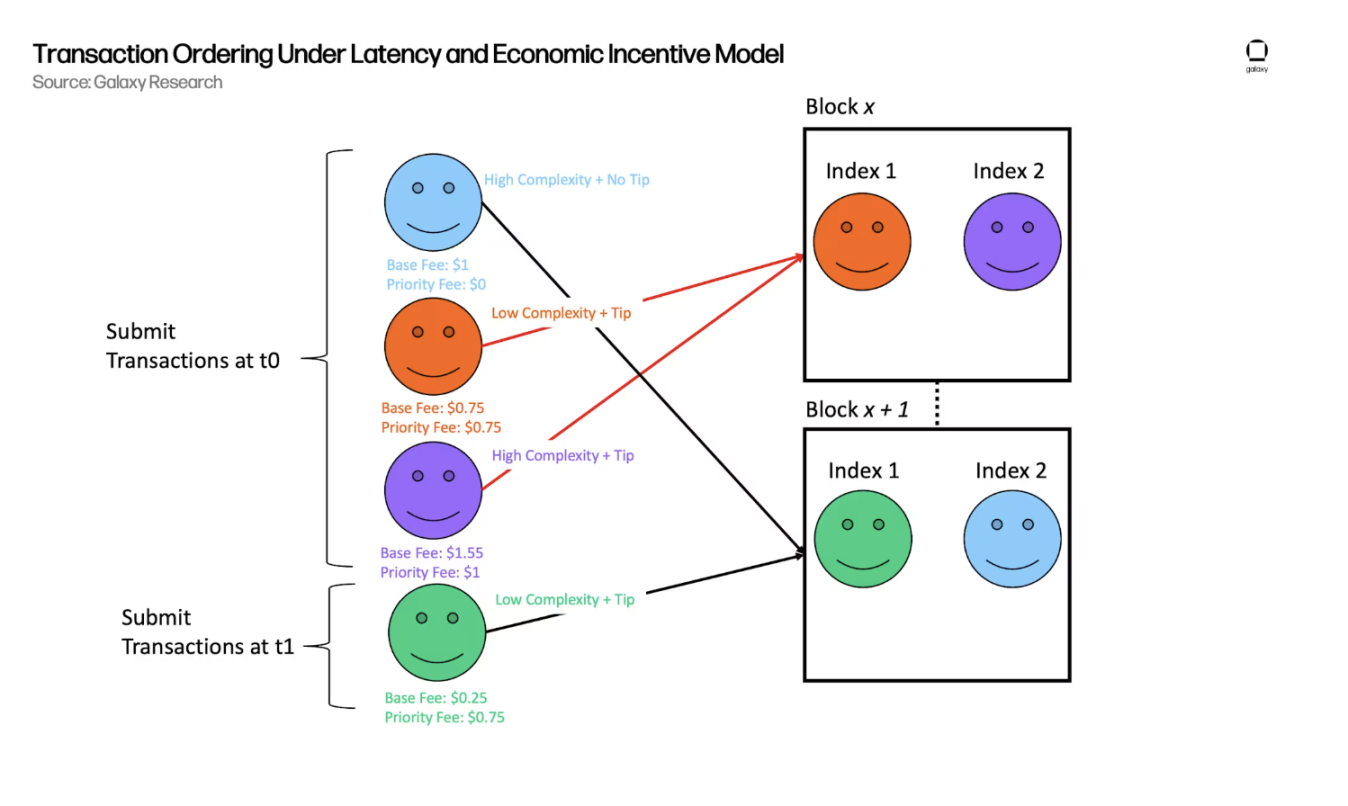

The transaction sorting on Base is determined by two variables:

Transaction submission time (latency);

The fee paid by the sender relative to the transaction complexity (economic incentive).

This mechanism is similar to the operational model of logistics companies like UPS: packages are sent in the order they are delivered by users, while allowing senders to pay extra fees for "expedited" delivery for faster service. The priority fee mechanism creates a dynamic auction market, consistent with the Ethereum EIP-1559 fee model, balancing delivery time and economic incentives.

Specifically, transactions on Base include a "base fee" (lowercase "b", do not confuse with the chain name) and a priority fee: all users must pay the base fee when sending transactions, while the priority fee is optional and only used to expedite transaction execution.

But how do sorters decide which "expedited" transaction to prioritize? They do not directly consider the total fee but focus on the bid per unit of Gas (the required computational resources), that is, the cost-effectiveness of the resources required for the transaction versus the revenue it brings.

Let’s illustrate this with the logistics company example: suppose the delivery truck has limited space (similar to the Gas limit of a block), and the driver (the sorter) wants to maximize tip income within that limited space. At this point, there are two packages:

A large package with a base shipping cost of $50, but a priority tip of only $10, taking up half the truck space;

A small package with a base shipping cost of only $20, but also a priority tip of $10, taking up very little space.

Even though the total cost of the large package is $30 higher than the small package, the driver will prioritize loading the small package because it has a better cost-effectiveness in terms of space occupied.

Base's sorters follow the same logic, prioritizing transactions with the highest priority fee per unit of Gas, ensuring that the blocks with the "highest cost" of computational resources are also the most profitable. Therefore, when two users submit transactions simultaneously, regardless of transaction complexity or total fees, the user paying a higher priority fee per unit of Gas is more likely to have their transaction prioritized in the block.

The following diagram illustrates this process:

Why is this important? How does Base differ from competing chains?

Base's EIP-1559 style fee model creates a continuous public market auction environment for block space, allowing users to bid directly for block space based on the urgency and profitability of their transactions. Thus, although there are still latency competition factors, the economic benefits allow sorters' income to grow directly with the demand for block space and the profitability of on-chain transactions.

This sharply contrasts with Arbitrum's primary sorting mechanism. Arbitrum adopts a strict "first-come, first-served" (FCFS) model, where users primarily compete on latency rather than economic cost. In this model, the main competition is not about who can pay more fees, as all users have the same Gas fee and do not use priority fees, but rather who can deliver their transaction to the sorter the fastest. This leads to a "latency race," where professional participants ensure their transactions are prioritized by investing in low-latency infrastructure. In this environment, Arbitrum's fees only grow with demand scale and do not effectively reflect the profitability or urgency of individual transactions.

In April 2025, Arbitrum launched the Timeboost feature, aimed at creating a more flexible FCFS system that allows sorters to earn similar to priority fees. In practice, Timeboost added a "fast lane" for transaction execution on Arbitrum, where users can bid to use this lane for a limited time. Users entering the fast lane can achieve near-instant execution, while other users are still processed in FCFS order, only adding a 200-millisecond delay to compensate for the priority of the fast lane. Although Timeboost introduced some form of priority bidding, its mechanism is more predictive than reactive compared to Base's priority fee model. Bidders must predict the potential total revenue for a future time period and bid based on estimates. This means Arbitrum receives fixed fees from winning bidders, regardless of the actual revenue situation during that time period. This proactive fixed-rate model is less effective than a reactive system where users bid individually for each transaction in capturing the value of sudden high-revenue transactions.

How much revenue does Base generate?

In the past 180 days, Base's average daily earnings were $185,291. In contrast, Arbitrum's average daily earnings were $55,025, and the combined average daily earnings of the other 14 Ethereum L2 networks were $46,742.

So far this year, Base's total revenue has reached $33.4 million, while Arbitrum's was $9.9 million, and the other 14 L2 networks totaled $8.4 million.

Relatively speaking, in the past 180 days, Base accounted for 64% of the total revenue of the top 15 Ethereum L2 networks ranked by total value locked. Its share has significantly increased over the past year, rising by 48 percentage points from an average daily share of 37% in July 2024. As of July 20, due to increased activity on other chains, Base's share of Ethereum Rollup revenue has decreased to 49.7%.

The Important Role of Priority Fees

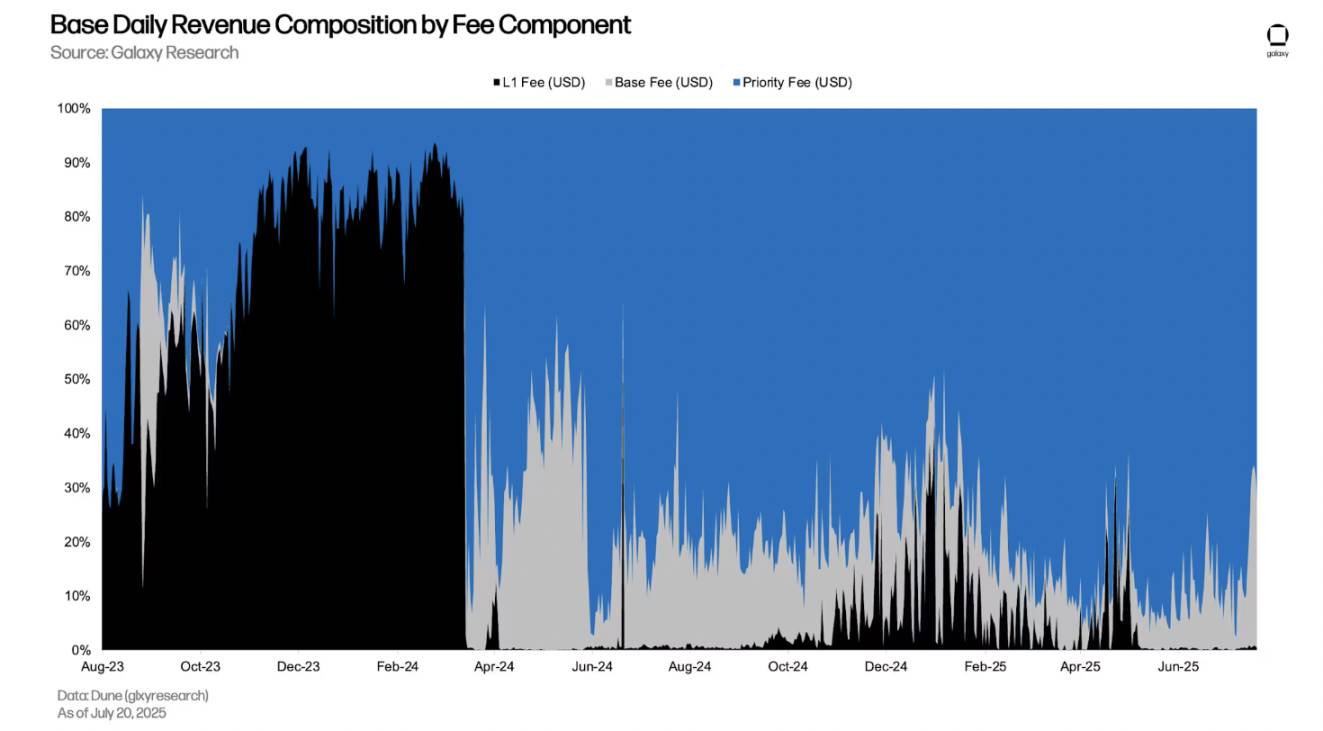

Transaction fees on Base consist of two main parts and an optional priority fee:

Layer 1 (L1) fees: used to pay the cost of submitting a batch of L2 transactions to the Ethereum mainnet. After the Ethereum Pectra upgrade in March 2024 introduced "blobs" (data blocks) through EIP-4844, the L1 fee portion for Base (and general L2 transactions) has significantly decreased. This is because submitting batch data through blobs is more economically efficient than submitting it in L1 transactions as call data.

Base fee: a mandatory fee for executing transactions on Base. Set by the protocol, it fluctuates based on the usage level of the previous block space—the busier the network, the higher the base fee; conversely, the lower it is.

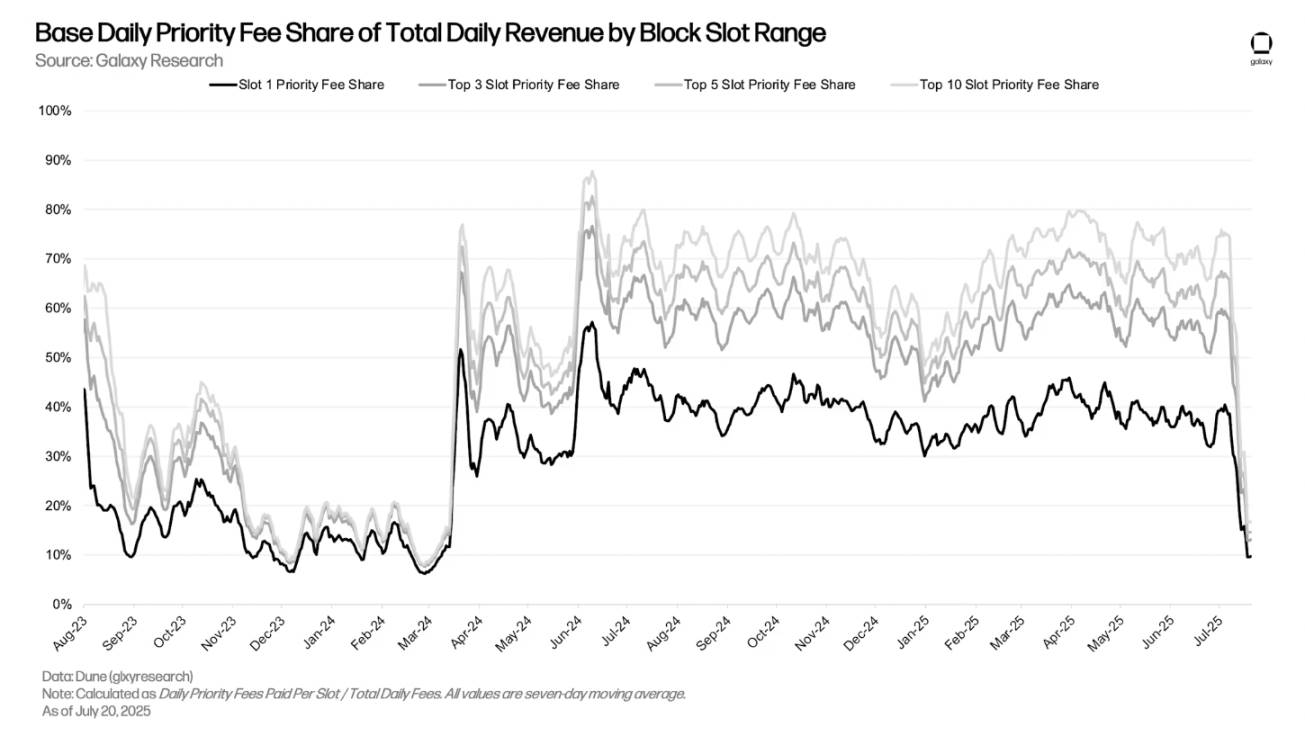

Priority fee: an optional fee, also known as a "tip," used to prioritize transaction execution. The priority fee helps transactions gain a more favorable position in the block or ensures that transactions are included in the current block rather than delayed to the next block. A block can contain thousands of transactions, which are executed in order of their slot. Typically, the first slot in a block is the most valuable because the transaction in that position is executed first and is not affected by subsequent transactions.

Priority fees are the main source of Base's revenue, with users bidding for expedited execution. In the past 180 days, Base's average daily priority fee revenue reached $156,138, accounting for 86.1% of its average daily earnings.

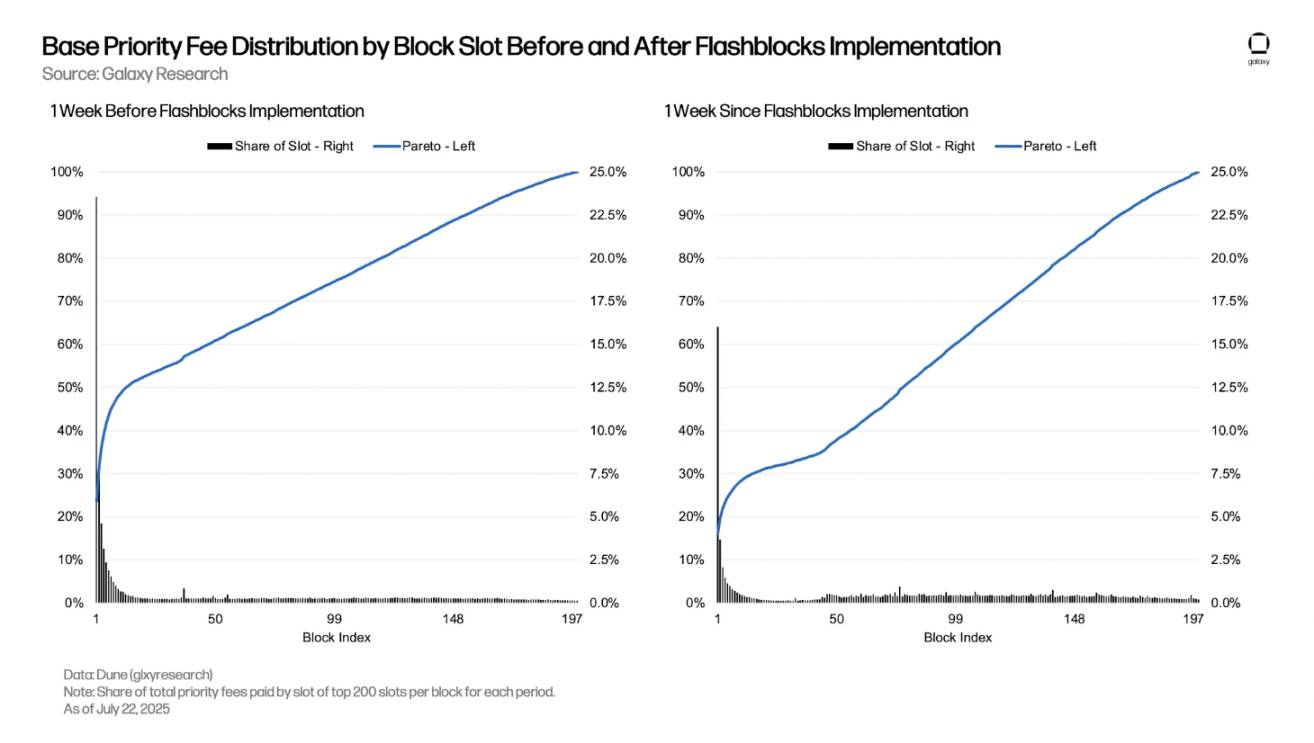

Specifically, the priority fees for the top slot of Base blocks are significant contributors to sorter revenue, as users compete for positions near the top of the block. Since 2025, transactions in the first slot of the block alone have contributed 30% to 45% of daily revenue from priority fees. Additionally, during the same period, transactions in the top 10 slots of each block contributed 50% to 80% of daily revenue from priority fees. However, in the weeks following July 5, the share of top slot priority fees in total daily revenue significantly decreased. This is attributed to two factors: 1) Increased traffic raised the base fee, thereby diluting the share of priority fee revenue; 2) The implementation of "Flashblocks" on July 16 (which will be detailed below) caused high-priority transactions to fall into lower slots in the block (but as we will see, this is not necessarily a bad thing).

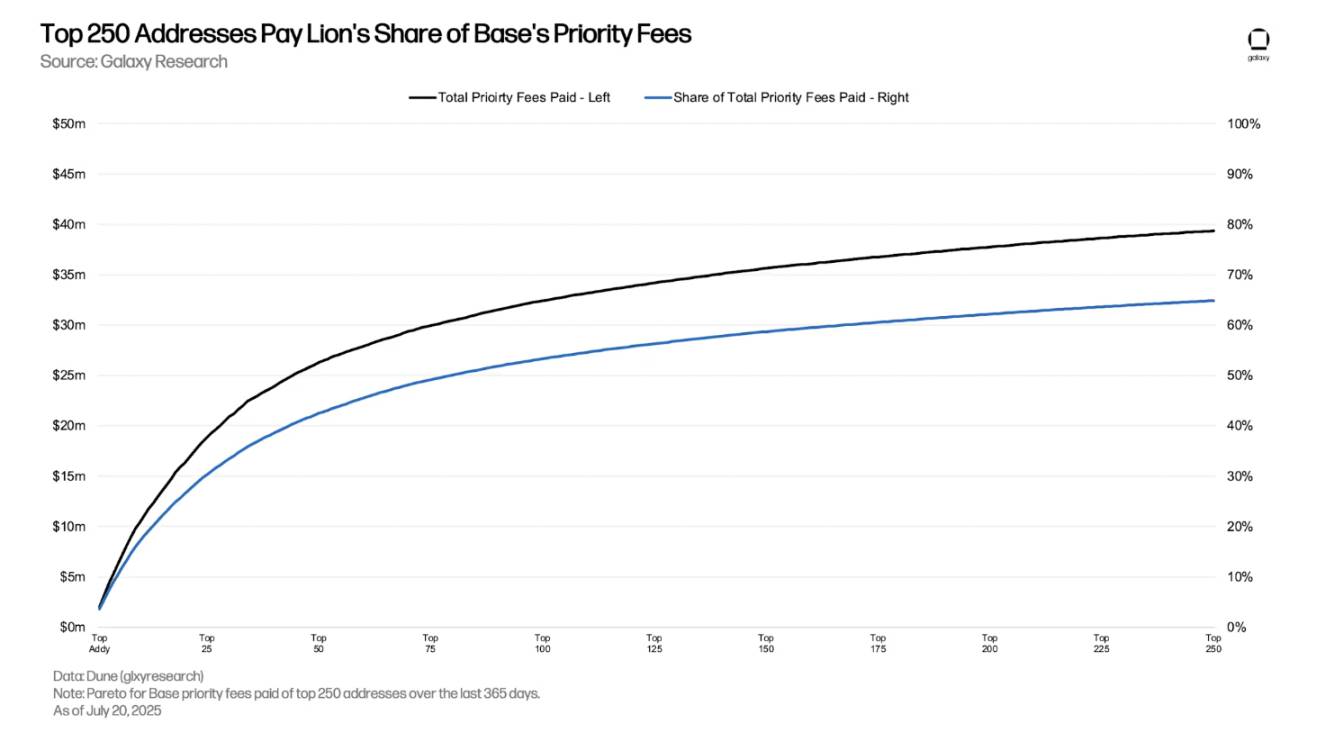

Priority fees mainly come from a small number of addresses, with 64.9% of priority fees in the past year coming from just 250 addresses. The top address alone accounted for 3.6% of all priority fees during the same period, which, based on the ETH price at the time of payment, equates to $1.99 million.

What are Flashblocks?

Developed by Flashbots, Flashblocks aims to improve transaction processing speed on Base. To achieve this, it introduces "sub-blocks," which are high-confidence pre-confirmations of block sub-sections created approximately every 200 milliseconds. For example, a block can contain three different sub-sections, allowing users to receive pre-confirmations of these transactions before the block is confirmed on-chain at the set 2-second interval. This means that even if Base's block interval remains unchanged, end users can experience transactions as if they are completed almost instantaneously, resulting in a smoother and more responsive experience.

Why is this crucial for analyzing Base network fees by slot? Because from the perspective of transaction sorting, each "sub-block" is effectively treated as a new block. Therefore, high-priority fee transactions may fall into lower slots of the overall "confirmed block," but be at the top of the "pre-confirmed sub-block."

The following diagram illustrates the difference in the distribution of priority fees for the top 200 block slots before and after the implementation of Flashblocks. The black bars represent the proportion of priority fees for each slot; the blue line represents the cumulative proportion of all slots up to that slot (Pareto distribution).

In the week before the implementation of Flashblocks, the Pareto curve sharply rose in the top 10 slots and then increased linearly towards the 200th slot. In contrast, in the week following the implementation of Flashblocks, the Pareto curve was relatively flat at the lowest slots, only beginning to steeply rise around the 50th slot of each block—indicating that high-priority fee transactions are falling into later slots of confirmed blocks.

Impact of DEX Transactions

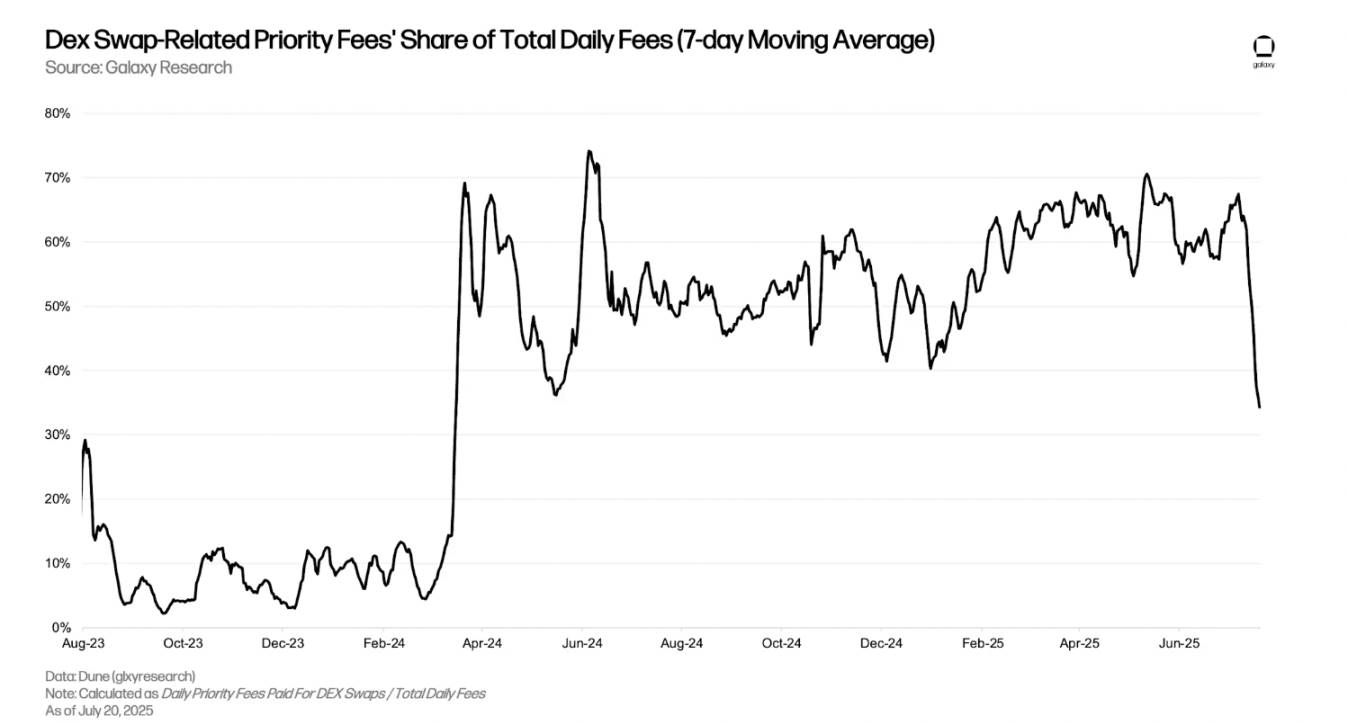

DEX activity on Base is very active. Among all Ethereum L2 networks, Base has the highest daily DEX trading volume, accounting for 50% to 65% of L2 network DEX trading volume, and its DEX total value locked (TVL) is the highest among all L2 networks (excluding perpetual futures DEX).

The active DEX activity is a significant reason for Base's high priority fees. Between 50% to 70% of the total fees earned by Base sorters daily come from priority fees on DEX transactions. However, since July 7, the proportion of DEX transaction fees in the total daily fees has dropped from 67% to just 34%. This is attributed to two factors: 1) The rise in base fees has diluted the share of priority fees; 2) Increased competition for on-chain block space has forced users to pay priority fees for non-DEX transactions.

Since 2025, priority fees from DEX transactions in the first slot alone have contributed 30% to 35% of the total daily priority fees, while priority fees from DEX transactions in the top three slots have contributed 50% to 62% of the total daily priority fees. The recent decline in the share of DEX priority fees in the top slots is due to increased overall competition on-chain leading to higher priority fees for non-DEX transactions, as well as the implementation of Flashblocks causing high-priority DEX transactions to fall into lower slots in the block.

Conclusion

Through the analysis of Base's DeFi and revenue structure, we find:

Priority fees constitute the vast majority of revenue;

Over 60% of priority fees in the past year came from just 250 addresses;

High DEX trading volume and TVL;

Priority fees from DEX transactions contributed nearly three-quarters of the total priority fees.

These points indicate that maximum extractable value (MEV) transactions, especially competitive activities like DEX arbitrage, are significant sources of revenue for Base sorters. The EIP-1559 style fee model adopted by sorters is a direct mechanism for achieving this: it transforms block space competition from an inefficient latency-based race into an efficient economic auction.

By charging priority fees to users willing to pay for urgent inclusion, this model allows sorters to capture and commercialize the competitive value of block space more effectively than traditional "first-come, first-served" or purely latency-driven systems.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。