撰文:Nathan Frankovitz

原文:《VanEck Mid-July 2025 Bitcoin ChainCheck》

Please note that VanEck has exposure to bitcoin and may have positions in bitcoin mining stocks mentioned.

Three key takeaways for mid-June – mid-July:

- Inflation, Inflation, Inflation: BTC surged to new all-time highs above $123K, fueled by dollar weakness, rising fiscal pressures, and the House’s passage of pro-crypto bills during July’s “Crypto Week.”

- Bitcoin Miners Are Being Rerated, But Not Equally: The Core Scientific-CoreWeave deal validated AI infrastructure pivots, but shareholder dilution and strategic absorption sent a warning: execution matters.

- ETP Inflows Roar Back, Driving ETH Rotation: ETH ETPs pulled in $2.2B during Crypto Week—nearly 30% of their all-time flows—triggering ETH/BTC outperformance and the sharpest BTC Dominance drop of the year.

Bitcoin ChainCheck Monthly Dashboard and Highlights

| As of July 21st, 2025 | 30-day avg | 30 day change (%) 1 | 365 day change (%) | Last 30 days Percentile vs all-time history (%) |

| Bitcoin Price | $111,197 | 5 | 82 | 100 |

| Daily Active Addresses | 721,874 | -2 | 1 | 64 |

| Daily New Addresses | 307,623 | 1 | 9 | 56 |

| Daily Transactions | 388,116 | 9 | -34 | 75 |

| Daily Inscriptions | 98,557 | 146 | 261 | 55 |

| Total Transfer Volume (USD) | $68,526,433,925 | 13 | 59 | 90 |

| % Supply Active, last 180 days | 21% | -10 | -16 | 55 |

| % Supply Dormant for 3+ Years | 45% | 0 | -3 | 92 |

| Avg Fees (USD) | $143,252.42 | -7 | 44 | 86 |

| Avg Fees (BTC) | 1.28809 | -11 | -21 | 65 |

| Percent of BTC Addresses in profit | 99% | 1 | 13 | 97 |

| Unrealized profit/loss ratio | 0.56 | 1 | 13 | 80 |

| Global Power Consumption (TWh) | 169 | -3 | 45 | 99 |

| Total Daily BTC Miner Revenues (USD) | $50,662,629 | 4 | 78 | 97 |

| Total Crypto Equities' Market Cap * (USD) (MM) | $306,825 | 35 | 133 | 100 |

| Transfer volume from Miners to Exchanges (USD) | $15,504,275 | 11 | 130 | 95 |

| Bitcoin Dominance | 64% | 1 | 19 | 96 |

| Bitcoin Futures Annualized Basis | 6% | -16 | -44 | 37 |

| Mining Difficulty (T) | 122 | -3 | 50 | 99 |

* DAPP market cap as a proxy, as of June 19th, 2025.

1 30 day change & 365 day change are relative to the 30-day avg, not absolute.

| Regional Trading ($) | MoM Change (%) | YoY Change (%) |

| Asia Hours Price Change MoM | 0 | 3 |

| US hours Price Change MoM | 3 | 1 |

| EU hours Price Change MoM | 0 | 2 |

Source: Glassnode as of 7/21/2025. Past performance is no guarantee of future results. Not intended as a recommendation to buy or sell any securities named herein.

Bitcoin Price: Bitcoin punched to new highs—at least in U.S. Dollar terms—above $123K this month. However, the move coincided with the U.S. Dollar Index (DXY) falling to its lowest level since February 2022. We reiterate our previous research showing that Bitcoin’s negative correlation with USD strength remains one of its most persistent and defining macro relationships.

The One Big Beautiful Bill Act (“BBB”), passed on Independence Day, raised the U.S. debt ceiling by $5 trillion , fueling inflation fears and boosting Bitcoin’s appeal as a hedge. While crypto-specific amendments (e.g., tax exemptions, staking rules) were excluded from the OBBBA due to partisan gridlock and time constraints, the Trump administration’s pro-crypto stance spurred optimism. During “Crypto Week” in July, the House advanced the GENIUS Act (regulating stablecoins, which the Senate had previously passed), the CLARITY Act (enhancing SEC/CFTC oversight), and the Anti-CBDC Surveillance State Act, reinforcing a positive outlook for cryptocurrencies. Institutional ETP inflows further supported Bitcoin’s rally, discussed below.

Bitcoin Futures Annualized Basis: The basis trade is a popular delta-neutral strategy among institutions in the Bitcoin market, where they hold spot BTC while selling BTC futures contracts, capturing the premium paid by bullish traders who believe Bitcoin’s price will increase. The annualized rate of return from this strategy, or the premium traders pay, serves as a proxy for bullish sentiment. Despite record-high prices, this medium-term signal is down 16% month-over-month, potentially signaling de-risking from June’s elevated rates. After Bitcoin’s 54% run-up from lows around $76K on April 8th to $117K on July 20th, we read this as healthy for Bitcoin’s medium-term outlook.

However, we note that BTC’s perpetual futures borrowing rates are elevated versus last month’s. Serving as a better indicator of shorter-term sentiment, we believe this signals a potentially overheated market due for correction. We also note that with the emergence of treasury companies like MSTR this market cycle, much of the leverage in Bitcoin markets is nested in corporate balance sheets. All else equal, we warn that basis trade premiums may not reach as high as the peak of this market cycle as they did during the last market cycle.

Bitcoin Dominance: While Bitcoin Dominance’s (BTCD) 30-day moving average is flat month-over-month, it may finally be inflecting. At the time of writing, on July 21st, BTCD is at 60.6% , presently in free fall from a peak of 66.0% on June 27th. While BTC prices have retraced slightly since peaking July 14th, the decline in BTCD is more so due to surging altcoin prices, particularly Ethereum. On July 18th, the total market value of cryptoassets crossed $4 trillion for the first time.

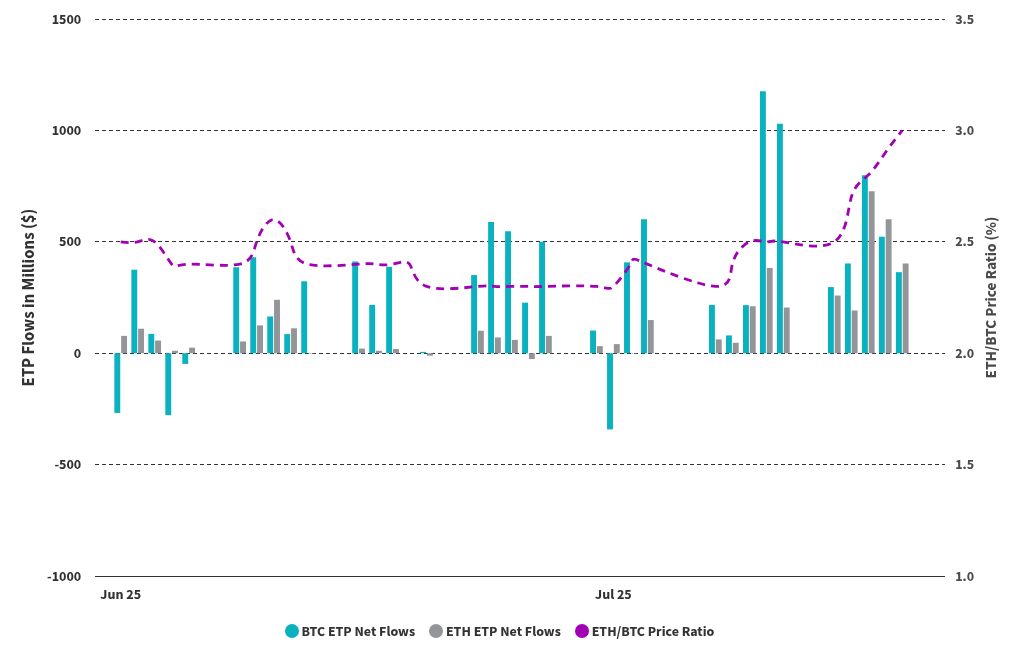

ETH ETPs Recorded Record Flows on July 16th, Driving Price Outperformance vs. BTC ETPs

Source: Farside Investors, Artemis, as of 7/21/2025. Past performance is no guarantee of future results. Not intended as a recommendation to buy or sell any securities named herein.

Ethereum ETPs posted back-to-back record flows on July 16th and 17th, adding $727 million and $602 million , respectively. In total, 29% of the all-time flows into ETH ETPs were added during “crypto week” alone.

Fortunately for Bitcoin, this isn’t a zero-sum game: in July, BTC ETPs saw two days of $1 billion net inflows, on track for the biggest month since November 2024.

Daily Inscriptions: After reaching lows not seen since November, Ordinals transactions picked back up again in July as Bitcoin’s rally renewed traders’ speculative enthusiasm. Per Cryptoslam.io data, daily Ordinals volume averaged $1.9 million in June versus $2.6 million so far in July (+37%) , with $11.6 million of volume on July 13th marking the highest daily volume since December 2024. Despite the turnaround, Ordinals activity remains niche, lagging behind Ethereum NFTs’ average of $3.3 million of trading volume in June, versus $6.7 million (+102%) so far in July.

Mining Difficulty: On June 29th, Bitcoin’s network difficulty dropped ~7.5% , from 126T to 117T , following widespread miner curtailments across Texas amid extreme heat. From peak to trough, Bitcoin’s hashrate fell from 1,006 EH/s on June 11th to 649 EH/s on June 24th, marking one of the sharpest difficulty drops (-3% MoM) since the 2021 China mining ban. Texas’s independent ERCOT grid, which has long been favored by miners for its cheap and abundant wind and solar electricity, can mandate shutdowns during peak demand events. Miners participating in these programs are compensated through energy credits or grid payments, effectively reducing their all-in power costs.

Meanwhile, several large-scale miners, including CORZ, IREN, and BITF, have paused upgrades or begun downsizing their mining fleets to pursue AI data center opportunities. Because Bitcoin’s issuance is fixed, miners who remain operational during curtailment or HPC pivot cycles benefit from improved economics, all else equal.

Crypto Equities Market Cap: With its 30-day moving average up 35% month-over-month, 133% year-over-year, the MVIS ® Global Digital Assets Equity Index (MVDAPP) reached new all-time highs this July, delivering significant alpha versus Bitcoin (more below).

Chart of the Month: Bitcoin Miner Rally Lifts MVIS ® Global Digital Assets Equity Index (MVDAPP) 59% from June to Mid-July, Outpacing Bitcoin’s 15% Gain

Source: Glassnode, MarketVector as of 7/21/2025. Past performance is no guarantee of future results. The MVIS ® Global Digital Assets Equity Index (MVDAPP) tracks the performance of the largest and most liquid companies in the digital assets industry. Index performance is not representative of strategy performance. Past performance is no guarantee of future results. Not intended as a recommendation to buy or sell any securities named herein.

MVDAPP returned +59% since May, driven by surging values in Bitcoin mining and treasury stocks including IREN, MARA, and MTPLF, marking the Digital Assets Equity Index’s best outperformance of Bitcoin so far this market cycle.

The move comes amid a wave of renewed interest in Bitcoin miners’ AI/HPC potential, driving outsized returns from miners with plausible capacity for neocloud tenants. In late June, The Wall Street Journal reported that Core Scientific—the Bitcoin mining company with the gold-standard hosting contract worth approximately $ 9 billion —was in talks to be acquired by its tenant, CoreWeave. This spurred investment activity in the sector and more recently developed into a formal deal announcement (discussed below).

We see clear signs that the Bitcoin mining sector is undergoing a rerating as a result. However, we also think this is a stock-picker’s market; nearly one year after we first noted their opportunity in AI, we see a Bitcoin mining market with increasingly dispersed strategies.

Bitcoin Miners: AI Gets Validated, Value Remains Stratified

To evaluate and compare Bitcoin miners, we begin with their hash rate. Measured in exahash per second (EH/s), this figure represents a miner’s total computational capacity and reflects both the scale and efficiency of its operations. Scale is determined by how much power (in megawatts) the miner has energized, while efficiency reflects the quality and age of its mining rigs. When benchmarked against enterprise value (equity + debt – cash), EH/s becomes a useful lens through which to assess a miner’s two core competencies: 1) acquiring energy at scale, and 2) converting that energy into computational work as cost-effectively as possible.

As the chart below shows, adjusting for bitcoin holdings reveals stark differences in how the market is valuing miners’ core operating businesses.

After Stripping Out BTC Holdings, HIVE and CANG's Operating Businesses are Priced Near or Below $0 per EH/s

Source: Bloomberg, Company Filings, VanEck Research as of 7/21/2025. Past performance is no guarantee of future results. Not intended as a recommendation to buy or sell any securities named herein.

- CORZ, WULF, and BTDR carry the highest EV/EH/s multiples, reflecting investor belief in AI monetization. In BTDR’s case, its emerging ASIC business is likely also a significant component of its valuation.

- IREN and RIOT valuations are modest despite their scale and AI/HPC potential, suggesting execution risk or AI skepticism.

- CLSK stands out as the cleanest pure-play benchmark with no AI premium baked in.

- Despite AI/HPC initiatives, BITF and HIVE valuations are lower than CLSK, suggesting even deeper execution risk and AI skepticism.

- CANG trades below cash/BTC, implying the market assigns negative value to their ops.

This wide dispersion in valuations reflects a sector in transition, where some miners are being rewarded for AI/HPC exposure, while others are still priced closer to pure-play Bitcoin operators.

Successful AI/HPC Pivoters

At the top of the BTC-adjusted EV/EH/s chart are Core Scientific (CORZ) and TeraWulf (WULF), both of which have executed major deals with neoclouds that validate their pivot toward AI/HPC hosting infrastructure. CORZ, in particular, signed a gold-standard agreement with CoreWeave, which has since evolved into a full acquisition. The all-stock deal values CORZ at ~$9 billion , less than the projected $10 billion in lease savings CoreWeave expects to realize from the transaction. CORZ shareholders will own less than 10% of the combined entity, receive no cash, and are subject to a fixed exchange ratio. With no premium paid for the mining business and no retained control, the market appears to value CORZ’s remaining ~500 MW of gross BTC mining infrastructure at effectively $0 . CORZ shares fell ~31% in the week following the announcement on Monday, July 7th, dragged down by CRWV, which declined 24% over the same period. This deal resembles a strategic acquisition of a critical infrastructure vendor, rather than a growth-driven acquisition that rewards CORZ shareholders with a premium.

For these reasons, CRWV may ultimately need to increase its offer before CORZ shareholders approve the merger, which is currently expected to close in Q4 2025. However, under definitive terms, the deal already has CORZ management’s approval, limiting the likelihood of a higher bid.

While the all-stock deal has dampened some expectations for miners’ opportunities in AI/HPC, it nevertheless validates their potential. As reflected in MVDAPP’s performance, miners pursuing AI/HPC pivots have rallied since the CORZ deal: at the time of writing on July 21st, RIOT, IREN, CIFR, and HUT are up 24% , 11% , 10% , and 2% , respectively, since the CORZ and CRWV deal was announced on July 7th.

Aspirational Pivoters with Potential Optionality

Clustered in the middle of the chart are Hut 8 (HUT), Cipher Mining (CIFR), Iris Energy (IREN), and Riot Platf toward AI or HPC, but remain early in the execution phase. For example, HUT’s newly energized 205 MW Vega site is designed for potential AI optionality: it uses proprietary rack-based architecture to house its Bitcoin mining ASICs, emulating the form factor used by traditional AI/HPC data centers, and can support up to 180 kW per rack , exceeding the requirements of existing NVIDIA Blackwell GPUs. Through this approach, Bitcoin mining serves as Hut 8’s “anchor tenant”, so to speak, enabling the company to finance infrastructure capable of more than doubling the company’s hashrate while preserving the site’s potential for future upgrades supporting more advanced AI/HPC use cases.

Similarly, in January, RIOT announced that it would pause its Phase II mining expansion at its 1 GW Corsicana facility to launch an AI/HPC feasibility study for the site’s remaining 600 MW of power capacity. Along with Hut 8’s site in Vega, we toured Corsicana and spoke to RIOT’s management in June, who told us that they are not only hopeful to secure a deal and break ground for an on-site AI/HPC data center within a year, but even to evaluate retrofitting the existing 400 MW of Bitcoin mining for AI use cases. While that decision is several years off, the existing ASIC “anchor tenants” will pay an estimated additional 10,000-15,000 BTC before the next halving, pointing to the value of mining power capacity and its potential repurposing. Like Corsicana’s proximity to Dallas/Fort Worth, RIOT’s other major site, Rockdale, is ~50 miles from Austin, placing it in an attractive market to meet AI inference demand and draw talent. With 700 MW , this mining site—North America’s largest by developed capacity—is another contender for an AI/HPC retrofit deal.

Like RIOT, CIFR has two large-scale Texas sites, Black Pearl and Barber Lake. Black Pearl’s 300 MW power capacity is split into two 150 MW phases: Phase I is dedicated to air-cooled Bitcoin mining, slated to add 9.6 EH/s by Q3’25, and is ahead of schedule as of early July; Phase II, meanwhile, remains in the process of evaluating its potential for HPC. Also on the HPC front, in early May, CIFR announced signing Fortress Credit Advisors as a JV financing partner for its Barber Lake site, which features 300 MW of approved ERCOT interconnection agreements, a newly constructed substation, and a signed MOU for an additional 500 MW data center. Multiple HPC tenants are under NDA as they perform due diligence on the site. In a positive outcome, CEO Tyler Page anticipates retaining 40% of the economics by contributing the site’s land, substation, and interconnect (no cash)—implying significant upside potential for the development of a $3.2 billion ( $ 10.7 million/MW ) data center.

IREN, the best-performing miner in our coverage YTD ( +60% ), has stood out both for its rapid 50 EH/s buildout and for the potential AI/HPC optionality that comes with it. Between June 2024 and June 2025, IREN's production reports show that its hashrate grew from 10 to 50 EH/s , thanks to the rapid buildout of its five-phase Childress site, now totaling 650 MW of operating Bitcoin mining data centers. The site is on target to energize its first AI-dedicated building, Horizon 1, by Q4’25, delivering up to 50MW of IT load with 200kW rack densities and setting the stage for further on-site buildouts with Horizon 2 and beyond. Whereas older mining sites were typically built without alternative use cases in mind, IREN’s newer, modular Bitcoin mining data centers are ostensibly designed to be more suited for AI/HPC-capable retrofits. And, while IREN paused its hashrate growth after hitting 50 EH/s in June, its Sweetwater 1 and 2 sites targeting energization in April 2026 and late 2027, respectively, give the company a sizable growth pipeline with the potential to develop one of the world’s largest Bitcoin mining or AI/HPC data centers. Like most other miners, however, IREN’s potential AI/HPC far capacity exceeds its ability to purchase and operate its own GPUs. To fully realize its potentially multi-GW AI/HPC capacity, it needs a customer like CoreWeave.

On a much smaller scale, IREN has developed its own AI Cloud since August 2023, reaching 1.9K NVIDIA GPUs as of its Q1 2025 update. This month, IREN more than doubled its GPU fleet, spending $130 million to add ~2.4k NVIDIA GPUs (plus fit-out costs incl. servers, storage, and ancillary equipment) to its Prince George, BC campus. At 50MW , Prince George can host over 20K Blackwell GPUs, implying ~$1.1 billion + in GPUs costs for each of its 50MW data centers.

Pure-Play Bitcoin Miners and Overlooked Outliers

Toward the lower end of the EV/EH/s spectrum lie more pure-play Bitcoin firms like Marathon (MARA), CleanSpark (CLSK), Bitfarms (BITF), Hive Digital Technologies (HIVE), and Canaan (CANG).

CLSK serves as a particularly useful benchmark for a pure-play miner without other product lines or AI exposure. While primarily a Bitcoin-only operation, too, MARA may benefit from a premium thanks to holding the largest public equity BTC treasury aside from Strategy (MSTR).

While BITF is also pursuing the HPC hosting pivot, it appears to be the most doubted. Nevertheless, the company has no plans to make large miner purchases in 2025 and 2026, focusing entirely on developing U.S. energy & HPC infrastructure. In April, the company entered a private debt facility with Macquarie Group for up to $300 million to fund the initial development of its HPC project at Panther Creek, one of the PJM (Pennsylvania-New Jersey-Maryland Interconnection) sites it acquired from HIVE in March. The company has ambitious plans: they want to save $2-4mn (20-40%!) of the ~$10mn/MW in capex it takes to build an AI/HPC data center by eliminating the need for traditional redundancy equipment (e.g., diesel generators). As CEO Ben Gagnon explains , the company plans to leverage its on-site power plants and treat its Bitcoin miners as a battery, shutting the miners down temporarily to redirect electricity to the AI/HPC data center in the rare event of a primary power failure. While this hasn’t been applied to AI/HPC data centers before, it is effectively the same concept as Bitcoin miners curtailing their power during times of peak grid demand. Such demand response programs have enabled Texas’s ERCOT grid to achieve better stability, pricing, and increased investment in renewables. In the case of BITF, the company wants to internalize those curtailment benefits to cheapen its HPC data center buildout while earning Bitcoin, replacing idle redundancy infrastructure with revenue-generating ASICs. It remains to be seen, however, whether Macquarie’s development milestones and BITF’s prospective AI/HPC customers will tolerate this approach, and that is if the engineering even proves feasible. We also note that BITF’s stock has suffered as a result of RIOT’s sales following RIOT’s attempted takeover. In September 2024, RIOT held as much as 19.9% of BITF’s outstanding common shares. In more recent months, RIOT’s share of BITF has fallen from 14.3% ownership on June 10th to 10.3% ownership on July 14th. With financing, engineering, and RIOT’s overhanging shares all presenting risk, we view BITF as an underdog.

Until the recent rally, HIVE’s operating business was trading below $0 after stripping out its relatively sizable Bitcoin holdings. Considering its rapid EH/s growth in Paraguay and growing cloud AI business, we think HIVE looks cheap. With BTBT spinning out its WhiteFiber HPC business and pivoting fully to ETH in June, HIVE (along with BTDR, discussed below) is one of the only two other miners in our coverage with a GPU Cloud service, Buzz HPC. As of HIVE’s Q1'25 presentation , the company has 4,000 NVIDIA A-Series GPUs and 848 H-Series GPUs, achieving a $20M ARR . While HIVE’s smaller scale and pipeline make it incapable of achieving the hyperscaler deals that IREN is pursuing, achieving predictable AI cashflows should help both companies unlock new financing pathways, differentiating them from other miners.

It reasons that CANG—which has no power infrastructure and thus pays a premium for its 100% hosted capacity—places last on an EV/EH/s basis, as it is singularly focused on BTC accumulation but has not formally launched a “value-additive” treasury strategy like MSTR’s.

Vertically Integrated and Idiosyncratic: Bitdeer (BTDR)

By developing its own brand of Bitcoin mining machines, the SEALMINER series, Bitdeer occupies a unique position amongst this peer group. As of this month’s production update , BTDR has manufactured 14.9 EH/s of the planned 16.0 EH/s of its second-generation miner, the SEALMINER A2, shipping 5.3 EH/s to customers and retaining 9.6 EH/s for its use. Like HUT, BTDR’s rapid hashrate growth trajectory potentially explains its high EV/EH/s, as the company expects to more than double its hashrate from 16.5 EH/s to 40.0 EH/s by the end of October 2025.

It is encouraging to see BTDR eating its own cooking with the SEALMINER A2, which yields a power efficiency of 14.9 J/TH . If the A2’s performance holds up in the field, and the next-generation SEALMINER A3 & A4 ASICs can match the 11-12 J/TH and 5.5-6.0 J/TH power efficiencies advertised on their roadmap, it could spell an enormous win for the company. Bitmain currently dominates the ASIC market with an estimated 82% share. Its most efficient next-generation model, the S23 Hyd—scheduled to ship in January 2026—is expected to deliver 9.5 J/TH in power efficiency. That’s more than 50% less efficient than the 5.5–6.0 J/TH target range advertised for Bitdeer’s SEALMINER A4. As other miners are pursuing AI/HPC, if BTDR can “sell picks and shovels” to diversify its revenues away from the fundamentally flawed business of pure-play Bitcoin mining, it could help the company finance more value-accretive opportunities in AI/HPC hosting infrastructure or even its own GPU fleet.

Still, SEALMINER's success is far from guaranteed. It must not only match or exceed Bitmain’s performance claims in the field, but also overcome the broader moat Bitmain enjoys via its financing partners, resale network, and entrenched miner loyalty. Without equivalent ecosystem trust or liquidity, even a technically superior chip may struggle to gain commercial traction, especially if deployment is delayed or yields underwhelm.

BTDR also has potential in the AI/HPC landscape. Last year, BTDR engaged TLM Group for feasibility assessments of its 2.5 GW power portfolio, which yielded “largely positive” results for the company’s two Ohio sites. This May, the company reported pausing mining-related construction at its 570 MW Clarington, Ohio site due to advancing HPC/AI discussions. Apparently, it resumed the site’s mining-related construction “with full optionality to reassess and repurpose for HPC at a later date.” Setting the mixed signals on BTDR’s AI/HPC hosting potential aside, like IREN and HIVE, the company has invested in its own cloud GPU services through Bitdeer AI, which offers AI model training and deployment. While Bitdeer has not disclosed the exact size of its GPU Cloud business, its Bitdeer AI division operates NVIDIA H100-, H200-, and upcoming GB200-powered clusters across at least seven countries, including the U.S., Canada, Singapore, and the Netherlands. The platform offers a full-stack MLOps suite comparable to other emerging GPU clouds, indicating significant infrastructure investment and a maturing product portfolio.

Where Are the Buyers? Self-Custody Slows as Exchanges Scale

Wallet Use Drops to 23% as Exchanges Dominate

Source: Sensor Tower as of 7/9/2025. Past performance is no guarantee of future results.

As the old saying goes, “Not your keys, not your crypto.” Between the infamous collapses of crypto institutions like Mt. Gox, Celsius, and FTX, self-custody hardliners have repeated this mantra, warning users about the dangers of outsourcing their crypto wallet’s security. Yet if you ask any crypto native how they store their private keys — to the extent that they’ll even tell you — it will likely sound risky, contrived, or downright precarious. Whether scribbled on paper, stashed in a password manager, or split across seed vaults, these practices reveal an uncomfortable truth: self-custody, while philosophically pure, remains operationally brittle for most users.

Whether self-custody is “better” is a personal decision hinging on factors such as one’s location, lifestyle, risk tolerance, technical knowledge, free time, and trust in institutions. However, the market tells a clearer story: users are voting with their thumbs, and they’re increasingly choosing custodial exchanges over non-custodial wallets. Monthly active users (MAUs) for exchange apps, such as Binance, Robinhood, and Coinbase have remained resilient, even as overall crypto app usage has softened. By contrast, many self-custody wallets, such as MetaMask, Trust Wallet, and Tonkeeper have experienced declines in users across nearly every time frame. In aggregate, the exchanges in our analysis gained ~4 million MAUs (3%) year-over-year, while the wallets collectively lost ~14 million MAUs (28%) over the same time frame. Put differently, wallets’ share of users has dropped from 30% to 23% over the past year, a trend indicating a broader preference for ease of use and custodial safety nets among new users, even if it means ceding control of private keys. Notably, however, this data doesn’t include the growing popularity of ETPs or crypto treasury equities, which arguably offer the benefits of accessibility and third-party custody even more effectively than exchanges.

Top 24 Crypto Apps by Monthly Active Users (millions), Growth (%)

Source: Sensor Tower as of 7/9/2025. Past performance is no guarantee of future results. Not intended as a recommendation to buy or sell any securities named herein.

However, we do not want to ascribe exchange’s recent success over wallets purely to their custodial services. Many crypto-savvy users may be on exchanges despite the custodial risks associated with them. Take, for example, Robinhood, Bitget, and Kraken, which offer trading products beyond cryptocurrency, such as equities, spot, futures, and FX trading. For active traders, the ability to unify their crypto liquidity with these other markets may be the driving factor in their decision—even if they remain self-custody purists ideologically, or with other less actively managed parts of their portfolio.

To the extent that this is the case, we caution against interpreting this trend as fundamentally bearish for self-custody. Advancements in real-world asset tokenization, such as Robinhood’s recent xTokens launch, pave the way for a world where the programmability and interoperability of on-chain DeFi ecosystems offer more features than any centralized exchange.

Links to third party websites are provided as a convenience and the inclusion of such links does not imply any endorsement, approval, investigation, verification or monitoring by us of any content or information contained within or accessible from the linked sites. By clicking on the link to a non-VanEck webpage, you acknowledge that you are entering a third-party website subject to its own terms and conditions. VanEck disclaims responsibility for content, legality of access or suitability of the third-party websites.

To receive more Digital Assets insights, sign up in our subscription center .

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。