If Web3 wallets become the new payment standard, the beneficiaries may also be those building the underlying infrastructure.

Written by: Prathik Desai

Translated by: Block unicorn

It took nearly a thousand years from the first paper money in ancient China during the Tang Dynasty to a functional check system. Then came wire transfers, which accelerated cross-border trade in the 19th century. But what truly changed the way we pay was a forgotten wallet.

In 1949, Frank McNamara forgot his wallet while dining with clients at Major's Cabin Grill in Manhattan, New York. This embarrassing moment led to an innovation that ensured such incidents would not happen again. A year later, he returned with the world’s first credit card—the Diners Club Card—which eventually evolved into a credit card network processing billions of transactions daily.

Soon after, Mastercard and Visa emerged from the chaos of bank alliances and brand reshaping, primarily out of necessity for survival.

As BankAmericard (later renamed Visa) gradually captured the market in the 1960s, other regional banks feared missing out on the credit card opportunity. To address this challenge, a group of banks formed Interbank in 1966, which was later renamed Master Charge and eventually became Mastercard, allowing them to pool resources, share infrastructure, and build a scalable competitive network.

This race to remain competitive evolved into one of the most successful collaborations in banking history. Payments became simpler, but more importantly, they became "invisible." Swiping or tapping a card was not just convenient; it laid the foundation for modern commerce.

People could now carry purchasing power with them. Merchants received faster payments. Banks gained new revenue streams. And the intermediaries—the credit card networks—became some of the most valuable businesses in the world.

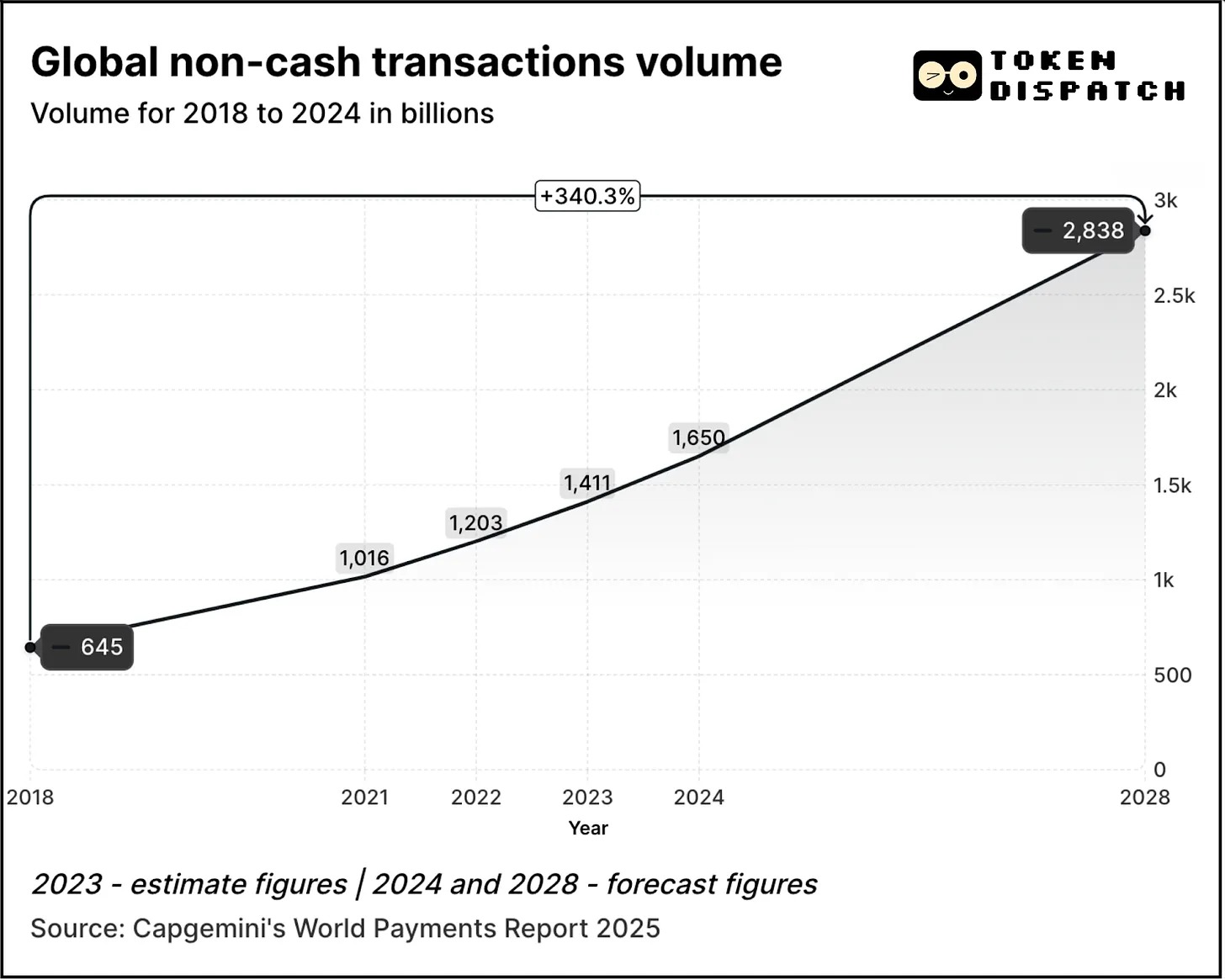

In 2024, Mastercard and Visa generated $17 billion and $16 billion in revenue, respectively, just from payment services. The volume of digital transactions continues to grow year after year.

Transaction volume grew from $645 billion in 2018 to $1.65 trillion in 2024, a 2.5-fold increase. According to Capgemini's World Payments Report 2025, transaction volume is expected to grow by 70% from 2024 levels, reaching $2.84 trillion by 2028.

In 2023, approximately 57% of global non-cash transactions were completed via debit or credit cards, which typically take 1 to 3 days to settle. Each transaction often passes through multiple institutions before the merchant finally receives the funds. Despite this, the system continues to operate smoothly. You can use the same card to make payments in Tokyo, Toronto, or Thiruvananthapuram. Payments have become invisible.

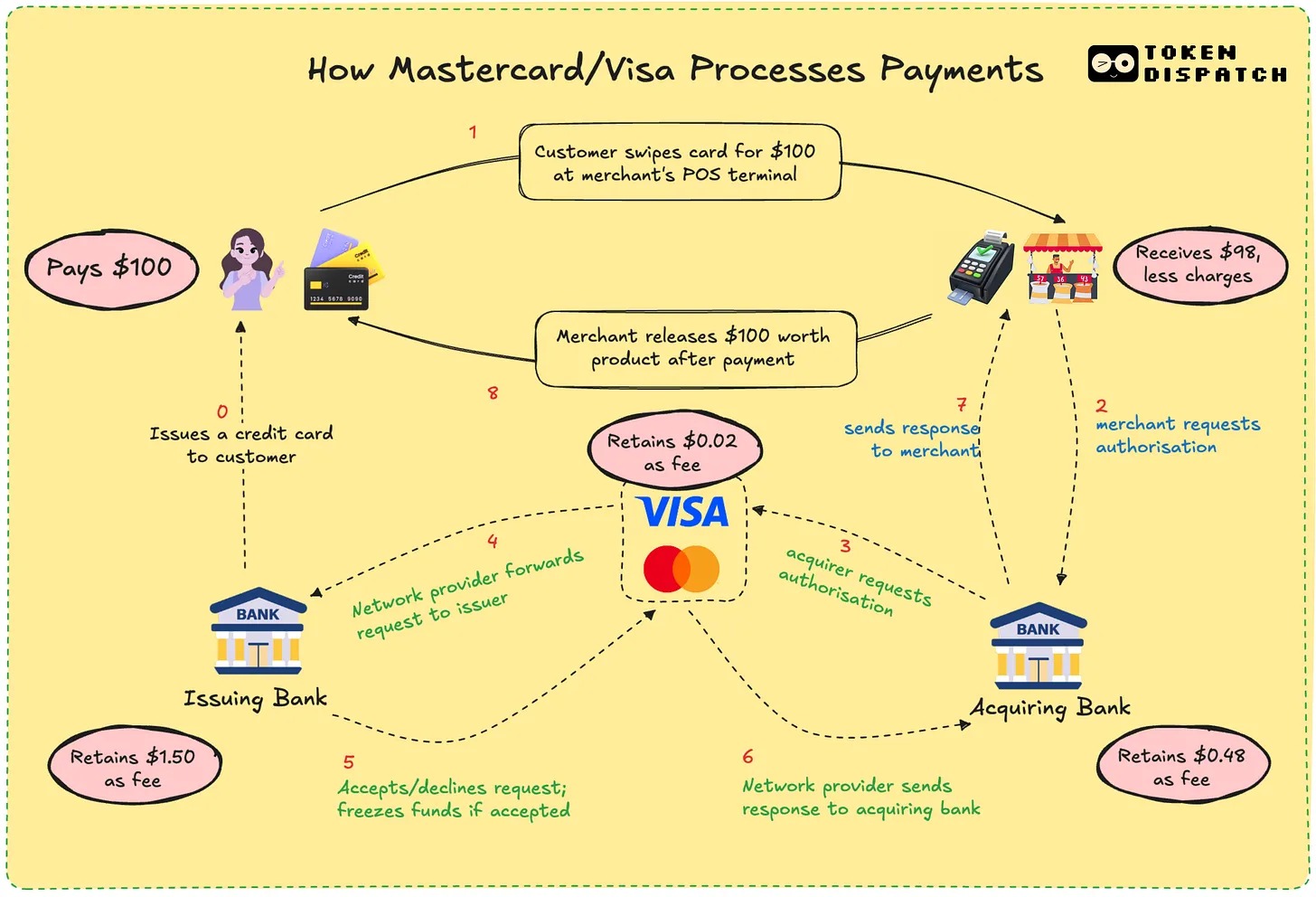

Visa and Mastercard have never actually issued cards or held your funds. What they possess is a channel built on trust between unacquainted financial institutions. When you swipe your card, their networks decide whether to allow the transaction, match the correct accounts, clear the bills, and ensure the funds are ultimately transferred.

To do this, merchants need to pay about 2-3% of the transaction value, with fees distributed among the issuing bank, acquiring bank, processing entities, and card networks. In return, everyone benefits from a fundamentally reliable system. You don’t need to know who settled the payment, as long as it gets done.

As a user, you might be completely indifferent to this process. Do you remember the last time you asked your favorite café how they received funds after you swiped your card? You paid, they smiled back, and life went on. But for merchants, those few percentage points add up, especially for small businesses with thin margins.

Have you ever felt frustrated about being charged a few extra dollars for using a card instead of cash or other digital payment methods? Now you know why.

Imagine if they could eliminate delays, receive payments instantly, and incur very low fees. This is the promise of blockchain. Visa and Mastercard are trying to emulate this model or risk being surpassed by it.

With the introduction of stablecoins, the dynamics of payment settlement have further changed. In the past 12 months, the monthly transaction volume of stablecoins has surpassed that of Visa.

With stablecoins, transactions can settle directly from one wallet to another in seconds. No banks, no processing entities, no delays—just code. On networks like Solana or Base, fees are just a few cents, and transactions are nearly instantaneous.

This is not just theoretical. Freelancers in Argentina are already accepting USDC. Remittance platforms are integrating stablecoins to bypass traditional banking systems. Crypto-native wallets allow users to pay merchants directly without a card.

Visa and Mastercard face a life-or-death threat. If the world begins transacting on-chain, their roles may disappear. Therefore, they are adapting.

Mastercard's actions over the past year have been noteworthy.

It recently partnered with Chainlink to connect over 3.5 billion cardholders directly to on-chain assets, representing over 40% of the global population. The system leverages Chainlink's secure interoperability infrastructure, combined with the power of payment processors like Uniswap and Shift4, to create a bridge for converting fiat to cryptocurrency.

Additionally, it has partnered with Fiserv to launch a stablecoin called FIUSD, which Mastercard plans to integrate into over 150 million merchant touchpoints. What is their goal? To enable merchants to seamlessly convert between stablecoins and fiat currency anytime, anywhere, just like sending an email.

Through its Multi-Token Network (MTN), Mastercard is also laying the groundwork for stablecoin-linked cards, digital asset merchant settlements, and tokenized loyalty programs. Why give up loyalty rewards associated with cards just for choosing on-chain payment options?

What’s in it for Mastercard? Quite a lot. Enabling on-chain settlements can reduce internal processing costs by minimizing intermediaries.

Mastercard's $300 million investment in Corpay's cross-border payments division in April 2025 indicates they are betting on high-volume, low-margin businesses where cost efficiency is crucial. Think about cross-border payments; this is one of the key differentiators for Mastercard compared to its competitor Visa. In 2024, Mastercard's cross-border transaction volume grew by 18% year-on-year.

They are also creating new fee structures: while traditional per-transaction fees may gradually decrease, they can now charge for API access, compliance modules, or integration with MTN.

Meanwhile, Visa is collaborating with Yellow Card in Africa to experiment with cross-border stablecoin payments—something that is urgently needed in Africa. It has partnered with Ledger to launch a card that allows users to spend cryptocurrency and earn USDC or BTC cashback. Furthermore, Visa continues to develop its Visa Tokenized Assets platform, aimed at enabling banks to issue digital fiat tools on-chain.

With stablecoin settlements, Visa no longer needs to transact through multiple banks or bear as much foreign exchange slippage. The motivation behind this is to reduce costs and improve profit margins.

The philosophies of both companies are shifting. They are programming themselves as the infrastructure layer for programmable money. They realize that the future may not be dominated by swiping cards but by smart contract calls.

Underlying all this are some deep personal factors.

I once waited three days for a refund due to a canceled reservation. I have witnessed international freelancers frustrated by wire transfer delays and costs. I have wondered why my cashback takes weeks to arrive after a transaction. For users like us, these inefficiencies, while inconvenient, have quietly become the norm. Web3 now offers an alternative.

For payment giants, the biggest hurdle will be cost. For merchants, traditional card transactions can cost 2% or more. With on-chain stablecoins, fees can drop below 0.1%. For users, this means faster cashback, real-time settlements, and lower prices. For developers and fintech companies, this means the ability to build applications that connect directly to a global payment network without traditional banking procedures.

Web3 will still have its own trade-offs. Credit card networks provide fraud protection, refunds, and dispute resolution services. Stablecoins do not. If you send funds to the wrong wallet, that money is likely gone forever. While the efficiency of on-chain fund flows is high, it still lacks the consumer protections we value. The recently passed GENIUS Act in the Senate may have addressed some consumer protection concerns.

Visa and Mastercard are not waiting for the opportunity. Instead, they see this gap as an opportunity. By layering traditional compliance, risk scoring, and security features on top of stablecoin transactions, they aim to make Web3 safe for the average user. The strategy is to let others build the protocols and then sell the hardware that will enable these protocols to be used at scale.

They are also betting on transaction volume. Not speculative trading, but real-world use cases: remittances, payroll, e-commerce. If this traffic shifts on-chain, companies that help manage this traffic will benefit, even if they are no longer the fee collectors of the past.

Visa and Mastercard want to be the drivers of building such ecosystems from the ground up. So when your chosen crypto wallet needs a trusted KYC layer, or your bank requires cross-border compliance, a branded API will be ready.

What does this mean for users? Perhaps a future where your wallet operates like a bank. You receive payments in stablecoins, spend through a Visa or Mastercard interface, earn tokenized rewards, and everything settles instantly. You might not even notice which chain it went through.

For someone like me, who has experienced everything from banking apps to UPI to buying coffee with cryptocurrency, the appeal is clear: I want payments to be simple and effective. I don’t care if it’s tokens or rupees. What I care about is that it’s fast, cheap, and error-free in transactions. If these old giants can guarantee that, perhaps they deserve to continue existing.

Ultimately, this is a race to remain indispensable. If Web3 wallets become the new payment standard, the beneficiaries may also be those building the underlying infrastructure. The card giants are betting that even with currency, the infrastructure may still belong to them.

They hope to once again fade into the background. Only this time, the pipeline will be made of code.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。