I. Definition and Classification of Stablecoins

Stablecoins, as the "stable anchor" of the cryptocurrency market, are typically pegged to fiat currencies, commodities, or algorithmic mechanisms. They can be classified into four categories based on the type of collateral and operational model:

- #### Fiat-Collateralized Stablecoins

- Definition: Such as Tether (USDT) and USD Coin (USDC), which are backed 1:1 by US dollars or other fiat currencies, with reserves typically held in banks or trust institutions.

- Mechanism: Issuers hold an equivalent amount of fiat currency (e.g., USD) as reserves, allowing users to redeem stablecoins at a 1:1 ratio at any time.

- Advantages: - High stability, low value fluctuation, suitable for payments and transactions. - Easy to understand, widely used in centralized exchanges and DeFi platforms. - Higher regulatory transparency (e.g., USDC reserves are audited regularly).

- Disadvantages: - Reliant on the issuer's credit and operational transparency (e.g., Tether has faced scrutiny over reserve controversies). - Centralized management leads to single point of failure risks. - Must comply with strict regulatory requirements, resulting in high compliance costs.

- Case: USDT has a market cap exceeding $110 billion, while USDC has a market cap of about $55 billion (2025 data).

- #### Crypto-Collateralized Stablecoins

- Definition: Such as MakerDAO's DAI, which is generated through over-collateralization of cryptocurrencies like Ethereum, typically operating via smart contracts.

- Mechanism: Users deposit cryptocurrencies (e.g., ETH) as collateral to generate stablecoins, with value maintained through algorithms and over-collateralization.

- Advantages: - Decentralized, no need to trust a single issuer, strong resistance to censorship. - Suitable for the DeFi ecosystem, high flexibility. - High transparency, all transaction records are on the blockchain.

- Disadvantages: - Price volatility of collateral assets may lead to liquidation risks. - Smart contract vulnerabilities may trigger systemic risks. - Higher complexity, users need technical knowledge.

- Case: DAI is widely used in DeFi, but the price crash of ETH in 2022 led to some liquidation events.

- #### Algorithmic Stablecoins

- Definition: Such as TerraUSD (UST, which collapsed in 2022), which dynamically adjusts supply through algorithms to maintain value stability without direct collateralization.

- Mechanism: Adjusts supply and demand through arbitrage mechanisms or token burning/minting, such as UST balancing value through the Luna token.

- Advantages: - No need for reserve assets, low operational costs. - Fully decentralized, theoretically infinitely scalable. - Suitable for the rapidly growing cryptocurrency market.

- Disadvantages: - Poor stability, easily affected by market sentiment and runs (e.g., UST's collapse led to losses of billions of dollars). - Complex algorithms, low market trust. - High regulatory difficulty, may be seen as high-risk assets.

- Case: The failure of UST highlights the vulnerability of algorithmic stablecoins, which currently hold a small market share.

- #### Hybrid Stablecoins

- Definition: Combining fiat or crypto collateralization with algorithmic mechanisms, attempting to balance stability and flexibility, still in the experimental stage.

- Mechanism: Such as partial reserve support combined with algorithmic adjustments, or dynamically adjusting collateral ratios.

- Advantages: May balance the advantages of stability and decentralization, with significant innovation potential, adaptable to various scenarios.

- Disadvantages: - Technically complex, risks not fully validated. - Low market acceptance, limited application scenarios. - High regulatory uncertainty, may face dual compliance requirements.

- Case: Frax Finance's FRAX attempts a hybrid model, but the market size is small.

Stablecoins are widely used in cross-border remittances, DeFi, payment settlements, and value storage due to their low cost, fast transactions, and low volatility, with a market size reaching $232 billion by 2025. The expansion of stablecoin scale (30% of cross-border payments completed through stablecoins in 2025) and risk events (UST collapse, Tether's opaque reserves) have forced the U.S. to regulate.

II. Main Provisions of the GENIUS Act

The GENIUS Act establishes a federal and state-level regulatory framework to regulate payment stablecoins (defined as digital assets primarily used for payments and settlements, pegged to fixed currency values). Below are its main provisions, based on publicly available information:

The bill passed the Senate Banking Committee with an 18–6 vote and the full Senate with a 66–32 vote, demonstrating bipartisan support.

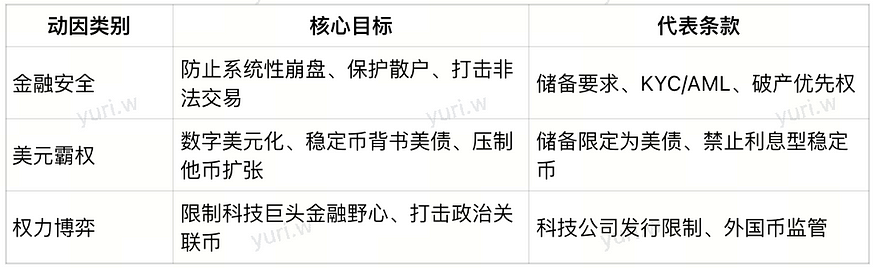

III. Legislative Motivation: From Financial Security to Digital Dollar Hegemony

Financial Security and System Stability: Regulation as the Foundation

- Consumer Protection is Urgent

- In recent years, stablecoins have frequently experienced "de-pegging" events, especially the collapse of TerraUSD (UST) in 2022, which led to the evaporation of billions of dollars in retail assets.

- The GENIUS Act requires all payment stablecoins to undergo monthly audits and hold 1:1 liquid reserve assets, granting users priority claim rights in the event of issuer bankruptcy, significantly enhancing user protection.

- Anti-Money Laundering and Financial Crime Prevention

- The widespread use of stablecoins in anonymous transactions has raised concerns among law enforcement agencies.

- Senator Elizabeth Warren pointed out that over 40% of ransomware payments are made through stablecoins.

- The bill mandates issuers to implement KYC (Know Your Customer), AML (Anti-Money Laundering), and CFT (Counter Financing of Terrorism) procedures, aiming to combat illegal fund flows.

Digital Continuation of Dollar Dominance: Elevating Financial Geostrategic Strategy

- Demand Side Binding of Digital Dollar: "Cryptocurrency" Pegged to the Dollar

- As of 2025, over 99% of global stablecoins are denominated in USD, making the dollar the core value anchor of global digital assets.

- The GENIUS Act explicitly aims to strengthen the foundational position of the dollar in the crypto financial system through regulatory means, ensuring the dollar continues to dominate the global payment and reserve system.

- Reserve Asset Structure Design: Stablecoins "Feeding" the U.S. Treasury Market

- The bill requires issuers to concentrate reserve assets in U.S. Treasury bonds, bank deposits, or physical cash.

- Republican Senator Bill Hagerty noted that by 2030, stablecoin issuers may become one of the largest holders of U.S. Treasury bonds, thereby supporting financing for the U.S. fiscal deficit.

- The current scale of U.S. Treasury bonds has reached $36 trillion, and the stablecoin reserve mechanism is seen as a "quasi-invisible purchasing power."

- Containing Foreign Currency Expansion: Countering the Digital Rise of the Renminbi and Euro

- The EU has launched the MiCA regulation, and China is also promoting the cross-border circulation of the digital yuan.

- The GENIUS Act is an important means for the U.S. to seize the global sovereignty high ground of digital currencies, aiming to prevent foreign digital currencies from threatening international settlement rights.

Technological and Political Power Balance: Interest Conflicts Behind Legislation

- Obstruction of Financialization Trends of Tech Giants

- Meta's stablecoin project Libra (later renamed Diem), proposed as early as 2019, was forced to terminate due to regulatory pressure.

- The GENIUS Act's revised provisions explicitly prohibit tech companies from issuing stablecoins without federal or state approval, and impose higher requirements on their data privacy, financial risks, and platform monopolistic behavior.

- Deutsche Bank analysis indicates that this move aims to prevent platform-based tech giants from using their "data + channel" advantages to monopolize financial infrastructure, thereby threatening the traditional banking system and dollar dominance.

- Renewed Doubts Over Trump's Interest Chain

- The legislative process of the bill has been questioned for potential "political quid pro quo."

- The stablecoin project USD1, supported by the Trump family and issued by World Liberty Financial, was launched in March 2025 and had a market cap exceeding $2 billion by May, ranking among the top seven globally.

- Critics argue that the bill may create a "compliance channel" for this project, facilitating funds to bypass the traditional banking system and flow to specific political figures.

- Democratic Senator Warren fiercely criticized, stating that this currency could become a "shadow banking tool for anonymous foreign funds to Trump."

- Foreign Stablecoins (such as Tether) Face Integration

- New provisions clearly state that foreign issuers must register in the U.S. and accept equivalent regulation, otherwise they cannot circulate in the U.S. market.

- Deutsche Bank commented that this move "closes previous regulatory loopholes," bringing offshore currencies like Tether into a unified regulatory framework, helping to weaken their "gray settlement tool" attributes.

IV. Stakeholder Impact Analysis

- Compliant Centralized Exchanges (CEX)

- Increased Compliance Requirements: Need to delist non-compliant coins, raising audit/KYC costs.

- Intense Competition for Licensed Stablecoins: Banks and tech companies may issue their own stablecoins, requiring CEX to strengthen user retention.

- Reduction in Types of Stablecoins: Simplifies operations but reduces asset diversity.

- Capital Flows May Become More Compliant/Transparent, benefiting the attraction of institutional investors.

- Ordinary Users

For ordinary users, the impact of the GENIUS Act mainly manifests in the following aspects:

- Enhanced Consumer Protection: The bill requires stablecoin issuers to hold 1:1 reserve assets and ensures that holders have priority claim rights in the event of bankruptcy. This reduces the risk of stablecoins de-pegging or issuers going bankrupt; for example, if an issuer goes bankrupt, users holding stablecoins will be repaid before other creditors. This enhances user trust in stablecoins, especially in light of past events like the collapse of TerraUSD (UST), which resulted in significant user losses.

- Expanded Use Cases for Stablecoins: The establishment of a regulatory framework may encourage more traditional financial institutions and businesses to accept stablecoins as payment tools, broadening their application scenarios. For instance, users may utilize stablecoins on e-commerce platforms, for cross-border payments, or in DeFi applications, increasing their convenience. Research indicates that stablecoins, due to their low cost and fast transaction characteristics, have been widely used for cross-border remittances, and the GENIUS Act may further promote this trend.

- Potential Limitations and Uncertainties: While the bill aims to protect consumers, strict regulations may also limit the use of certain stablecoins. For example, if some stablecoins fail to comply with the new regulations, compliant CEXs may stop supporting these coins, reducing user choices. Additionally, users may need to adapt to new KYC/AML requirements, such as providing more identification information before transactions, which could increase the barriers to use.

- Stablecoin Issuers

- Large Issuers (e.g., Circle, Tether): They may benefit from the legitimacy and market recognition brought by the bill but will also incur higher compliance costs. For example, Circle may attract more institutional users due to enhanced compliance of USDC, but will need to regularly disclose reserves and undergo audits.

- Small Issuers: They may exit the market due to high capital and liquidity requirements, leading to market concentration. For instance, issuers with a market cap of less than $10 billion can be regulated by states but still need to meet certain standards, which may pose challenges for small startups.

- Regulatory Agencies

The GENIUS Act provides regulatory agencies with clear authority, allowing them to more effectively oversee the stablecoin market and reduce systemic risks and illegal activities. For example, the Federal Reserve and the Commodity Futures Trading Commission (CFTC) may gain greater regulatory power.

- Traditional Financial Institutions

Banks and financial companies may see opportunities to enter the stablecoin market. For instance, institutions like JPMorgan or Visa may issue their own stablecoins to expand their business scope. Critics warn that the bill may allow large tech companies like Amazon, Walmart, or Meta to enter the banking sector without sufficient restrictions.

V. Criticism and Controversy

Despite the support for the GENIUS Act, controversies persist:

- Federal Bailout Risks: Adam Levitin points out that the bill may mislead the public into believing stablecoins are safe, but without amending bankruptcy laws, users may suffer during bankruptcies or require federal bailouts.

- Conflicts of Interest: Trump's crypto business (e.g., World Liberty Financial) may benefit, raising concerns about conflicts of interest.

- Insufficient AML/KYC Measures: Senator Warren criticizes the bill for not adequately addressing money laundering issues, as Tether and others may exploit loopholes.

- Innovation Suppression: High compliance costs may push out small issuers, hindering innovation.

- Regulatory Loopholes: Decentralized finance provisions may allow non-compliant stablecoins to enter the market.

These criticisms reflect the tension between consumer protection and market freedom within the bill.

VI. Conclusion and Outlook

The passage of the GENIUS Act marks an important milestone in the regulation of stablecoins in the U.S. By establishing reserve requirements, consumer protections, and AML compliance measures, it provides a clear framework for the payment stablecoin market. This not only solidifies dollar hegemony but also lays the groundwork for the global promotion and application of stablecoins.

However, the bill still needs to balance consumer protection with innovative development, preventing excessive suppression of small issuers and decentralized ecosystems while mitigating systemic risks. In the future, its implementation effectiveness will depend on regulatory details, industry adaptability, and international regulatory coordination.

As a crucial tool in digital finance, the development prospects of stablecoins will be profoundly influenced by the GENIUS Act, warranting continued attention.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。