But you can't wear new shoes and walk the old path.

Written by: Meng Yan

Introduction: With the U.S. Senate passing the stablecoin bill and the Hong Kong Legislative Council approving the Hong Kong dollar stablecoin regulation draft, stablecoins have quickly become the hottest topic in the industry, attracting broader attention. There is a general expectation that with the implementation of the U.S. stablecoin bill, the blockchain digital economy will experience a spectacular explosion, creating a new window of opportunity for entrepreneurship around stablecoins and real-world assets (RWA). Dr. Xiao Feng is a leading figure in Chinese blockchain research and practice, with a deep understanding of blockchain, stablecoins, and RWA. To fully grasp the opportunities of this era, I had the privilege of engaging in an in-depth discussion with Dr. Xiao Feng through video conferencing and text, which I have organized into this article for publication and discussion with peers. Due to the length of the original text, it is published in two parts. The first part has been published, mainly interpreting the significance of the U.S. stablecoin. This article is the second part, focusing on the opportunities that the stablecoin economy and RWA bring to Chinese entrepreneurs. The views expressed in this article are solely those of the author, and readers are welcome to engage in discussion.

4. The Stablecoin Economy is the Initial Stage of RWA, Driving Blockchain Applications Across the Chasm

Meng Yan: Regardless, with the legislation of U.S. stablecoins and Hong Kong stablecoins, this significant event is on the way. What does this mean for entrepreneurs?

Xiao Feng: In the coming years, stablecoins will drive a massive explosion in blockchain and RWA applications. On the demand side, hundreds of millions of users will open crypto accounts and hold stablecoins, with user numbers increasing several times in a short period. At the same time, on the supply side, millions of platforms, businesses, internet merchants, self-media, and creators will begin to accept stablecoin payments, and a large number of assets will be tokenized and become RWA. "How to earn stablecoins" will become one of the most concerning topics for all businesses in the coming years.

Various application demands surrounding stablecoins and RWA will rapidly explode, and truly capable entrepreneurs will put aside hesitation and rush in. Stablecoins and blockchain will become the most attractive track in the coming years, nurturing the most success stories.

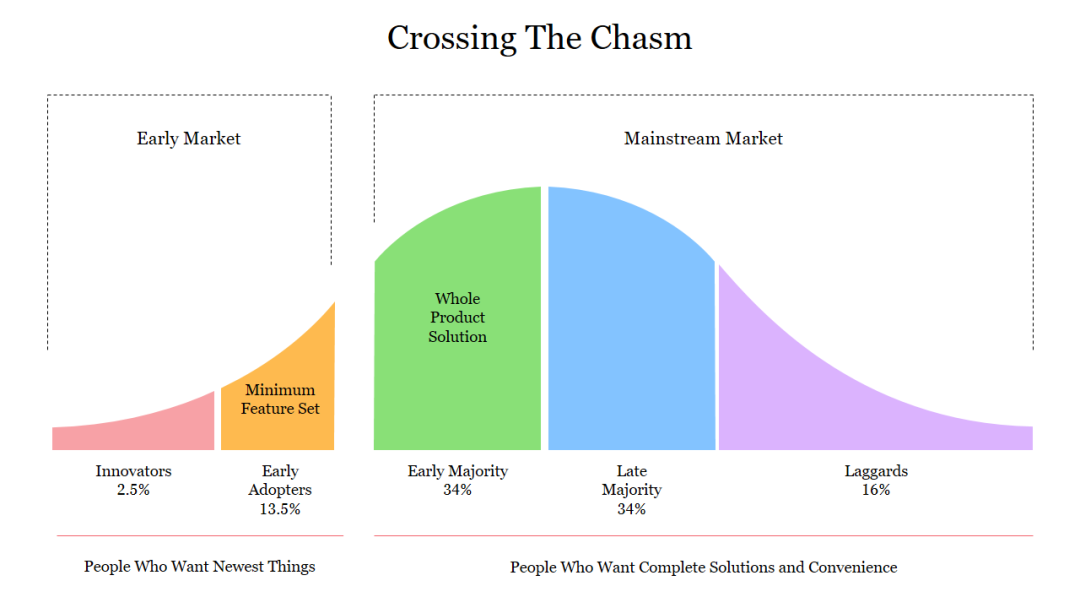

Here, I would like to quote a model from a classic business book to explain this phenomenon: Geoffrey Moore's "Technology Adoption Life Cycle" in "Crossing the Chasm." He divides users into five categories: Innovators, Early Adopters, Early Majority, Late Majority, and Laggards. Most high-tech products die in the "chasm" between Early Adopters and Early Majority. Technology must transition from vision to reality, solving specific problems and delivering real value to cross the chasm; otherwise, it will fall silent.

I believe stablecoins are becoming the bridge for the blockchain industry to cross this "chasm." In the past, when we talked about crypto and Web3, we always stayed within the small circle of "believers" and "tech enthusiasts." Many people agree with the concept, but when it comes to large-scale use, issues like "lack of landing scenarios," "users not understanding," and "high compliance risks" arise. Stablecoins will become the first blockchain product to be widely adopted by "pragmatists." Cross-border e-commerce, freelancers, platform settlements, global payments—everyone is starting to use them. It allows blockchain to integrate into the real economic system for the first time, not just as a narrative.

For users to use stablecoins, they need to open digital currency accounts and will come into contact with and learn about wallets. Therefore, stablecoins are not just a product; they are the passport for the entire blockchain industry to cross the market chasm. Once this chasm is crossed, there is a vast blue ocean market, the mainstream user market composed of the Early Majority and Late Majority. Once crossed, "mass adoption" is no longer a dream but a natural outcome.

I have recently quoted Nobel laureate John Hicks in many occasions: "Behind every industrial revolution, there is a financial revolution." Now we stand at the next part of this statement—every financial revolution requires a universally applicable product to bridge user boundaries. Stablecoins are becoming such a product.

I want to emphasize that such an explosion will only happen once in an industry; what has passed is past. Therefore, entrepreneurs should not hesitate any longer. Those who have experienced the internet and mobile internet know that missing this window will significantly increase the difficulty of future endeavors.

5. RWA Innovation Cannot Wear New Shoes and Walk the Old Path

Meng Yan: You just mentioned RWA, which is another very hot topic following stablecoins. It is said that many entrepreneurs in first-tier cities in China are exchanging ideas on how to seize RWA opportunities. However, I have some doubts about this. RWA refers to the tokenization of real-world assets on the blockchain. Many people fantasize about putting their unsellable assets on the chain to become RWA, thinking they will immediately become hot commodities. I believe this is illogical. You must have encountered this more often and have deeper insights. What do you think?

Xiao Feng: I meet with entrepreneurs discussing RWA almost every day, and I have encountered the asset types you mentioned. However, in 90% of the cases, I advise them to give up. Tokenizing these assets on the blockchain to become RWA is technically simple, but the question is, would you buy such RWA? I certainly would not.

RWA is an inevitable trend and will grow significantly in the future. Recently, Boston Consulting Group released a report predicting that by 2033, the total scale of on-chain RWA assets will reach $18.9 trillion, meaning that over the next eight years, the annual growth rate of RWA will reach 53%. No entrepreneur wants to miss the opportunity to board this rocket.

However, this does not mean that you can simply slap an RWA label on something and expect it to soar. From the development of the crypto industry over the past decade, we have learned that development must follow objective laws and be based on value. Objectively speaking, bubbles are inevitable, but if the bubble is too large, it will always burst, dragging down the industry's development.

I have told many people this: there is a serious cognitive mismatch regarding RWA. RWA is not just about slapping a label on the blockchain or applying a layer of technological "gold leaf" to transform an asset. It cannot change the essential properties of the asset. If the assets you hold lack liquidity, have opaque pricing, and high transaction costs, then going on-chain will not elevate them. RWA is not a magician; it cannot turn a crow into a phoenix.

RWA is a digital mapping of real assets, and the key lies in what you are mapping. If the underlying assets are poor, lack clear ownership, and are not standardized, no amount of packaging will help. It is not financial alchemy, nor is it a panacea on the blockchain.

Therefore, I believe the development of RWA must also follow an objective law. What is this law? It is to start with high-grade assets, standardized assets, and leading assets, gradually expanding to long-tail assets and non-standardized assets. What are high-grade assets? They are sovereign bonds, large enterprise blue-chip stocks—assets that are highly standardized, widely accepted in global markets, and have transparent pricing mechanisms. Next are leading corporate bonds, quality notes, accounts receivable, and even real estate mortgages in high-growth areas. These types of assets truly possess the potential to be tokenized because their value foundation is solid, and both buyers and sellers have a symmetrical understanding of the price. Only then can liquidity be amplified on-chain, rather than creating illusions.

You are right; many people come to RWA with a speculative mindset, looking for a shell on the chain to "monetize" worthless offline items, or even engaging in some quasi-pyramid schemes. I do not have high hopes for this route of wearing new shoes and walking the old path. RWA is not a tool to evade regulation, nor is it a dumpster for bad assets. If you have not truly solved the issues of trust, circulation, and pricing, then it is meaningless whether you go on-chain or not.

We must be pragmatic. Objectively speaking, high-quality assets are mainly concentrated in the United States. The real opportunity for Chinese people is not to rush to tokenize any asset but to first establish a foothold in the "stablecoin economy" phase. What does this mean? It means going overseas first, selling products and providing services online and on-chain, earning stablecoins—that is our current advantage. In short, for RWA, start by earning stablecoins.

Why? Because we have the world's strongest supply chain, engineering manufacturing capabilities, and internet operation capabilities. Cross-border e-commerce has already reached scale, and e-commerce owners are adept at traffic and efficiency. Once they use stablecoins, transaction costs will immediately decrease, and settlement speed will significantly increase. This is the true starting point for integrating with blockchain and represents the Chinese solution for the stablecoin economy phase.

This is not my imagination; it is the reality that is happening. In recent years, some small and medium-sized e-commerce companies and foreign trade enterprises that have gone overseas, such as exporters in Yiwu, are now rapidly accepting stablecoins. Some have achieved considerable scale, and their ability to earn stablecoins is much stronger than that of many blockchain projects. This is just the beginning. I am confident that once the GENIUS Act is passed, platforms like Amazon will immediately support stablecoin payments, and tens of thousands of e-commerce merchants will quickly become the main players in the stablecoin economy.

Therefore, I believe the time has truly come for Chinese internet elites to embrace blockchain and the stablecoin economy. As long as you establish a foothold, gather users, merchants, and cash flow, a batch of high-quality RWA will naturally emerge. For example, accounts receivable from cross-border orders and supply chain debts based on real logistics are all natural on-chain assets. By that time, you won’t need to tell stories; investors will naturally come to buy and sell your RWA.

So I suggest that the first step should be solid. The stablecoin economy is the initial stage of RWA and serves as the bridgehead for blockchain to truly enter industries and cash flows. Whoever establishes a foothold in this stage will naturally own the high ground of RWA in the next stage.

Meng Yan: Some people also think that with the RWA concept gaining popularity, they can issue tokens again. They set up an RWA project and then launch an ICO. Is this possible?

Xiao Feng: This question should be viewed from two aspects.

On one hand, telling a story about a blockchain, creating a protocol, and issuing a token to become rich is a phase that has passed; the wind has shifted. Over the past decade, we have experienced the first growth curve of the blockchain industry, which was dominated by infrastructure development and token financing. During that phase, it was indeed "narrative-driven capital"; issuing a token could pull in an entire round of financing.

But looking at it today, the marginal effect of token financing is rapidly declining. Investors in the crypto space are becoming increasingly rational, and the market is becoming more competitive. Users have seen their fair share of extravagant white papers; the key is whether there are real application scenarios and whether they can acquire users and cash flow. Therefore, I say the energy of the first curve is waning, and what we need is the second growth curve—an explosive phase centered on applications.

On the other hand, the U.S. has not taken a one-size-fits-all approach to token financing; rather, it is establishing a new legal framework for token financing through two paths. The first is the FIT21 Act, and the second is the regulatory exemption mechanism known as "Token Safe Harbor." Together, these form the embryonic shape of a new compliance financing system for tokens.

If you have a slight understanding of the history of U.S. securities law, you will know that the status of FIT21 is similar to the Investment Company Act of 1933. It is structural legislation for an economic entity, alongside the Securities Act of 1933 and the Securities Exchange Act of 1934, laying the legal foundation for a century of prosperity in U.S. capital markets. Now we see the SEC and CFTC continuously issuing explanatory documents to define whether tokens are securities, commodities, or virtual goods, while also delineating regulatory responsibilities. This is the gradual process of clarifying the entire framework.

I judge that if these two efforts can continue and combine, today's U.S. legislation may set a precedent for global token financing and token market regulation. If development goes smoothly, this could lay the foundation for a new century of prosperity in digital finance. In the past, we talked about stocks and bonds; now we talk about RWA and tokens. The forms are changing, but the underlying logic of finance remains the same—risk pricing, information transparency, and legal protection.

I still say: do not rush to issue tokens; first, do well in the stablecoin economy phase, develop applications, and solidify the foundation. Once your model is validated by the market and cash flow is established, you can issue tokens for financing according to the new U.S. rules. Why worry about not being able to finance efficiently? Why worry about not being able to go public? First, create good products and applications; the path of legal governance is being opened up, and the bridge of capital will naturally come to connect with you.

In the future, tokens can be traded on Nasdaq and NYSE, and conversely, exchanges like HashKey can also trade stocks. Recently, the U.S. crypto exchange Kraken has taken the lead in announcing support for trading some U.S. stock tokens. As SEC Chairman Gary Gensler recently stated, in the future, there will be some "super applications" that allow trading of all types of assets—stocks, bonds, tokens, stablecoins, and RWA—on a single platform. That day is not far off.

6. Chinese People Must Be the Main Characters in RWA Innovation

Meng Yan: However, in my conversations with many Chinese blockchain entrepreneurs, I feel that their overall confidence is lacking. The main concern is that the center of this wave of stablecoins and RWA is in the U.S., and due to the current overall strategic competition between China and the U.S., the rhetoric of "decoupling and breaking chains" is rampant, with rising nationalist sentiments on both sides. Will Chinese entrepreneurs be treated differently? Will they have a fair chance to compete?

Xiao Feng: If I say this problem does not exist, it would certainly be unobjective. The geopolitical game between China and the U.S. will indeed impact the entrepreneurial environment, especially in highly sensitive areas like technology and finance. However, history is never a linear progression, and reality is often more complex and tense than public opinion suggests. Despite the friction, I am still very confident in saying that Chinese entrepreneurs have not only opportunities but also unique advantages in this wave of stablecoin economy and RWA.

The first reason is the enormous existing advantage. Even during the most difficult phases in recent years, China has remained one of the regions with the most blockchain developers, the highest quality of innovation and engineering, and the most active community. We must not be deceived by surface phenomena; behind many leading global projects, there are actually codes, algorithms, and infrastructures developed by Chinese engineers. In an interview, I bluntly advised the Ethereum Foundation: "Ethereum has fallen to this point because you lost China." From 2014 to 2016, China was the most solid base for Ethereum developers and users. Later, for various reasons, Ethereum became absent from China, which was a significant reason for its loss of momentum. This applies to any global blockchain project; whoever masters the Chinese language will dominate the world. No one can ignore Chinese developers and communities.

The second reason is the high degree of alignment in real interests. The stablecoin economy and RWA represent a brand new global channel in the digital economy era. What does it mean for China? It means we can bypass the traditional U.S. dollar settlement system and centralized platforms to export Chinese goods, services, and content in new ways. This can not only create jobs, stimulate growth, and ignite innovation but, more importantly, establish China's own competitiveness in the Web3 world. In other words, this is a new "digital going out."

The third reason is that the new system itself is diverse. The future stablecoin economy will not be a single structure but a multi-layered, multi-regional global network with spectrum and granularity. We will see both onshore and offshore U.S. dollar stablecoin economies, similar to today's Eurodollar system, with vast space in Asia, Africa, and Latin America. These regions have great innovation potential and more flexible rules. With the enterprising spirit and sharpness of Chinese entrepreneurs going overseas, these markets will become our home ground.

The fourth reason is that the trend is irreversible. Once the U.S. breaks the deadlock, other major economies will inevitably follow suit. Look at Hong Kong, which has already taken the lead by passing the Stablecoin Ordinance. I believe we will eventually start discussing whether to develop an offshore RMB stablecoin. I think this is a very serious strategic issue worth discussing. If we can promote it, then in these non-U.S. dollar stablecoin ecosystems, Chinese entrepreneurs will have greater dominance and voice.

The fifth reason is my consistent long-term judgment—that China will eventually embrace the tide of blockchain and digital assets. We are a country known for pragmatism; as long as this can promote development, serve the real economy, and create benefits, it will ultimately be accepted. Once opened up, with China's market size and entrepreneurial density, combined with the hardworking and pragmatic nature of the Chinese people, blockchain will surely experience explosive growth in China, becoming the most prosperous land of innovation globally.

Therefore, for Chinese entrepreneurs, do not let a single leaf block your view and miss the entire era due to local obstacles. The stablecoin and RWA you see today are a once-in-a-decade wave. If you do not stand up, you are actively giving up your voice. If you dare to step up, no matter how big the waves or how strong the winds, there is an opportunity to secure a place in this new world. I believe Chinese entrepreneurs will succeed; five years from now, eight years from now, the stablecoin economy could reach a scale of two to three trillion dollars. I believe that by then, a significant proportion of the entrepreneurs at the pinnacle of the industry will be Chinese faces.

7. The Most Important Innovation is the Innovation of Order

Meng Yan: There is now little doubt about the ability of Chinese entrepreneurs to create quality products; market concerns are focused on integrity. As a blockchain entrepreneur myself, I am very dissatisfied with the order that has formed in the industry. When I decided to join this industry, I was inspired by the spirit of Satoshi Nakamoto, believing that we could use blockchain as an open and transparent infrastructure to construct a more inclusive and equitable large-scale collaboration mechanism outside of commercial companies. However, looking back over the past decade, the order established in this industry could be described as "sowing dragon seeds and reaping fleas," which may not be an exaggeration. Our original ideal was to oppose excessive centralized regulation, but now the order of the crypto market is even worse than the order we originally sought to replace, filled with fraud, dishonesty, bullying, opaque operations, and bottomless mutual harm. To be honest, if ten years ago, the U.S. proposed to legislate and regulate stablecoins and crypto projects, I would probably have jumped out to oppose it. But now I feel that since this industry cannot spontaneously generate a healthy order, it can only be input from the outside.

Xiao Feng: Order is also a product, and it is the most important product.

You just said "sowing dragon seeds and reaping fleas," and I do not refute that. Over the past decade, everyone has indeed experienced the gap between ideals and reality. Starting from technological idealism, we hoped that blockchain could spontaneously form an open, transparent, and fair economic order without relying on traditional regulatory structures. But reality has proven that a market without basic rules is difficult to operate stably. This is similar to the U.S. stock market in the 19th century. Human nature has not changed, and the results will not differ.

But the problem is not solely our own fault. Over the past decade, financial regulatory authorities in major jurisdictions have mostly taken a "one-size-fits-all" approach to block the rapid development of blockchain, failing to provide a clear compliance path. This has actually led to adverse selection in the market, where many entrepreneurs who were willing to innovate honestly and had the ability to do good projects could not see the rules or hope and thus exited. What remains are many more radical and speculative individuals.

Now, the FIT21 Act and the Token Safe Harbor proposal put forward by the U.S. are positive signals that we have been waiting for a long time. They do not aim to completely ban tokens but to "set rules and leave a way out" for them. For example, with the Token Safe Harbor, project parties can use tokens for financing after registering with the SEC, and three years later, regulatory agencies will assess the project's degree of decentralization: if it meets the standards, it can continue to operate without being treated as a security; if it does not meet the standards, it will be subject to securities regulation according to the law. This represents a dynamic balance between regulation and innovation. It acknowledges the high efficiency of token financing while establishing regulatory bottom lines and exit mechanisms. In my view, this is a process of establishing order. It is not about cutting off tokens with a blunt knife but about incorporating them into a sustainable development track through institutional means.

More importantly, the establishment of this order is meaningful not only for the crypto industry. In the future, entrepreneurs in emerging industries such as AI, robotics, biomedicine, new energy, and carbon assets may also finance and govern through tokens. This is not just a matter for Web3; it is a new infrastructure issue for the entire innovation ecosystem.

So I am optimistic. The right people are willing to come in and work according to the rules; as long as there is a clear order, they will ultimately succeed. The market is not afraid of regulation; it is afraid of a lack of rules. As long as order can be established, innovation will naturally follow.

Meng Yan: What advice do you have for Chinese entrepreneurs who have the courage to participate in this wave of stablecoins and RWA?

Xiao Feng: This question has been asked of me quite a bit recently. I want to say that the entrepreneurs who stand up today indeed need more courage than in previous years. But precisely because the threshold has been raised, it also indicates that this industry is beginning to enter a real construction phase. My suggestions are quite simple, summarized in five points for everyone's reference.

First is to go overseas. This wave is global; you must go out and enter the eye of the storm of the times. Go to the U.S., to Hong Kong, to Singapore, to Dubai—these places are becoming the forefront of global stablecoin and RWA innovation. If you want to participate, you cannot be overly cautious; you must fight in the storm and seize positions where the rules are being formulated.

Second is to align your heart. The game rules of the industry have changed; the path of getting rich by simply issuing a token is no longer viable. Now is an era that competes on real user value and application capability. For every product you create and every model you design, you must ask: does it truly solve user problems? Does it create new efficiencies? Only projects that genuinely create value for users will be retained by this era.

Third is to learn. Not only should you learn technology and compliance, but you should also learn new ideas and new institutional frameworks. You cannot use Web2 thinking to do Web3 things, nor can you use the mindset of issuing tokens to exploit others in the era of stablecoins and RWA. Behind this is a whole new paradigm; continuous learning and breaking through oneself are essential.

Fourth is to unite. In this new phase, Chinese entrepreneurs must band together, not only for self-protection but also for resource integration, mutual learning, and even mutual supervision. This is also the beginning of building a new order in the industry. We have previously suffered from the "chaos of the crypto space," and those lessons must not be repeated. Now is the starting point for rebuilding order, and it requires everyone to work together to shape a healthy ecosystem.

Finally, openness. The essence of blockchain is an open, transparent, and fair collaborative network; this is the soul of blockchain. We must participate in the stablecoin economy and RWA with the spirit of blockchain to drive blockchain innovation.

That's it; these are not grand principles, but I hope they can provide some inspiration to entrepreneurs who are still contemplating whether to dive into this industry.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。