Author: Tuo Luo Finance

Whether we admit it or not, in terms of application, the current crypto world does not differ fundamentally from the crypto world of five or even ten years ago. Of course, the scale has been continuously increasing, with DeFi being one of the biggest highlights, but ultimately, the crypto market has only seen currency-related applications break out of the niche, with stablecoins being the primary example aside from Bitcoin.

Both have broken out of the niche, but their paths are quite different. Bitcoin has captivated people with its price surges, creating a jaw-dropping growth curve of hundreds of times, successfully earning recognition as a major representative of decentralized currency. However, when measured by practicality rather than value, stablecoins are the true examples of large-scale adoption of crypto on a global scale.

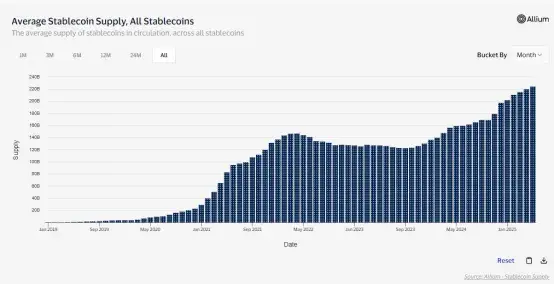

As of now, the global market capitalization of stablecoins has reached $243.8 billion. According to panel data provided by Visa, in the past 12 months, the total transaction volume of stablecoins has reached $33.4 trillion, with a staggering 5.8 billion total transactions, and the number of unique active addresses has also reached 250 million.

With high frequency and large scale, it is evident that the demand and application logic for stablecoins have essentially matured. However, from a regulatory perspective, stablecoins are still in a phase of adjustment. In recent years, global regulations surrounding stablecoins have been continuously improving. Just today, the U.S. Senate voted to pass the "Guiding and Promoting U.S. Stablecoin National Innovation Act" (also known as the GENIUS Act), clearing another obstacle for global stablecoin regulation.

01. Rapid Development of Stablecoins, Prominent Head Effect

Stablecoins, as the name suggests, are a type of crypto asset that provides value stability by being pegged to underlying assets such as fiat currencies, precious metals, commodities, or asset combinations. Their main goal is to eliminate the volatility characteristic of many cryptocurrencies, providing users with reliable settlement, value storage, and investment tools. As a measure of value in the crypto market, every expansion of stablecoins reflects the growth of the industry. In 2017, the total circulation of stablecoins globally was less than $1 billion, but now it has approached $250 billion, while the global crypto market has grown from less than $1 trillion to $3 trillion, moving from a small niche market into mainstream visibility.

From recent data, this bull market can be seen as a bull market for stablecoins. After the FTX incident, the global supply of stablecoins dropped from $190 billion to $120 billion, but subsequently, the supply of stablecoins has steadily increased over 18 months, corresponding with Bitcoin's rise from a low of $17,500 to over $100,000. The reason for this is that the liquidity in this bull market comes from external institutions, which typically prefer stablecoins as a medium when they enter the market, thus showing a characteristic of increased external liquidity and growing stablecoin scale.

As of now, the types of stablecoins are diverse and complex. They can be categorized into centralized and decentralized stablecoins based on control centers, into dollar stablecoins and non-dollar stablecoins based on fiat currency types, and even into interest-bearing and non-interest-bearing stablecoins. They can also be subdivided based on collateral into U.S. Treasury, U.S. dollar, or digital asset-backed stablecoins, covering a wide range. Unlike other use cases, although the market has begun to see interest-bearing or rebate stablecoins, due to the stable value, stablecoins essentially serve as core pricing tools, not for speculation, and generally have no official institutional restrictions, making them a foundation for stablecoins to leap into global currency status.

In terms of coverage, aside from mainstream regions like Europe, the U.S., Japan, and South Korea, emerging markets such as Brazil, India, Indonesia, Nigeria, and Turkey, especially those with weak financial infrastructure and deep inflation, have begun to use stablecoins for daily transactions. According to a report released by Visa last year, the most popular use of stablecoins outside of crypto is as a currency substitute (69%), followed by payment for goods and services (39%) and cross-border payments (39%).

It is evident that stablecoins have begun to shed the label of crypto investment, becoming an important entry point for the integration of the crypto market and the global economy. Against this backdrop, the development landscape of global stablecoins has also attracted attention. In terms of market share, dollar stablecoins account for 99% of the stablecoin market, leading to stablecoins being humorously referred to as "dollar branches."

In detail, due to the scale effect inherent in currencies, the strong get stronger, and the head effect is a key characteristic in the stablecoin field. Centralized stablecoins dominate the market, with USDT being the absolute leader, holding a market share of $152 billion, accounting for 62.29% of the total market. The second is USDC, with a market size of about $60.3 billion, accounting for 24.71%. Together, these two account for over 80% of the total market, indicating a high degree of concentration. The third is USDe, which has emerged with a unique mechanism and high yield, and is considered a semi-centralized stablecoin, currently with a market size of $4.9 billion. Since the Terra incident, algorithmic stablecoins have declined, with only the decentralized stablecoin in the Sky ecosystem still ranking high, USDS at about $3.5 billion, while DAI has shrunk to only $4.5 billion due to diversion effects. In terms of public chains, Ethereum holds an absolute dominant position, with a market share of 50%, followed by Tron (31.36%), Solana (4.85%), and BSC (4.15%).

From a business perspective, the issuance of stablecoins is a harmless transaction. Large-scale issuance allows issuing institutions to bring marginal costs close to zero, and the direct exchange of digital currencies for cash allows issuers to earn substantial risk-free profits. Taking Tether, the issuer of USDT, as an example, according to its revenue report for 2024, it achieved a net profit of $13.7 billion in one year, with the group's net assets soaring to $20 billion, while the company has only 165 employees, showcasing an astonishing employee productivity. Such high returns attract various institutions to enter the market. In recent years, traditional financial institutions like Visa and PayPal have been actively laying out this sector, and internet companies are also eager to participate. In addition to overseas Meta, domestic JD.com also hopes to share a piece of the pie in Hong Kong. Currently, the Trump family project WLFI is also launching the stablecoin USD1, which had a soft launch on April 12 and has quickly expanded, integrating over 10 protocols or applications.

02. Accelerated Regulatory Adjustment, U.S. Senate Passes the GENIUS Act

As institutions rush in, regulation has also arrived as expected. As of now, globally, including the U.S., EU, Singapore, Dubai, and Hong Kong, legislation around the stablecoin framework has begun or has already been improved. The U.S., as a crypto hub, is undoubtedly the most watched region globally.

From the perspective of U.S. regulation, stablecoins have undergone a complete process from high uncertainty to certainty. Before 2025, the U.S. Congress had not issued specific regulations regarding stablecoins and cryptocurrencies. In existing regulations, the SEC, CFTC, and OCC have defined stablecoins to gain dominance in this emerging sector. The Financial Crimes Enforcement Network (FinCEN) is responsible for regulating entities engaged in the issuance and trading of cryptocurrencies through a licensing system, while the SEC relies on securities laws to classify some stablecoins (such as BUSD and USDC) as securities. The CFTC focuses on anti-fraud and anti-market manipulation aspects of stablecoins. The complex regulatory nesting has made it difficult to define the subjects involved, and under the U.S. administrative system, the state-level regulatory environment for stablecoins has shown a trend of diversification, with state laws requiring currency trader licenses. For example, New York has an independent cryptocurrency license.

It is evident that before 2025, the regulation of stablecoins was quite fragmented, even leading to regulatory chaos due to the struggle among regulatory agencies, bringing high uncertainty and compliance challenges to the stablecoin industry. However, as time has progressed, with Trump taking office, the regulation of stablecoins has been accelerated.

As early as February this year, Bryan Steil, chairman of the House Digital Assets Subcommittee, and French Hill, chairman of the Financial Services Committee, submitted the "2025 Stablecoin Transparency and Accountability Promotion Ledger Economy Act" (abbreviated as "STABLE") draft. In the same month, Senators Bill Hagerty, Tim Scott, Kirsten Gillibrand, and Cynthia Lummis jointly proposed the "Guiding and Establishing U.S. Stablecoin National Innovation Act" in the Senate.

The simultaneous introduction of these two major bills is not coincidental but rather a proactive action supported by top-level backing. At the first crypto summit held at the White House in March this year, Trump expressed interest in stablecoins, stating that this would become a "promising" growth model and explicitly hoped that Congress could submit relevant legislation to the President's office before the August recess, sending a clear signal.

On March 17, the Senate Banking Committee passed the GENIUS Act with bipartisan support, 18 votes in favor and 6 against, officially submitting the bill to the Senate. On March 26, the STABLE Act successfully submitted a revised version, which was passed by the House Financial Services Committee on April 3 and submitted to the House for a full vote.

Although both are stablecoin bills, their focuses differ slightly. STABLE prioritizes federal unified control, while GENIUS emphasizes the establishment of a dual regulatory system that operates in parallel at the state and federal levels. STABLE limits issuance qualifications to insured deposit institutions and federally approved non-bank institutions, while GENIUS allows for a broader range of issuing entities. Both require a 1:1 reserve backing and monthly disclosures, but STABLE is stricter, requiring additional insurance from the Federal Deposit Insurance Corporation (FDIC) and imposing a two-year ban on algorithmic stablecoins, while GENIUS allows for exploration of algorithmic stablecoin mechanisms under specific conditions. Additionally, the GENIUS Act supports stablecoins providing interest or returns to holders, while the STABLE Act explicitly prohibits interest payments.

In practice, both bills face various criticisms. State governments oppose federal regulatory priority for STABLE, some industry participants express dissatisfaction with the stringent terms, and GENIUS primarily faces discussions about compliance costs, arguing that the dual-track system will increase compliance costs and that the bill overly focuses on the U.S. domestic market, neglecting the needs of third-world countries.

Currently, the GENIUS Act is progressing more rapidly than STABLE. On May 9, during a Senate vote, the GENIUS Act failed with 48 votes in favor and 49 against, as Democrats demanded stronger anti-corruption provisions and a ban on members of the executive branch holding cryptocurrencies, accusing Trump of crypto corruption, but the Republicans did not relent. In response to this incident, the U.S. Treasury Secretary tweeted that U.S. lawmakers are doing nothing and expressed dissatisfaction with the decision.

Not long after, the GENIUS Act made another attempt, and in the updated version, it divided the regulatory mechanism based on scale: stablecoins with assets exceeding $10 billion would be federally regulated, while those with a market value below $10 billion would be self-regulated by the states. It also clearly delineated the separation from U.S. insurance credit and government credit, reducing systemic risk and increasing restrictions on technology companies' participation in stablecoins. Although the updated bill still did not address the ethical standards questioned by the Democrats, it made progress in protecting investors and existing mechanisms. Against this backdrop, some Democrats successfully switched sides, and on the evening of the 19th, the U.S. Senate passed the procedural motion for the GENIUS Act with a vote of 66 in favor and 32 against, clearing the way for final legislation. The next step will be to enter the full debate and amendment process in the Senate, followed by submitting the bill to the House of Representatives for review. Considering the relatively low threshold for passage in the House, the likelihood of this bill being submitted to the President's office for signature and becoming final legislation is very high.

The passage of this bill is undoubtedly an important milestone in the history of U.S. crypto assets, filling the regulatory gap for stablecoins in the U.S., clarifying regulatory subjects and rules, and further promoting the vigorous development of the U.S. stablecoin industry, contributing to the mainstreaming of the crypto industry. From the perspective of the U.S. itself, after the regulations are enacted, the benefits of the dollar penetrating and influencing based on stablecoins will become more pronounced, with the trend of the crypto market becoming an appendage to the dollar continuing to strengthen, providing a core driver for building centralized and decentralized hegemony for the dollar. It is worth noting that regardless of the type of bill, stablecoin holders are required to hold U.S. Treasury bonds, dollars, etc., which also creates new and sustained demand for U.S. Treasury bonds.

03. Beyond the U.S., Global Stablecoin Regulation is Taking Shape

With clear stablecoin regulation not expected until 2025, it is evident that the regulation of stablecoins in the U.S. is not at the forefront. In fact, even before the U.S., the European Union had introduced the Markets in Crypto-Assets (MiCA) regulation, providing a comprehensive regulatory framework for all crypto assets, including stablecoins. In terms of stablecoins, MiCA categorizes them into asset-referenced tokens and electronic money tokens, also prohibiting algorithmic stablecoins. It requires stablecoin issuers, especially those with a certain market scale, to maintain a 1:1 capital reserve, comply with transparency rules, and register with EU regulatory authorities. Meanwhile, the European Insurance and Occupational Pensions Authority (EIOPA) has recommended implementing strict capital management systems for insurance companies holding crypto assets (including stablecoins), requiring these companies to maintain a 100% capital adequacy ratio for such asset holdings, treating them as zero-value assets in solvency calculations.

Outside the EU, Hong Kong is also a leader in stablecoin regulation. On December 6, 2024, the Hong Kong government published the "Stablecoin Bill" in the Gazette and submitted it for a first reading in the Legislative Council on December 18. According to the latest news, the plan will resume second reading debates in the Legislative Council on May 21. Hong Kong's approach to stablecoin legislation shows a cautious and inclusive attitude, also adopting a licensing system for management. It specifies that issuers must establish themselves in Hong Kong, have sufficient financial resources and liquid assets, and pay a minimum capital of HKD 25 million. They must ensure that reserve assets are segregated from other reserve asset combinations and specify that the market value of the reserve asset combination must at all times be at least equal to the face value of the outstanding and circulating stablecoins, i.e., a 1:1 reserve. Earlier, in July of last year, the Hong Kong Monetary Authority announced the list of participants in the stablecoin issuer "sandbox," including JD Coin Chain Technology (Hong Kong) Co., Ltd., Yuan Coin Innovation Technology Co., Ltd., Standard Chartered Bank (Hong Kong) Ltd., Anni Group Ltd., and Hong Kong Telecommunications Ltd.

In addition to the regions mentioned above, Singapore and Dubai have also engaged in stablecoin regulation. Singapore released a stablecoin regulatory framework in 2023, while Dubai included stablecoins in the "Payment Token Services Regulation."

Overall, the differences in global stablecoin regulation are limited, with later adopters showing clear signs of absorbing the experiences of earlier ones. Global regulatory agencies focus on licensing to regulate issuers and have made clear provisions regarding reserve issuance, risk isolation, anti-money laundering, and anti-terrorism. The main differences lie in the categories of stablecoins allowed, restrictions on issuers, and localized anti-money laundering compliance.

However, the successive introduction of stablecoin regulations in major global regions reflects that the role of stablecoins in the global financial market is transitioning from being overlooked to becoming a topic of widespread discussion. Stablecoins are gradually becoming an important component of the global currency market, further enhancing the voice of the crypto market and adding significant weight to killer applications in the crypto field. On the other hand, third-world countries can also use stablecoins for 24-hour global settlements, which truly realizes Satoshi Nakamoto's original vision—free electronic cash.

Time changes everything, and life is full of changes. After a century of crypto, how many proclaimed value applications will still exist after the sands of time have settled? As it stands, at least stablecoins and Bitcoin still hold their significance.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。