Original Title: "In the Narrative-Free Market, Binance Alpha's Artificial Bull Market Falls into a Mixed Situation"

Original Author: Kevin, the Researcher at Movemaker

The Failure of Binance Alpha 1.0 and the Strategic Shift to Alpha 2.0

Due to failures on the Binance wallet, Binance Alpha 1.0, which served as a liquidity bridge for Binance on-chain, has been declared a failure. The trading volume and user numbers before the upgrade fell to historic lows, with the total daily trading volume of all tokens on Alpha being less than $10 million and daily transaction counts dropping below 10,000, which is undoubtedly a stark contrast to the scale within the Binance trading platform. Not only did it fail to attract on-chain users and corresponding liquidity to the trading platform, but it also reflected negatively in marketing.

As a result, Binance Alpha was upgraded to Binance Alpha 2.0 at the end of March. This upgrade directly integrated Alpha into the Binance APP, allowing users to purchase Alpha tokens using funds from the trading platform, unlike 1.0, which could only be accessed through the Binance Web3 wallet.

The inability to expand the wallet user base means that Binance's strategy of using Binance Alpha as a bridge to compete for on-chain liquidity has not worked, failing to attract liquidity while also failing to enhance attention on BSC. In other words, when Binance's on-chain growth cannot form a natural positive cycle, it can only go against the grain by injecting traffic from the trading platform back into Alpha, allowing Binance Alpha to achieve a quantitative change that attracts market attention, and under sufficient wealth effect, complete a qualitative change, ultimately becoming a forward base for Binance to attract on-chain liquidity and amplify the presence of the BSC chain.

The Waiting Period Without Consensus Confirmation: The Low Point Before Alpha 2.0's "Gunshot"

This assumption is reasonable, but for it to work, a major premise is needed: in a market where liquidity is not abundant, providing a consensus for observing funds to take the next step is essential to ignite market attention for Binance Alpha 2.0. Without such a trigger, even if Alpha upgrades to 2.0, from the data between the end of March and mid-April, whether in terms of order book depth or the promotion of wealth effects, it can only stimulate market discussion for less than a week within a brief window, quickly returning to silence and falling back into a low point in early April.

Of course, this is not a failure of the Alpha 2.0 upgrade or a misstep in strategic direction, because to expand Alpha's scale, which is the total trading volume of Alpha, apart from introducing liquidity from DEX, the only option left is to inject liquidity from Binance's own trading platform. The reason why 1.0 chose the former option is that, on one hand, it is a ready-made approach for second-tier trading platforms that the market can quickly accept; on the other hand, Binance's absolute confidence as a leading trading platform differs from the starting point of second-tier trading platforms, which view the introduction of on-chain liquidity as their foundation. Therefore, they can achieve agile responses in user experience or marketing, while Binance's approach to introducing on-chain liquidity is more of a precaution rather than an urgent necessity. Consequently, the poor experience of the Binance wallet and the sharp downturn in the Q1 market made it difficult for Binance to quickly pivot, leading to the demise of Alpha 1.0.

Thus, it can be said that injecting liquidity back from the trading platform is Binance's last resort and the most powerful upgrade. However, from the data of Alpha 2.0 between March 20 and April 20, it can still be described as bleak. Why? Because even though the pipeline or path for injecting liquidity has been successfully built, the influx of liquidity still requires a signal, a gunshot. In the current atmosphere of despair where all narratives in the crypto market have collapsed, only Bitcoin can take on the role of that starting gun.

Bitcoin Signal Activation, Alpha 2.0 Trading Ecosystem Welcomes a Turning Point

Bitcoin's price has become closely tied to the macroeconomic trends in the U.S., and for Bitcoin to break out into a new market, it also requires support from macro market confidence. In the previous article, Bitcoin's consolidation around $85,000 for a week was waiting for confirmation of macro confidence. Therefore, when the market was deeply entrenched in fears from tariffs and recession, and due to the positive news from the 90-day tariff cooling period, strong U.S. economic performance, and progress in U.S.-China negotiations, a brief market easing period emerged. At this moment, there was no need to consider the risk of further tariff deterioration, and the funds could ignore the safe-haven caused by recession. In the not too long future of several days, the sources of negative news were tightly constrained, which provided sufficient confidence confirmation for Bitcoin. The market began to activate on April 21, and from Ethereum's strong breakout over three days, it can be seen that large funds were rushing in, entering the second phase of the market.

Thus, when Bitcoin sends out a signal, the thirsty liquidity will first flow into high-risk assets, and the pipeline created by Alpha 2.0 will begin to show its effects.

Point Incentives and Token Bubbles: The Dual-Drive Strategy of Alpha 2.0

Returning to Alpha 2.0 itself, its main role, in addition to attracting on-chain liquidity mentioned earlier, is to serve as a reservoir for Binance. To weaken Binance's coin listing effect, it is necessary to preemptively divert liquidity when new coins are listed while ensuring that this liquidity is indeed within Binance and not spilling over to other trading platforms. Therefore, when Bitcoin sends out a signal and the market's short-term consensus is strong, the direction for Alpha 2.0 becomes very simple: how to create a bubble in the reservoir through the narrative manipulation of the market makers in each cycle. Alpha 2.0 chooses two methods to create bubbles:

Bottom-Up Point Promotion

Alpha points are a direct incentive to increase trading volume and liquidity, calculated by adding balance points and trading volume points within 15 days.

Balance Points: Different assets held in varying balances in the trading platform and wallet can earn different points daily, for example: $10,000 to $100,000 = 3 points/day.

Trading Volume Points: Points are awarded based on the purchase amount of Alpha tokens, for example: every $2 spent earns 1 point, and every time the purchase amount doubles, an additional point is awarded (e.g., $2 = 1 point, $4 = 2 points, $8 = 3 points…).

The level of Alpha points is related to eligibility for airdrop activities, for example: having 142 Alpha points can qualify for an airdrop of 50 ZKJ tokens.

The difficulty of obtaining points increases with the rise in balance and trading volume. The goal of Alpha 2.0 is to provide incentives to the widest range of users, encouraging them to maintain a certain asset balance in the trading platform and wallet and actively participate in Alpha token purchases, ultimately driving market depth and activity. The double trading volume points event starting on April 30 stimulated the enthusiasm of longer-tail users, allowing anyone who places an order or directly buys BSC tokens to earn double points. Binance uses double points to allow a broader range of users to qualify for airdrops, creating market heat and activity, giving the main force behind Alpha tokens more substantial momentum.

From the trading volume of Alpha 2.0 since April 20, Binance has effectively increased the asset holdings and trading volume within the platform, further enhancing the overall market activity and depth. As more and more users actively participate, the market liquidity of Alpha tokens will be significantly enhanced, and the continuous operation of this virtuous cycle will be key for Binance to stand out in future market competition.

Liquidity Convergence Forming a Leading Effect

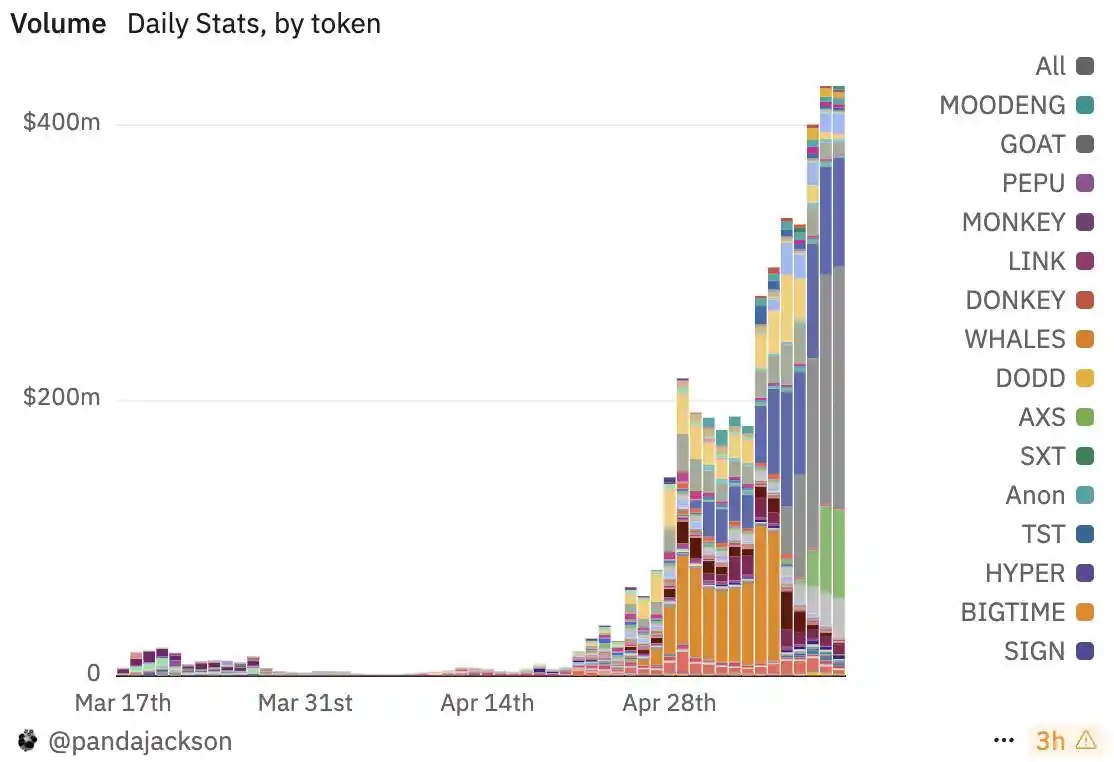

Observing the daily trading volume trend of Alpha tokens after the shift to Alpha 2.0, it can be seen that the change in rules itself did not create enough stimulation or interest among market funds. However, the signal from Bitcoin is a strong consensus, and the main sources of daily trading volume for Alpha tokens are: $KMNO, $B2, $ZKJ.

$KMNO: A DeFi protocol on Solana, Kamino Finance, began a one-sided decline after entering Binance Alpha on February 13. Over the week of April 28, trading volume began to expand, increasing 40 times compared to two weeks ago, but the price fluctuated only between $0.065 and $0.085. It wasn't until May 6, when it was listed on Binance, that trading volume returned to normal levels.

$B2: A Bitcoin ecosystem L2 protocol, launched on April 30 and entered Binance Alpha. Its market cap peaked at only $30 million, currently at $27 million, with trading volume gradually increasing after the token launch, showing a clear pattern of increased trading volume during Asian daytime and decreased at night.

$ZKJ: A ZK protocol, Polyhedra Network, launched on May 6 and entered Binance Alpha. Its market cap is $130 million. The fluctuations in trading volume are similar to $B2, with increased trading volume during Asian daytime and decreased at night.

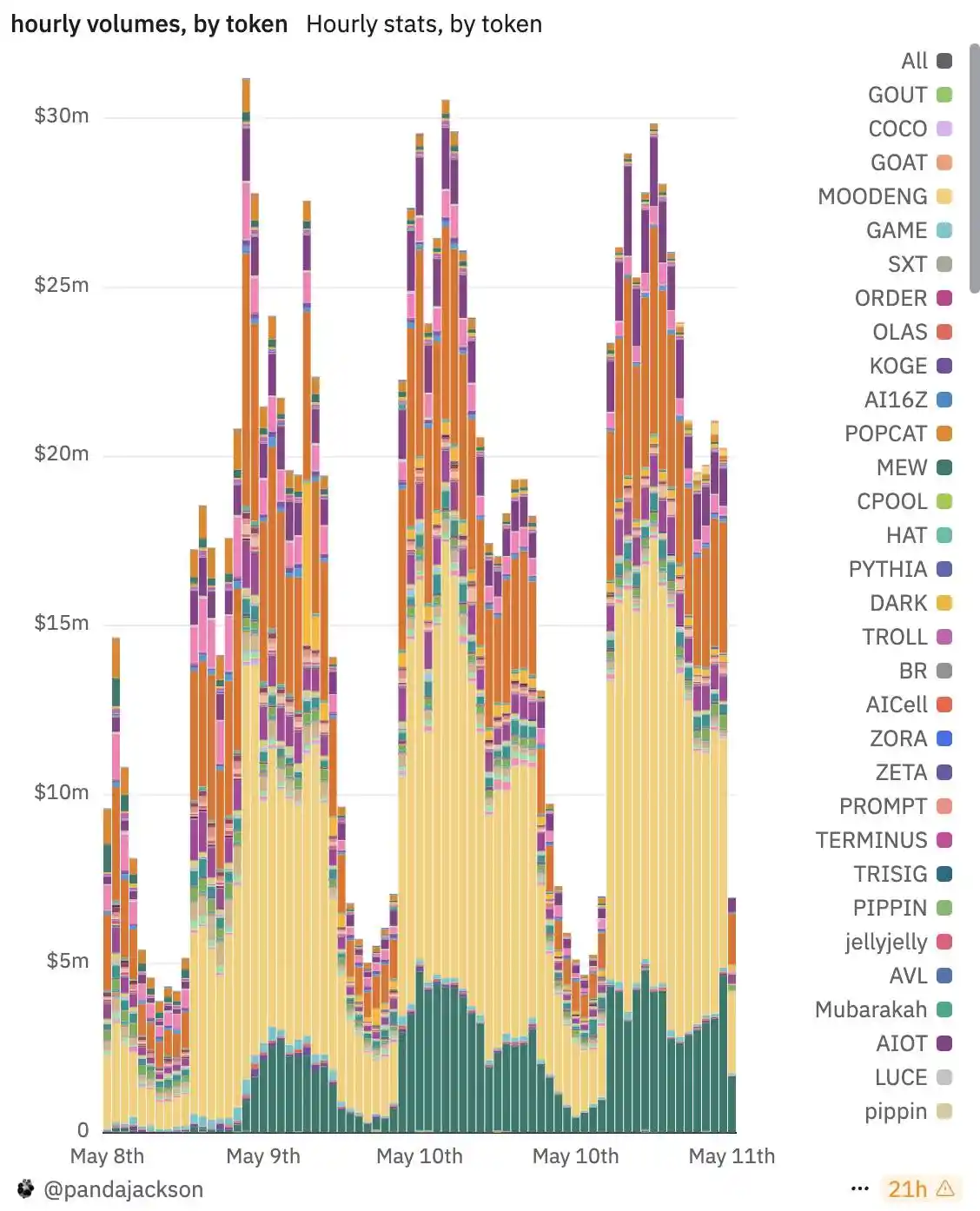

Asian Daytime Driving Model: The True Picture of Alpha Liquidity

From the hourly trading volume charts, it is clear that the main contributing tokens to Alpha 2.0 exhibit strong intraday cyclical volatility characteristics. This regular trading behavior was repeated over the four days from May 8 to May 11, showing significant volume increases daily from midnight to noon UTC (approximately from 8:00 AM to 8:00 PM Beijing time), while trading volume noticeably declined or even languished from the afternoon to late night UTC (evening to early morning Beijing time). This rhythm aligns perfectly with the working hours of the Asian trading zone, indicating that the trading ecosystem of Alpha 2.0 is currently highly dependent on the liquidity support from the Asian market. Especially during active daytime hours in Asia, the total hourly trading volume repeatedly exceeded $25 million, even approaching $30 million at one point, demonstrating a highly concentrated market-making and trading operation.

Additionally, from the trading volume distribution structure of various tokens, ZKJ (yellow) is the absolute main force in trading volume, dominating the majority of time periods. Its trading volume changes in sync with the overall market rhythm, further reinforcing the inference of "systematic market-making." Besides ZKJ, tokens like B2 and SKYAI also showed significant activity during peak periods, forming a "market-making matrix" within the Alpha 2.0 ecosystem. The trading volume fluctuations of these tokens are highly consistent, resembling not spontaneous trading by natural users but rather batch orders and matching operations controlled by automated market-making systems or bots. The fixed time periods for initiating and withdrawing trades likely stem from a standardized, automated trading program, possibly indicating that the team conducts concentrated operations during Asian daytime and significantly reduces activity or shuts down strategies at night.

Overall, the current trading activity of Alpha 2.0 presents a typical "Asian daytime market-driven model," where market depth and liquidity largely depend on the market-making activities of a few leading tokens and the natural trading of global users. Although this model can support trading volume and activity in the short term through concentrated market-making, it also exposes the platform's ecosystem to reliance on a single time zone and limited market-making entities. Once these market-making accounts cease operations, the platform's trading volume may experience a sharp decline. To build a more sustainable trading ecosystem in the future, Alpha 2.0 needs to introduce more time zones and more participants' natural trading behaviors, thereby breaking free from the current overly singular rhythm and obvious market-making traces.

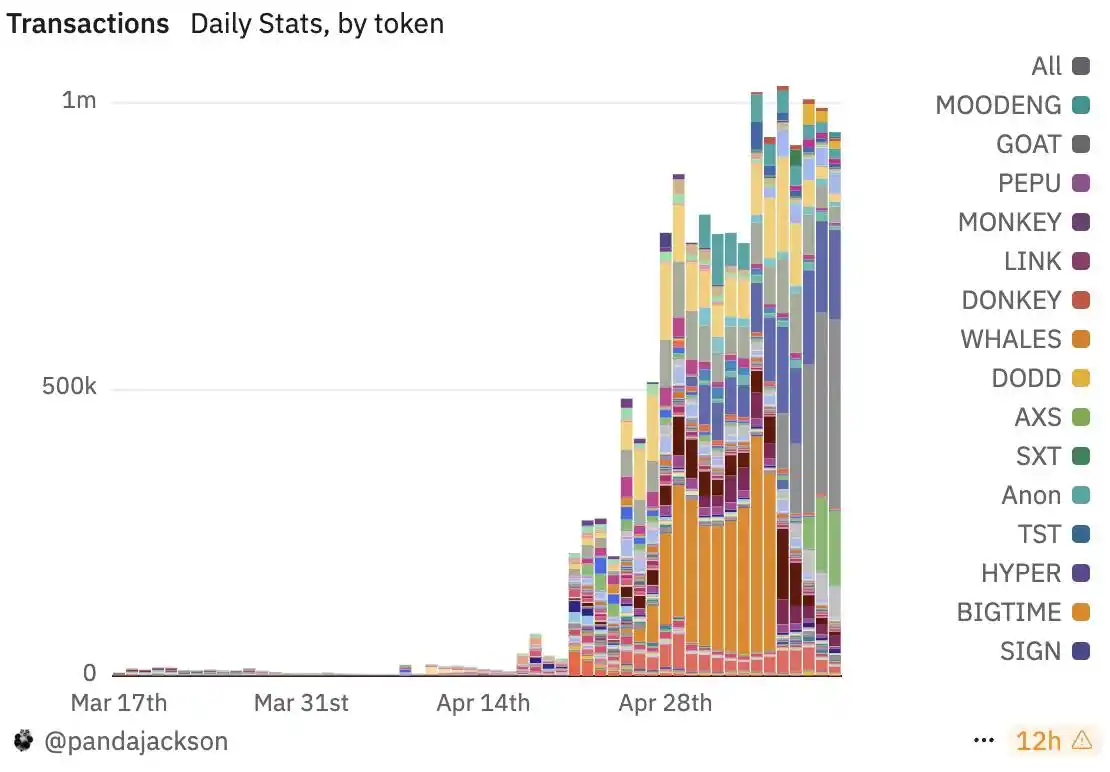

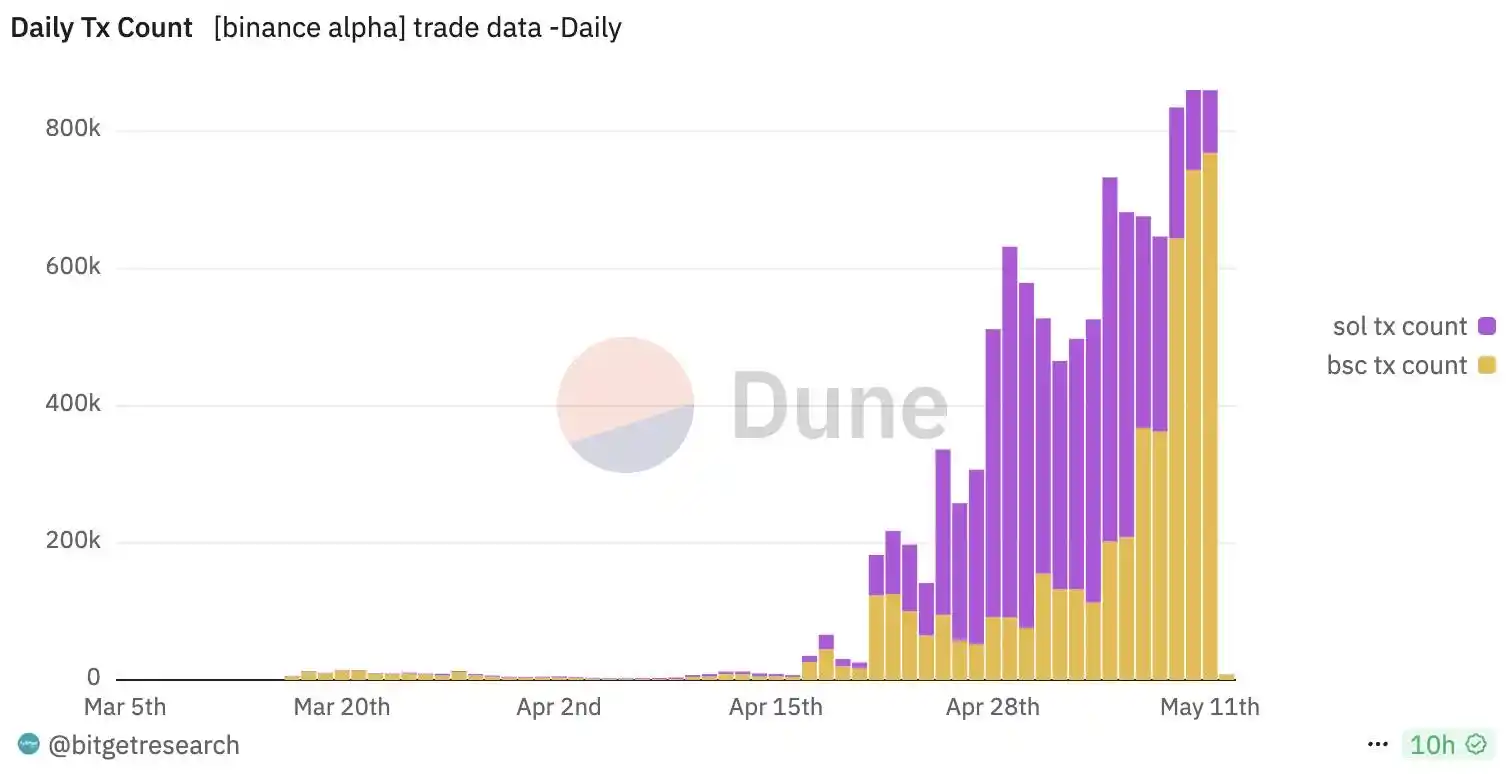

From the chart below, it can be observed that after April 20, the platform's trading activity entered a rapid growth phase, with the number of transactions quickly climbing from the early hundreds of thousands to an average of nearly one million per day. However, starting around April 28, although trading volume remained high, the daily transaction count began to stabilize, even showing a slight decline in recent days. This divergence of "slowing growth in transaction count while trading volume continues to rise," combined with the previous "hourly trading volume distribution chart," points to a very clear structural change: the trading behavior on the Alpha 2.0 platform is gradually shifting from a high-frequency, low-value "retail trading" model to a low-frequency, high-value "market-making driven" model.

The main driving force behind this change is likely the strengthening of market-making strategies for leading tokens. The tokens shown in the previous chart, such as ZKJ and B2, experience dramatic increases in trading volume during specific periods (especially during Asian daytime), indicating that these tokens have become the liquidity hub of the platform. The trading of these tokens is typically executed by a small number of market makers or automated trading bots, whose strategies may no longer pursue high-frequency matching but instead focus on placing orders, matching, and arbitraging with larger transaction amounts. Therefore, even if the number of transactions grows limited, the volume of individual transactions may significantly increase, thus driving the overall trading volume to continue rising. This structural "quality substitution" phenomenon, combined with the incentives for users to place orders during the double points event, indicates that Alpha 2.0 has entered a new phase characterized by liquidity depth optimization and concentrated trading of core tokens.

Further inference suggests that this structural change also reflects the development bottlenecks and adjustment strategies currently faced by the platform. On one hand, the platform's original phase relied on a large number of tail tokens and retail participation to drive transaction counts, but the marginal effects of this growth model are gradually diminishing; on the other hand, the platform is attempting to maintain or even elevate overall trading volume by introducing stable market-making mechanisms and a leading token ecosystem, thereby attracting more liquidity and user attention. If this trend continues, Alpha 2.0 will face two strategic choices: one is to further expand market maker participation, guiding the formation of more "high-value low-frequency" main trading pools; the other is to optimize user experience and fee structures to re-stimulate retail intraday activity, achieving a new peak of "high-frequency high-value" trading.

Inter-Chain Switching and Market-Making Structure: The Liquidity Migration Logic of Alpha 2.0

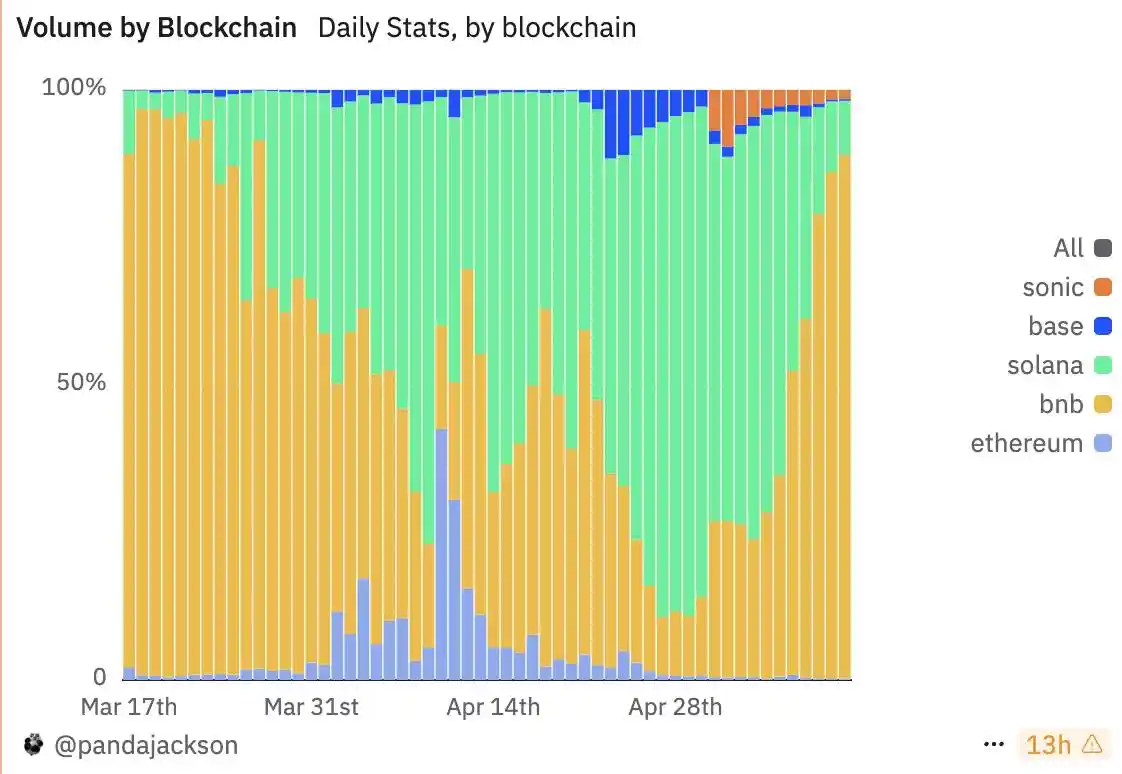

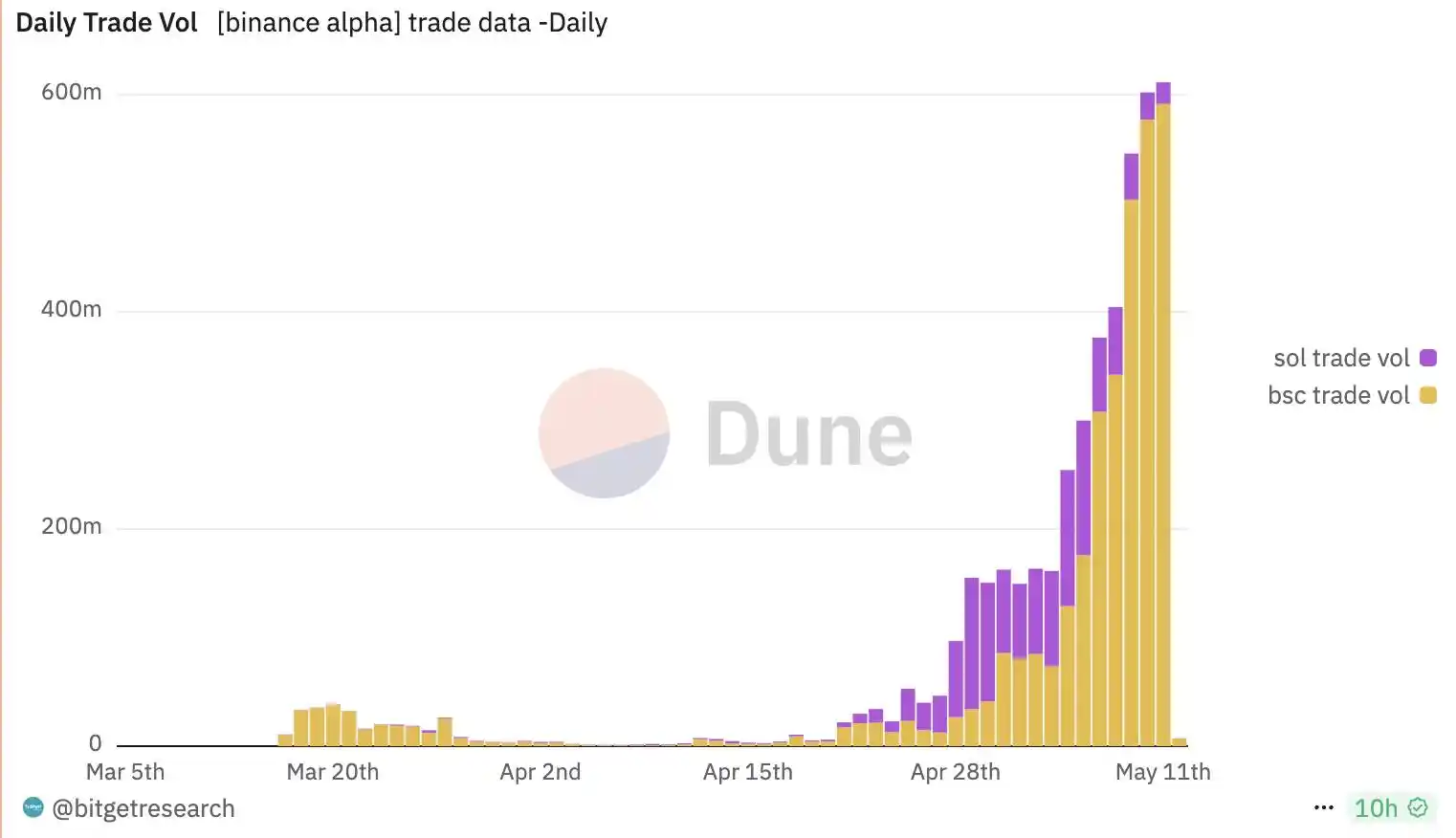

From the chart below, it can be seen that the daily trading volume of Alpha 2.0 tokens has undergone significant structural migration between different blockchains, showing a clear phase of dominant chain changes. Starting from mid-March, after the rule changes of Alpha 2.0, the BNB chain (orange) was the absolute dominant force, accounting for nearly 100% of the trading volume. However, entering late March and early April, Solana (green) gradually rose, beginning to compete for dominance with the BNB chain, and by mid-April, it completed an "overtake" of BNB, stabilizing its share of daily trading volume at over 60%-80% for about two weeks, becoming the main liquidity venue for Alpha 2.0. This period can be seen as a calm phase in the market, which I believe reflects the true traffic level of Alpha 2.0.

Following this, from late April to early May, the BNB chain regained its dominant position, with its share rising back to nearly 60%-70%, marking a round of inter-chain liquidity return.

From this trend, several key changes can be interpreted: first, the liquidity of Alpha 2.0 is highly migratory, and it can also be seen that the activity of BSC is highly dependent on market makers and bots; second, Solana once became the preferred chain for carrying Alpha trading demand due to its high-speed and low-cost on-chain performance, but this lead is not stable; as long as market sentiment reverses, a massive trading volume can be injected into BSC at any time.

Overall, the current rhythm of trading volume migration between chains in Alpha 2.0 reflects a typical "liquidity arbitrage + incentive migration" driven model, rather than a long-term deep cultivation fixed on a single chain. This also indicates that the future traffic construction of the Alpha platform will still be constrained by inter-chain competition, cross-chain deployment costs, incentive strategies, and other external variables, and it is not ruled out that a new round of main chain switching may occur.

When comparing the changes in trading volume and transaction counts of Alpha 2.0 tokens on BSC and SOL, it can be found that overall, Binance Alpha 2.0 experienced explosive growth after mid-April, and this growth trend continued until mid-May.

In terms of transaction counts, Solana performed particularly well in the early stages (especially in late April), with its transaction numbers significantly higher than those on BSC, indicating that during this phase, the main liquidity of Alpha 2.0 was still on Solana. However, by early May, the transaction numbers on BSC quickly caught up and even surpassed those on Solana, showing that as time progressed, the activity of Alpha 2.0 on BSC rapidly increased, possibly related to adjustments in market-making strategies. Although Solana still maintained stable trading volume, its growth rate appeared to slow down slightly.

Opportunities and Concerns During the Emotional Recovery Period: The Next Challenge for Alpha 2.0

In the current recovery period following the recession and tariff shocks, the crypto market has fallen into a deadlock lacking narrative breakthroughs: without a new main storyline, it is impossible to form a market synergy, and the leading effects commonly seen in main narratives are difficult to manifest, making it naturally challenging to generate a true wealth effect. Although USDT is abundantly supplied in the market, overall liquidity remains tight in horizontal comparison. At this moment, no other narrative can take on the responsibility of driving the overall situation; only Ethereum can play the dual role of "narrative core" and "liquidity reservoir" in the fleeting waves. While it is difficult to firmly state that expectations of network upgrades or the actual implementation of ETF staking have brought buying pressure to Ethereum, from another perspective, the current market has deteriorated to the point where Ethereum needs to become the main carrier of market sentiment and capital flow. The past small bull market often sees this role taken on by leading projects.

When Ethereum or some Memecoins or other hot assets experience short-term explosive gains, strong project parties and top trading platforms (like Binance) must unhesitatingly follow this wave of enthusiasm, never remaining on the sidelines or missing opportunities due to hesitation. Because whether this current small cycle bull market, catalyzed by emotional recovery, can further evolve into a larger-scale bull market remains uncertain. If strong project parties do not respond in a timely manner to price K-lines or trading volume on the trading platform, they can easily be judged by the market as "insufficient energy" and subsequently abandoned. Even if the current small bull market ultimately fails to upgrade successfully, there are still many potential positives (such as liquidity recovery) to initiate market movements.

In this context, strong project parties and trading platforms should leverage every rising cycle to cultivate market confidence and solidify wealth consensus: as long as liquidity is continuously injected and transactions are actively generated before market corrections, they can establish a positive image in investors' minds of "ample funds and a keen market sense." Conversely, if they choose to "hold back" at critical junctures, they are likely to be seen as lacking sustained driving force, making it difficult to gather sufficient market synergy when larger-scale market movements arrive in the future.

For Alpha 2.0, the current emotional recovery period brings both opportunities and exposes concerns. From the perspective of real on-chain traffic, the activity on BSC is almost negligible—this is clearly not the ideal result that Binance and its ecosystem hope to see. The current hustle and bustle of Alpha 2.0 relies more on concentrated operations by market makers and project parties rather than spontaneous participation from global retail investors. This "artificially stacked" apparent trading volume, once external stimuli are lost, is highly likely to experience a sharp decline. How many more small or large bull markets will need to be experienced to gradually cultivate a truly spontaneous and positive liquidity ecosystem? This is precisely the core variable we need to focus on when observing the future development of Alpha 2.0.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。