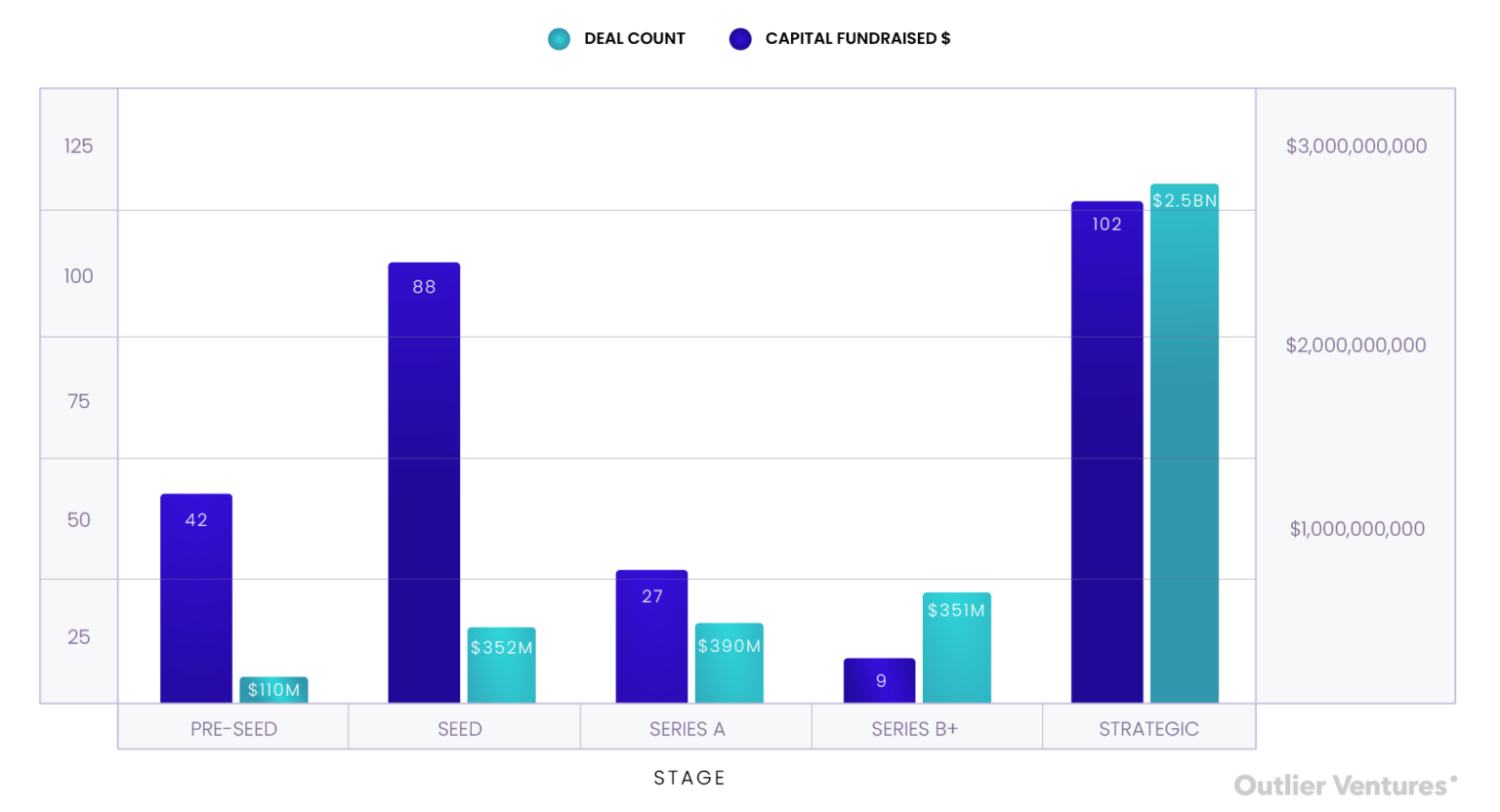

Strategic financing rounds dominate the market, with 102 transactions attracting $2.5 billion in funding, continuing the trend of sovereign funds and ecosystem capital supporting large infrastructure and Layer 1 projects.

Author: Robert Osborne

Translation: Deep Tide TechFlow

Overview

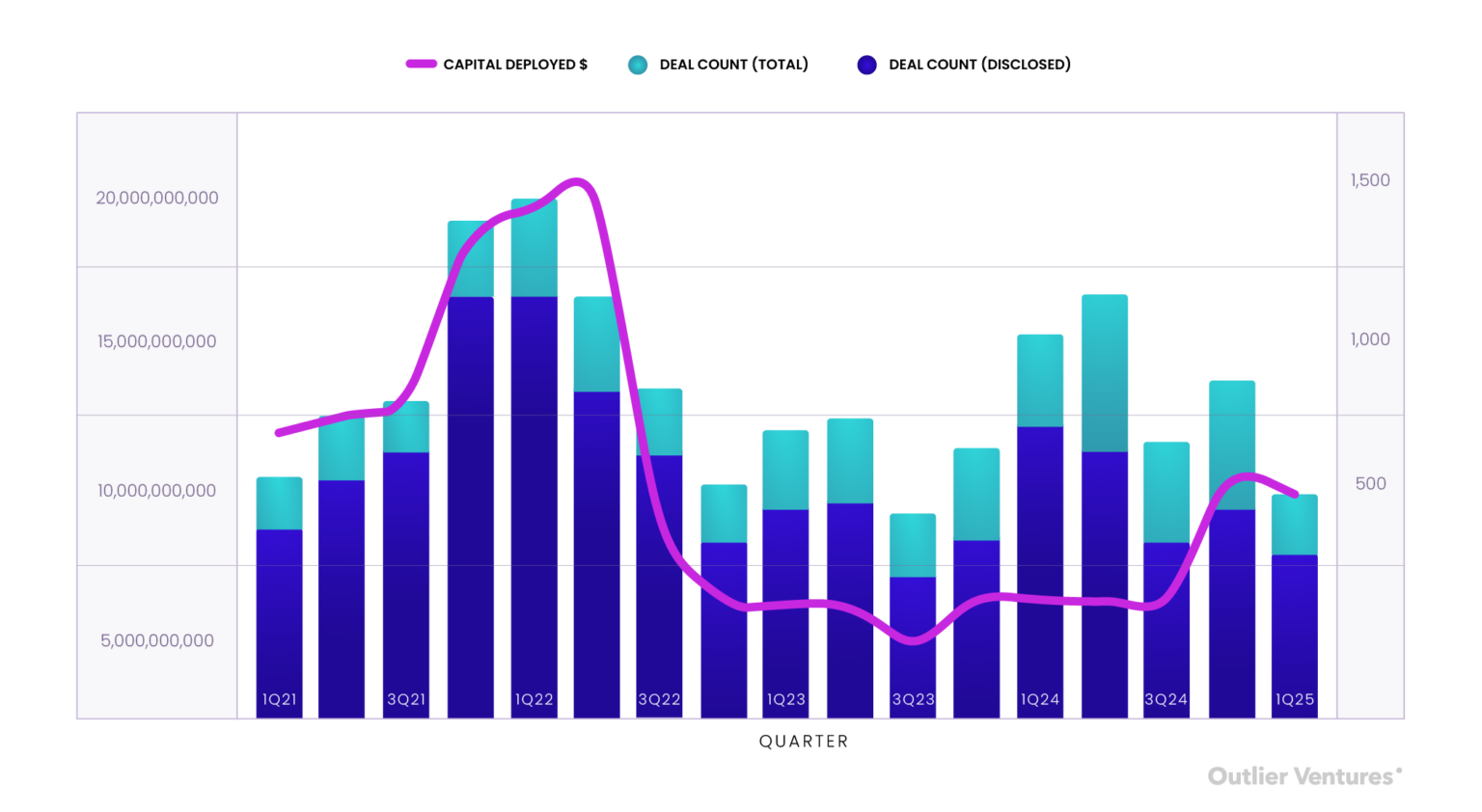

In the first quarter of 2025, the financing scale in the Web3 sector remained stable, raising a total of $7.7 billion, nearly matching the record $7.9 billion in the fourth quarter of 2024. However, the number of transactions decreased by 34%, reaching the lowest level since the third quarter of 2023.

Binance's single financing of $2 billion accounted for more than a quarter of the total capital this quarter. Excluding this financing, actual market activity was about $5.7 billion, roughly in line with the average level of 2024.

Strategic financing rounds dominated the market, with 102 transactions attracting $2.5 billion in funding, continuing the trend of sovereign funds and ecosystem capital supporting large infrastructure and Layer 1 projects.

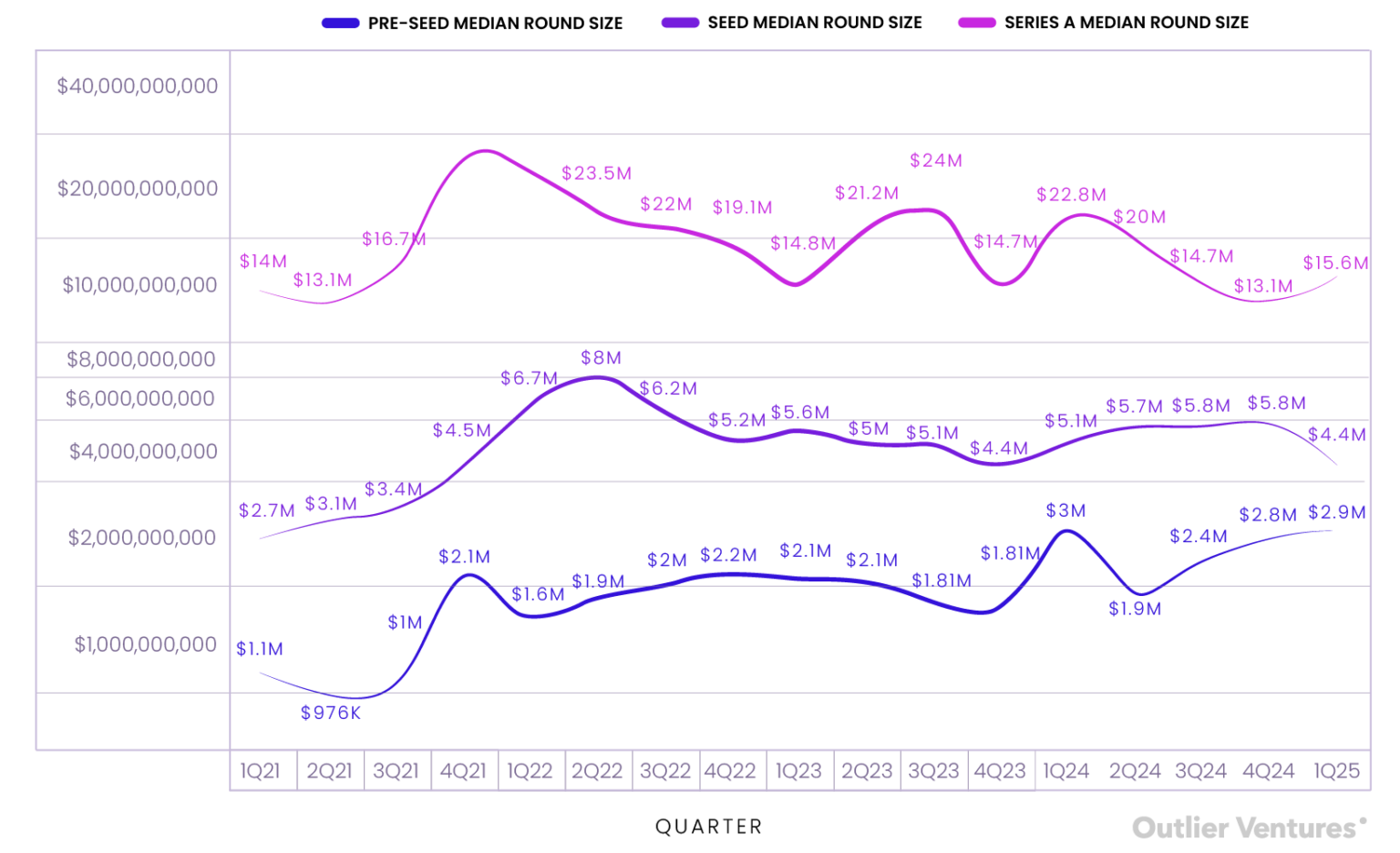

Early-stage financing showed divergence: Seed round financing dropped to a two-year low of $4.4 million, while Pre-seed round financing remained strong at $2.9 million. Series A financing continued to be squeezed, completing only 27 transactions, but the average financing amount rebounded to $15.6 million.

Category landscape exhibited characteristics of both decentralization and focus. The Networks category topped the list (thanks to Binance's push), while Data, Wallets, and Consumer Infra showed higher median financing amounts. Developer Tooling attracted the most investor participation, but the scale of financing rounds was smaller, indicating it remains the "long tail" part of the infrastructure sector.

Token financing rebounded strongly: 96 public and private sales raised a total of $1.6 billion, marking the strongest quarterly performance since 2022. Among them, World Liberty ($590 million) and TON ($400 million) became landmark cases.

Market Overview: Capital Concentration Prioritizes Transaction Quantity

The Web3 financing in the first quarter of 2025 displayed a unique contrast: while total capital deployment remained high at $7.7 billion, nearly reaching the record $7.9 billion in the fourth quarter of 2024, the number of transactions plummeted to just 603. What does this mean? Investors are putting larger amounts of money into fewer companies, prioritizing concentrated capital rather than widespread dispersion.

Figure 1: Quarterly number of transactions and funds raised in Web3 from Q1 2021 to Q1 2025

Source: Outlier Ventures, Messari

This divergence highlights the ongoing adjustment of investor strategies. As market liquidity gradually recovers, overall sentiment is becoming optimistic, and venture capital firms seem to be doubling down on "category winners" and increasingly mature infrastructure projects, rather than spreading capital across high-risk long-tail projects in early stages. Similar to the fourth quarter of 2024, most funds flowed into mid to late-stage financing rounds and projects that define ecosystems, which typically have strong market traction, support from well-known investors, or are ready to launch token strategies in the market. (For a deeper understanding of this shift from consumer projects to infrastructure projects, please refer to our previous analysis article: “Everything You Know About Web3 Fundraising Is Wrong”.)

However, the total financing amount of $7.7 billion masks the underlying reality. Binance's $2 billion financing—led by UAE-based MGX Capital and described as the largest single private crypto financing to date—accounted for over 25% of all capital deployed this quarter. Excluding this exceptional case, the total financing in the first quarter of 2025 would drop to about $5.7 billion, closer to the overall level of 2024 (which was below $4 billion before the fourth quarter of 2024). This indicates that investor interest is relatively sustained, rather than a sudden surge in financing activity.

Even excluding this outlier, capital deployment still shows resilience. Late-stage growth rounds in infrastructure and AI-related fields continue to attract attention. Phantom's $150 million Series C financing, Flowdesk's $91.8 million financing, and LayerZero's $50 million extension round financing all indicate that a group of increasingly mature infrastructure companies is consolidating market share and moving towards revenue scaling.

Financing Stages: Strategic Capital Dominates

The financing data segmented by round stage in the first quarter of 2025 again emphasizes a core theme: strategic capital dominates.

Strategic rounds accounted for only 18% of total transaction volume but attracted over 32% of capital deployment, totaling $2.5 billion across 102 transactions. This continues the trend we observed at the end of 2024: crypto industry giants, ecosystem funds, and sovereign-backed entities are actively engaging in targeted and high-conviction investments, which are often highly aligned with national, institutional, or protocol-level interests. These financing rounds typically focus on Layer 1 (first-layer blockchain), middleware protocols, and token infrastructure—where the driving force behind capital deployment is not just return on investment (ROI), but also a deep alignment of interests and goals.

In contrast, early-stage financing still exhibits a trend of decentralization. Pre-seed and Seed rounds accounted for nearly a quarter (24%) of total transaction volume but attracted only 6% of capital deployment. The average pre-seed round financing was about $2.6 million; seed round financing averaged $4 million, significantly lower than the median financing amount in 2024. This indicates that valuation compression is occurring, or investors are investing with smaller check sizes while being stricter on terms for founders. This also means that "real due diligence" is making a comeback: founders need to demonstrate market traction, not just rely on vision to secure capital support.

Chart 2: Number of transactions and fundraising amounts from Pre-seed to Series B and above, as well as strategic rounds in Q1 2025. Further analysis of token activity will be elaborated below.

Source: Outlier Ventures, Messari

Series A financing continues to face pressure. Only 27 Series A financing transactions were recorded this quarter, accounting for less than 5% of total transaction volume, but attracting $392 million in funding, with an average round size of about $14.5 million. Investors seem to be completely skipping Series A financing, opting instead to enter at the seed round stage in a similar option-like manner, or waiting to enter the lower-risk, clearer token strategy B rounds and above.

Late-stage investments performed steadily. Only 9 transactions were completed in the B round and above, but they attracted $531 million in funding, with an average round size close to $59 million. These companies typically have validated business models and token mechanisms, and are prepared for exchange listings or treasury management. In many cases, these transactions are no longer traditional venture capital in the conventional sense, but resemble growth-stage quasi-private equity transactions.

Overall, the data segmented by financing stage confirms a broader view: the financing market is exhibiting a trend of divergence, not only between consumer projects and infrastructure projects but also between early experimental stages and later high-conviction investments. The intermediate stage—Series A financing—is precisely where risk appetite has disappeared and is currently the area where capital is least willing to venture.

If the number of transactions reflects market sentiment, capital deployment reveals investment conviction, then the median financing amount reflects the bargaining power of founders. In the first quarter of 2025, this bargaining power is gradually moving away from teams in the seed stage.

Chart 3: Changes in median financing amounts for Pre-seed, Seed, and Series A stages from Q1 2021 to Q1 2025.

Source: Outlier Ventures, Messari

The median financing amount for pre-seed rounds reached $2.9 million, nearly matching the peak in Q1 2024 and approaching three times the average value in 2021. This marks a quiet recovery of confidence in the earliest stages. Accelerators, ecosystem funds, and angel investment alliances seem to still favor early investments with options, especially those based on high-conviction narratives, such as decentralized physical infrastructure networks (DePIN), native AI infrastructure, and on-chain agent tooling. For founders, this remains the most capital-friendly stage.

However, the seed round has encountered a setback. The median financing amount dropped to $4.4 million, down from over $5.8 million in the previous quarter, marking the lowest level since Q4 2022. This is a strong signal indicating that the intermediate stage is shrinking. Investors are reducing check sizes, tightening terms, or directly bypassing this stage unless the project has clear key metrics or distribution capabilities. The "spray-and-scale" model is clearly no longer in existence.

Series A financing saw a slight rebound, with the median reaching $15.6 million, up from the cyclical low of $13.2 million in the previous quarter. Nevertheless, this is still far below the peaks of 2021 and early 2022, when medians often exceeded $30 million. More importantly, the number of transactions at this stage is extremely low (only 27), highlighting the selectivity of the market. These Series A financings are not just nominal—they are priced more like mini Series B rounds, applicable only to those companies that already have revenue, market traction, and executable token strategies.

In short, the "barbell effect" still exists: there is still capital flowing into the creative stage and market traction stage, but the intermediate stage is being abandoned. This is not a financing winter, but rather a reshaping and balancing of expectations for founders.

Capital Flow: Category Highlights

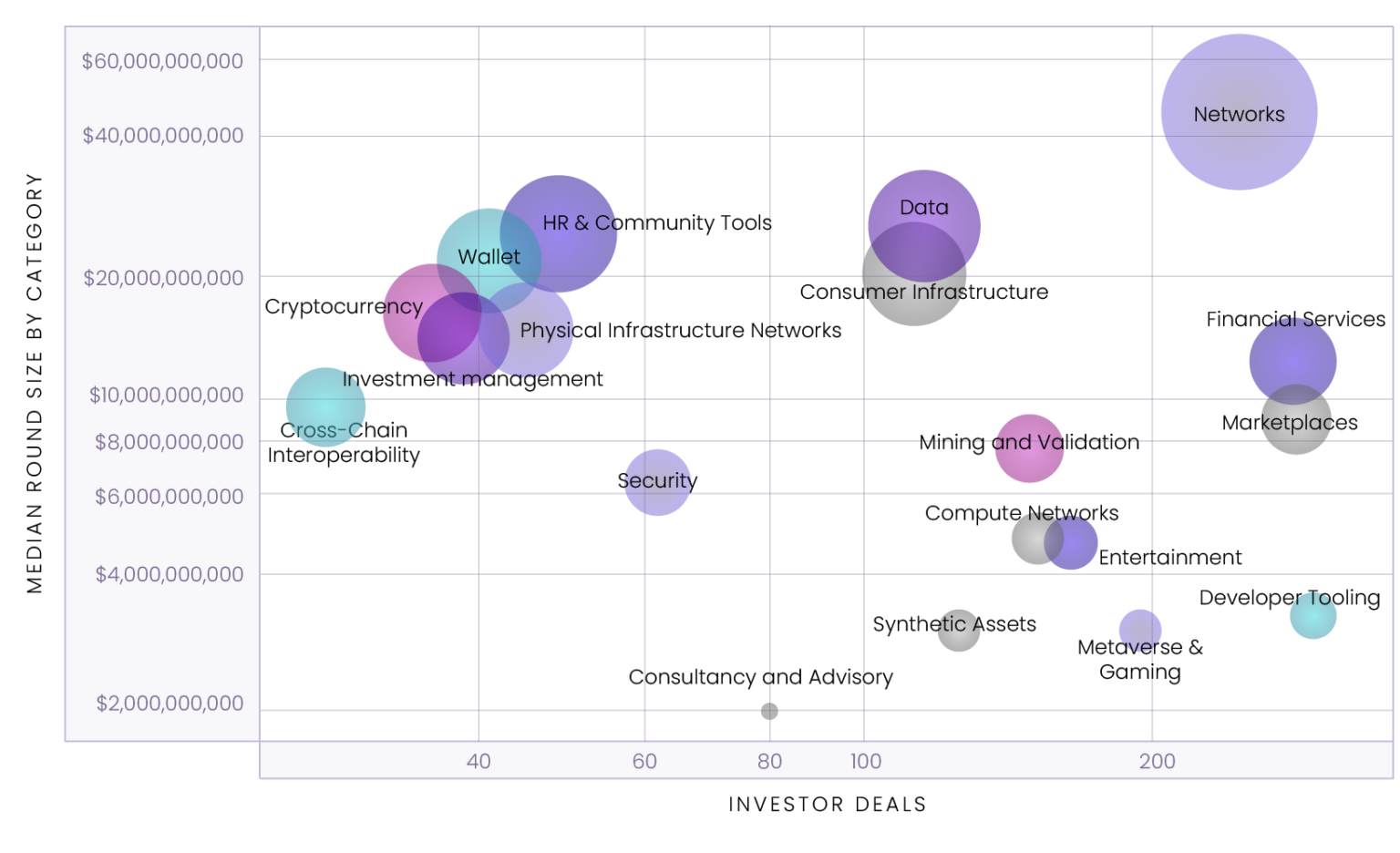

From a category perspective, the first quarter of 2025 continued to highlight the decentralization of capital deployment and the divergence of investor enthusiasm.

As expected, the Networks sector topped the list, with a median financing amount of $45.1 million, significantly influenced by Binance's $2 billion strategic financing. However, even excluding this outlier, the 243 investment transactions in this category indicate a high interest from institutional allocators, strategic funds, and ecosystem supporters in Layer 1 public chains and scalability projects. Network infrastructure remains a "stronghold" for capital flow, representing an area where investors wish to demonstrate serious intent.

Figure 4: Average financing stages and round sizes by category in Q1 2025

Source: Outlier Ventures, Messari

Note: "Investor transactions" refer to the total number of times investors participated within a category, rather than the number of independent investors. If an investor participated in three financings, it will count as three investor transactions.

Developer Tooling attracted the most investor participation, with a total of 290 investor transactions, but its median financing amount was only $3.1 million. This contrast highlights the role of developer tools as the "long tail" of infrastructure: high interest, low risk, and modular potential. These are typically smaller, faster transactions—led by engineers, aligned with protocols, and sometimes receiving funding subsidies.

On the consumer side, the Metaverse and Gaming sectors recorded 193 investor transactions, with a median financing amount of only $2.9 million, reflecting a trend towards "entertainment infrastructure" investments. The Entertainment sector also exhibited a similar pattern—with a median financing amount of $4.65 million and a total of 164 investor transactions—again indicating that venture capital firms (VCs) remain interested in audience-centric Web3 projects, but with a more cautious attitude.

The Marketplaces and Financial Services sectors also attracted attention due to high investor participation, with 279 and 277 investor transactions, respectively, but with differing capital intensity. The median financing amount in the marketplaces sector was $9 million, showing new interest in trading infrastructure and tokenized commerce. The median financing amount in the financial services sector was $11.98 million, making it one of the highest consumer sectors in terms of financing this quarter.

In the infrastructure category, Consumer Infrastructure ($19.3 million), Wallets ($20.7 million), and Data ($24.3 million) all showed high median financing amounts and moderate investor participation, indicating that although these areas are not as highly regarded as Networks or Compute, they are benefiting from a return to fundamentals: User Experience (UX), Composability, and Data Liquidity.

On the other end, the Consultancy & Advisory and News & Information sectors had low median financing amounts (around $2 million) and investor numbers—these categories struggle to demonstrate prospects for venture-scale funding and may be squeezed by public goods funding or native monetization models.

This quarter's "mid-tier" highlight categories—Cross-Chain Interoperability ($9.7 million), Security ($6.4 million), and Compute Networks ($4.8 million)—reflect that the highly technical, low-exposure infrastructure layer is still receiving significant support. These categories are no longer cutting-edge but have become part of the expected tech stack.

Token Financing Strongly Rebounds: Strategic Private Placements and Public Sales Advance Together

In the first quarter of 2025, token financing showed a clear reversal of the trends seen in 2024, with high-value, high-risk private sales making a strong comeback, while large-scale public sales also reignited enthusiasm.

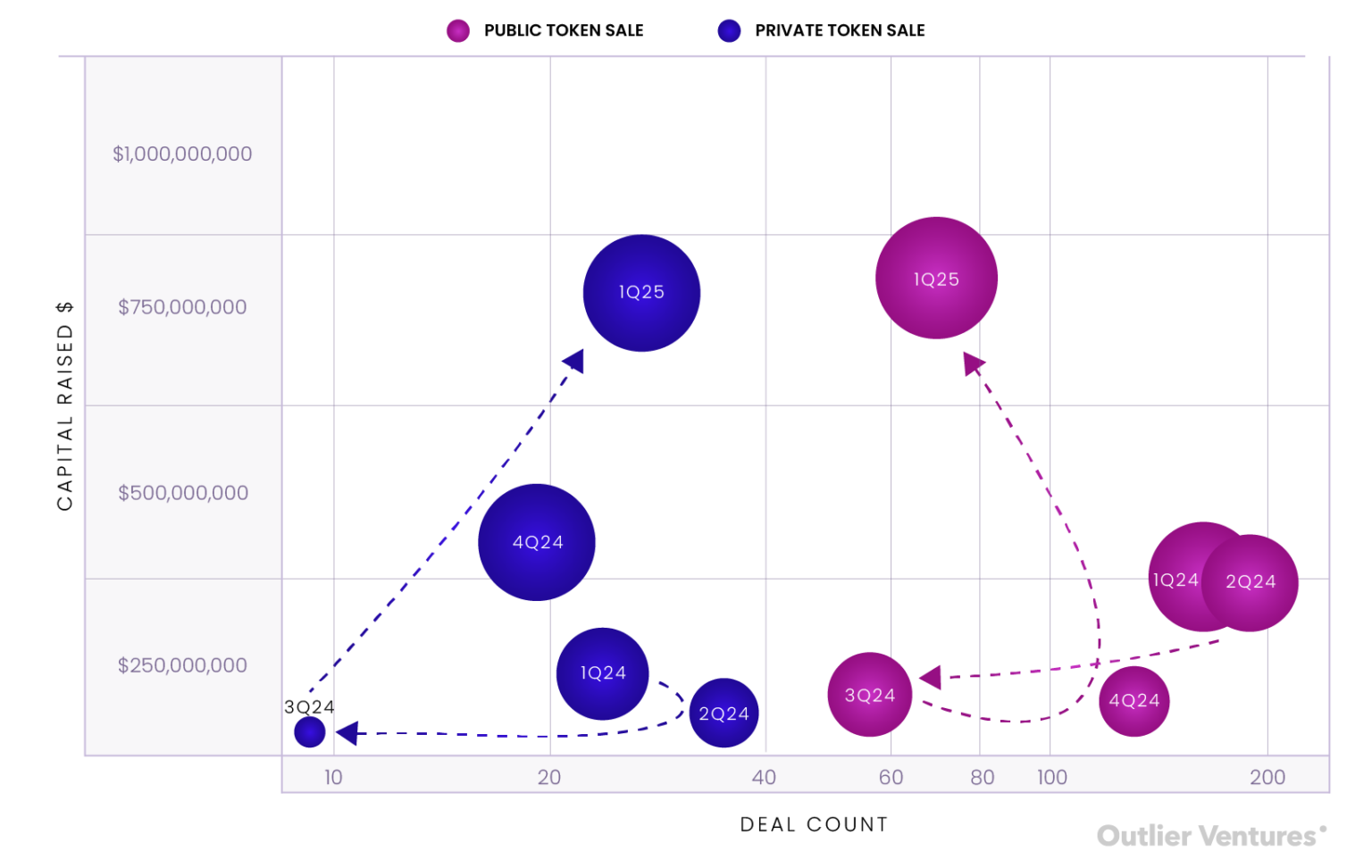

This quarter saw 69 public token sales, raising a total of $798 million, with World Liberty Financial leading with $590 million, accounting for nearly 74% of the total public token financing this quarter. Meanwhile, private token sales raised $771 million through only 27 transactions, with the TON Foundation's $400 million financing at the forefront. Overall, the total token financing in the first quarter reached $1.6 billion, far exceeding any quarter in 2024.

Figure 5: Comparison of private and public token sales by fundraising amount and transaction number from 2022 to 2024

Source: Outlier Ventures, Messari

Comparing to last year: In the first quarter of 2024, the number of transactions for public sales far exceeded private sales (163 to 24), but the overall fundraising amount was lower ($296 million to $140 million). The market at that time leaned more towards liquidity issuance, retail participation, and community-driven token economics. The first quarter of 2025, however, shows the pendulum swinging to the other side: centralized, institution-led token distribution has regained dominance—this is both a signal of rising market confidence and reflects a preference for control, lock-up mechanisms, and over-the-counter pricing.

Most notably, it is not just absolute growth but structural change: public sales now account for less than 60% of the total token financing transactions, yet they raised only slightly more than private sales—despite the number of public sales transactions being more than double that of private sales. This capital disparity per transaction reveals a market shift.

Private token transactions have regained popularity, being larger in scale, deeper, and more strategic. These transactions are no longer ordinary Initial DEX Offerings (IDOs) or hype machines for quick launches, but rather important layouts shaping ecosystems—closely tied to Layer 1 treasury, foundation missions, or cross-border capital flows.

Meanwhile, public sales appear top-heavy. Excluding World Liberty's financing, the average financing amount for the remaining 68 public rounds was only $3 million—indicating that while market access is expanding, large-scale retail demand remains concentrated in a few high-trust, high-brand projects.

Summary Thoughts: Navigating a Divergent Market

The first quarter of 2025 validated many industry insiders' feelings: this is not abear market, but a more focused market. Capital has not disappeared; rather, it has become more selective and strategic, leaning towards supporting infrastructure development, tangible outcomes, and long-term narratives.

This quarter also marked the return of a healthy dual-track dynamic: private rounds for strategic control, while public rounds build the framework for market image and liquidity. This is the first time in over a year that both private and public rounds have thrived simultaneously.

For founders, the path forward is clear: you do not need to "time the market perfectly"; you need to create those things that "are bound to happen."

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。