Ethena successfully captured arbitrage opportunities by shorting perpetual futures contracts, with protocol revenue exceeding $500,000 last week.

Author: Ethena Labs Research

Translation: Shenchao TechFlow

Summary

The perpetual futures market experienced the largest liquidation event in history last week, with a record drop in open interest.

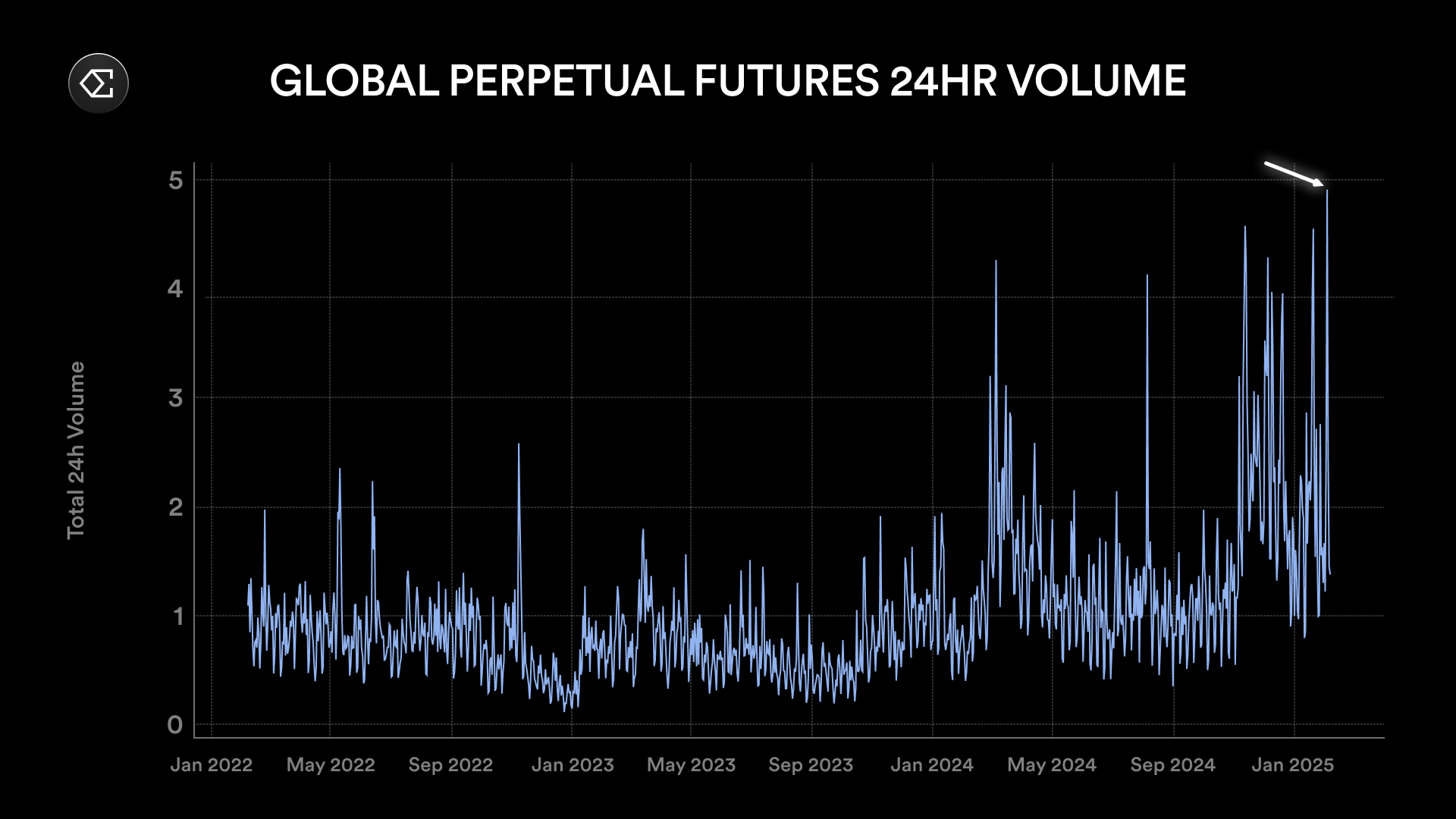

Within 24 hours, the trading volume in the perpetual futures market reached an all-time high.

Open interest decreased by approximately $14 billion, which is consistent with the estimated liquidation scale of about $10 billion.

Despite the market's extreme volatility, the USDe stablecoin remained stable, aligning with other fiat-backed stablecoins.

During the sell-off, perpetual futures contracts traded at a discount of up to 5.8% compared to the spot market.

Ethena successfully captured the discount opportunity by shorting perpetual futures contracts, with protocol revenue exceeding $500,000 last week.

Ethena automatically unwound underperforming contracts, helping to restore the funding rate to positive values while transferring over $1 billion in perpetual futures contracts to stablecoins with stable yields.

Historic Liquidation Event

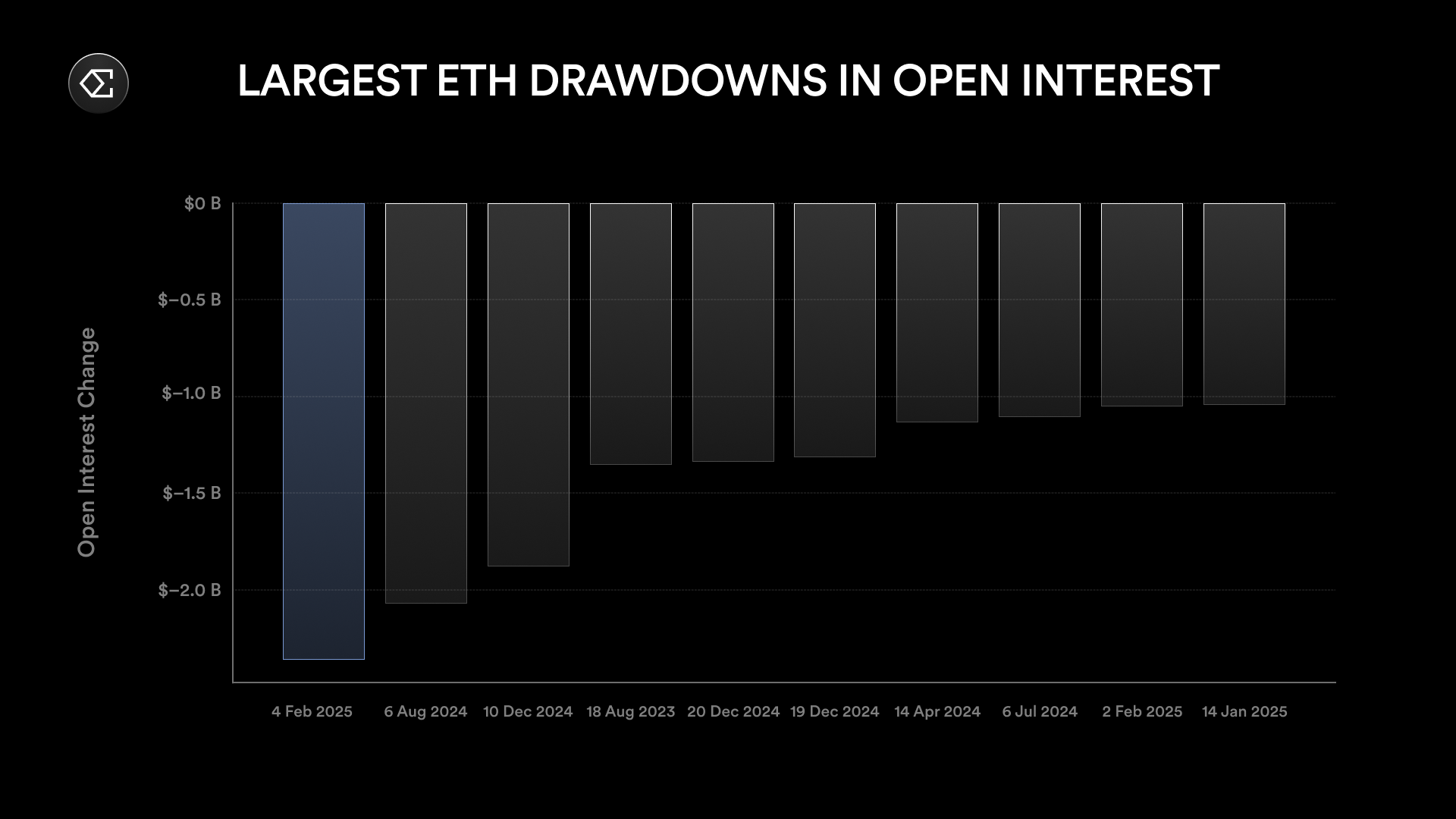

The perpetual futures market experienced the largest liquidation event in history, with the ETH market showing the most significant volatility. This marks the ninth time since Ethena's launch that ETH open interest has decreased by over $1 billion, and the second time it has dropped by over $2 billion. In just 24 hours, ETH open interest fell by $2.3 billion, setting a new record for the largest single-day drop.

Figure: 24-hour drop in ETH open interest

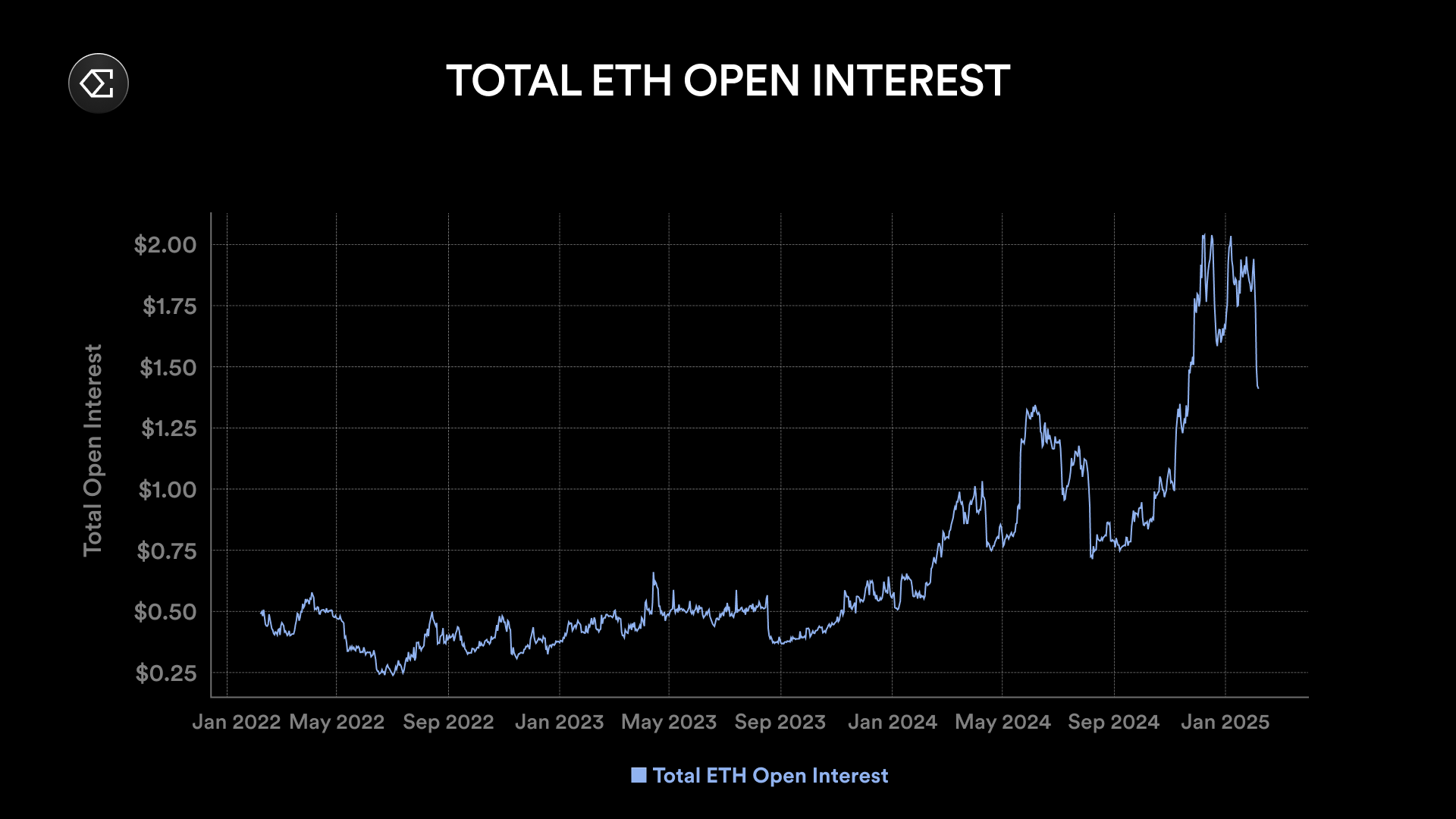

Over the past week, ETH open interest decreased by more than $5 billion, a drop of over 25%.

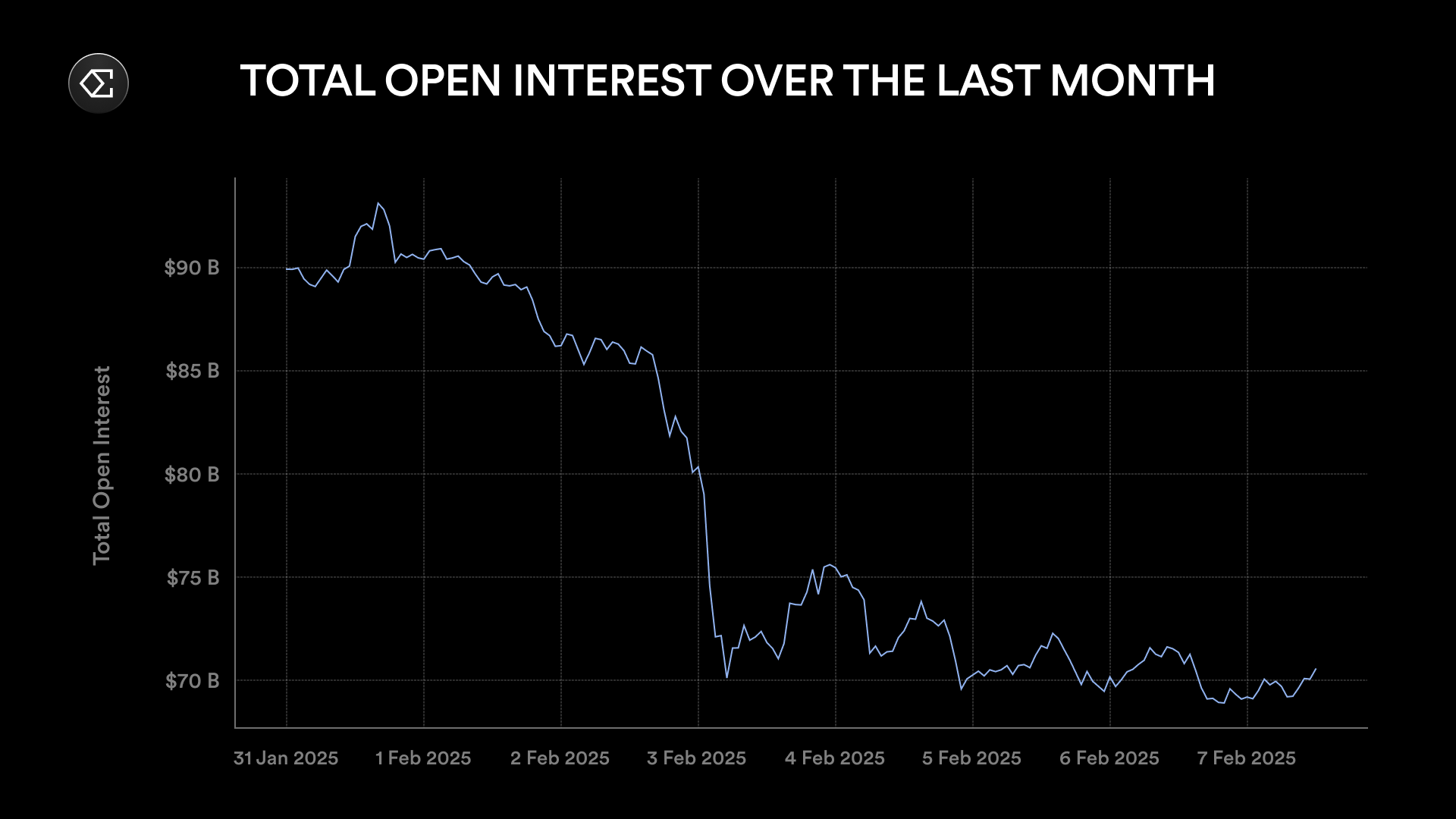

The total open interest across all assets decreased by over $20 billion in the past week. Notably, the nominal loss in BTC contracts was less than that in ETH, despite the BTC market being nearly twice the size of ETH. From February 2 to February 3, total open interest decreased by $14 billion.

This severe sell-off also led to a record high in 24-hour trading volume in the perpetual futures market.

It is difficult to accurately determine how much of this trading volume and open interest reduction was triggered by liquidations. Due to the limited amount of data pushed by APIs per second, exchanges often underestimate liquidation data, leading to underreporting by third-party data providers.

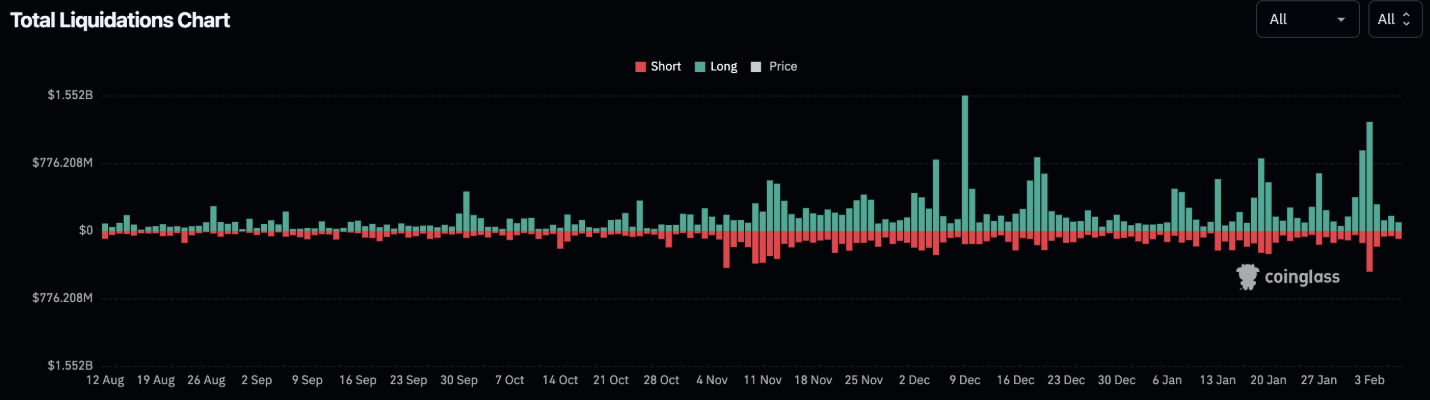

Of the approximately $14 billion in open interest cleared on February 3, it is estimated that only $2.3 billion was directly related to liquidations.

Figure: Coinglass data

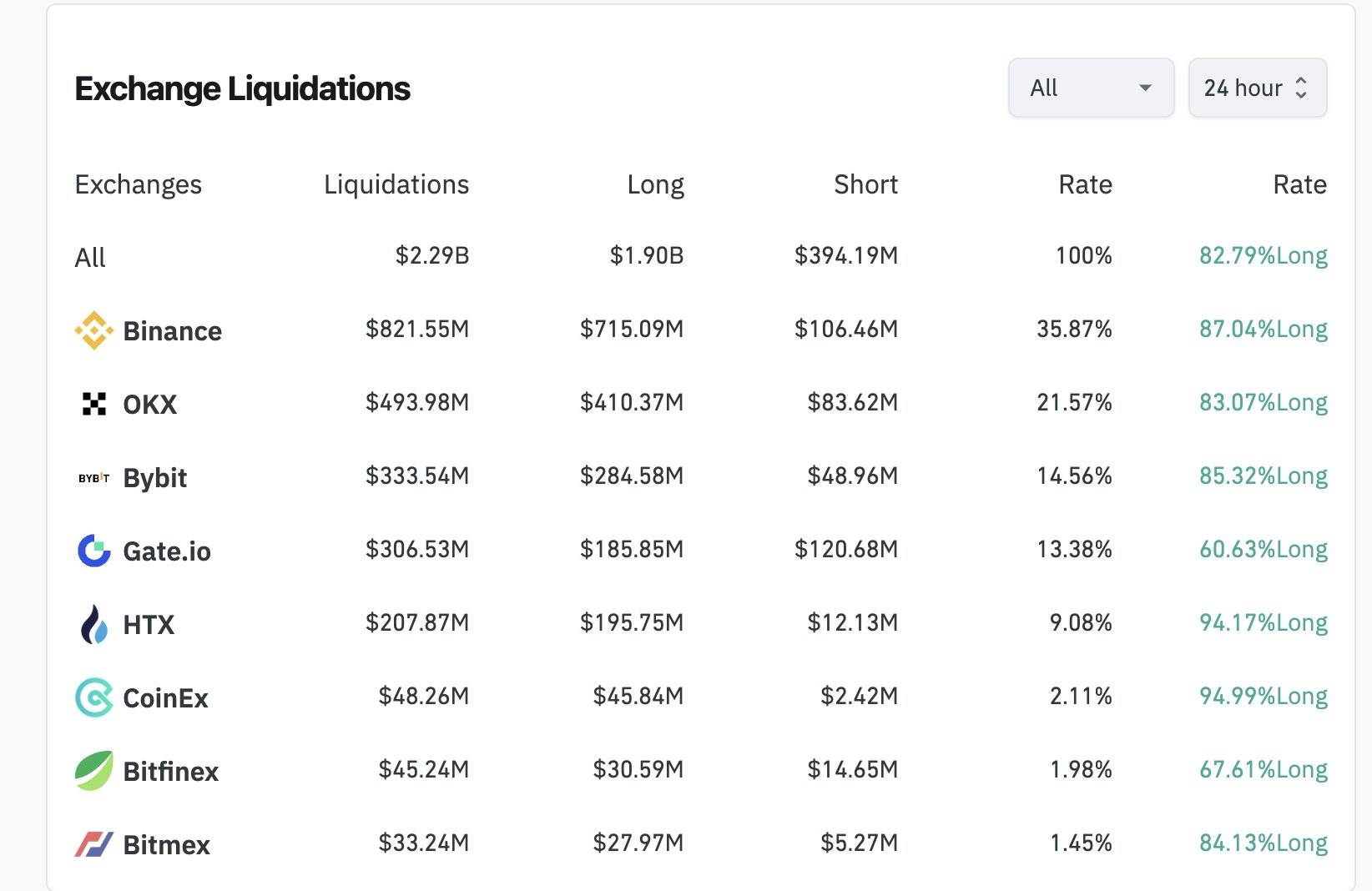

However, the founder and CEO of Bybit tweeted after the sell-off that $2.1 billion in liquidations occurred on the Bybit platform alone, while Coinglass reported only $333 million.

Figure: Coinglass data

He estimated that the total liquidation amount could be between $8 billion and $10 billion. This figure is closer to the drop in open interest across exchanges within 24 hours. For example, from February 2 to February 3, Bybit's open interest decreased by $4 billion, while Binance's decreased by $5 billion.

If this logic holds, it could be one of the largest liquidation events in cryptocurrency history. This market stress test also provided an opportunity for Ethena to further validate the stability of USDe during extreme volatility.

Resilience of USDe

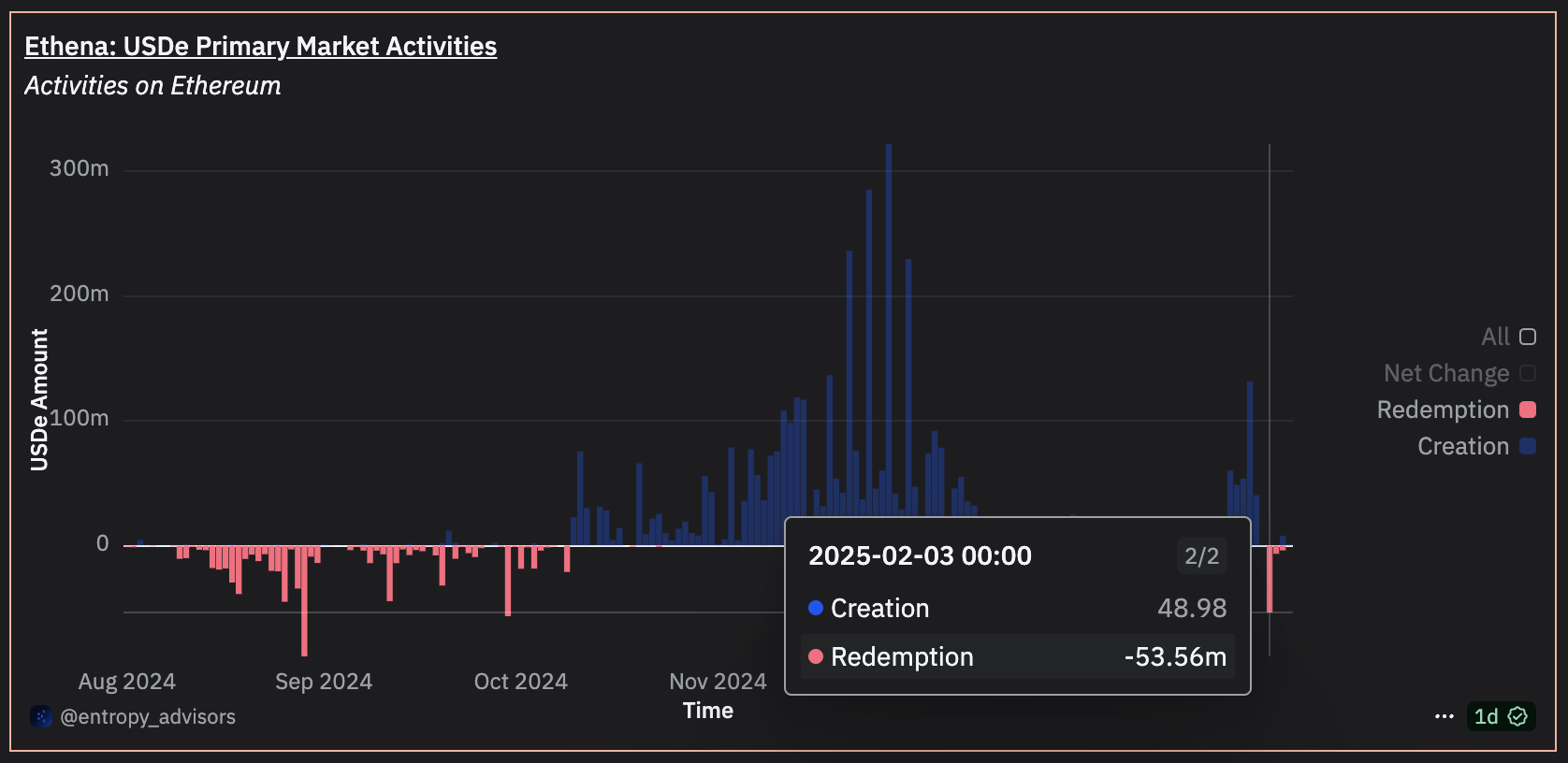

Despite being the largest nominal liquidation event in the crypto derivatives market to date, the overall market operation remained normal. The redemption process for USDe was uninterrupted, and unwinding perpetual futures contracts caused minimal losses. The trading prices of these contracts were below the spot market during the sell-off, providing Ethena with profit opportunities.

Within 24 hours, the main market completed $50 million in USDe redemptions smoothly. The secondary market saw USDe trading volume exceed $350 million, with the price difference between USDe and USDT consistently remaining within 10 basis points.

During market fluctuations, the price of USDe remained consistent with USDC and DAI. This was thanks to the intervention of market makers, who timely balanced the arbitrage opportunities between the main and secondary markets.

Figure: USDe price vs USDC (red) and DAI (purple)

In the DeFi ecosystem, sUSDe and USDe collateral (such as Aave, Morpho, Fluid, Curve, and Pendle) operated normally, with no liquidations, unwinding, or liquidity issues.

As prices fell, many perpetual futures contracts traded below the spot market, providing Ethena with opportunities to profit by unwinding perpetual futures positions.

Profit Opportunities During the Sell-off

Ethena's design has an often-overlooked advantage: **during market downturns, Ethena is typically on the "favorable" side of trades, namely *shorting* perpetual futures contracts while holding spot.** In market sell-offs, due to liquidation pressure and panic in the futures market, the prices of perpetual futures contracts often fall below their corresponding spot prices. This discount has previously exceeded 5% during past market sell-offs, and a similar situation occurred this time.

Shorting perpetual futures contracts with significant discounts can yield higher unrealized profits and provide more margin buffer for Ethena's unleveraged positions. When Ethena's system automatically unwinds these perpetual futures contracts, the protocol can benefit from the market's price imbalances, thus positioning itself more favorably in the market.

By closing those perpetual futures contracts that are significantly below the spot price, the protocol can capture discount profits and convert them into realized gains. This portion of the profit will directly benefit sUSDe holders.

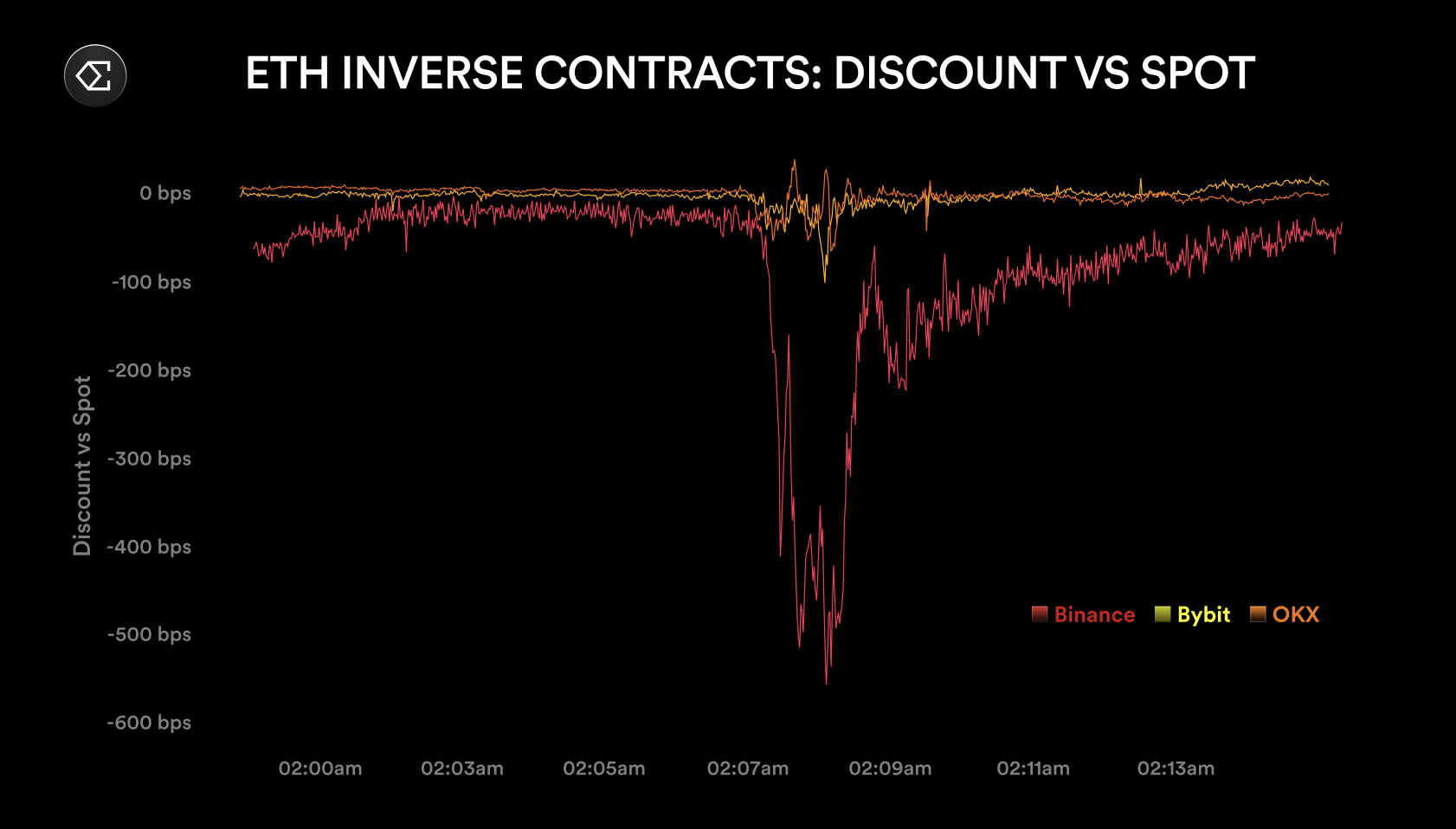

For example, during this sell-off, Binance's ETH contract (ETH coin-m) traded at a discount of -5.8% compared to the spot price (as shown in the figure below, in basis points). Ethena held approximately $200 million in short positions on this contract, and when the discount peaked, the theoretical unrealized profit exceeded $11 million—if these positions were fully closed, the protocol could have converted these profits into revenue.

Compared to Binance, Bybit and OKX's ETH contracts had smaller discount rates, close to only 1%. BTC contracts generally performed better than ETH contracts across the three exchanges, as the sell-off was primarily concentrated on ETH contracts, especially those settled in coin-based (inverse) terms.

Figure: Discount situation vs spot

Overall, Binance's perpetual futures contracts generally had higher discount rates than those of other exchanges.

Figure: Maximum discount between perpetual futures contracts and the spot market (in basis points)

The price differences between contracts and assets highlight the importance of execution quality. Ethena's automated execution mechanism can efficiently capture these market imbalance opportunities.

In the past week, the Ethena protocol generated a total revenue of $5.5 million, with over $500,000 coming from two aspects: capturing the discount between perpetual futures contracts and the spot market, and unwinding contracts with the lowest funding rates. These operations increased the annualized yield (APY) for sUSDe holders by approximately 50 basis points. Additionally, this realized profit provided extra buffer for potential negative funding cycles over the weekend.

Adapting to Lower Funding Rates

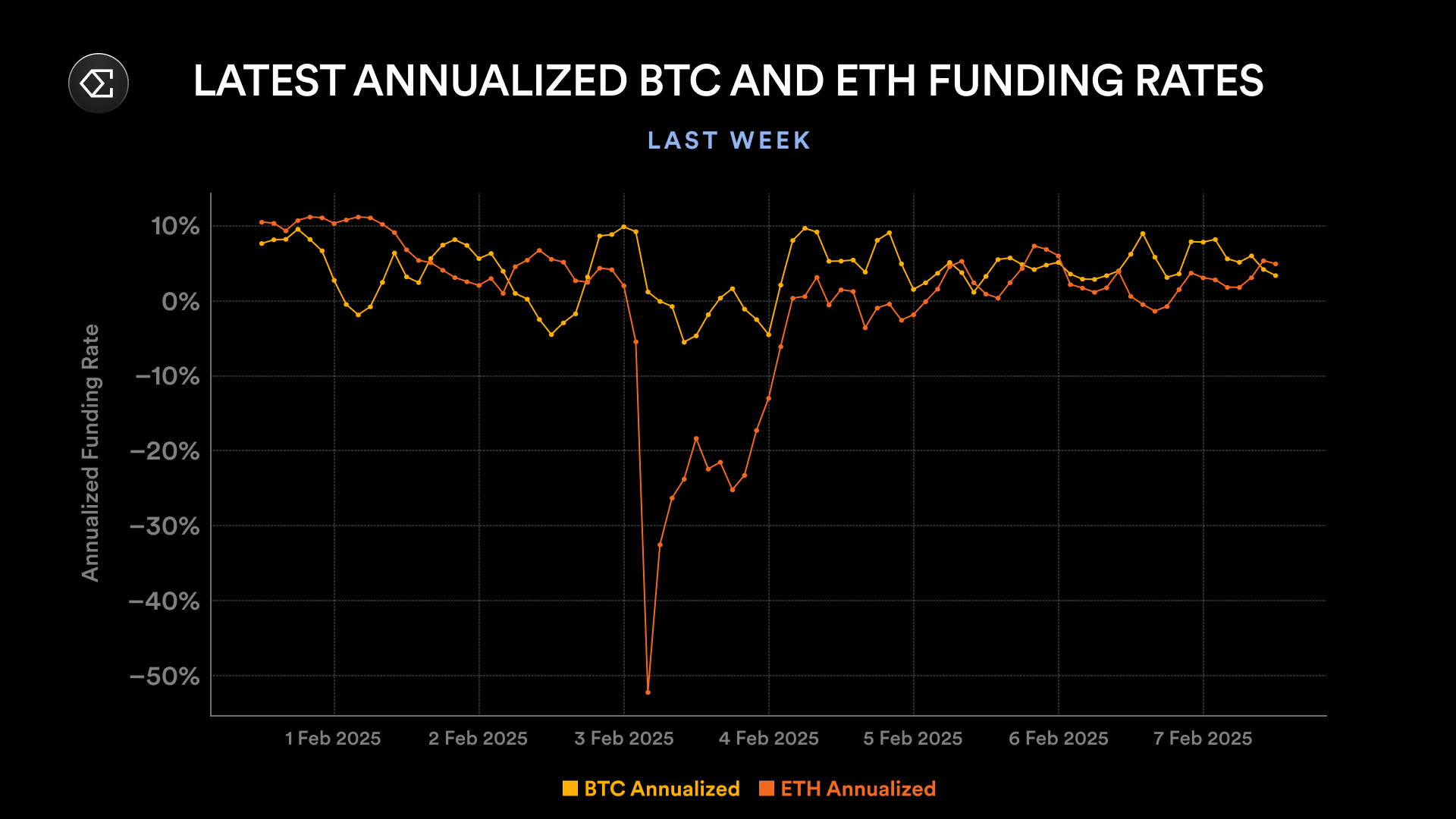

As market volatility intensified and significant differences emerged between different exchanges and assets, Ethena had to respond quickly to the structural changes in the perpetual futures market. Over the past week, the funding rate for ETH contracts was significantly lower than that for BTC contracts, with both funding rates below the levels at the beginning of the year.

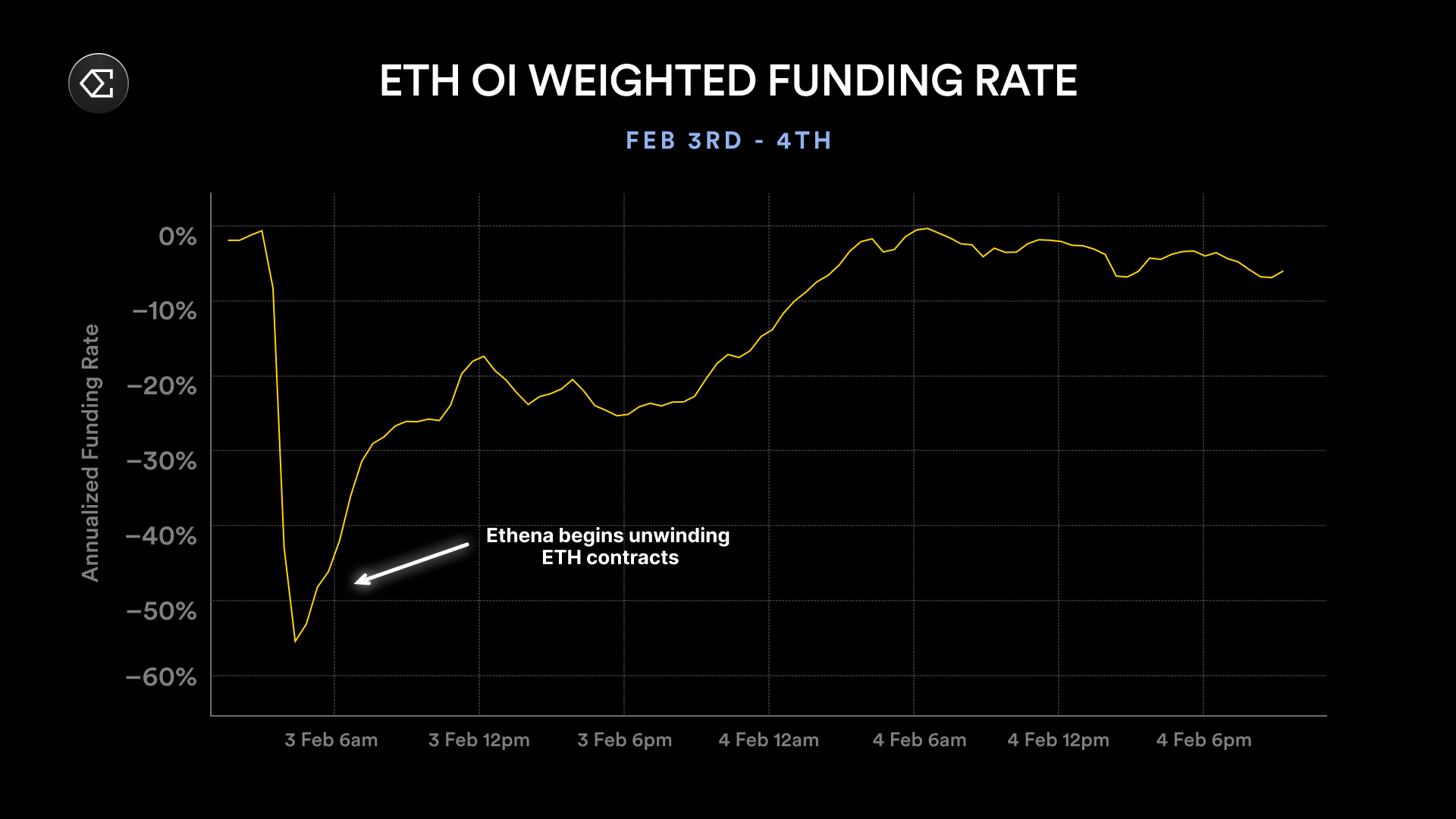

The changes in funding rates indicate that Ethena needs to adjust the asset allocation strategy for USDe. By reallocating some funds to yield-generating stablecoins (such as USDS), the protocol can achieve yields of up to 8.75%, while reducing reliance on underperforming perpetual futures contracts. As Ethena begins to unwind its short positions in ETH, the funding rates gradually improve.

Figure: Improvement in funding rates after Ethena unwinds short positions

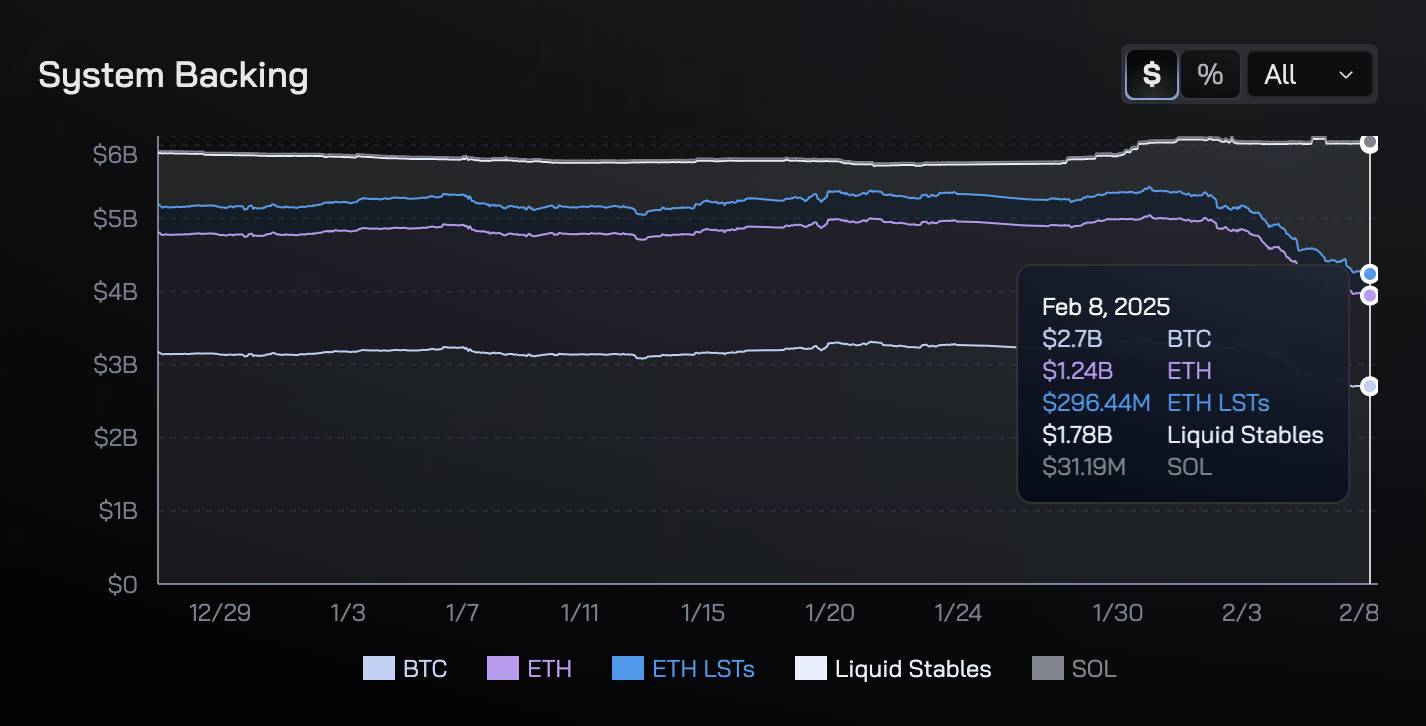

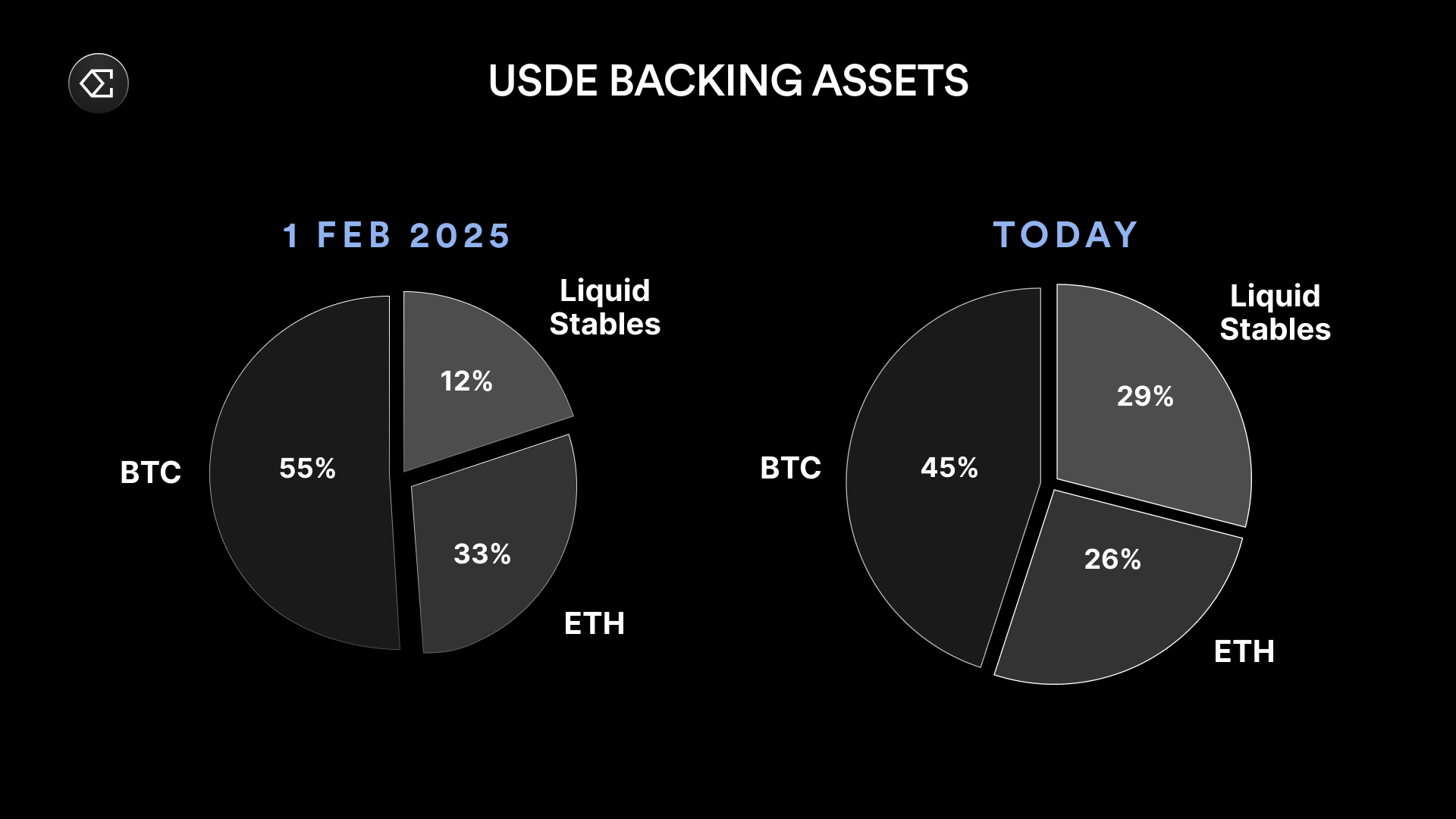

Over the past week, Ethena has demonstrated its ability to respond quickly to market changes. In a low funding rate environment, the protocol transferred $1 billion from BTC and ETH contracts to stablecoin assets, providing further assurance for the stability of sUSDe.

The following comparison chart shows the changes in the composition of USDe's supporting assets from early February to the present. USDe currently has nearly $1.8 billion in liquidity stablecoins as support, accounting for 29% of the total supporting assets. Some of these liquidity stablecoins have yields that exceed the funding rates of perpetual futures. As long as the performance of perpetual futures does not meet expectations, Ethena will continue to increase the allocation of liquidity stablecoins to optimize the structure of USDe's supporting assets.

Even in the face of the largest nominal liquidation event in history, USDe has demonstrated strong resilience, successfully processing all redemption requests while maintaining a stable peg to the target exchange rate. This performance is attributed to Ethena's ability to capture profits during market sell-offs and its structural design advantage in shorting perpetual futures. This design effectively protects the interests of sUSDe holders during market downturns.

USDe has shown outstanding resilience in every stress test, proving to be one of the most reliable assets in the current market. Ethena hopes to further earn users' trust through continued excellent performance.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。