A more detailed discussion on the composition and operational mechanism of Hyperliquid.

Author: Tranks

1. Introduction

The Decentralized Perpetual Futures Exchange is a DeFi protocol that allows users to establish leveraged positions on specific assets on the blockchain.

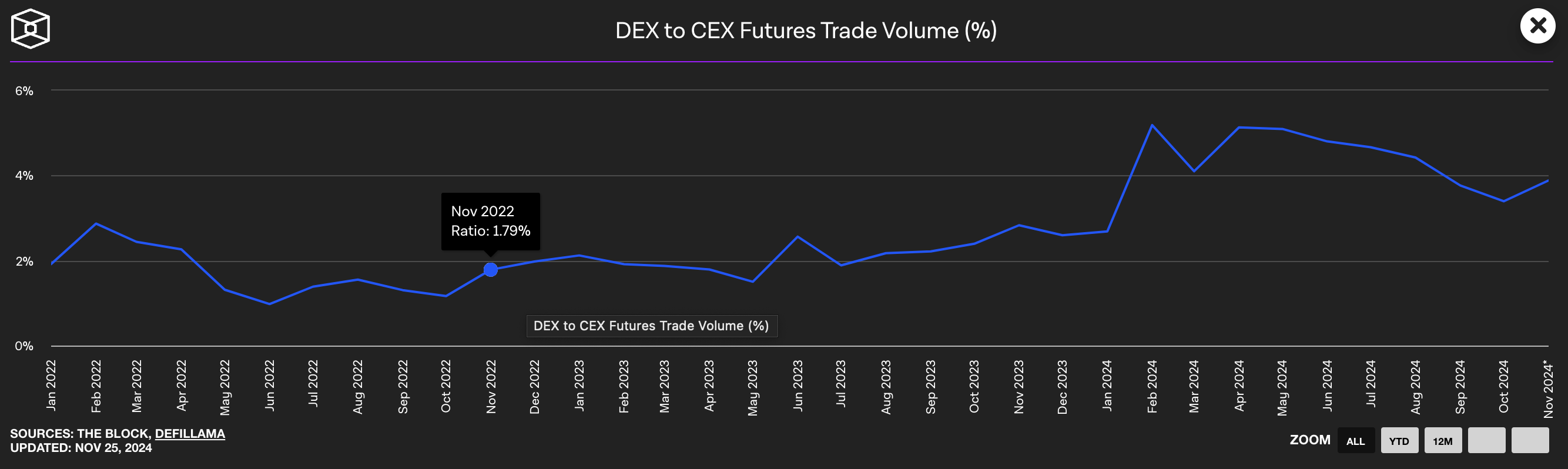

Since the collapse of FTX, the world's second-largest centralized exchange, in November 2022, decentralized exchanges have steadily developed under the market's growing distrust of centralized exchanges.

CEX vs DEX futures trading volume has been steadily increasing since November 2022; Source: The Block

Based on their price discovery mechanisms, existing PerpDEX can be roughly divided into three models:

Oracle Model: A model that operates based on external price data and does not have its own price discovery mechanism. The advantage is that, due to reliance on external oracles, the liquidity scale of the protocol has minimal impact on traders (Takers), but liquidity providers (Makers) face single-point risks and attacks from oracles, and the lack of an independent price discovery mechanism limits its development (e.g., Jupiter).

Orderbook Model: A model that utilizes the buy-sell system of traditional capital markets. Although traders can specify the desired buy/sell price, making Maker risk relatively low, the limitations of blockchain block time restrict quick trading for market makers (e.g., dYdX).

AMM Model: A model that uses CPMM (Constant Product Market Makers), which is also the price discovery mechanism of Uniswap. Prices are determined according to a specific formula (e.g., X*Y=K) based on the liquidity provided. While it can easily handle asset supply and demand without submitting or modifying an order book, all trades will involve a certain degree of slippage (e.g., Perpetual Protocol).

For detailed information on the price discovery mechanisms of PerpDEX, please refer to the "Perpetual DEX" series of articles.

1.1. Development and Limitations of Orderbook PerpDEX

In the early development stages of Perpetual DEX, Oracle and AMM models were widely adopted in the market because they more easily ensured the liquidity required for trading. However, market makers found it challenging to operate effectively due to the slow processing speed and high costs of blockchain. Most of these models faced zero-sum games, competing for limited liquidity while only targeting existing cryptocurrency market participants. Therefore, discussions and efforts to develop Orderbook-based PerpDEX have always existed to provide a familiar trading environment for traditional financial traders and achieve larger-scale growth based on their liquidity.

Recently, with the development of blockchain infrastructure such as Layer 2 and Appchains, as well as the introduction of methods for receiving off-chain orders, the trading environment for Orderbook PerpDEX has significantly improved. Additionally, the development of Orderbook PerpDEX and related infrastructure continues, with agreements such as:

Vertex Protocol: A hybrid model PerpDEX that combines AMM and Orderbook models to address the challenges of launching liquidity in Orderbook compared to other models.

Elixir: A protocol that helps anyone easily execute liquidity provision in Orderbook PerpDEX.

Despite these developments, Orderbook PerpDEX, apart from allowing users to simply "deposit" funds and create "positions" within the protocol, has no other differences from centralized exchanges. This makes them unable to avoid competition with centralized exchanges, and due to the following two factors, PerpDEX is at a disadvantage in this competition:

Orderbook PerpDEX that processes orders off-chain and records results on-chain struggles to gain user trust in terms of transparency.

Fully on-chain Orderbook PerpDEX requires users to sign and pay Gas Fees every time they submit a trade, making the trading experience quite inconvenient compared to centralized exchanges.

Therefore, the current Orderbook PerpDEX needs infrastructure that can optimize Orderbook-based trading while establishing its own ecosystem to create network effects. In this context, Hyperliquid was born with the vision of becoming a fully transparent and user-friendly "On-chain Binance."

2. Hyperliquid, the Hyperliquid Protocol

Hyperliquid is a high-performance Layer 1 optimized for Orderbook trading, capable of processing 2 million transactions per second, launched in June 2023 with the team's own capital and no external investment.

At its core, Hyperliquid is a native PerpDEX in the form of an Orderbook, with all processes from order placement to trade execution recorded on-chain. While Hyperliquid DEX records all user activities on-chain, it also provides convenient features such as creating trading accounts via email and submitting trades without requiring separate signatures or Gas Fees, offering a user experience similar to centralized exchanges.

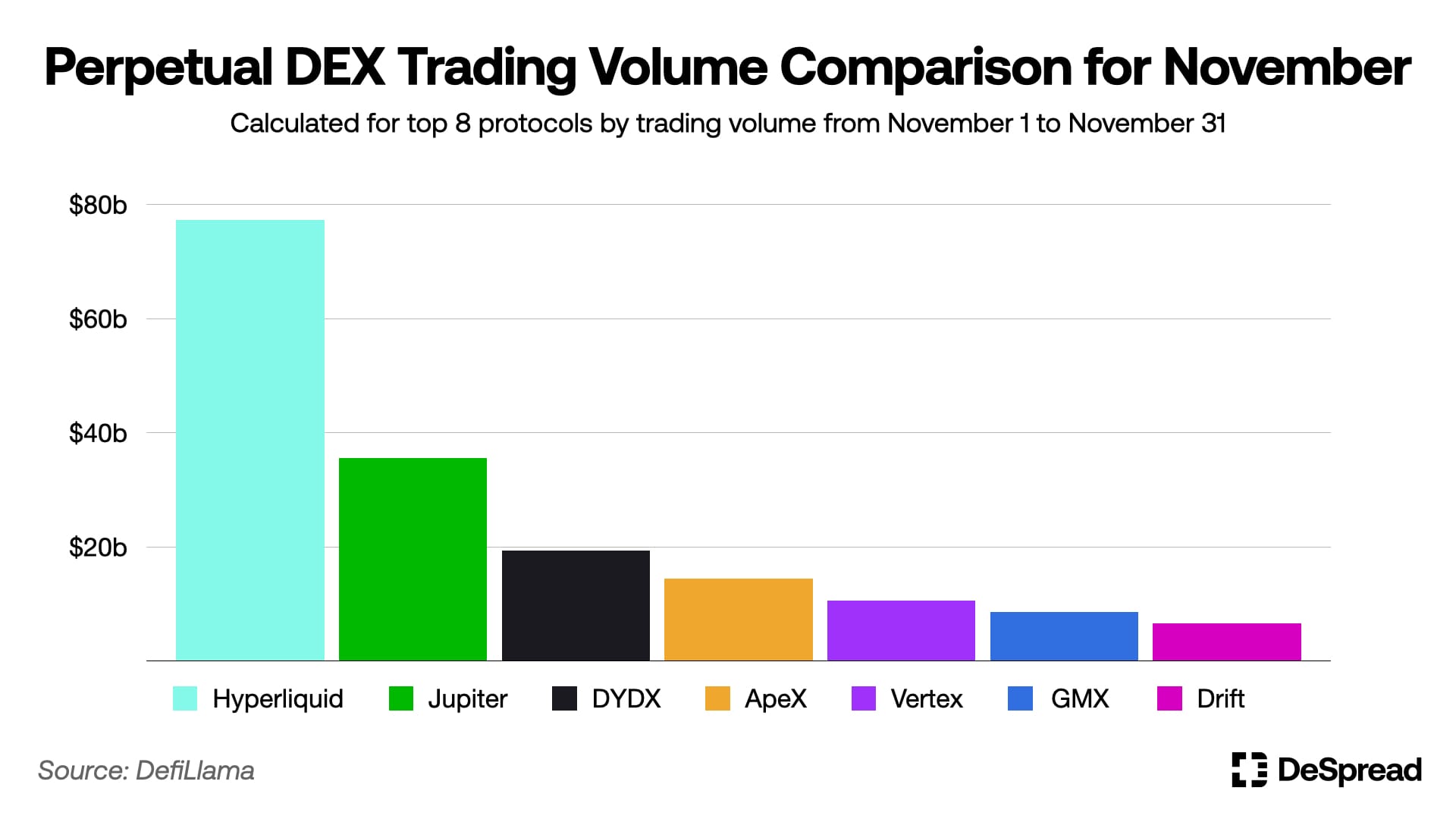

With these distinctive features, Hyperliquid has grown steadily since its launch, achieving a net inflow of $2.14 billion as of December 11, 2024, with a monthly trading volume of $77 billion. As of November, the open interest reached $3.37 billion, approximately four times that of Jupiter's open interest, ranking second in trading volume and leading significantly among Orderbook PerpDEX.

Let’s delve deeper into the composition and operational mechanism of Hyperliquid.

2.1. Hyperliquid Network

At its launch, Hyperliquid adopted the Tendermint consensus algorithm from the Cosmos ecosystem for interoperability and ease of deployment, replacing HyperBFT. However, the Tendermint consensus algorithm showed scalability limitations, processing only about 20,000 instructions per second. To address this, the Hyperliquid team developed and launched HyperBFT in May 2024, a consensus mechanism specifically designed for fast, high-volume transaction processing.

HyperBFT is a model that further optimizes the Hotstuff consensus algorithm for Hyperliquid, with Hotstuff being a more efficient improvement of the Tendermint consensus algorithm. Although HyperBFT theoretically can process 2 million transactions per second, in practical operational environments, it can handle up to 200,000 transactions due to the integration with HyperVM (an execution layer based on Rust), with latency just below a second. This is only one-eighth of the TPS of the centralized exchange Binance, but about eight times higher than Injective, which executes its Orderbook protocol on its own network.

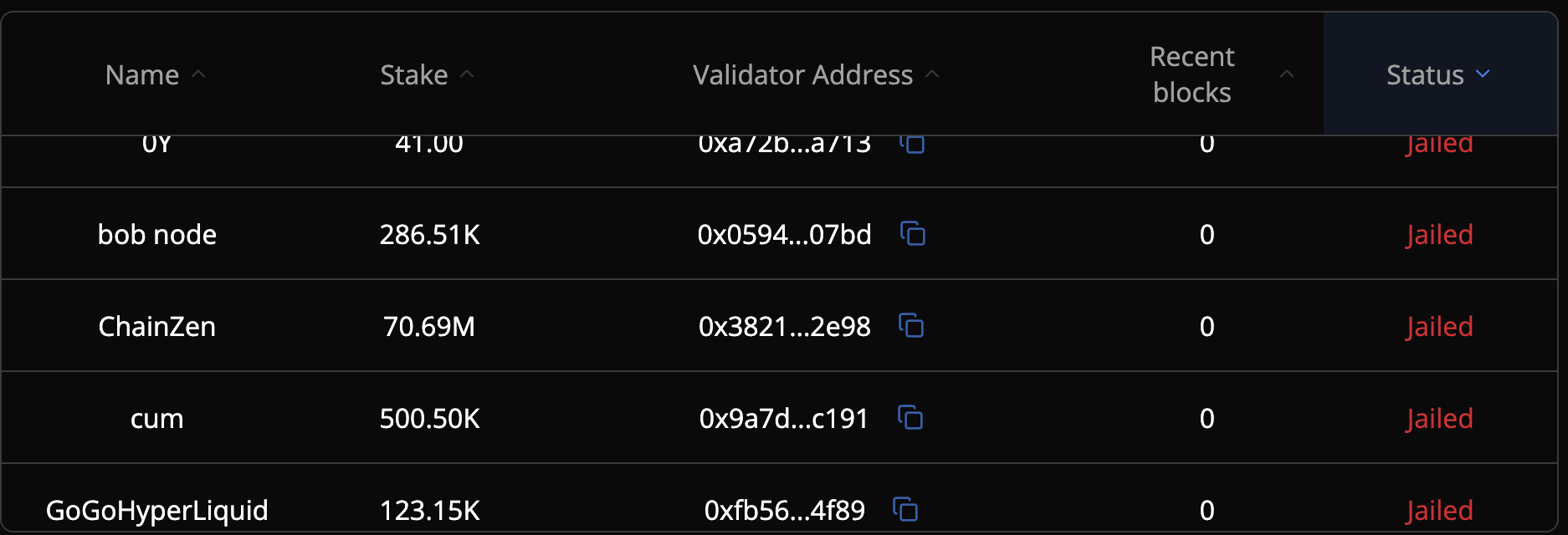

Thus, Hyperliquid is designed and built around "trading efficiency," with the advantage that all orders submitted by users are recorded and processed quickly on-chain without Gas Fees. However, without providing rewards to validators, the team currently operates all four nodes to ensure a fast order processing environment, raising external concerns about decentralization.

Recognizing this, the Hyperliquid team is testing trustless node operations to achieve validator decentralization on the test network, while also exploring how users can participate in network validation by staking $HYPE (Hyperliquid's token) even without directly operating nodes. To maintain a high-efficiency network state while ensuring decentralization, Hyperliquid has introduced a mechanism to convert nodes that cannot maintain a certain performance level into a "Jailing" state, restricting their ability to propose new blocks and participate in voting.

Nodes in Jailing state; ASXN Dashboard

Additionally, the Hyperliquid team plans to launch HyperEVM, which will work in conjunction with the existing execution layer HyperVM. This is expected to allow EVM-based applications to join the Hyperliquid ecosystem and bridge ERC-20 tokens to expand the ecosystem.

2.1.1. Hyperliquid Bridge

Users can deposit and lock stablecoins through the Hyperliquid Bridge, secured by Hyperliquid's validators, and receive the same amount of assets in their personal accounts on Hyperliquid to use the network and PerpDEX.

Currently, Hyperliquid only supports bridging USDC on the Arbitrum network. Recently, with the launch of Hyperliquid's native token $HYPE, interest in Hyperliquid has increased, and the number of users depositing assets has significantly risen, with net inflows on the Arbitrum network noticeably higher compared to other networks.

Weekly net inflows by network as of December 3; Source: Artemis

Currently, withdrawals on the Arbitrum network incur a $1 fee to cover Gas Fees. Hyperliquid plans to support various stablecoins on other networks in the future, particularly after the launch of HyperEVM, which is likely to integrate with Circle's CCTP (Cross-Chain Transfer Protocol) to ensure seamless interoperability of stablecoin transfers across different networks.

2.2. Hyperliquid DEX

As mentioned earlier, Hyperliquid DEX operates on the Hyperliquid network, offering fast transaction processing without the need for signatures and fees, providing a user experience almost identical to centralized exchanges, and supporting leveraged trading environments for over 100 different token pairs.

Hyperliquid DEX offers the following four types of orders:

Market Order: Executes a trade immediately at the current market price.

Limit Order: Executes a trade at a specified desired price.

Scale Order: Establishes and executes multiple limit orders within a set price range.

TWAP: Splits a single order into multiple orders executed at fixed time intervals.

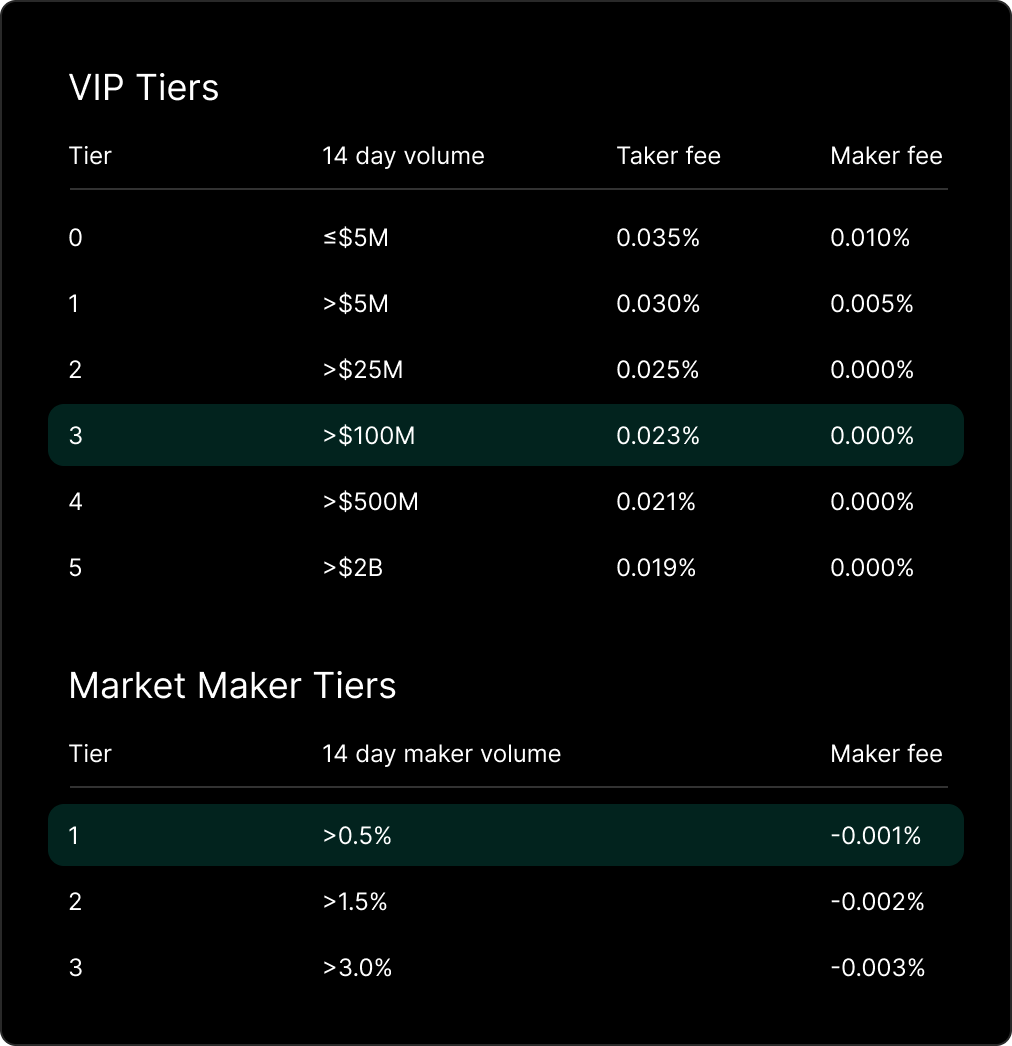

Hyperliquid implemented a free trading policy for the first three months after the mainnet launch to attract early users, after which a fee policy will be introduced, charging Takers a fee of 0.25% and providing Makers with a 0.2% rebate. However, starting in March 2024, they switched to a tiered fee mechanism based on the trading volume of each wallet over a 14-day period, restructuring the system so that only market makers meeting specific trading volume thresholds can receive rebates.

Hyperliquid fee structure; Hyperliquid Docs

The fee revenue generated in Hyperliquid is not collected by the team but is distributed to users who deposit liquidity into the HLP Vault (Hyperliquid Liquidity Provider Repository) and to a support fund, which will be detailed further below.

2.2.1. Mark Price Mechanism

Since Hyperliquid is based on an Orderbook, the buy/sell prices for users are essentially determined by the liquidity of the Orderbook. However, when the liquidity of the Orderbook is insufficient, price discrepancies with other markets can occur, potentially leading to small-scale liquidity attacks that can trigger liquidations, TP (Take Profit), and SL (Stop Loss) events.

Additionally, due to the nature of perpetual futures trading with no expiration date, to control the deviation of prices from spot prices, holders must pay a certain amount to the opposing position holders at each specific time interval (Hyperliquid's is one hour) as a funding rate. Therefore, Hyperliquid calculates the Mark Price based on external exchange price data for liquidation, TP/SL, and funding rate calculations. The standards for calculating Mark Price in Hyperliquid are as follows:

Binance: 27.27

OKX: 18.18

Bybit: 18.18%

Kraken: 9.09%

Kucoin: 9.09

Gate IO: 9.09

MEXC: 9.09

2.2.2. Derivatives and Spot Trading

In addition to futures trading for specific tokens, Hyperliquid DEX also offers the following types of tool trading:

Index Perpetual Contracts: Provides perpetual futures trading for various blockchain ecosystem indices, such as an index tracking the average floor price of specific blue-chip NFT collections (NFTI-USD) and an index tracking the average Key price of the middle 8 accounts among the top 20 influencers on the blockchain social platform Friend Tech (FRIEND-USD).

Hyperps: A product that supports pre-trading of tokens not yet launched in the market, using the weighted moving average (EWMA) of the previous day's minute-by-minute prices over an 8-hour period to determine prices, rather than relying on specific prices.

Spot: Native tokens issued on the Hyperliquid network.

Recently, Hyperliquid has been investing significant effort in building and expanding its ecosystem centered around its native token and spot trading. The native token of Hyperliquid will continue to evolve through HIP (Hyperliquid Improvement Proposals).

HIP-1: Proposal for the issuance standard of Hyperliquid's native token, including token standard formats and a Dutch Auction system with a 31-hour cycle to curb the disorderly issuance of tokens. This proposal also includes a Spot Dust feature that automatically submits sell orders to the Orderbook for tokens held in user wallets valued at less than $1 once a day.

HIP-2: Proposal for an automatic liquidity provision solution for issued native tokens. This solution submits buy/sell orders to the Orderbook every 3 seconds at ±0.3% of the current price, and token issuers must choose whether to implement the liquidity provision solution and deposit the required liquidity when issuing tokens.

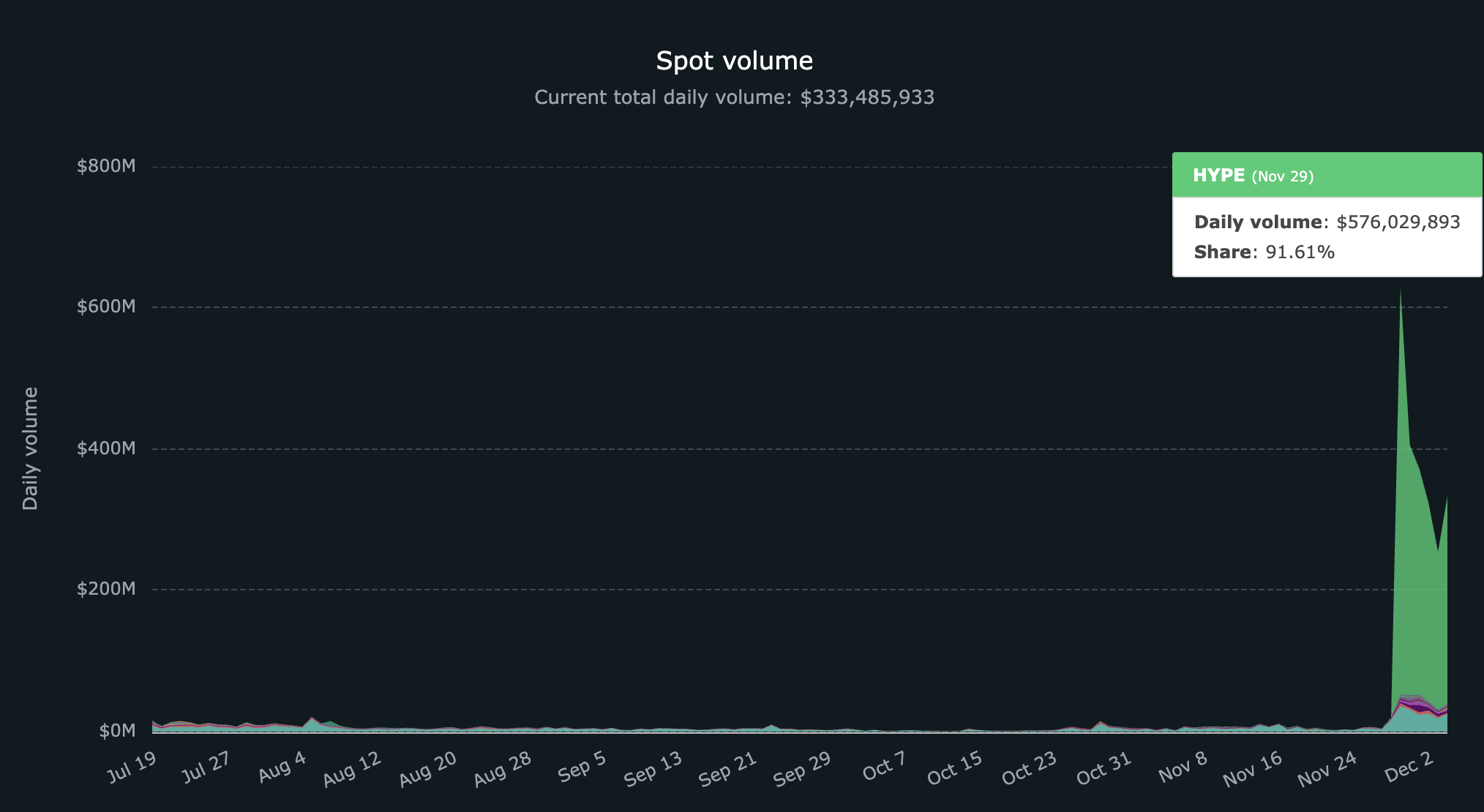

As of December 4, 2024, there are 53 types of alternative tokens traded on Hyperliquid DEX through the HIP standard, including the mainnet token $HYPE. After the launch of $HYPE, spot trading volume has significantly increased, reaching a daily trading volume of $628 million. With the increase in the number of issued tokens and the emergence of more dApps that can utilize these tokens, Hyperliquid's spot trading volume is expected to grow further. Currently, Hyperliquid's daily spot trading volume remains at $333 million, slightly decreasing after the issuance of $HYPE.

Hyperliquid native token trading volume trend; Source: Purrburn

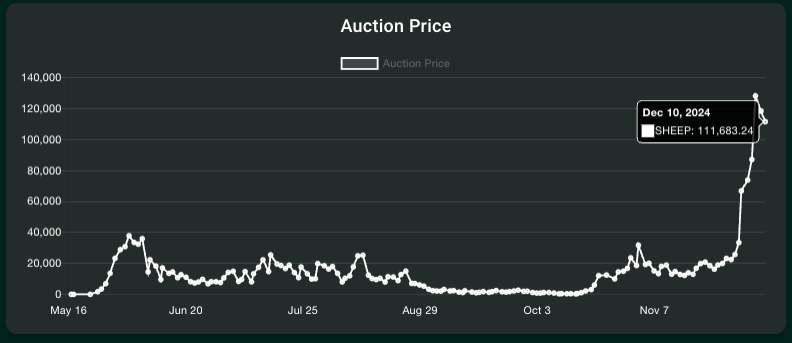

Additionally, as external liquidity flows into the Hyperliquid ecosystem and spot trading becomes more active after the issuance of $HYPE, the winning prices for token auctions launched through HIP-1 have also shown an upward trend.

Ticker auction winning price trend; Source: Hypurrscan

2.2.3. HLP and User Repository

In existing Orderbook exchanges, liquidity providers must continuously monitor and submit and modify buy/sell orders based on the situation, which also means relying on a few professional market makers to provide liquidity, leading to these market makers monopolizing the profits generated from liquidity provision.

In contrast, Hyperliquid offers a feature where users can participate in market making and earn profits simply by depositing assets into the HLP Vault (Hyperliquid Liquidity Provider Vault), with the HLP Vault directly managed by the team to provide liquidity to the Hyperliquid Orderbook. As mentioned earlier, most of Hyperliquid's revenue is distributed to users who deposit liquidity into the HLP.

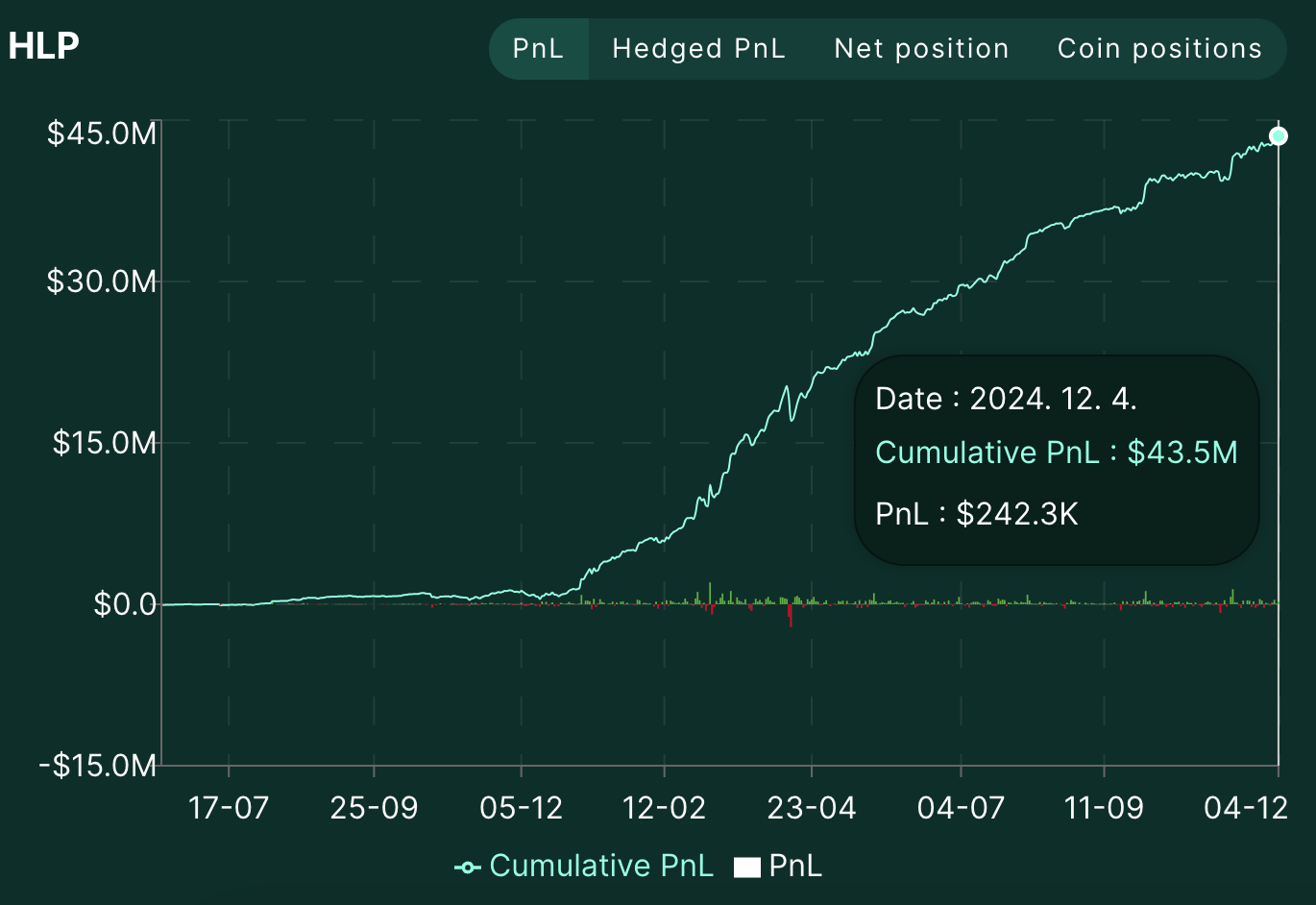

The HLP Vault consists of three strategies: Strategy A, Strategy B, and the Liquidator Strategy. The Liquidator Strategy operates by taking over positions when the maintenance margin of the liquidation target falls below 2/3, while the specific operational mechanisms of the other two strategies are not disclosed to prevent exposure of operational details. However, since the order submission history and balance status of each strategy are recorded on the Hyperliquid network, they can be transparently checked through the HLP Dashboard.

As of December 4, 2024, the total assets deposited in the HLP Vault amounted to $168 million, with cumulative profits of $43 million, and the annual interest rate recorded in November was approximately 20%.

HLP vault PNL trend; Source: Stats.hyperliquid

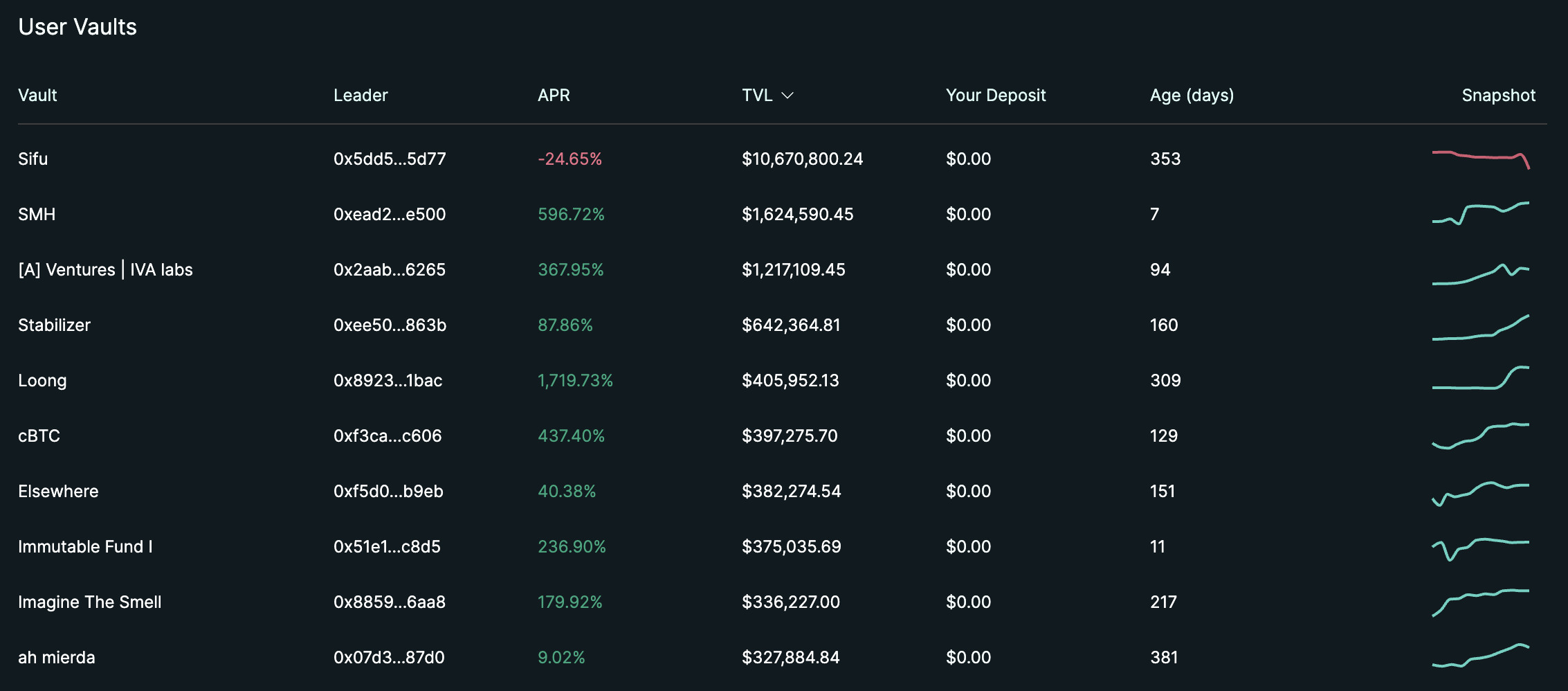

Additionally, Hyperliquid provides a user vault feature outside of HLP, allowing anyone to create a vault, execute trading strategies similar to HLP, and also accept user deposits for operation. Vault operators can charge a fee of 10% from the profits generated from operations and must maintain their own asset ratio in the vault at 5% or higher to align with the interests of depositors.

User vault list; Source: Hyperliquid

2.3. $HYPE

Since the closed testing launch in November 2022 until September 2024, Hyperliquid has allocated Hyperliquid points to users based on the following criteria:

Closed Testing & First Quarter (2022.1~2024.4): Points distributed based on Perp trading volume.

Second Quarter (2024.6~2024.10): Points distributed based on participation in the ecosystem (such as Layer 1 and spot trading).

Retroactive distribution of points for trading in May, October, and November 2024.

After the end of the second quarter, on October 15, 2024, Hyperliquid established a foundation and announced the issuance and airdrop of the network token $HYPE. On November 29, $HYPE tokens equivalent to approximately 31% of the total supply and 83% of the initial circulating supply were distributed to users who mined Hyperliquid points.

The utility of $HYPE announced by the foundation is as follows:

To be used as the security budget for HyperBFT through future $HYPE staking (currently being tested on the test network).

To be used as a network fee token on the upcoming HyperEVM.

Approximately 40% of the total supply will be used for future community rewards and ecosystem grants.

After the token airdrop, $HYPE was listed on the HYPE/USDC spot trading pair on Hyperliquid, with an initial price of $2. In the first 7 days after listing, the price increased by about 7 times and maintained an upward trend even during the correction phase.

$HYPE price trend; Source: Hyperliquid

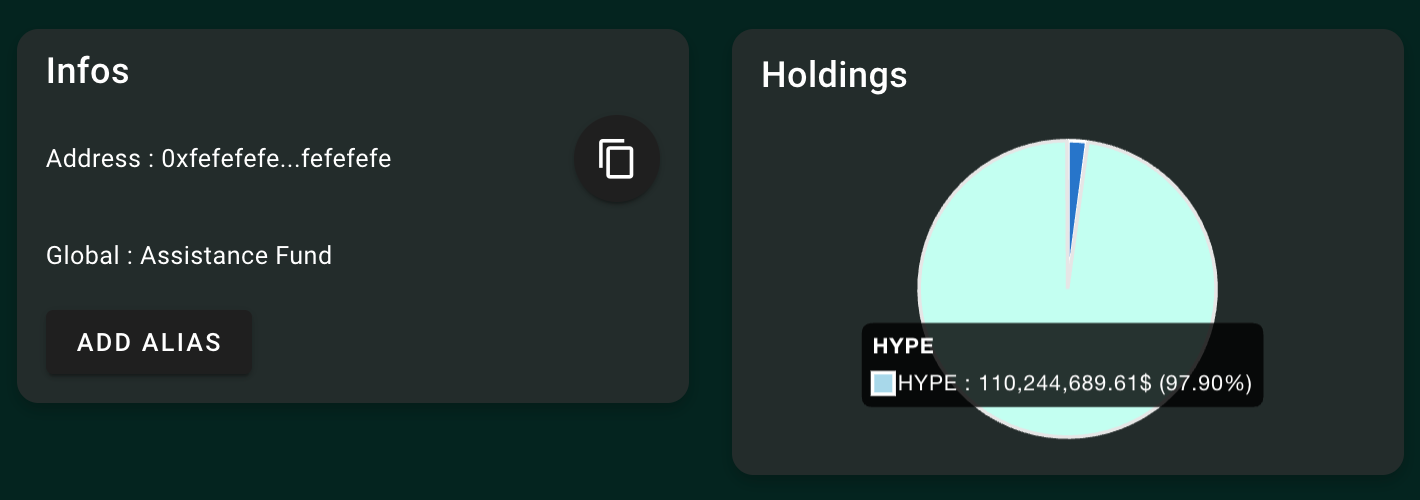

Factors driving the rise of $HYPE include: 1) The establishment of a solid community that shares the agenda of the Hyperliquid exchange centered around the team; 2) The absence of institutional investors for large-scale sell-offs without external funding; 3) Continuous $HYPE buybacks using fees accumulated in the Hyperliquid assistance fund wallet.

Amount of $HYPE held by Hyperliquid assistance fund wallet; Source: Hypurrscan

3. Hyperliquid Ecosystem

Most Orderbook-based PerpDEX either lack their own networks or focus solely on "trading" functions, making it difficult to form a subordinate ecosystem that generates synergies with PerpDEX. In contrast, Hyperliquid, as a Layer 1 network, is not limited to PerpDEX but aims to build a vast ecosystem that combines existing on-chain users with centralized exchange users, creating network effects unattainable by PerpDEX through the listing of various dApps, the issuance of native tokens through HIP, and the introduction of HyperEVM.

3.1. $PURR

$PURR is Hyperliquid's first native token and meme coin, issued on April 16, 2024, with the launch of HIP-1.

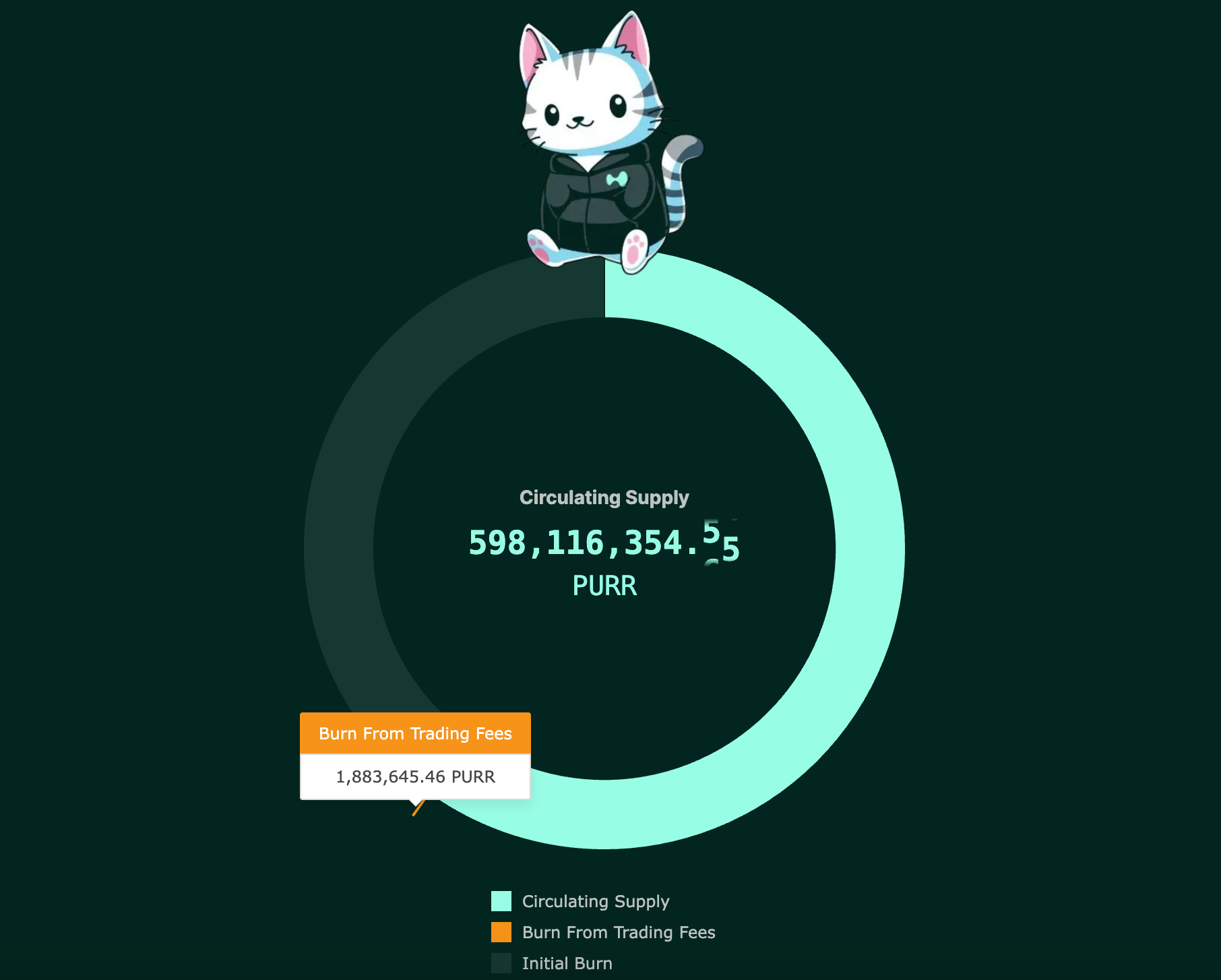

At the time of issuance, 50% of the total circulating supply was proportionally distributed to Hyperliquid users' Hyperliquid points, while the remaining 50% was originally intended for providing liquidity to the PURR/USDC spot pair according to HIP-2. However, due to community feedback during the testing period indicating that too much liquidity had already been provided, the team decided to burn 80% of the liquidity supply allocation. Additionally, a burn mechanism using a portion of the trading fees was introduced, leading to continuous burns, with a total of $401.8 million in PURR burned to date, including the initial burn amount.

$PURR circulation status; Source: purrburn.fun

After the issuance of $PURR, a trend emerged among other native tokens to provide airdrops to $PURR holders, coupled with rumors of Hyperliquid points being allocated to $PURR holders, resulting in a price increase of approximately 166% within three days of issuance. Recently, with the announcement of $HYPE's launch and external liquidity flowing into Hyperliquid, $PURR has also seen significant gains, maintaining a market cap of $176 million, ranking second after $HYPE.

3.2. Hypurr Fun($HFUN)

Hypurr Fun is a Telegram bot that helps users trade on Hyperliquid through Telegram and has recently launched and operated Hypurr Pump, a meme coin issuance platform.

Hypurrfun Dashboard; Source: hypurr.fun

Users can easily create and close positions on Hyperliquid through the Telegram bot, participate in meme coin financing on Hypurr Pump, and meme coin projects that raise over $100,000 in financing can participate in Hyperliquid's stock auctions, issuing their own meme coins based on the financing situation.

The core of the project is $HFUN, the second native token issued on Hyperliquid after $PURR, which is structured to burn $HFUN using platform revenue generated through Hypurr Fun and Hypurr Pump.

3.3. HyperLend

HyperLend is a lending protocol designed specifically for the Hyperliquid ecosystem, expected to launch alongside HyperEVM, currently operating only on the HyperEVM test network.

The features that HyperLend is preparing include:

Leveraged yield farming: Providing leveraged yield farming positions using $stHYPE, which is the liquid staking token for $HYPE that Thunderhead plans to issue in the future.

HLP collateral loans: Offering loan services using funds deposited in HLP as collateral.

Vault Share token issuance: Issuing tokens that can secure funds stored in the vault and providing collateralized loans for these tokens.

One-click cross-chain loans: Bridging functionality for various Layer 2 network assets, using these assets as collateral for HyperLend.

HyperLend provides these features to tokenize various locked liquidity on Hyperliquid and offer loan services using them as collateral, which is expected to diversify yield farming pathways within the Hyperliquid ecosystem and enhance liquidity.

Additionally, the Hyperliquid ecosystem includes various protocols that are ongoing or preparing to join from other networks, such as Abracadabra (which offers lending and leverage based on the stablecoin $MIM), Rage Trade (a multi-chain perpetual aggregator), and Solv Protocol (a Bitcoin pricing protocol). The activation of these protocols and the issuance of native tokens are expected to help increase trading volume on Hyperliquid DEX.

4. Conclusion

While other PerpDEXs struggle to simultaneously meet user trading experiences and liquidity issues, Hyperliquid has achieved a fast, orderbook-based on-chain PerpDEX that does not require user signatures or gas fees, maintaining a good user experience. Furthermore, with the launch of $HYPE as a turning point, Hyperliquid has garnered significant market attention and demonstrated unprecedented rapid growth among other PerpDEXs.

In particular, the spot token issuance mechanism introduced through HIP-1 serves as a platform for token issuance, similar to Pump.fun on Solana, Clanker on Base, and Virtual Protocol, greatly facilitating the recent increase in network usage. Hyperliquid aims to become a community centered around the team.

Moreover, Hyperliquid aims to become a Layer 1 protocol by integrating other protocols, forming an ecosystem beyond spot and futures trading functionalities. In doing so, Hyperliquid has established its leadership position and gained the expectation of attracting centralized exchange users, who have been difficult to engage with existing blockchain projects, into the on-chain environment, merging them with existing on-chain users.

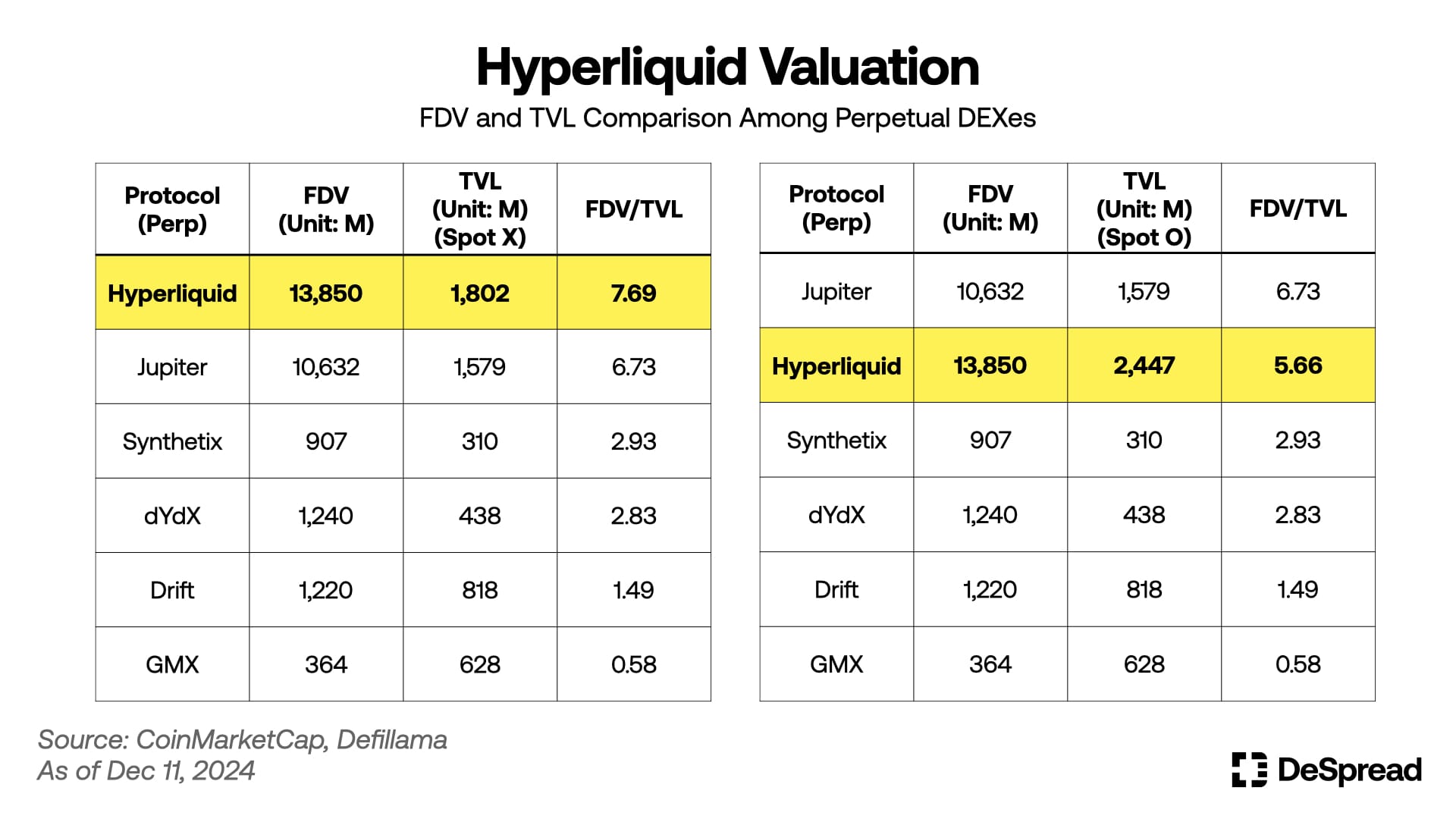

As mentioned in our “Market Commentary | 12.06”, there are opinions suggesting that the value of Hyperliquid's token may be somewhat overvalued due to its rapid growth post-token issuance. However, considering that the article did not include the value of other tokens within the Hyperliquid ecosystem (mainly tokens in the spot market), there is room to refute the argument of overvaluation. As shown in the above chart, when including the value of spot market tokens in the TVL, the FDV/TVL ratio is 5.66, which is still in the undervalued range compared to Jupiter.

This valuation assessment can also be applied among Layer 1 projects, with a simple comparison as follows (valuations based on DeFiLlama):

Hyperliquid($HYPE)

FDV: $13.85B / TVL: $2.45B

FDV/TVL: 5.66

Sui($SUI)

FDV: $37B / TVL: $2.74B

FDV/TVL: 13.5

Aptos($APT)

FDV: $13.1B / TVL: $2.48B

FDV/TVL: 5.28

Avalanche($AVAX)

FDV: $31.8B / TVL: $2.57B

FDV/TVL: 12.37

As these comparisons show, Hyperliquid appears to be in the undervalued range compared to Layer 1 projects with similar TVL metrics. Considering this, we believe that with the launch of HyperEVM and the expansion of the Layer 1 ecosystem, Hyperliquid's value has the potential to receive a higher valuation.

However, for Hyperliquid to realize their vision and enhance project value, they must successfully launch $HYPE staking and achieve decentralization of validators while introducing HyperEVM without compromising existing network performance, subsequently forming an organic ecosystem centered around the community. Therefore, we should closely monitor the subsequent developments of the protocol to assess whether they can prove the proposed vision.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。