Author: Alvis, MarsBit

OG Tokens in the DeFi Field Seem to Have Died?

This was the focus of discussion during the remarkable cryptocurrency market black swan event on August 5th. The global market was shrouded in recessionary panic, followed by a spectacular crash, and the cryptocurrency market suffered a severe deleveraging impact. However, in this stress test, the DeFi sector, as the pillar of liquidity, did not show severe disconnection or credit risk, but instead demonstrated a stronger ability to withstand pressure than ever before.

Does this mean that the turning point for DeFi has arrived? Let's take another look at this phenomenon.

Token Performance

Data sourced from CoinGecko

Despite Bitcoin reaching a historic high in March, we can see that most DeFi tokens have significantly underperformed BTC, and even lagged behind ETH. The DeFi Pulse Index (DPI) has declined relative to ETH for three consecutive years. During this period, ETH's performance itself also lagged behind BTC. DPI includes DeFi-related tokens such as UNI, MKR, LDO, AAVE, SNX, and PENDLE.

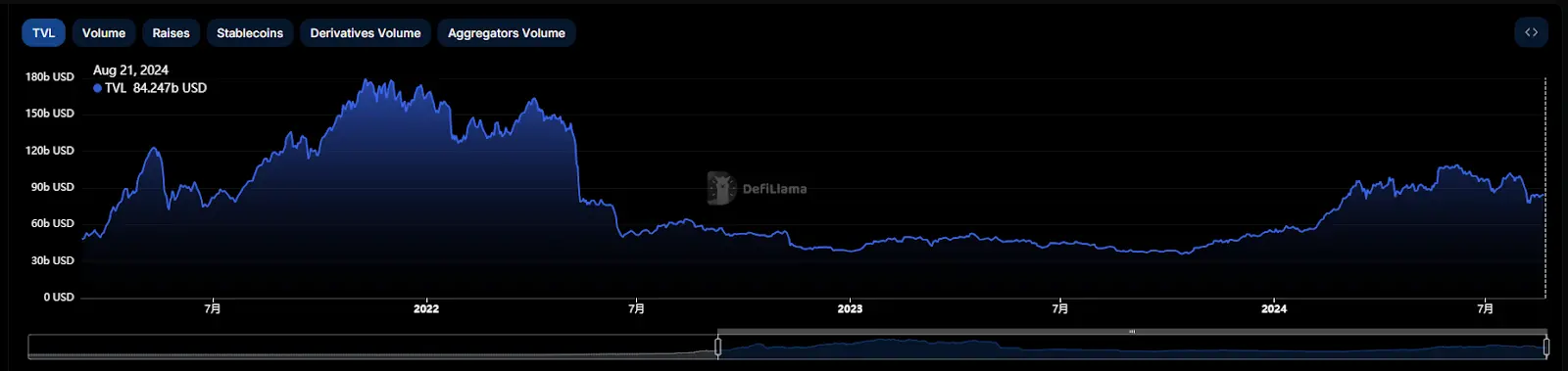

Total Value Locked (TVL)

Data sourced from DeFiLlama

As of August 21, 2024, the total value locked (TVL) in multi-chain DeFi has dropped to $8.46 billion. This figure has decreased by 54.7% from the historical peak of $18.68 billion in December 2021, only 61% higher than the level after the market turmoil caused by the Luna event. This significant downward trend can be partly attributed to the widespread reduction in asset integration, such as wrapped assets of Ethereum and Bitcoin, and the compression of capital outflows has also contributed to this downward trend.

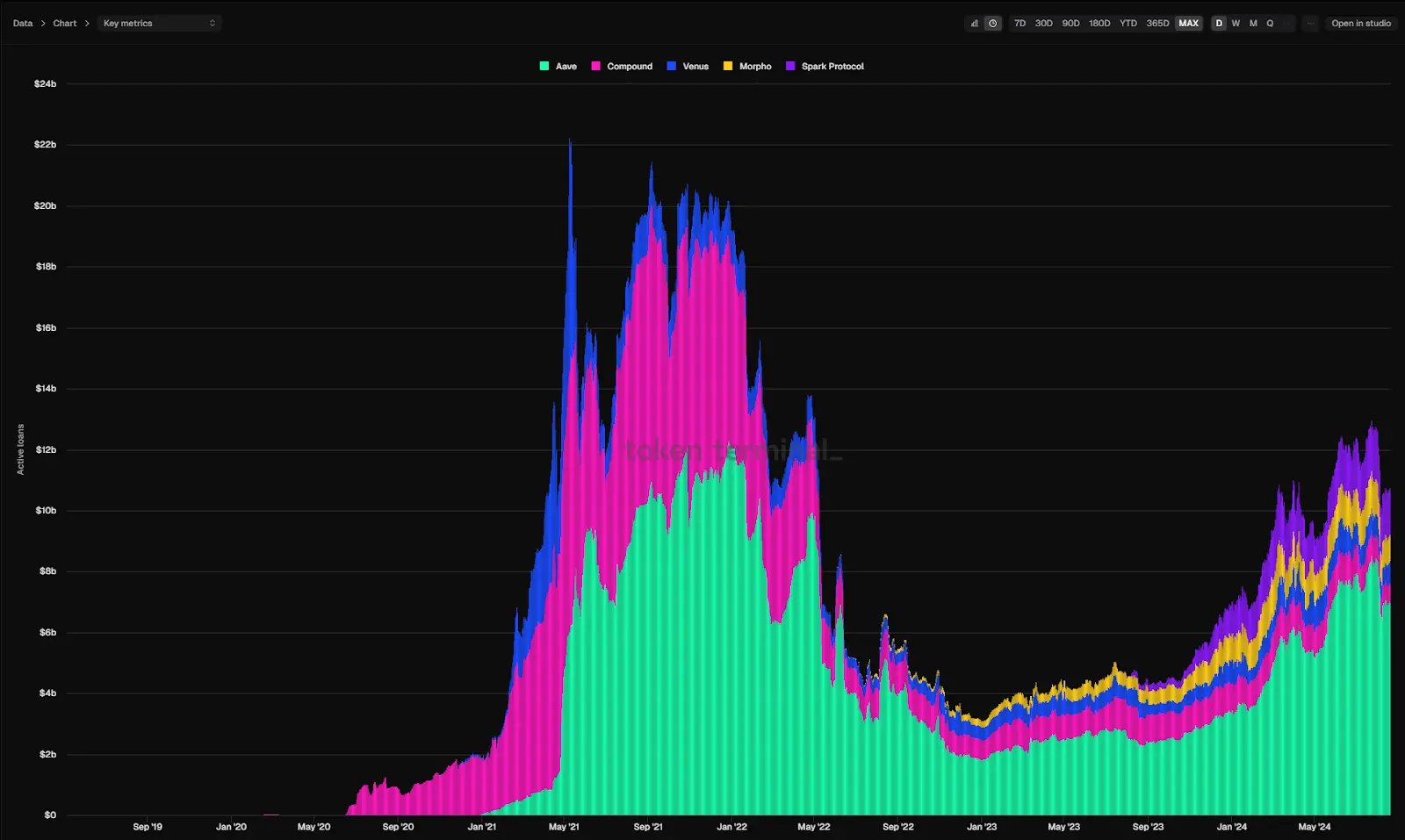

Loan Volume

Data sourced from Token Terminal

The loan volume, which measures the value of outstanding debt in lending protocols, is currently $106 billion. This is a 49.7% decrease from the peak of $211 billion in December 2021. The decrease in demand for loan leverage directly led to the weakness of the DeFi ecosystem.

As one of the oldest tracks in the cryptocurrency field, the performance of the DeFi track in this bull market cycle has not been satisfactory.

If we only consider these three points, we would not hesitate to conclude that this bull market cycle has fallen far short of expectations for DeFi.

DeFi tokens have similar reasons for their continuous decline in valuation to most altcoins, mainly summarized in three points:

First, the growth on the demand side appears weak. There is a lack of novel and attractive business models in the market, and the product-market fit (PMF) in many areas seems out of reach.

Second, the growth on the supply side is too rapid. With the continuous improvement of industry infrastructure and the lowering of the entrepreneurial threshold, a large number of new projects have emerged, and the token issuance has exceeded the market's carrying capacity.

Finally, the continuous emergence of unlocking waves. The continuous unlocking of tokens from projects with low liquidity and high fully diluted valuation (FDV) has brought heavy selling pressure to the market.

The decline in the valuation center of altcoins is actually the result of the market's self-adjustment, the natural process of the bubble bursting, and the manifestation of capital's self-redemption through market selection.

Most tokens supported by venture capital are not without value; they are just overvalued, and the market eventually brings them back to a reasonable price.

When mountains are heavy and waters are difficult, there is another village in the dim light.

DEX Volume

Data sourced from DeFiLlama

In recent months, DEX trading volume has surged, reaching 80% of the peak of $308.6 billion on November 21, 2021. The trading volume in June 2022 is expected to reach $190 billion. With the liquidity brought by ETF funds, this upward trend may continue until the end of the year.

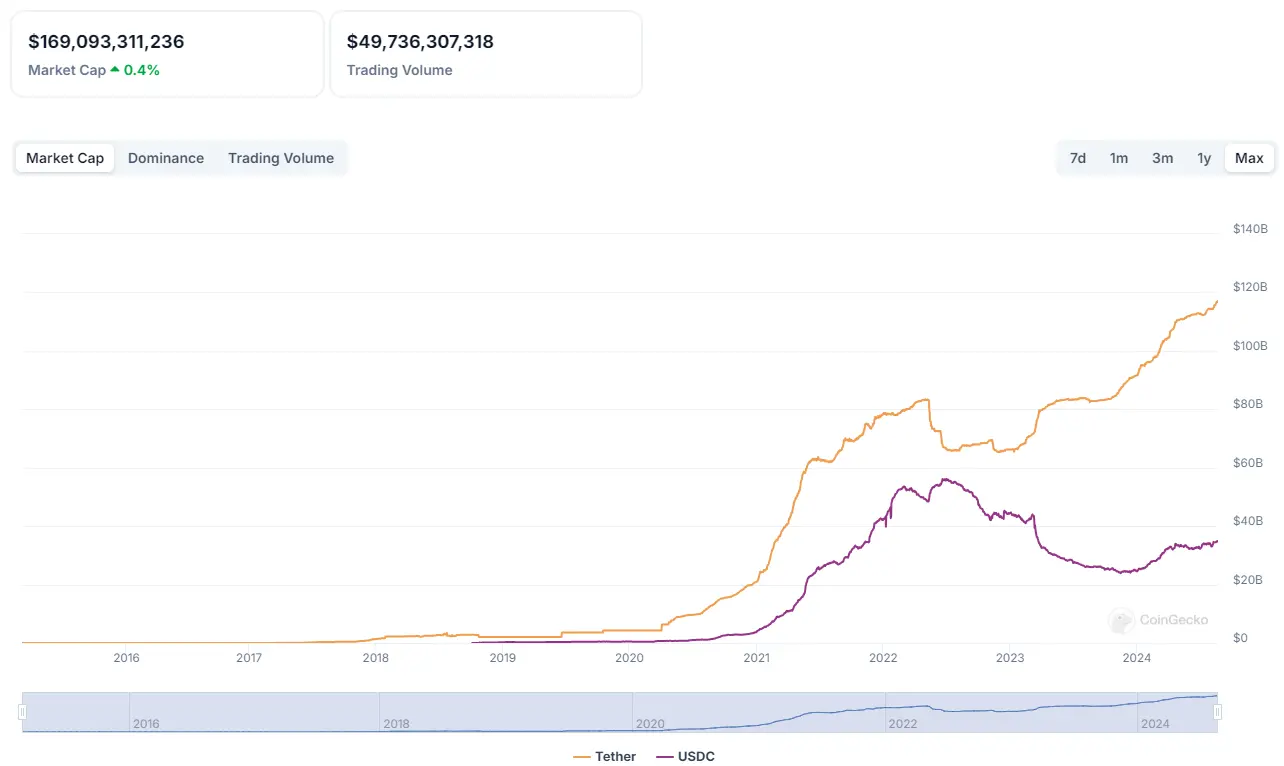

Stablecoin Supply

Data sourced from CoinGecko

The current market value of stablecoins is $169 billion, which has gained widespread attention and application globally, gradually expanding from the narrow context of cryptocurrency trading to an important choice for globalized payments.

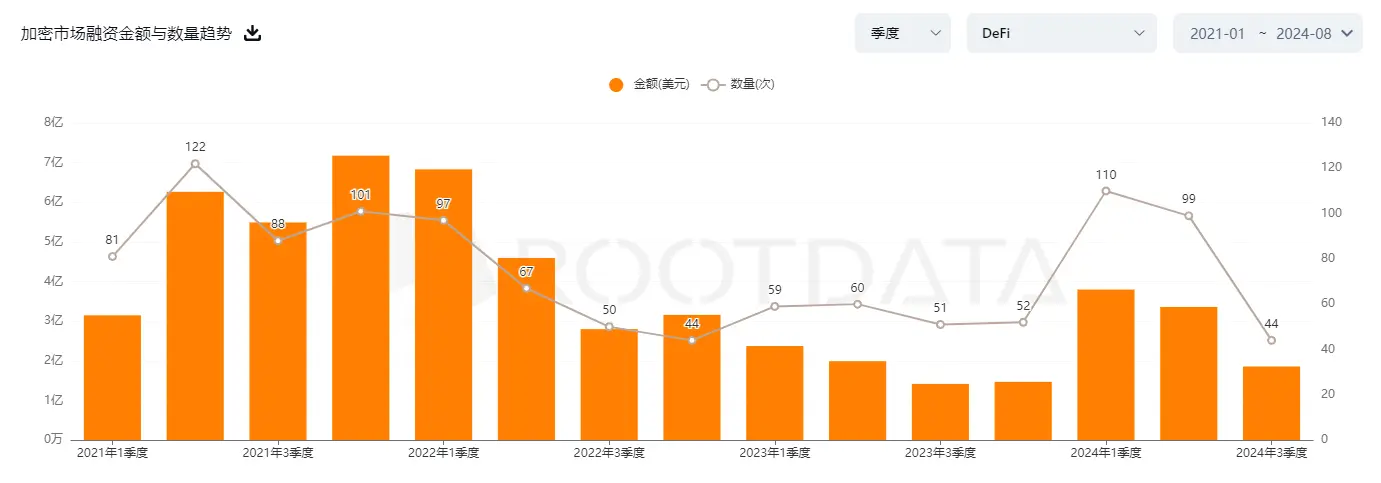

Institutional Financing

Investment funds in the DeFi sector are undergoing a significant revival. According to the latest data from Rootdata, the total investment in the DeFi sector has climbed to $900 million in the first half of 2024. Although this figure has not reached the peak of glory in 2021, it has clearly rebounded from the low point in 2023, showing signs of market recovery.

From the above three points, we can also see that the current situation of DeFi is not as bad as some people think. Is the value of DeFi tokens, like Layer2, currently in an overvalued area?

Let's take a look at what some leading DeFi projects are doing.

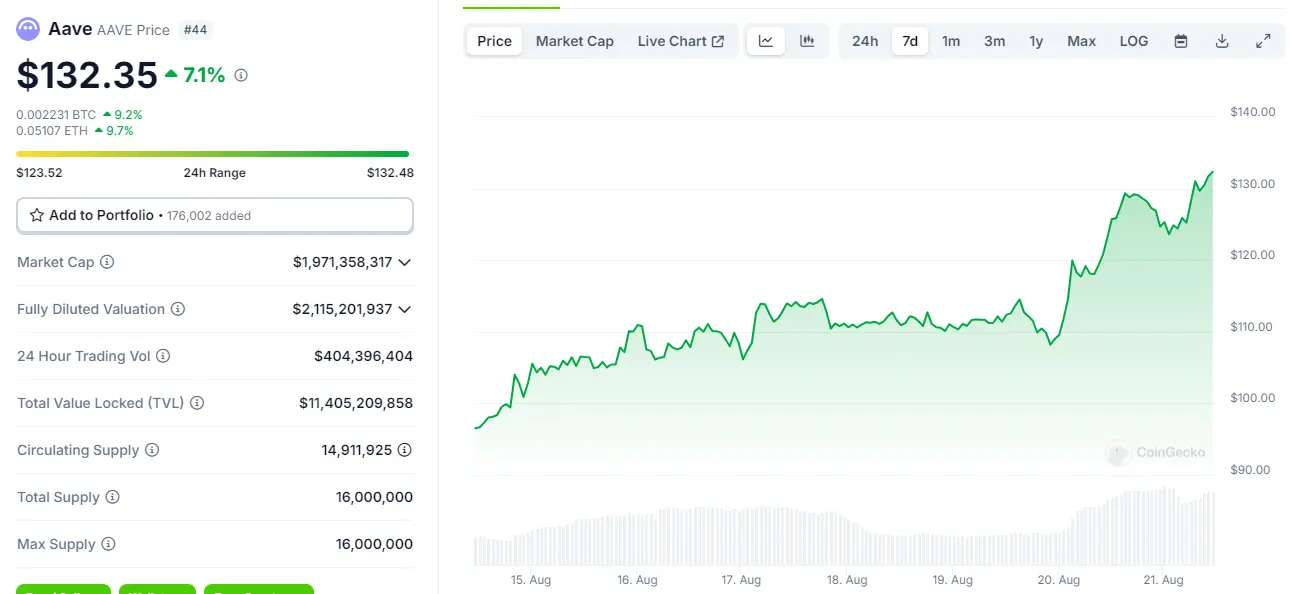

Lending: Aave

Aave is one of the oldest DeFi projects in history. After completing financing in 2017, it transitioned from peer-to-peer lending (when the project was still called Lend) to pool-based lending, and surpassed the leading project Compound in the previous bull market cycle. Currently, it is the number one in the lending track in terms of market share and market value, with an active loan amount of $7.5 billion. Aave's revenue has exceeded the peak of the bull market period, demonstrating strong profitability.

Data sourced from CoinGecko

At the time of writing, the AAVE token price has exceeded $132, with a 7-day increase of over 50%, reaching the level of the peak in March.

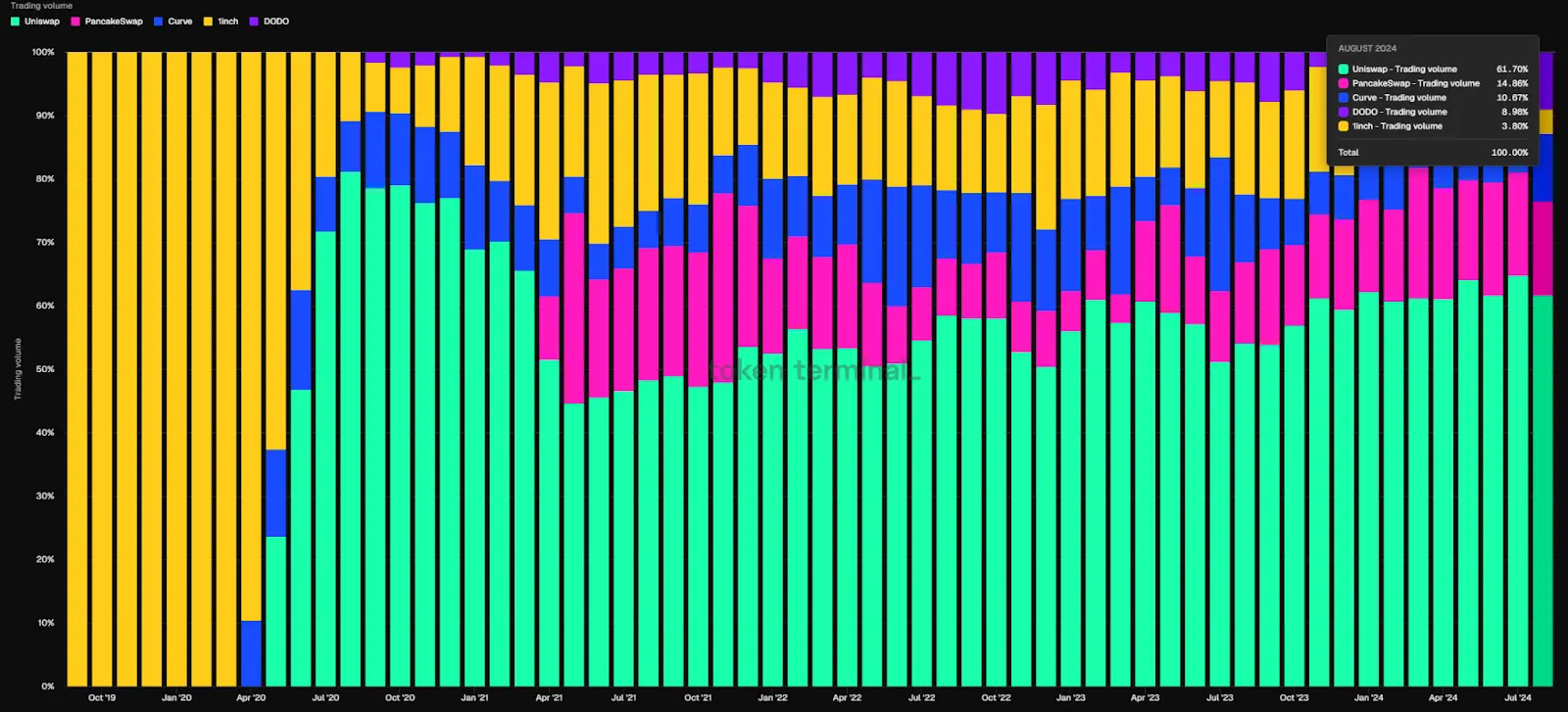

Dex: Uniswap

Data sourced from Token Terminal

Since the launch of version 2 in May 2020, Uniswap has experienced a tumultuous journey in the decentralized trading sector. It once reached its peak in August 2020, occupying nearly 78.4% of the market share, but plummeted to a low of 36.8% in the intense competition of DEX in November 2021. However, like a phoenix rising from the ashes, it not only regained its footing but also declared its resilience and perseverance with a market share of 61.7%.

The problem with many DeFi tokens is that they lack practical use and serve only as governance tokens. However, this situation is beginning to change: Uniswap's fee switch may become a turning point that other DeFi protocols will emulate, and UNI surged after this news.

Furthermore, regulatory clarity may accelerate the trend of revenue sharing. In April 2024, Uniswap received a Wells Notice from the SEC, indicating that regulatory authorities may take enforcement action against it. While this notice brought uncertainty, it also accompanied positive progress with the FIT21 bill, painting a clearer and more predictable regulatory future for DeFi projects like Uniswap.

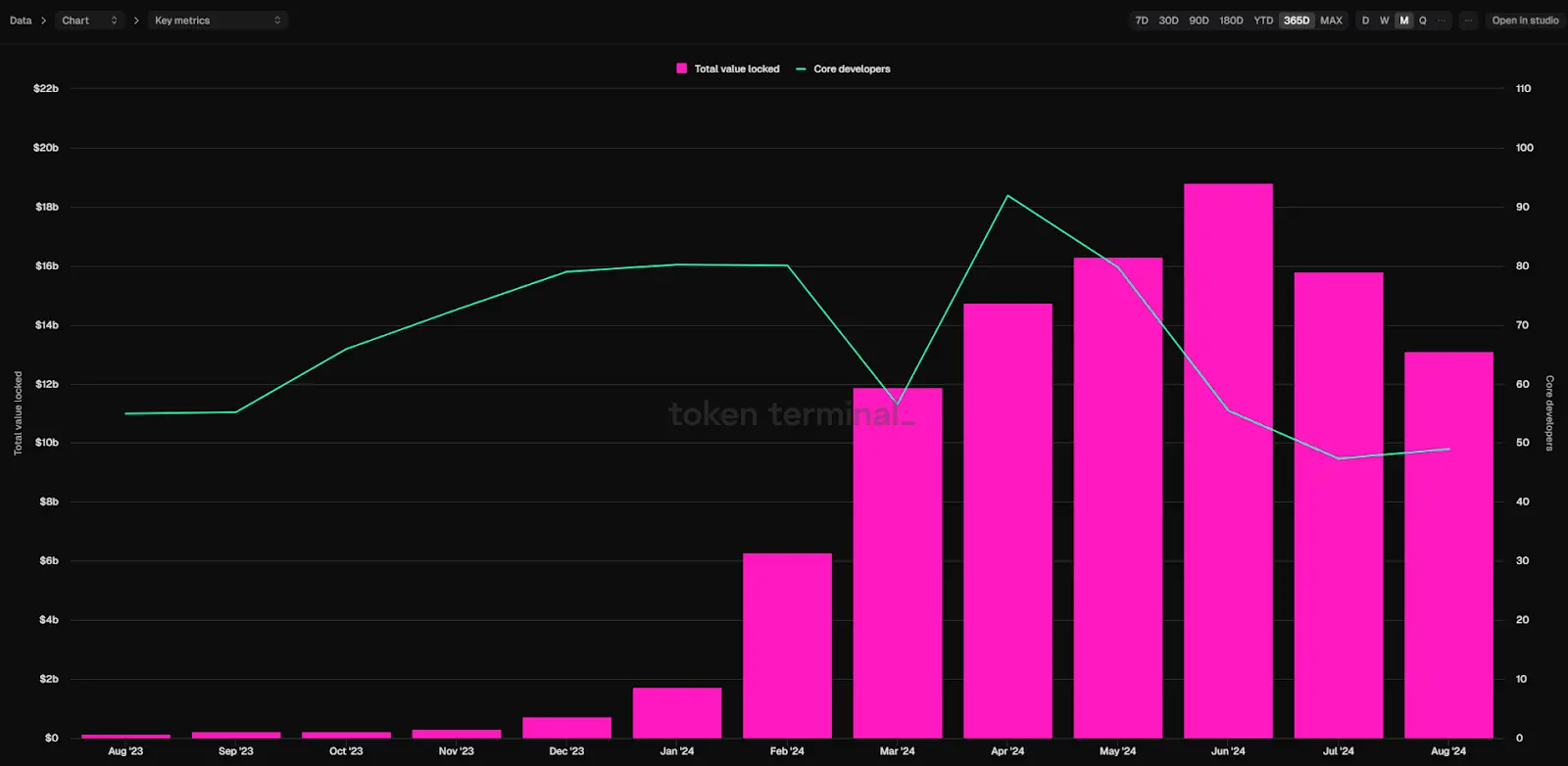

Restaking: EigenLayer

Restaking refers to the reuse of ETH staked on the Ethereum mainnet to support the security of other projects. Through this method, users can not only receive returns from their original staking but also increase potential rewards by supporting more projects.

Founded in 2021, EigenLayer is a pioneer in the concept of restaking. It is a middleware platform between the Ethereum mainnet and other applications. The platform allows stakers to restake their ETH and ETH staking derivative tokens (LST) on EigenLayer by deploying mainnet smart contracts.

Data sourced from Token Terminal

Since its launch in June 2023, EigenLayer has experienced rapid growth, with a current total staked value exceeding $12 billion, making it one of the largest blockchain protocols in the market, with a staked value even surpassing many major decentralized finance (DeFi) platforms such as Aave, Rocket Pool, and Uniswap.

This shows that the current DeFi is not only not dead, but it is an excellent time for layout

The DeFi sector has nurtured mature business architecture and profit models, with leading projects such as AAVE, Uniswap, and EigenLayer building strong moats.

From a supply perspective, leading DeFi projects have mostly crossed the peak of token issuance due to the advantage of early launch. With the comprehensive release of institutional tokens, future selling pressure in the market is likely to significantly decrease.

Although DeFi's market attention and price performance in this bull market cycle are not outstanding compared to emerging concepts such as Meme, AI, and Depin, its core business data—trading volume, lending scale, and profit levels—continue to rise. For example, AAVE's quarterly net income not only surpassed the previous cycle's peak but also set a new all-time high. This indicates that the recent price increase of AAVE tokens is not without purpose.

Considering the positive acceptance of crypto assets by traditional financial institutions such as BlackRock in recent years—whether in promoting the listing of crypto ETFs or issuing national debt assets on Ethereum—DeFi is likely to become a key investment area for them in the coming years. With the entry of these financial giants, mergers and acquisitions may become a convenient way for them to enter the market quickly. Any signs of mergers and acquisitions, even the slightest intention, may trigger a reassessment of the value of leading DeFi projects.

As cryptocurrency investments gradually return to rationality, the bubbles formed during the irrational boom have been burst by the market's liquidity tightening. In such an environment, crypto applications with solid economic value support, high product-market fit, and demonstrated strong resilience are more likely to usher in new development opportunities.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。