Overall, whether it is the OP Rollup or ZK Rollup project, the token prices have not performed well, failing to synchronize with the upward trend of Ethereum itself.

Written by: BitMart Research

Main conclusions

Change in narrative cycle: In the first half of the year, the Ethereum ecosystem was in a macro narrative and capital-driven cycle. Despite the continuous launch of technical Layer 2 tokens represented by ZK and OP, the prices of these new Layer 2 tokens continued to decline due to early market selling pressure and lack of investor confidence. This failure to effectively support the overall market ultimately led to price trends diverging from Ethereum itself. While the price of Ethereum continued to rise, the prices of the newly launched Layer 2 tokens continued to decline.

Rise of Base: Base has emerged as a dark horse this year, showing strong growth in the ecosystem and user activity, and has become the second largest leader in Layer 2.

OP rollup vs. ZK rollup: In the first half of 2024, OP rollup has already taken the dominant position in the Layer 2 market, with the top four projects in the overall Layer 2 TVL rankings being OP rollup projects. However, overall, whether it is OP rollup or ZK rollup projects, their token price performance has not been satisfactory, failing to synchronize with the upward trend of Ethereum itself.

L2 Token Secondary Market Performance

In the past six months, Ethereum's price has experienced a period of correction before starting to rise, ultimately achieving a 35.01% increase. Despite Ethereum's strong price performance, newly launched L2-related tokens such as MNT, BLAST, ZK, MANTA, and STRK experienced even greater declines. Market participants seem to prefer purchasing Ethereum itself rather than related L2 technical projects. The following is the price performance of ETH and L2 project tokens from January 1, 2024, to July 1, 2024:

ETH, up 35.01%

MNT, up 9.27%

BLAST, up 1.36%

ZK, down 26.46%

MANTA, down 59.44%

STRK, down 76.89%

This phenomenon indicates that in the first half of the year, Ethereum is still in a macro narrative and capital-driven cycle. The market generally believes that the approval of ETH ETFs will bring more institutional investment and market liquidity to Ethereum, rather than technical innovation in L2 projects. This phenomenon is caused by: first, a large number of institutional projects entering the market this year, with higher average valuations, leading to continuous price declines after initial launch and subsequently undermining investor confidence in these projects; second, the newly launched tokens of the aforementioned Ethereum Layer 2 projects have a relatively short time on the market, with relatively low initial market acceptance and liquidity, resulting in more significant price fluctuations. Therefore, despite the price of Ethereum rebounding after a correction, its Layer 2 tokens have failed to rebound in sync and have instead suffered even greater declines.

Figure 1: In terms of token price performance, the observed L2 token price trends are diverging from the price trends of ETH.

Data source: Trading View

Layer 2 On-Chain Data Indicator Analysis

- Ecosystem & TVL Analysis

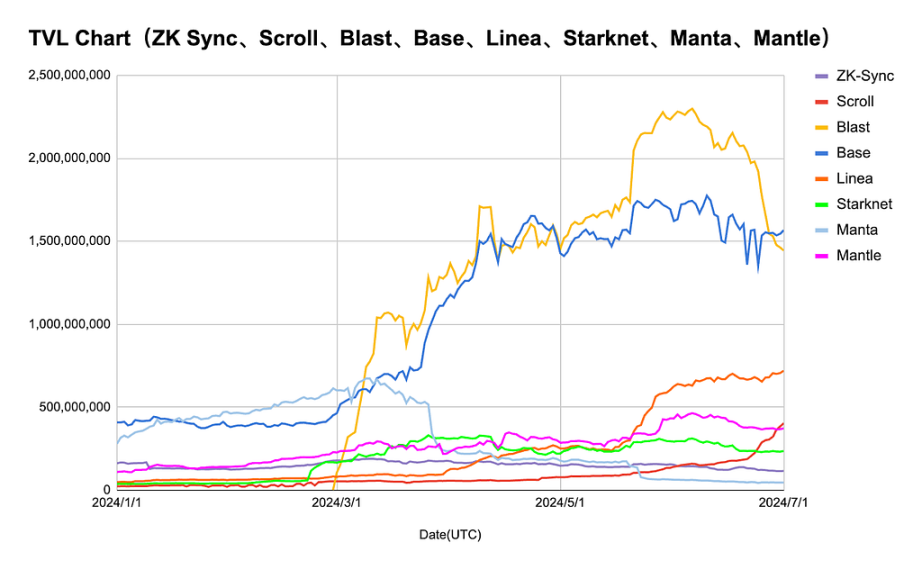

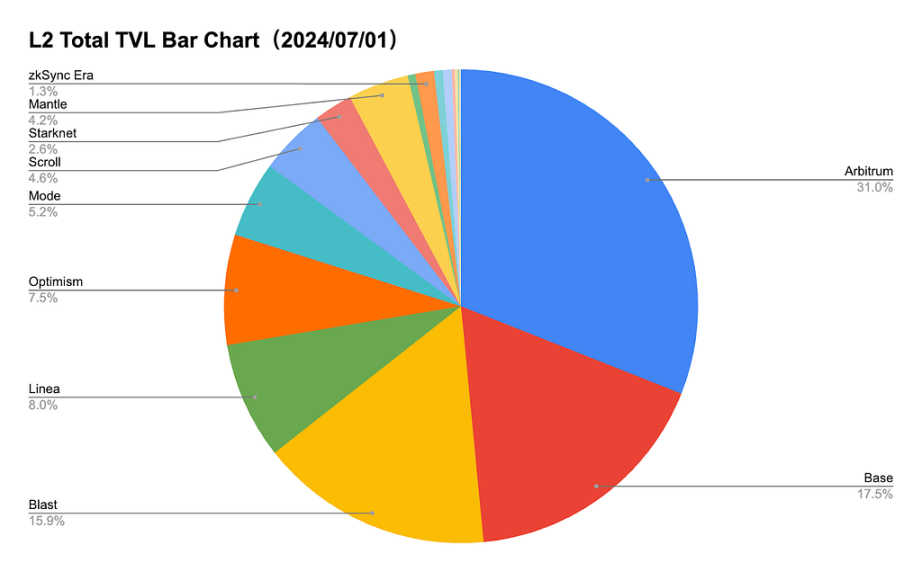

Although the price performance of most L2 tokens in the first half of the year was not very satisfactory, the on-chain data performance of some projects still had bright spots. The TVL of Base and Blast showed a significant upward trend in the first half of the year and far exceeded other L2 projects in terms of total value locked. The peak TVL of Base reached around 1.8 billion, and the peak TVL of Blast reached around 2.3 billion. In addition, the combined market share of Base, Blast, and Linea in the L2 TVL has surpassed Optimism, ranking in the top four. The growth of Base's TVL is mainly due to its diversified ecosystem. According to Coingecko data, the Base ecosystem supports a total of 656 tokens with a daily trading volume of approximately 664 million USD. In contrast, despite having a higher average TVL, the ecosystem of Blast is not as comprehensive, currently supporting only 74 tokens with a daily average trading volume of approximately 65 million USD.

Linea's TVL showed a significant increase in mid-May, possibly due to the announcement of the Zerolend re-staking project airdrop and coin issuance, as well as the staking points activity launched by Linea in May, attracting a large amount of TVL. Currently, the Linea ecosystem supports 57 tokens with a daily average trading volume of approximately 37 million USD. Starknet, ZK Sync, Scroll, and Mantle showed relatively small fluctuations in TVL throughout the observation period, consistently showing a gradual upward trend. However, starting from April, Manta's TVL showed a significant decline, continuing to decline until July 1.

Overall, from the perspective of ecosystem size, activity, and TVL, Base is currently in a leading position, and its diversified ecosystem has brought greater on-chain activity and TVL to Base.

Figure 2: As of July 1, the number of tokens supported and 24-hour trading volume for each Layer 2.

Data source: Coingecko

Figure 3: In the first half of the year, the TVL of Balst and Base far exceeded that of other observed Layer 2 projects.

Data source: Defillama, Coingecko

Figure 4: As of July 1, Arbitrum still has the highest share of total Layer 2 TVL (31%), with Base, Blast, and Linea TVL surpassing Optimism, ranking in the top four.

Data source: Defillama

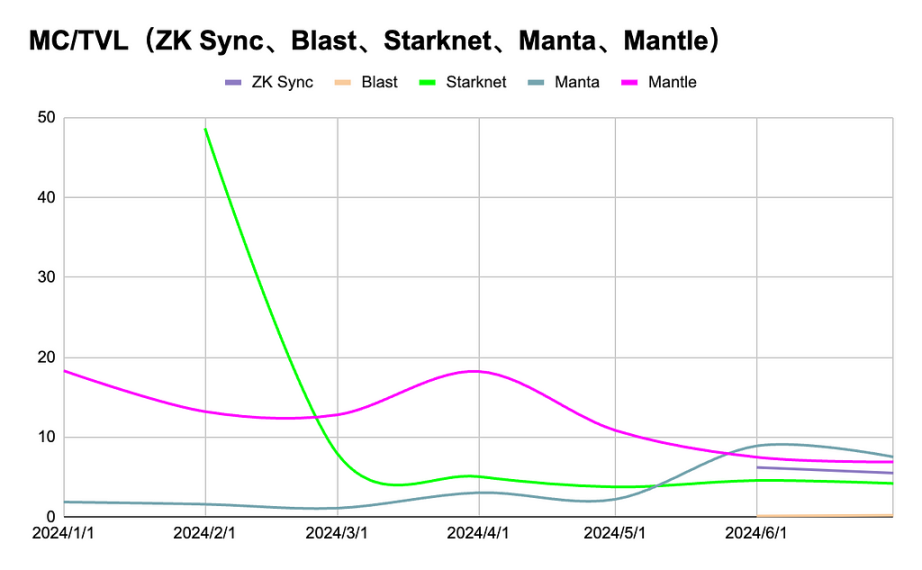

- PE Ratio Analysis (TVL/MC)

Starknet and Mantle: These two projects had a high PE ratio in the early stages, but then quickly declined and remained stable. The market is cautious about their future growth potential, and the initial high PE ratio may be due to overvaluation. According to CMC and Defillama data, the circulating market value of STRK was close to 1.9 billion USD when it opened in February, but its TVL at that time was only about 40.47 million USD, leading to its price being severely overvalued. Although a nearly six-fold increase in TVL a month later significantly reduced the PE ratio, investor confidence remained low, and large early market selling pressure caused STRK to be the token with the largest decline in the first half of the year among the observed Layer 2 tokens (-76.89%).

ZK Sync and Linea: Showed strong growth momentum in the first half of the year, but experienced a decline in TVL after reaching their peak. This indicates that they attracted a lot of attention and funds in the short term, but still faced market fluctuations.

Scroll, Blast, Base, and Manta: Showed minimal changes, with small fluctuations in TVL and PE ratios, indicating that their positions in the market are relatively stable but have not attracted significant attention. This may reflect the token holders' relatively stable confidence in these projects, but without particularly outstanding growth expectations.

Overall, the market performance of Ethereum Layer 2 solutions shows significant differences, reflecting different levels of confidence and expectations from market participants for different projects. The rapid growth and subsequent decline of ZK Sync and Linea indicate speculative behavior in the market for emerging projects, while Starknet and Mantle demonstrate a more stable market acceptance. The relatively stable performance of Scroll, Blast, Base, and Manta indicates their relatively stable positions in the market, although not particularly outstanding.

Figure 5: Starknet, as the first ZK rollup project to go live, was severely overvalued in the early stages

Data source: Defillama, CMC

- Layer 2 First Half-Year Revenue Statistics

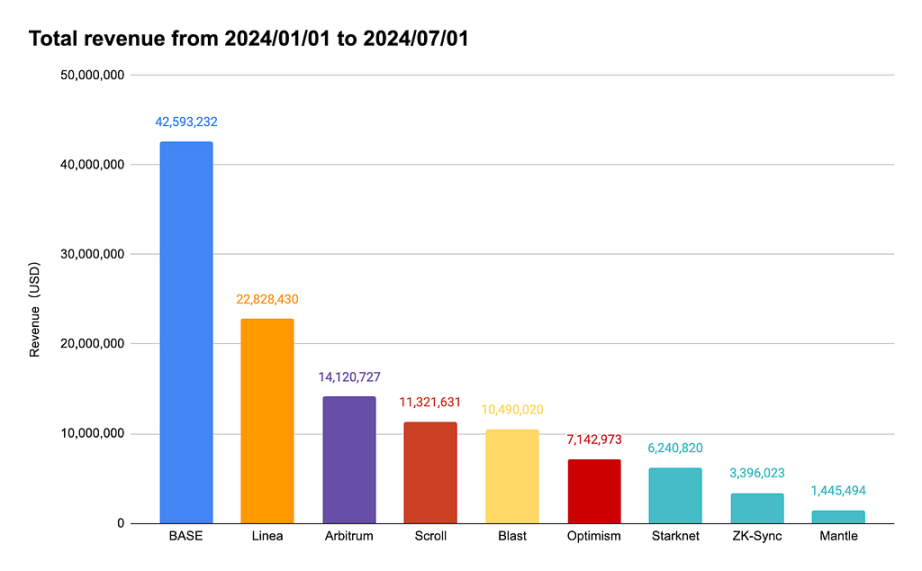

In the past first half of the year, Base's revenue reached as high as 42.59 million USD, far exceeding the two leading Layer 2 projects, Arbitrum and Optimism. As mentioned above, Base's high revenue is mainly due to its diversified ecosystem, making it the new leader in Layer 2. In addition, Linea's revenue of 22.82 million USD surpassed Arbitrum and Optimism, ranking second.

Figure 6: Base becomes the highest revenue-generating Layer 2, with revenue far exceeding Arbitrum and Optimism

Data source: Artemis

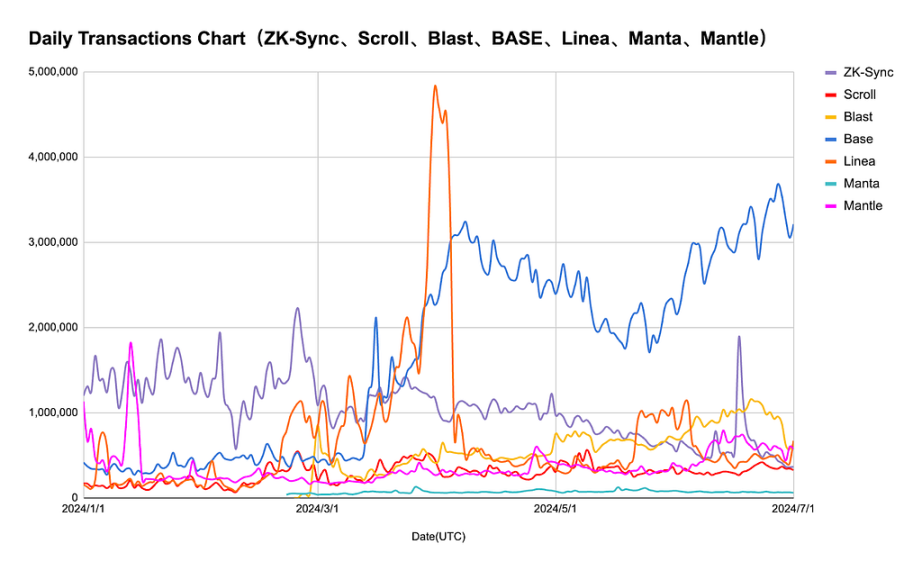

- Number of Transactions

According to official browser data for each Layer 2, the daily transaction volume for each Layer 2 showed significant differences over the past six months. Base's daily transaction volume saw a significant increase in April and has since been consistently leading, fluctuating between 2 to 4 million transactions per day. Linea saw an abnormal increase in transaction volume in April, with a daily average transaction volume approaching 5 million, the specific reason for which is currently unknown. The daily average transaction volume for other Layer 2 projects has remained at around 2 million transactions or slightly increased. Overall, in the first half of the year, Layer 2 has remained active, with no significant decrease in the overall daily average number of transactions.

Figure 7: Among the observed Layer 2 projects in this article, Base's daily transaction volume is consistently leading

Data source: Each L2Scan

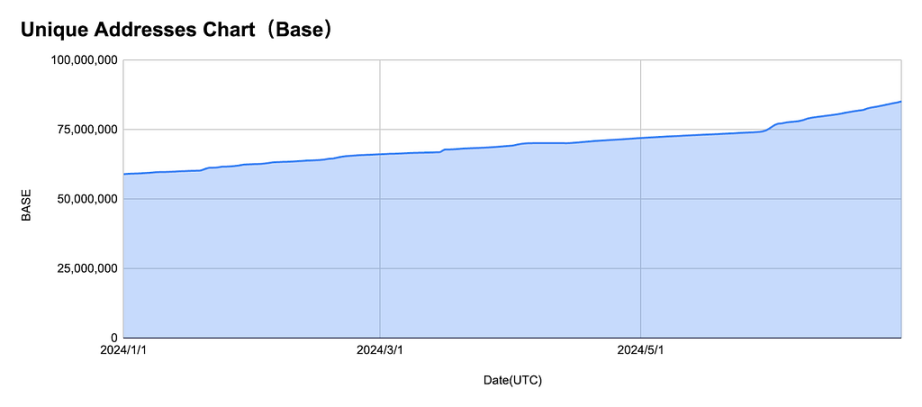

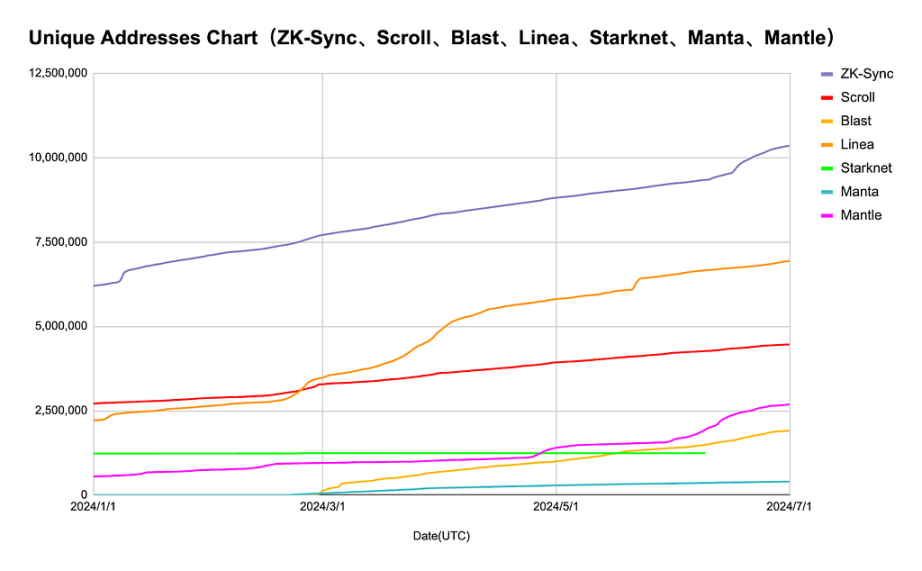

- Number of New Addresses

Base: At the beginning of 2024, the number of unique addresses for Base was approximately 60,000,000, which increased to nearly 85,000,000 by early July 2024, more than seven times that of the second-place ZK Sync. This shows that Base's user base is continuously expanding, and its network adoption rate is steadily increasing.

ZK Sync: From the beginning of the year to early July, the number of unique addresses increased from approximately 6,000,000 to nearly 10,000,000, showing a significant growth trend, indicating that it has gained increasing user recognition in the market.

Scroll, Blast, Linea, Mantle: The number of unique addresses for these four Layer 2 projects has remained steadily increasing over the past six months.

Starknet and Manta: The number of unique addresses for these two Layer 2 projects has remained almost unchanged over the past six months, indicating that they have not attracted many new users to their ecosystems.

Overall, the performance of these Layer 2 projects in terms of user numbers shows significant differences, with Base, ZK Sync, and Linea showing strong growth momentum, indicating that many new users have joined their ecosystems in the past six months, while Starknet and Manta have seen almost no change in the number of unique addresses.

Figure 8: Among the observed Layer 2 projects in this article, Base's daily new address count is consistently leading

Data source: Each L2Scan

Data source: Each L2Scan

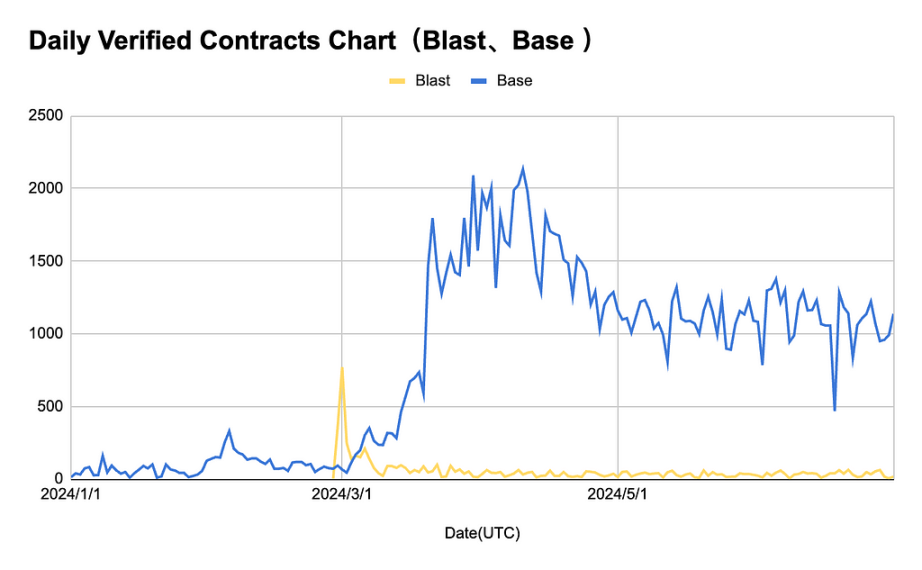

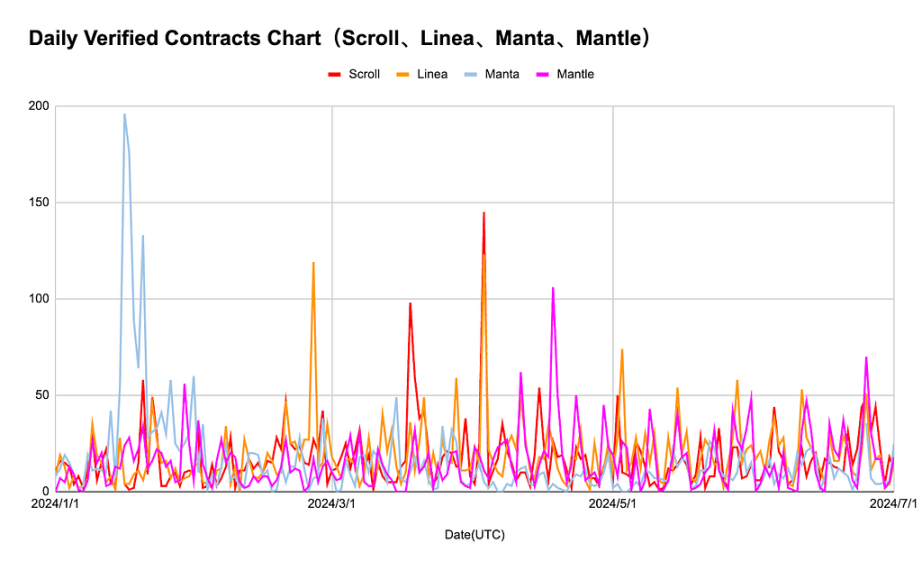

- Number of New Verification Contracts

The chart below shows that the daily number of new verification contracts for Base has a significantly different trend from other Layer 2 projects. The daily number of new verification contracts reached its peak in March 2024, with nearly 2,000 contracts in a single day, and then declined but remained at a relatively high level. The main reason for such a high number of new contracts is the continuous development of the MEME token in the Base ecosystem. According to Coingecko data, the total market value of the MEME token is currently about 56.2 billion USD, of which the MEME token on Base accounts for approximately 3.2%, ranking third, second only to the 16.6% market share of Solana's MEME token. The birth of a large number of Base MEME tokens has led to a continuous increase in the number of contracts. The overall fluctuation of new contracts for other Layer 2 projects has remained relatively small, averaging less than 200 new contracts per day in the first half of the year. Blast and Manta showed a significant peak in the early stages, possibly due to the promotion of specific projects, followed by a rapid decline and stabilization, indicating high initial popularity but poor sustainability.

Overall, the Base platform stands out among all platforms, showing strong growth momentum and user activity. In contrast, the number of new verification contracts for Blast, Scroll, Linea, Manta, and Mantle is relatively low and fluctuates significantly, reflecting the unstable influence and user activity of these platforms in the market.

Figure 9: Among the observed Layer 2 projects in this article, Base's daily new verifiable contract count is consistently leading

Data source: Each L2Scan

Data source: Each L2Scan

Comparison of OP rollup and ZK rollup Market Performance

OP rollup (Base, Blast, Mantle, Manta)

Base: Base has made significant progress in the first half of the year. Despite being launched for only about a year, its TVL has reached 1.5 billion USD, surpassing the OP mainnet, making it the second most popular Ethereum Layer 2 after Arbitrum. Additionally, Base has become the highest revenue-generating L2 chain, with revenue reaching 42.6 million USD in the first half of 2024, almost twice that of the second-place Linea.

Blast: After the mainnet launch on February 29, Blast attracted a large number of users to participate in its ecosystem's DAPP interaction through marketing strategies such as airdrops and point activities, causing Blast's TVL to exceed 2 billion at one point. However, with the listing of Blast tokens, the significant early selling pressure from the airdrop activities and user attrition led to a continuous decline in Blast's token price and TVL. Currently, Blast's TVL ranks third in the entire Layer 2 market (approximately 1.4 billion). Whether Blast can maintain its TVL and activity level after the airdrop will reflect the stickiness of its initial user base.

Mantle: The on-chain data performance of Mantle in the first half of the year was average, with no outstanding highlights in terms of TVL, revenue, or on-chain activity.

Manta: At the beginning of the year, Manta had relatively high on-chain activity, but as the token price declined and the lack of innovation in the ecosystem led to a gradual decrease in its TVL and on-chain data performance. Currently, it is at the bottom of the Layer 2 projects.

ZK rollup (ZK Sync, Starknet, Linea, Scroll)

ZK Sync: As a well-established ZK rollup project, ZK Sync issued its token ZK in the first half of the year and airdropped it to early users of the L2 chain. The initial circulating market value of the token was 800 million USD, with a fully diluted market value of 4.5 billion USD. Since its launch, the token's price has remained stable between 0.15 and 0.18 USD, with a circulating market value of approximately 670 million USD, slightly lower than its competitor Starknet's $STRK token, which currently has a circulating market value of nearly 900 million USD.

Linea: Linea currently ranks first in TVL among ZK rollups and fourth in the entire Layer 2. Linea's rapid growth in TVL and on-chain activity since its launch in August 2023 is mainly due to its point activities launched in May. However, it is worth noting that Linea has not yet issued tokens. If there is significant early selling pressure after the token issuance from the point activities, and whether users can remain active after receiving the airdrop will be issues that Linea needs to pay attention to in the future.

Starknet: Starknet airdropped the $STRK token on February 20, 2024, making it the first ZK rollup to issue tokens. However, as it was the first issuance of ZK-based tokens, the market initially severely overvalued its value. The circulating market value of STRK was close to 1.9 billion USD when it opened in February, but its TVL at that time was only about 40.47 million USD. The significant early market selling pressure caused STRK to be the token with the largest decline in the first half of the year among the observed Layer 2 tokens (-76.89%). In the first half of the year, Starknet's main focus was on laying out the GameFi track, but due to the continued slump of meme coins, Starknet's on-chain activity and TVL did not show significant growth.

Scroll: In May of this year, Scroll launched L2 point activities similar to Linea, which led to a significant increase in Scroll's TVL from around 100 million to around 400 million. Such high on-chain activity makes Scroll one of the airdrop projects to focus on in the second half of the year.

Overall, in the first half of 2024, OP rollup currently occupies the dominant position in the Layer 2 market, with the top four TVL rankings in the entire Layer 2 market being OP rollup projects. Especially, Base has shown strong growth in its ecosystem and user activity this year, becoming the second largest leader in Layer 2. However, overall, whether it is OP rollup or ZK rollup projects, their token price performance has been unsatisfactory and has not kept pace with the upward trend of Ethereum itself. This reflects that the market is currently not in a cycle of innovative tracks, and market participants' funds are more inclined to be driven by macro narratives.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。