- Student author: @Floraaa_upup

- Supervising teacher: @CryptoScott_ETH

- Initial release date: July 10, 2024

This article is about 17,752 words long, and is expected to take a long time to read. Please refer to the table of contents for efficient reading.

Payment is a key scene in the cryptocurrency ecosystem, with tens of thousands of cryptocurrency payments occurring on-chain and off-chain every day. A new cryptocurrency usually appreciates due to its actual payment use, and payments have become an important bridge connecting the Web2 world and the Web3 world.

In the business of Web3 payments, some people make a fortune by providing payment channels, while others focus on building more secure wallet technologies. So, how exactly does capital transfer work in the Web3 world? This article will take you deep into various business scenarios and projects in the Web3 payment industry.

In August of last year, PayPal announced the launch of "Paypal USD," a stablecoin pegged to the US dollar, for transfers, payments, and other businesses. In April of this year, the financial infrastructure platform Stripe stated that stablecoin payments would be integrated into its payment suite within a few weeks and would begin supporting USDC payments this summer. In June, Mastercard announced the first launch of the infrastructure feature Mastercard Crypto Credential for peer-to-peer transactions, enabling cross-border payments in Latin America and Europe on the blockchain. Traditional payment industry giants have been making high-profile entries into the Web3 payment industry over the past two years. What exactly are the reasons for this?

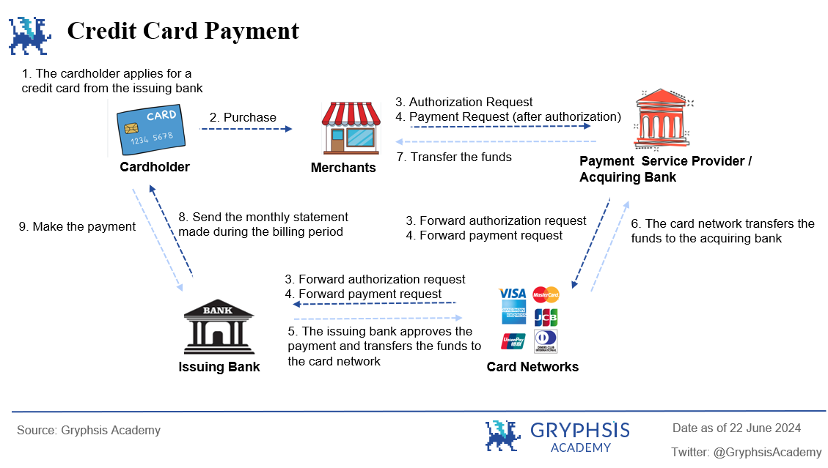

Before uncovering the reasons, let's first understand what payment is. The essence of payment is the flow and transfer of funds. In the traditional payment industry, users complete fund transfers through cash payments, card/bank transfers, and third-party payments. The completion of a cross-border payment usually requires the support of multiple participants. Taking the payment chain of a bank card as an example, we will briefly introduce the participants and the process of cross-border payments.

- Cardholder (user/buyer): The user selects goods/services at the merchant and initiates payment.

- Merchant: The merchant needs to access the payment gateway of the payment service provider to receive and process payments through the integrated payment gateway.

- Payment service provider: Provides payment gateways and payment processing services. The payment information entered by the user is sent through the payment gateway to initiate the payment. Some payment service providers also provide acquiring services.

- Acquiring institution: Banks or financial institutions cooperating with merchants. The acquiring institution receives payment requests and forwards them to the card organization, and is also responsible for processing settlement and clearing after transaction authorization.

- Card organization (such as MasterCard, VISA): Global network for processing payment card transactions. The card organization receives payment requests from acquiring institutions, sends authorization requests to the issuing bank, and forwards the authorization response back to the acquiring institution to ensure that the transaction request is approved by the issuing bank.

- Issuing bank: The issuing bank receives authorization and request for payment from the card organization, verifies the user's identity and account status, authorizes or declines the transaction, and disburses funds after successful authorization.

- Settlement: The final stage of the payment process, involving the transfer of funds from the user's account to the merchant's account. Settlement is usually coordinated by the acquiring institution and the issuing bank, and the actual transfer of funds may be conducted through interbank clearing networks.

The above payment process shows the clear division of labor and high maturity of traditional cross-border payments, with high acceptance, relative security, and the advantage of large-scale transactions. However, traditional cross-border payments also have some limitations:

- Longer payment processing time: Due to the involvement of multiple parties, cross-border payments processed through international card organizations usually take at least T+1 day to complete, meaning that it takes at least T+1 day to reach the merchant's account, resulting in relatively weak immediacy of delivery.

- Multi-tier fee structure: Due to the involvement of many parties in a transaction, there is a multi-tier fee structure. For example, for a credit card payment, the acquiring institution, bank, and card organization will charge different fees.

- Limited transparency and time-consuming traceability: If a credit card is stolen, it usually takes several working days to trace and query the transaction.

- Dependence on traditional banks: Slow technological development and inadequate performance of traditional banking systems in meeting emerging payment demands.

- It is these limitations that have prompted technological innovation, leading us into a new era of Web3 payment chains.

With the relatively mature development of traditional payments today, why are giants gradually shifting their focus to Web3?

In 2023, Mastercard's net profit was $11.2 billion (about 33,400 people), while Tether, the company issuing the stablecoin USDT in the cryptocurrency industry, had a net profit of $6.2 billion in 2023, with only about 100 employees. In comparison, the wealth created per employee is much higher in the cryptocurrency industry, and the return is also the same.

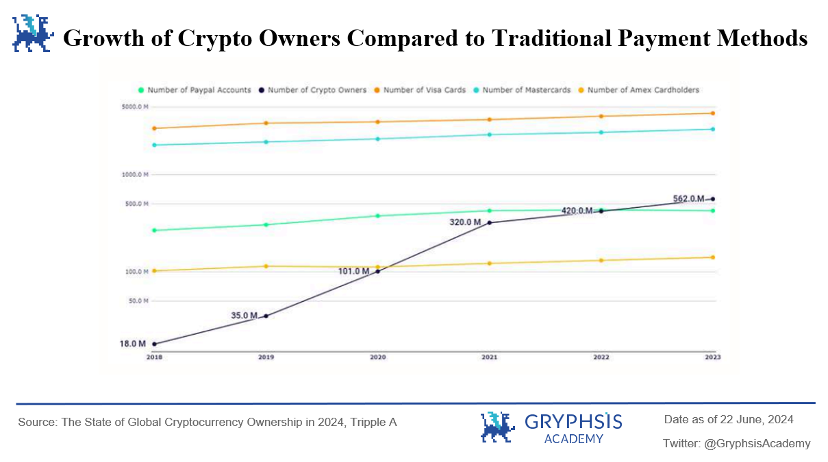

From the chart, we can see that from 2018 to 2023, the compound annual growth rate of cryptocurrency ownership reached 99%, far exceeding the 8% growth rate of traditional payment methods. During the same period, the growth rate of cryptocurrency ownership exceeded that of several US payment giants.

In 2022, faced with fierce industry competition and relatively high operating costs (operating costs accounted for 70.8% of gross profit in 2022), PayPal also began to focus on cryptocurrency business. The importance of cryptocurrency business in PayPal's overall revenue is gradually increasing.

Within a year, cryptocurrency-related operating expenses increased from $800 million to $1.2 billion, a 50% increase, and cryptocurrency-related net profit increased from $700 million to $1.1 billion, a 57% increase. The increase in operating expenses related to cryptocurrency reflects PayPal's continued investment in this area and its confidence, including technological upgrades, security measures, and market expansion.

The significant increase in net profit not only demonstrates the profitability of cryptocurrency but also proves PayPal's effective operational strategy in the cryptocurrency market and its optimism about the future growth potential of cryptocurrency. Therefore, PayPal has the motivation to continue to explore new industry opportunities.

The halving of BTC and the compliance of BTC ETF have brought more recognition and payment demand to the cryptocurrency industry. The Bitcoin halving event, by reducing the speed of new Bitcoin generation, has increased its scarcity and expected value growth, attracting widespread market attention. The launch of Bitcoin exchange-traded funds provides traditional investors with a low-threshold, convenient investment channel, enhancing market confidence. The expected launch of Ethereum exchange-traded funds has further sparked interest in the Ethereum ecosystem and innovative applications. These factors together have driven more people to understand and participate in Web3 payments.

In addition, the increasing demand for deposits and withdrawals has also driven the need for conversion services between fiat currency and cryptocurrency (deposits and withdrawals involve the conversion between fiat currency and cryptocurrency). The avenues for providing these services include centralized exchanges, independent deposit and withdrawal payment institutions, cryptocurrency ATMs, and POS machines that support cryptocurrency payments. Through these channels, users can easily convert between fiat currency and cryptocurrency, promoting the widespread use and popularization of cryptocurrency.

Microsoft began accepting Bitcoin as payment for its online Xbox store in 2014; Twitch, a leading game streaming platform owned by Amazon, accepts Bitcoin and Bitcoin Cash as payment for its services; Shopify, as a leading e-commerce platform overseas, supports Bitcoin payments through integration with payment processors such as BitPay. The support for cryptocurrency payments by leading companies in different industries indicates that Web3 payments are bringing more possibilities.

- Reducing Exchange Rate Risk

Cross-border e-commerce often involves transactions between multiple currencies, with a certain exchange rate fluctuation risk. Shopping using cryptocurrency as the unit can reduce this risk, as cryptocurrency does not involve exchange rate losses between different currencies.

- Reducing Transaction Costs

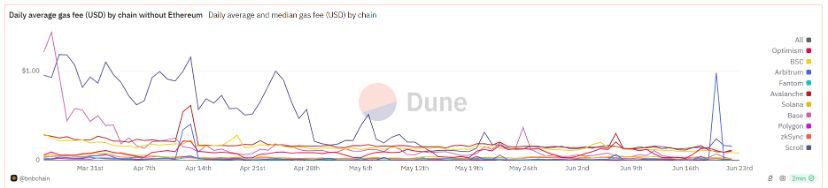

Traditional cross-border payments are often accompanied by high transaction fees and the involvement of multiple institutions. In contrast, cryptocurrency transaction fees are usually cheaper because they eliminate the intermediation of banks or other financial institutions. If it is an on-chain payment, only a network fee needs to be paid, which is usually low. If the transaction is processed through payment service providers (such as Coinbase, BitPay), there is a transaction fee. Compared to the multi-layered fees of traditional payment institutions, this means that for large-volume cross-border e-commerce, transaction fees can be effectively reduced. For example, cross-border payments made using traditional methods may incur transaction fees of 3-5%, while using cryptocurrency payments, this ratio can be reduced to below 1%. Due to the high transaction fees on the Ethereum mainnet, this has also sparked more public chains to achieve cheaper network fees through technological innovation. As shown in the figure below, since the network fee for transactions is not related to the amount but to the congestion level of the network, for some large cross-border on-chain payments, the transaction fee is less than $0.5, greatly reducing the cost of transaction fees.

Source: dune @bnbchain

- Enhancing Payment Security

The decentralized and distributed ledger characteristics of blockchain technology make every transaction publicly transparent and unchangeable once recorded. This reduces the possibility of fraud and hacking attacks. Due to the transparency of the blockchain, the trust level of transactions is increased for both merchants and consumers. Consumers know that their payment information is secure, while merchants reduce the possibility of fraud and chargebacks.

- Connecting Global Markets

Using cryptocurrency for payments is not restricted by the international banking system, and transactions can be completed quickly. Additionally, cryptocurrency transactions (24/7) are not affected by holidays and working hours. Many consumers in certain countries and regions may not be able to use traditional payment methods on cross-border e-commerce platforms, but they can use cryptocurrency as an alternative.

Regardless of whether it is enterprises or individual investors in the cryptocurrency industry, they are attracted by tax incentives. For example, Portugal does not tax individual cryptocurrency gains; Singapore does not impose capital gains tax on cryptocurrency; Bermuda, with its secure and transparent regulatory environment and the Digital Asset Business Act, has attracted token issuance companies, cryptocurrency custody service providers, and blockchain development enterprises, becoming an important hub for digital assets and innovative technologies.

Since 2019, the Bermuda government has announced that it can accept USDC for payment of taxes, utilities, and other administrative service fees. In addition, based on decentralized network systems, transactions in Web3 bypass many centralized institutions and banks, circumventing conventional tax processes. Therefore, bonuses within some digital asset companies are also distributed in the form of stablecoins.

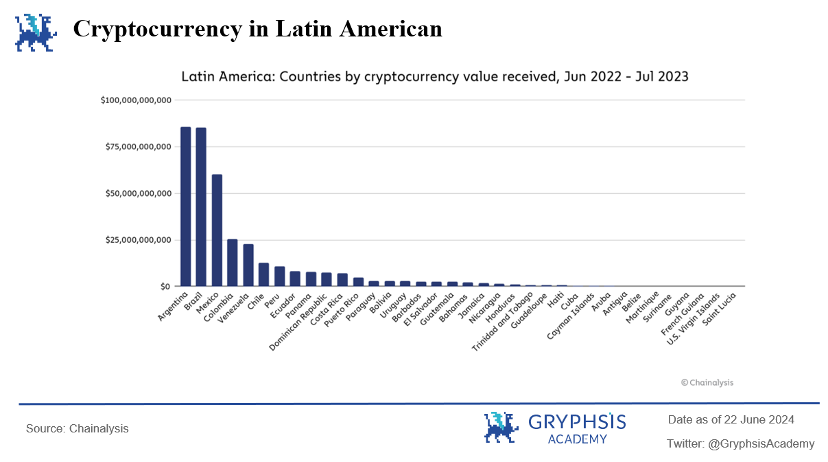

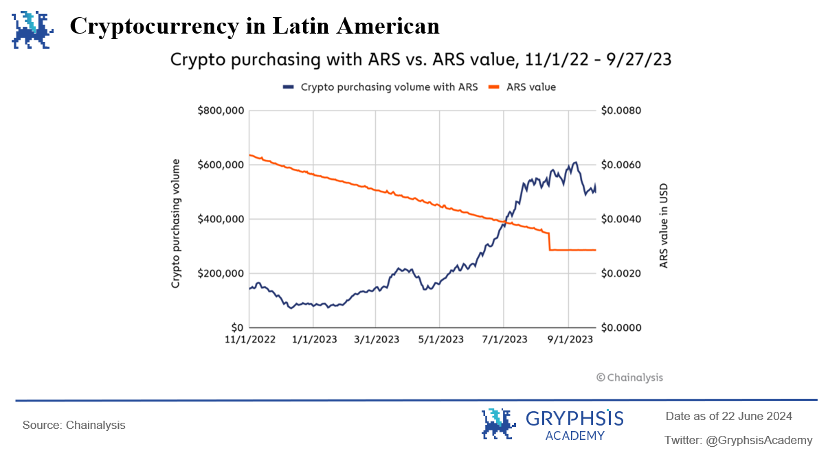

For decades, Argentina has been facing economic difficulties, and the cyclical extreme devaluation of its currency has damaged the savings ability of residents, making daily financial activities difficult. Therefore, Argentina is also one of the most active places for cryptocurrency in Latin America. In 2023, Argentina's inflation rate reached 211.4%, and according to Chainalysis data, approximately 10.9%, or about 5 million people (out of a total population of 45.8 million), use cryptocurrency for daily life payments.

To prevent the devaluation of the peso, Argentinians immediately convert their peso-denominated salaries into USDT or USDC, and almost everyone knows the exchange rate between the dollar and the peso. Similarly, Turkey is also one of the places where cryptocurrency is developing rapidly. Therefore, in places where there is a demand for devaluation, cryptocurrency becomes a "hard currency" where it is easier to carry out cryptocurrency-related payment businesses, as long as it is allowed by laws and regulations.

And for Venezuela, cryptocurrency is a weapon against dictatorship. During the COVID-19 pandemic in 2020, the interim government led by Guaidó decided to provide direct assistance to the country's doctors and nurses using cryptocurrency. The reason is that the corruption of the Maduro regime and its control over banks made it difficult to provide international aid through normal channels. The plan directly helped 65,000 doctors and nurses, at a time when the average salary for doctors was $5 per month. Using cryptocurrency for aid payments allowed each person to receive $100. Thus, the decentralized cryptocurrency payment method effectively supported the local democratic movement.

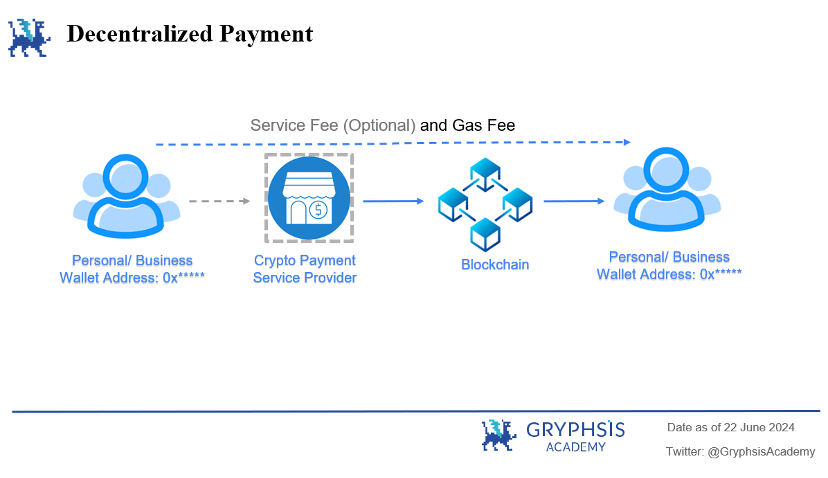

Web3 payments are based on blockchain technology, allowing cryptocurrency to be transferred on the blockchain network as long as the recipient's "wallet address" is known, and can be viewed and traced in real-time, achieving decentralized peer-to-peer payments. This implementation path addresses issues in traditional payments such as low transparency, long transaction settlement times, and high costs due to multiple institutional involvement.

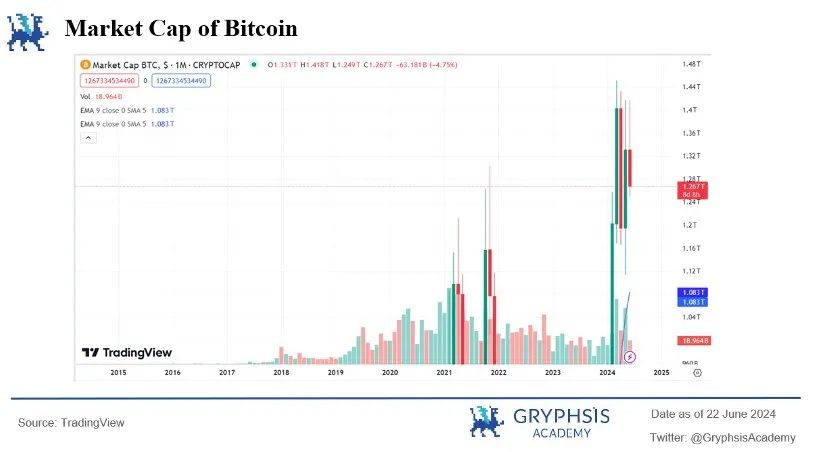

With the approval of BTC ETF, the halving of BTC, and the expected launch of ETH ETF, more and more countries are including cryptocurrency payments in their regulatory scope, and more individual and institutional funds are pouring into the cryptocurrency market. As of June 23, the BTC market size has reached $1.27 trillion, while Ethereum has reached $15.2 billion.

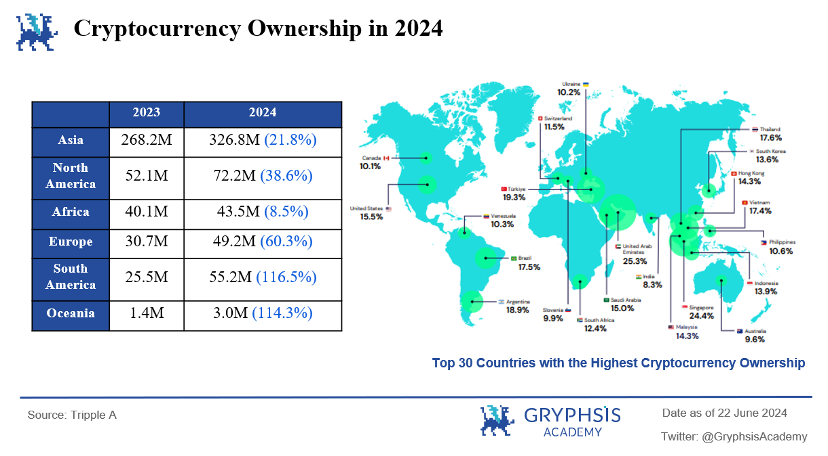

According to a report by Triple A, as of 2024, the global penetration rate of cryptocurrency is 6.9%, with approximately 560 million people worldwide owning cryptocurrency, a 33% increase from the previous year's 420 million. Asia has the most cryptocurrency holders, while South America and Oceania have the fastest-growing share (116.5%). Dubai has the highest population penetration rate at 25.3%, making it the country with the highest proportion of cryptocurrency holders, coupled with its advantages in financial free zones, personal income tax, and capital gains tax exemptions, explaining why Dubai has become the headquarters for many exchanges and cryptocurrency companies in the past two years.

Therefore, whether it is the region with the highest population share or the region with the fastest-growing population share, it is essentially the result of relaxed policies and the need for real transactions, which will provide a great opportunity for exploration and development of cryptocurrency payments.

From an enterprise perspective, in the traditional field, well-known brands in the physical economy such as Starbucks, Coca-Cola, Tesla, and Amazon have embraced cryptocurrency, and the adoption rate and consumer familiarity of cryptocurrency in the mainstream market are gradually increasing. This year, more traditional enterprises have started accepting cryptocurrency and expanding their payment methods. Ferrari has now partnered with Bitpay to accept Bitcoin, Ethereum, and USDC payments in the United States, and plans to expand this option to Europe and other regions in early 2024. In Singapore, Grab users can now order rides and food using Bitcoin, Ethereum, Singapore Dollar stablecoins, USDC, and USDT in their daily lives. Therefore, when industry giants on the B-side start adopting cryptocurrency payments, this not only signifies recognition of the cryptocurrency industry itself, but also opens the door to cryptocurrency payments for C-side users with the endorsement of the credibility of B-side enterprises.

From a user perspective, in 2021, the largest cryptocurrency exchange in the world, Binance, had only 3 million registered users. However, by June 2024, Binance's registered user base had surged to 200 million, with a daily trading volume of $189 billion. This significant growth proves that more and more people are joining the ranks of cryptocurrency users, and cryptocurrency payments are gradually becoming a vast blue ocean.

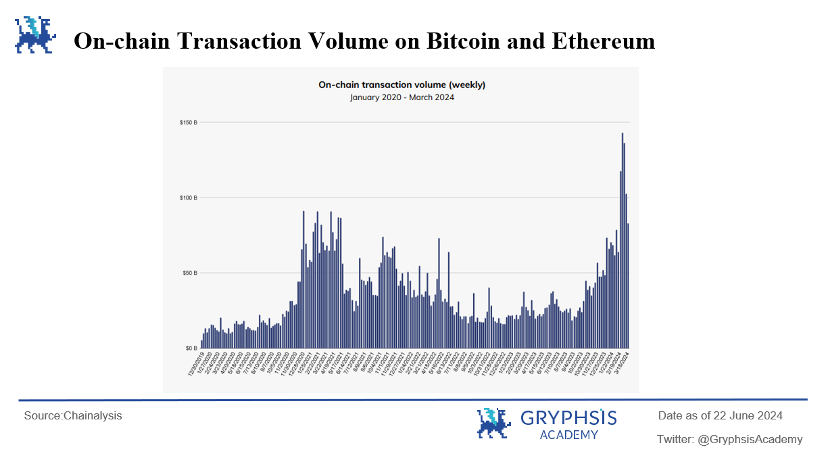

- From on-chain data, from January 2020 to March 2024, on-chain transaction volume and transaction activity continued to grow. Driven by a series of positive events, these indicators have repeatedly reached historical highs, and are about to surpass the $150 billion mark.

In the Web3 field, many project parties and exchanges have seen the industry's upward trend and the huge opportunity for cryptocurrency payments, and have accelerated the application for payment licenses in various regions, expanded card issuance businesses, and other businesses linking Web3 payments with the real economy, while accelerating the construction of exchanges and on-chain wallet settings.

Recently, Coinbase announced the launch of a self-hosted wallet platform, which integrates asset and identity management, purchasing, sending, exchanging, NFTs, and transaction history, providing its users with a more convenient on-chain transaction path. This not only provides more convenience for Coinbase's user base but also becomes an important part of the Onchain Summer event, further promoting the development of Web3 payments.

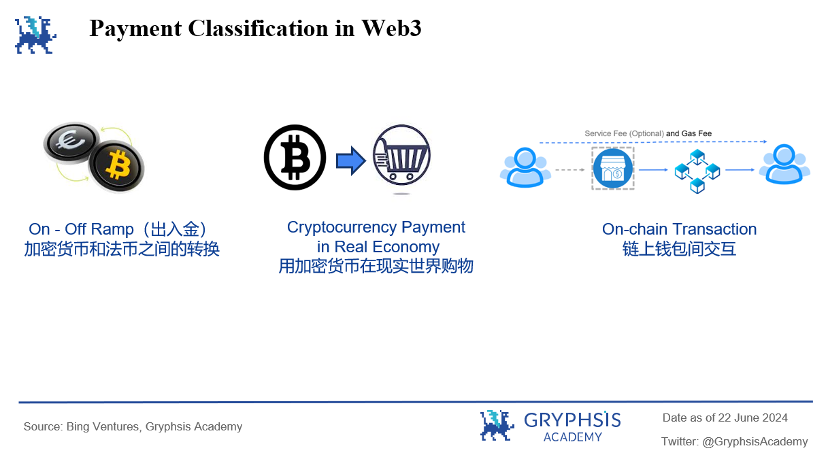

Definition:

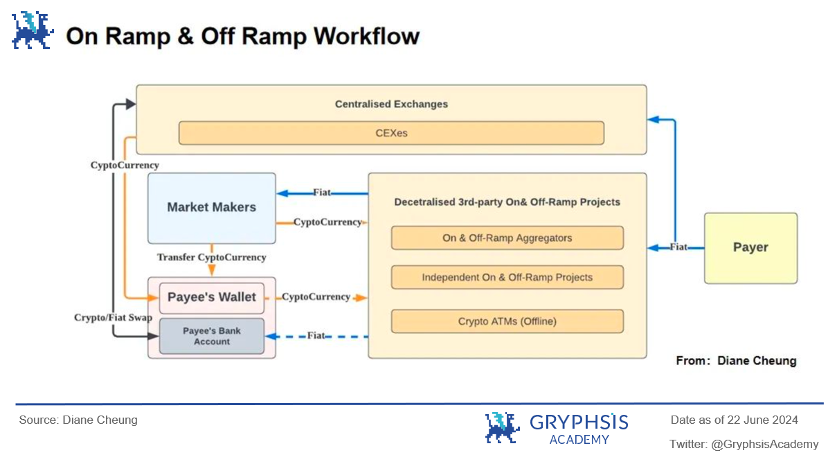

Refers to the process of converting fiat currency (such as USD, EUR, etc.) into cryptocurrency. This process is equivalent to the entrance into the cryptocurrency economy. The payer transfers fiat currency into cryptocurrency through centralized exchanges or decentralized deposit and withdrawal platforms of third parties. Centralized exchanges can directly convert it into cryptocurrency and transfer it to the on-chain wallet; decentralized deposit and withdrawal platforms of third parties exchange cryptocurrency through market makers. When the market maker receives fiat currency, they will transfer an equivalent amount of cryptocurrency to the payer's on-chain wallet.

The market makers here are usually cryptocurrency-friendly banks (such as the now-defunct Silvergate Bank, Silicon Valley Bank, and Signature Bank). After the closure of these banks, more stablecoin issuers (Tether, Circle), and payment service providers (BCB Group) have taken on the role of liquidity providers.

Deposit Methods:

- Centralized Exchanges: Users can create accounts on centralized exchanges after completing KYC, and purchase cryptocurrency with fiat currency through bank accounts, credit cards, or e-wallets.

- Peer-to-Peer Platforms: These platforms directly connect buyers and sellers to exchange fiat currency for cryptocurrency. Transactions are usually held by a third party until both parties agree on the operation.

- Over-the-Counter (OTC) Desks: OTC desks facilitate large cryptocurrency transactions directly between buyers and sellers, often used by institutional investors or high-net-worth individuals.

- Decentralized Cryptocurrency Wallets: The most common type of cryptocurrency wallet is a self-hosted wallet, allowing users to have full control over their cryptocurrency as it does not involve third parties.

Entities Involved in Deposits:

Centralized exchanges, third-party decentralized deposit and withdrawal platforms, banks, liquidity providers (cryptocurrency-friendly banks, stablecoin issuers, payment service providers)

Fee Structure:

- Payment Channel Fees: Fees charged by credit card issuers, Paypal, Apple Pay, etc.

- Fiat-to-Cryptocurrency Exchange Rate Fees: USD and USDT are usually not 1:1, and intermediaries often profit from the difference.

- Network Fees: Gas fees are required when transferring from a self-hosted wallet to another wallet address.

Definition:

Contrary to deposits, withdrawals refer to the process of converting cryptocurrency back into fiat currency. Users can sell their cryptocurrency holdings, convert them into traditional currency, and then withdraw to their bank accounts or other payment methods. This process is equivalent to the exit from the cryptocurrency economy.

Entities Involved in Withdrawals:

Centralized exchanges, third-party deposit and withdrawal platforms, banks/card issuers, liquidity providers (cryptocurrency-friendly banks, stablecoin issuers, payment service providers)

Withdrawal Methods:

- Centralized Exchanges, Peer-to-Peer Platforms, OTC, Cryptocurrency Wallets

- Cryptocurrency Debit Cards (Virtual and Physical): Debit cards associated with cryptocurrency wallets or platforms can convert cryptocurrency into fiat currency for regular spending.

Fee Structure:

- Transaction Fees: Service providers (exchanges or third-party deposit and withdrawal platforms) may charge a transaction fee for withdrawals.

- Cryptocurrency-to-Fiat Exchange Rate Fees: Currency conversion during withdrawals (e.g., converting USD to EUR) may incur exchange losses.

- Bank Fees: Banks receiving funds may charge fees for incoming funds.

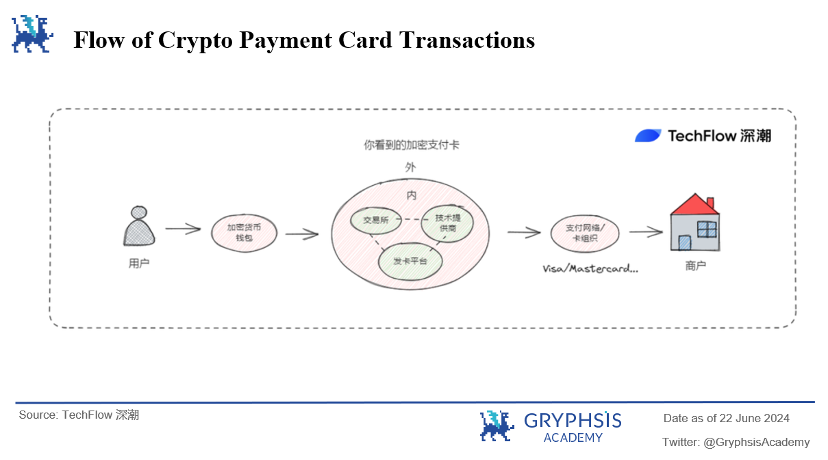

Traditional payment card issuers or Web3-native payment card issuers support the use of cryptocurrency in the physical economy. There are four main entities involved: technology service providers assisting card issuers, issuers (traditional card issuers, Web3-native card issuers), and card organizations.

In the current market environment, prepaid cryptocurrency debit cards are quite popular: they do not need to be linked to existing bank accounts and only require the pre-conversion of cryptocurrency into fiat currency to load onto the card.

Entity 1: Virtual/Physical Card Technology Service Providers

In the Web2 world, issuing credit and debit cards was the domain of banks, requiring high technological and qualification thresholds. However, in the cryptocurrency payment card field, this is not the case. Card technology service providers offer "issuance as a service" solutions. When users see a cryptocurrency card with a VISA logo, for example, it is actually a collaboration between the card issuer and the technology service provider. The API of the card technology service provider is integrated with payment networks such as Visa and MasterCard, and has established partnerships with card issuers and other industry players, providing users with real-time transaction authorization and fund conversion services.

Demand for card issuance only requires compliance and licensing conditions, and the card issuer can issue and manage cryptocurrency credit/debit cards by using the technology service provider's API or SaaS solution.

* Technology service providers often need to hold licenses in multiple regions and provide services including necessary security technology, payment processing systems, and user interfaces to support cryptocurrency card issuance, currency conversion and payment, transaction monitoring, and risk control.

Entity 2: Traditional Payment Card Issuers

Visa has partnered with Web3 infrastructure provider Transak to launch cryptocurrency withdrawals and payments through the Visa Direct solution. Users can directly withdraw cryptocurrency from wallets such as MetaMask to a Visa debit card, convert cryptocurrency into fiat currency, and use it to pay at Visa's 130 million merchants. Therefore, the absolute advantage of traditional payment card issuers in cryptocurrency payments lies in their historical payment licenses, brand credit endorsements, large user and merchant traffic, and absolute financial strength.

Entity 3: Web3 Payment Card Issuers

Hardware wallet providers such as Onekey and Dupay launched virtual and physical cards last year, providing mainland users with the possibility to purchase OpenAI ChatGPT. The business model mainly revolves around earning card issuance fees and transaction fees, and different levels of cards have different limits and fee standards. In addition to Web3-native payment card issuers, major exchanges have also introduced business models that earn fees and card issuance fees based on their own business forms.

For example, Binance's cryptocurrency payment card spending can earn a certain amount of BNB cashback, similar to "cash back" in the real world. Crypto.com's cryptocurrency payment card allows users to earn waived card issuance fees and other payment benefits by staking different amounts of the platform's token CRO. Leveraging their user traffic and brand endorsement, exchanges are attempting to expand more C-side payment scenarios through card issuance business, given the natural consumption scenarios of post-trading withdrawals.

The logic behind this business is that exchanges themselves have payment scenarios after trading withdrawals, and compared to traditional payment card issuers, the educational cost for users to use cryptocurrency payment cards is lower. From a user perspective, the exchange app can directly interact with the card using the existing trading product matrix, greatly improving the user experience for switching between different platforms for transfers, deposits, and other uses.

Entity 4: Card Organizations

VISA and Mastercard authorize their networks to technology service providers, earning more profits through increased cryptocurrency card transaction volume and overseas transactions. The more transactions and the larger the amount, the higher the revenue they receive in fees. Therefore, they do not need to issue cards themselves, as they can earn "authorization fees" based on their payment networks and credit card brand endorsements.

Evaluation:

Although the roles in the card issuance business chain are different, each participant has its own logic and advantages in doing card issuance business. For example, the virtual/physical card issuance technology service provider sees the SaaS business as a lucrative opportunity. Once the licensing and technology are in place and the trading channels of the Web3 ecosystem are aggregated, this business model can be replicated effortlessly. Its audience is very broad, not only providing services to Web3-native card issuers, but also expanding its compliance and technological advantages to other payment business areas. Web3-native card issuers can earn transaction fees from buying and selling cryptocurrencies or card payments through an outsourced technology model, making it easier to reach more Web3-native communities and having lower customer acquisition costs for users with cryptocurrency usage habits. Traditional card issuers or traditional payment giants have capital accumulation, the widest user base, and strong brand endorsements. If card issuance becomes easier to gain acceptance from virtual card payment users, non-crypto users, and earn B2B authorization fees from payment service providers, etc.

Traditional/Web3-related third-party payment platforms expand deposit and withdrawal and cryptocurrency payment businesses, enabling the use and consumption of cryptocurrency in the physical economy. The following two platforms have their own usage advantages: Revolut app supports fiat currency exchange and card payments in traditional payments, and naturally can also be a platform for exchanging cryptocurrency for fiat currency. Binance Pay, backed by the largest cryptocurrency exchange Binance, naturally has a demand for consumption, forming a closed loop for cryptocurrency deposits, trading, withdrawals, and consumption.

Revolut: The fintech company and global neobank Revolut was founded in the UK in 2015, offering services such as transfers and payments, with over 40 million users worldwide. In March 2024, the company launched Revolut Ramp, a service that allows Revolut users to purchase cryptocurrencies in their wallets through a partnership with MetaMask developer Consensys, and trade between the platform and their Revolut accounts without paying additional fees or being restricted. At the same time, within the traditional payment app, Revolut links the Revolut card to the user's cryptocurrency account, automatically converting the cryptocurrency into the purchasing currency for payments.

Binance Pay: Shopping platforms can choose from a variety of cryptocurrencies to purchase gift cards for different retail brands and games according to their preferences, enabling consumption in the physical economy. For example, Coinbee:

Source: @Coinbee

On-chain payments are also based on the demand for a certain payment scenario in the Web3 world, usually arising from participation in project activities and transactions.

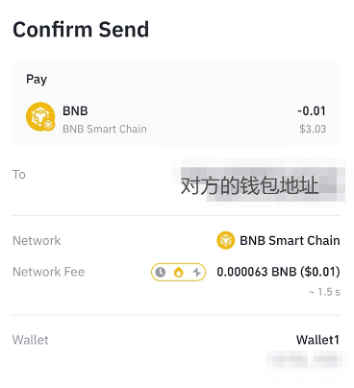

- Payments and Transfers: Web3 wallets (using Binance Web3 wallet as an example) provide peer-to-peer payment and transfer functions, allowing for cross-space transfers with just the recipient's wallet address, usually incurring a network fee (Network Fee/Gas Fee) for receipt within a few minutes. Users can easily transfer assets globally quickly and at low cost.

Source: @binance

- DeFi/NFT: Users can interact with DeFi applications through Web3 wallets, engaging in cryptocurrency deposits and loans, borrowing, liquidity mining, and purchasing/trading NFTs and other digital assets.

- DEX: Web3 wallets support users in trading cryptocurrencies on decentralized exchanges, which do not rely on centralized order books but match trades through smart contracts.

- Cross-chain Interaction: Multi-chain wallets support users in transferring assets between different blockchains, achieving interoperability between different blockchain ecosystems.

- GameFi: In GameFi, Web3 wallets can be used to purchase virtual goods, land, or other in-game virtual assets.

- Social Networking and Content Creation: Web3 wallets support users in content creation and monetization on decentralized social platforms, as well as receiving tips and payments.

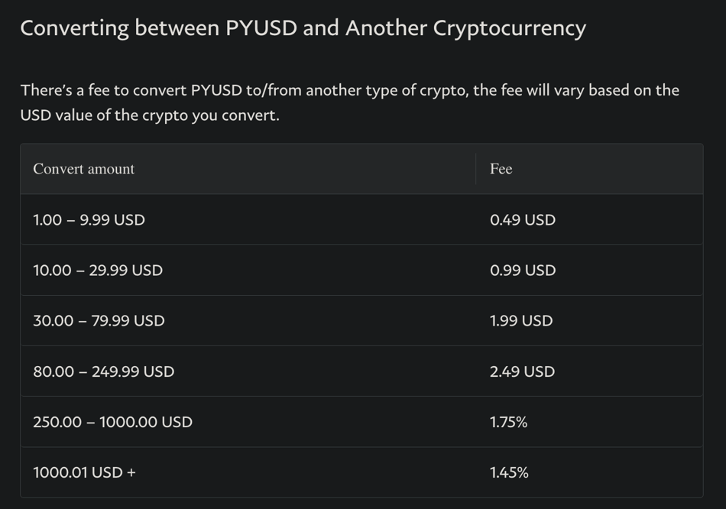

In August 2023, PayPal launched its first stablecoin, PYUSD, with Paxos as the issuer, which regularly provides proof of reserve assets. The stablecoin PYUSD is issued on Ethereum (currently also available on Solana). PYUSD maintains a 1:1 value with the US dollar and can be exchanged within the PayPal ecosystem. PYUSD is backed by US dollar deposits, short-term US government bonds, and similar cash equivalents to ensure its stability, unaffected by fluctuations in other cryptocurrencies.

Use Cases: Mainly used for gaming, remittances, and as a payment medium on Web3 platforms and decentralized exchanges; currently, PYUSD is only available to US users, with trading pairs available on Coinbase. Due to limited supported public chains and regions, as well as limited usage scenarios, the stablecoin's usage scope is still to be expanded.

- Transfers: Users can transfer with zero fees using PYUSD.

- Payments: PYUSD is used for payment settlement when purchasing goods.

- Cryptocurrency Conversion: PYUSD can be converted to other cryptocurrencies supported by PayPal, with fees varying depending on the amount converted, ranging from 1.45% to 4.9%, which is relatively high. Additionally, as it currently only supports the Ethereum chain, the network fees for transferring the stablecoin can be very expensive.

Source: @Paypal

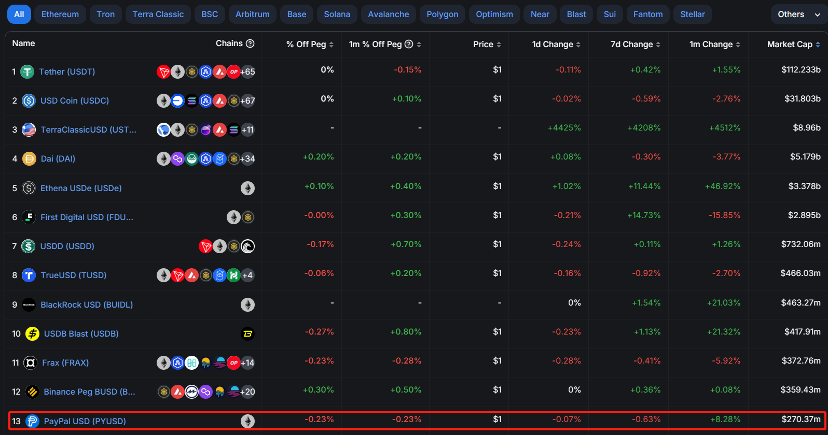

Market Value: The market value of the stablecoin issued by PayPal is currently $270.37 million, ranking 13th in the stablecoin market. The total market value of stablecoins is $170.2 billion, with PayPal's stablecoin accounting for 0.15% of the market share, while Tether has the highest market share at 65.9%. This indicates that even when a payment giant enters the cryptocurrency industry, it is difficult to take the lead in the cryptocurrency market quickly due to late entry, limited involvement in public chains, regional restrictions, and limited usage scenarios. However, PayPal is also working to expand its application scope, with Solana already launched, and the development goal for PYUSD is to be listed on major exchanges, achieve higher circulation, and aim for compatibility with the Web3 and Web2 ecosystems.

source: @Defilama

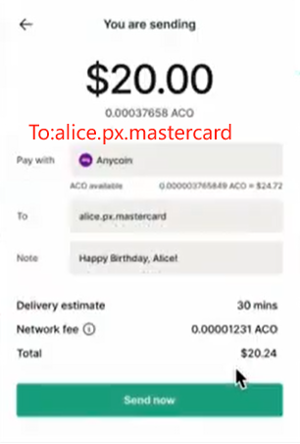

Mastercard has launched the Mastercard Crypto Voucher, marking the first peer-to-peer pilot transaction in collaboration with exchanges. The feature of this system is the use of aliases instead of lengthy blockchain addresses when making transfers. This new system aims to simplify cryptocurrency transactions for exchange users and provide a more user-friendly peer-to-peer transfer method.

Pilot scope: Mainly in Europe and Latin America, users in Argentina, Brazil, Chile, France, Guatemala, Mexico, Panama, Paraguay, Peru, Portugal, Spain, Switzerland, and Uruguay will be able to make cross-border and domestic transfers across multiple currencies and blockchains. The choice of these locations for the pilot is mainly due to the relatively relaxed cryptocurrency environment in these countries, as well as the significant demand for cryptocurrencies in the Latin American region due to currency devaluation.

Collaborating exchanges: Exchanges such as Bit2Me, Lirium, and Mercado have already enabled real-time trading functionality.

Source: @Mastercard

Usage steps: Exchanges first conduct KYC according to the Mastercard Crypto Voucher standard. At this point, the user will receive an alias to send and receive funds across all supported exchanges. When the user initiates a transfer, the Mastercard Crypto Voucher will verify the validity of the recipient's alias and whether the recipient's wallet supports digital assets and the relevant blockchain. If the receiving wallet does not support the asset or blockchain, the sender will be notified and the transaction will not proceed, thus protecting all parties from potential financial losses. Finally, the amount is entered for the transfer, and a mobile verification code is required to complete the transfer.

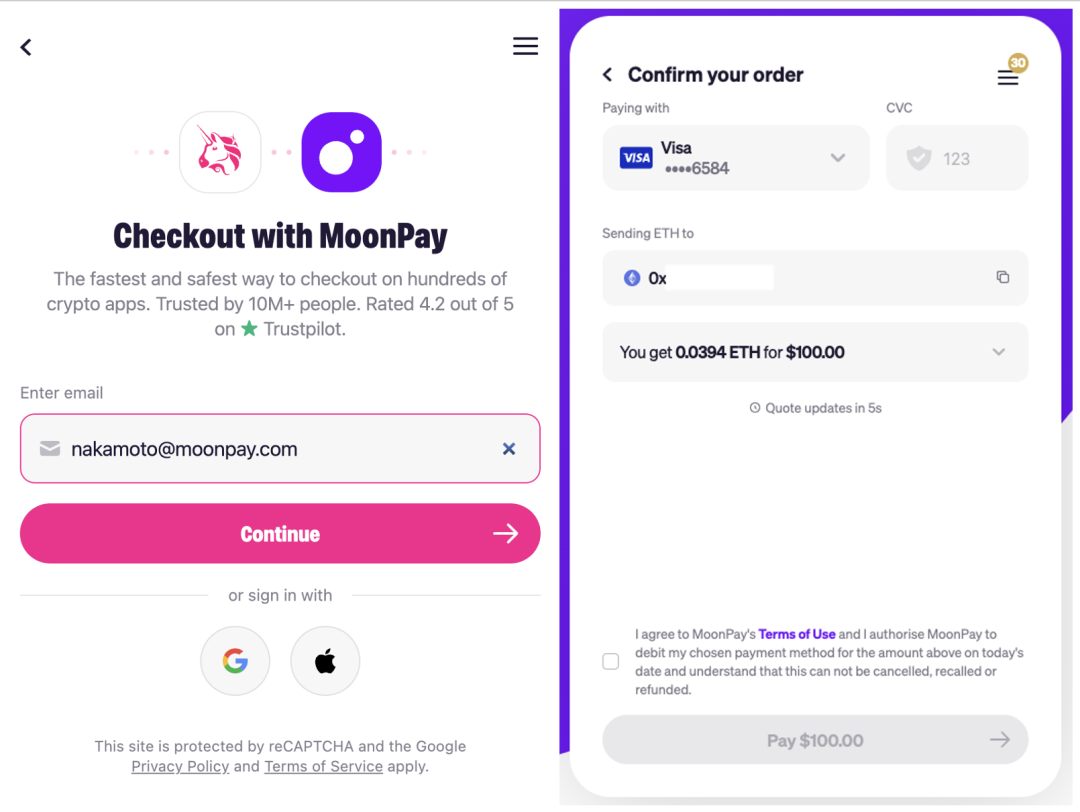

MoonPay, founded in 2019, positions itself as the PayPal for Web3. MoonPay is now one of the few companies licensed and compliant in all states in the United States through an MTL license, in simple terms, it is a cryptocurrency service provider primarily focused on deposits and withdrawals.

MoonPay enables developers to integrate its services into Web3-related applications through API and SDK, establishing connections with centralized exchanges and wallets to provide deposit and withdrawal services.

Users can also purchase NFTs and other digital assets on various Web3 exchanges through the MoonPay app or platforms such as Coinbase, OpenSea, MetaMask, and Bitcoin.com. The service has served over 15 million individual users.

The latest news shows that Moonpay has been integrated into PayPal, allowing US users to purchase over 110 cryptocurrencies using their existing PayPal balance and bank cards.

- Funding history: The first round of funding raised $555 million, led by Tiger Global Management and Coatue Management, with a valuation of $3.4 billion. This includes a total of 60 investors, including Justin Bieber, Maria Sharapova, and Bruce Willis.

- Access channels: Moonpay platform (KYC), partnered centralized exchanges, and wallet service providers (including Metamask, Bitcoin.com, OpenSea, Uniswap, Sorare, etc.)

source: @Moonpay

- Business Scope

○ Deposits and Withdrawals: MoonPay provides individuals with the ability to buy or sell cryptocurrencies with fiat currency. It offers deposit services for 34 fiat currencies to 126 cryptocurrencies and withdrawal services for 22 cryptocurrencies in over 100 countries. It supports credit and debit cards, bank transfers in Euro/Pound/Dollar, local payment methods such as PIX and Yellow Card.

○ Cryptocurrency Trading Platform: MoonPay provides a secure non-custodial cryptocurrency trading platform, allowing users to exchange different cryptocurrencies without paying fees. Users can connect their crypto wallets to MoonPay for cross-chain exchanges. As of April 2024, MoonPay supports wallets such as Trust Wallet, Ledger, MetaMask, Rainbow, Uniswap, and Exodus. In terms of deposits and withdrawals, MoonPay focuses on establishing connections with major platforms (such as exchanges and wallets) to acquire user traffic, while Alchemy Pay's deposit and withdrawal services focus more on expanding different local payment channels and strengthening the product's localization capabilities.

○ Enterprise-level Cryptocurrency Payments: MoonPay supports various payment methods for enterprise-level cryptocurrency transactions. Users can embed the API into their enterprise applications, with payment methods ranging from credit cards such as Visa and Mastercard to wire transfers, bank transfers, and Apple Pay. MoonPay has a 50-person anti-money laundering monitoring system, fraud engine, and anti-fraud stack to handle credit card refunds, fraud, or dispute issues for enterprise clients.

○ NFT-related Services:

MoonPay Concierge Service: Provides high-end NFT purchase and custody services for high-net-worth clients. MoonPay has close partnerships with Yuga Labs and others to promote blue-chip NFTs such as BAYC and CryptoPunks through concierge services to celebrity clients.

NFT Checkout: Moonpay collaborates with platforms such as OpenSea, Magic Eden, ENS, and Sweet.io to provide NFT purchase and sale services. Users can buy NFTs using credit or debit cards, as well as payment methods like Apple Pay and Google Pay, without needing to purchase cryptocurrency first.

HyperMint: A self-service infrastructure platform and Web3 API provided through a no-code platform for creators and brands. Users can:

i. Write, design, and deploy smart contracts ii. Create, manage, mint, and sell tokens to end users iii. Manage funds, royalties, and distribute NFTs on a large scale

- Moonpay's Business Model:

○ Fees, Service Charges, NFT Minting/Concierge Fees: MoonPay earns revenue by extracting a certain percentage from total transactions. The main transaction types are buying and selling cryptocurrencies and NFTs, with service fees and transaction commissions for concierge services and NFT minting fees. The company charges a 4.5% fee for buying and selling cryptocurrencies with a credit card and a 1% fee for bank transfers (minimum $3.99), making it less friendly for small and frequent deposit and withdrawal users. For NFTs, it charges a 4.5% fee, with a minimum of $0.50; high-net-worth users of NFTs also incur high service fees, and more.

○ Exchange Rate Spread: MoonPay earns income through the exchange rate spread when users deposit and withdraw, as well as buy or sell cryptocurrencies.

- API Integration Fees: MoonPay provides an API that allows third-party platforms and developers to integrate cryptocurrency purchasing functionality into their applications. MoonPay may charge integration fees or subscription fees to these partners to access their API and utilize their services.

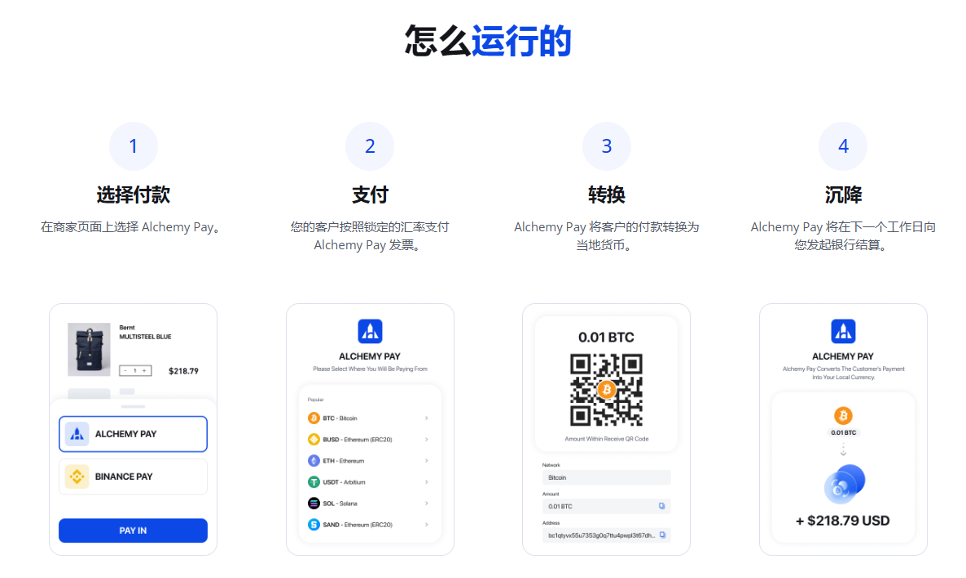

Alchemy Pay was founded in Singapore in 2017 and is a cryptocurrency payment gateway that serves both businesses and individual users. It supports payments in 173 countries/regions, with a primary service area in Southeast Asia, which sets it apart from Moonpay. Due to the varying economic levels in Southeast Asian countries, each country supports different mainstream payment methods, which requires Alchemy Pay to aggregate a wider variety of payment methods in different countries to actively explore and improve user experience in developing countries. Alchemy Pay provides a one-stop payment solution.

Recently, Alchemy Pay invested in LaPay UK Ltd and obtained an authorized payment institution license regulated by the FCA. The company also partnered with Victory Securities in Hong Kong to provide virtual asset trading and advisory services, especially for new Bitcoin and Ethereum spot ETFs. This shows that Alchemy Pay is responsive to market trends and expands its services accordingly.

- Funding Background: Alchemy Pay completed a $10 million funding round at a valuation of $400 million, with investment from DWF Labs.

- Alchemy Pay's Business:

a. Fiat and Cryptocurrency Deposits and Withdrawals:

Provides channels for deposits, withdrawals, and purchasing cryptocurrencies. Currently, over 50 cryptocurrencies can be deposited into bank accounts in over 50 fiat currencies. Unlike Moonpay, which is more popular in the European and American markets, Alchemy Pay is more popular in Southeast Asia and Latin America, where electronic wallet payments are more common, requiring integration of more payment channels to actively explore and improve user experience in developing countries. The client business mainly involves integrating APIs for Dapp to facilitate deposits and withdrawals.

b. Payment Gateway:

Enterprise-level payment gateway: Alchemy Pay provides online payment and banking solutions within the regulatory framework, allowing traditional and Web3 enterprises to manage multiple fiat currency accounts on the platform and facilitate conversions between fiat and cryptocurrencies. Users on the payment side and the receiving side can choose to use cryptocurrency/fiat as a payment method. Additionally, Alchemy Pay provides customized cryptocurrency payment services for large enterprises.

Source: @Alchemy Pay

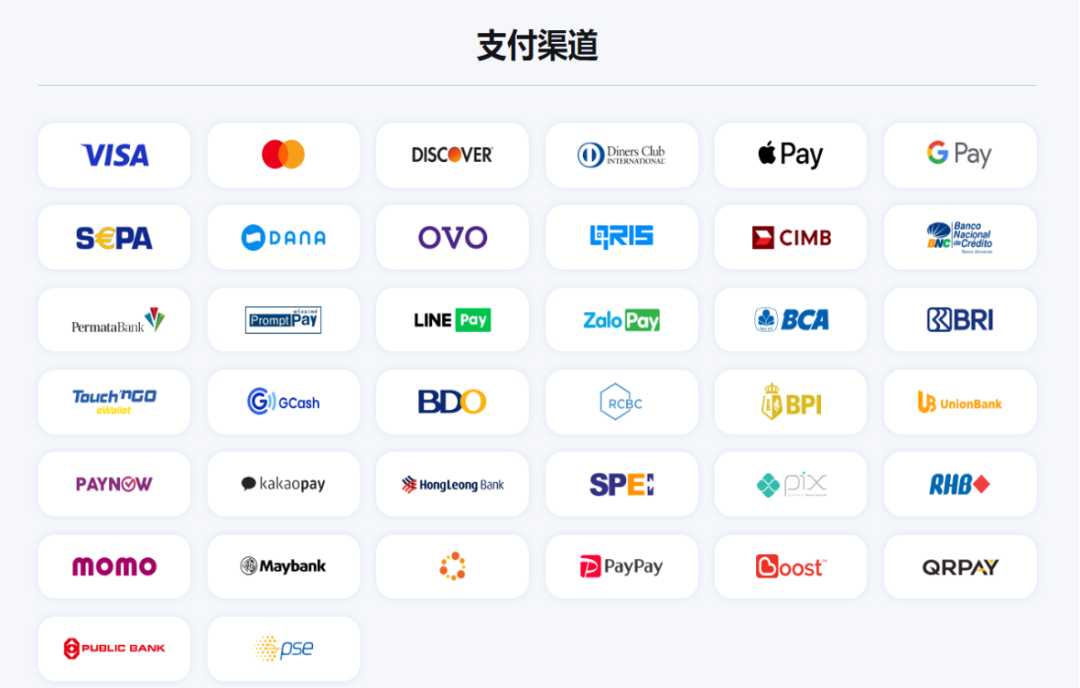

Personal Payments: Supports all popular global and local payment methods, including debit cards, credit cards, bank transfers, mobile wallets, etc.

Source: @Alchemy Pay

c. Cryptocurrency Card Issuance Technology Solutions:

Alchemy Pay's virtual card is a Mastercard prepaid card that allows users to directly top up USD with various cryptocurrencies.

- Currently supported currencies: USDT, USDC, ETH, BTC, and platform tokens

- Supported networks: Trc20, Bep20, Erc20, Sol, Bitcoin, Polygon

- Current supported card BINs: 558068 (Mastercard), 531847 (Mastercard), 404038 (Visa)

Source: @Alchemy Pay

Collaboration Model: Alchemy Pay collaborates with card issuers to generate custom branded credit cards for merchants. Users can top up USD directly with USDT and platform tokens for spending, and can instantly convert the remaining amount to a cryptocurrency wallet.

Use Cases: Can be used for online platform purchases worldwide that support Mastercard (such as Amazon, eBay, etc.), and can be linked with Apple Pay for offline store payment scenarios.

- Alchemy Pay's Business Model

○ Transaction fees for individual and enterprise deposits and withdrawals, exchange rate spreads for fiat and cryptocurrency conversions

○ Integration service fees for APIs provided to physical and Web3 enterprises

○ Card issuance technology service fees

○ Profits from platform tokens: $ACH

- Project Evaluation

In 2024, in terms of business, Alchemy Pay will mainly strengthen deposit and withdrawal services, cryptocurrency card services, launch innovative Web3 bank accounts, and obtain necessary regulatory licenses.

In terms of licensing acquisition, Alchemy Pay is expected to submit and obtain over 20 licenses globally this year, expanding its business geographically and in depth. Alchemy Pay has gradually expanded from its initial focus on Southeast Asia to Europe. It has currently applied for licenses in Singapore, Hong Kong, the United States, the United Kingdom, South Korea, Indonesia, Australia, and is seeking more compliance certifications through acquisitions or applications.

Therefore, for payment service providers, global regulatory relaxation, the gradual compliance of BTC, and the proactive acquisition of different business licenses in different regions by the project party are very favorable and important. Once a payment service provider obtains a license early on, it opens up a user entry point in a region, making it easier to obtain the most original and extensive B-side resources in that region (not only for enterprises, but also for providing services to banks) and accumulate C-side user awareness. With more resources and accumulation, it is easier to cooperate with more traditional industries and Web3 projects with on-chain transaction needs, and to expand more forms of payment derivative services based on resources and user accumulation.

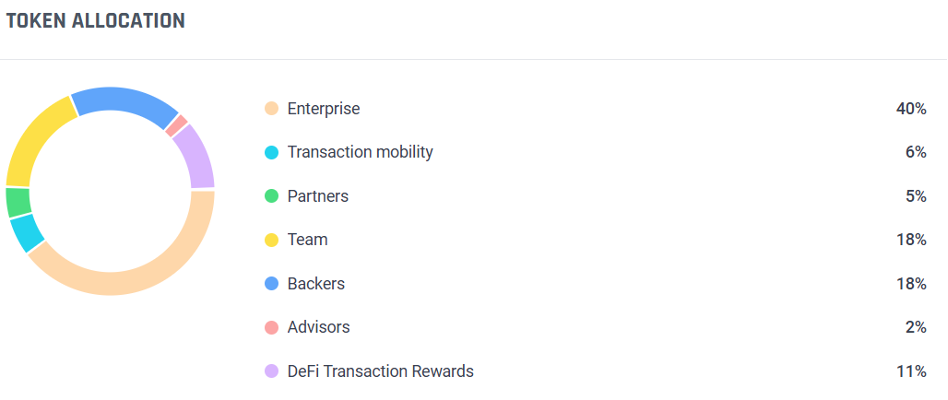

- Token Economics

Source: @Alchemy Pay

Token Use Cases:

Alchemy Pay's token $ACH is a utility token with uses for payment fees, enterprise network fees, participation in DeFi services, governance, and more.

- Payment Fees: Users can enjoy fee discounts when using $ACH for transactions, and they can also receive rebates, discounts, or other forms of rewards through the payment network.

- Enterprise Payment Network: Enterprises can receive enterprise transaction rewards based on their network scale and transaction volume.

- DeFi Rewards: DeFi participants can earn rewards through staking and other DeFi services.

- Governance: ACH holders can gain voting rights for key business decisions and protocol changes based on their holdings; ACH token holdings can be used to facilitate non-governance voting scenarios, such as opinion polls and promotional activities.

Token Economics Evaluation:

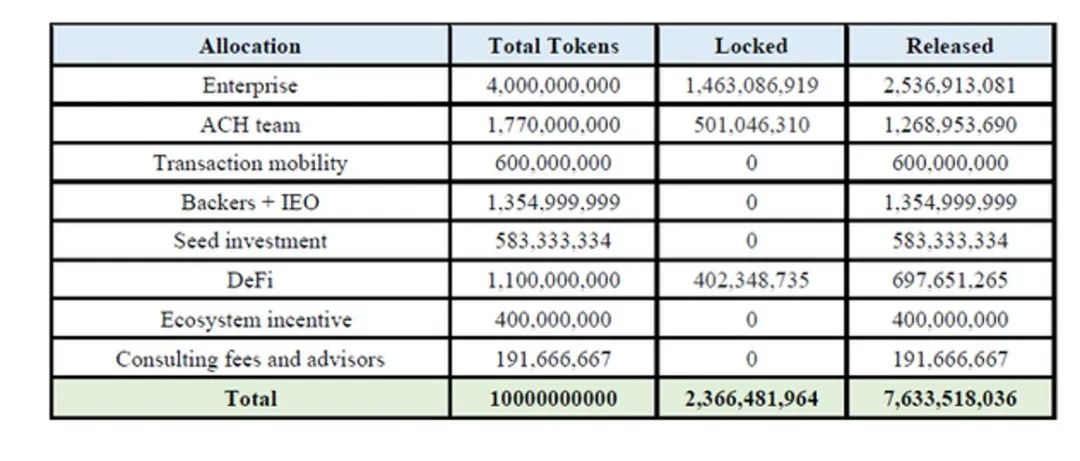

From the token economics chart, we can see that approximately 77.7% of the total token supply has been released. Although there is no token release speed chart, based on the token distribution chart, we find that the seed round, backers, and IEO portions have all been fully released, indicating that institutions in the private placement round (18%) may hold very low-priced chips. Additionally, 40% of the tokens for early participants were distributed through payment mining, which is a double-edged sword. While a high proportion encourages participant involvement, it may also lead to potential selling pressure in the future.

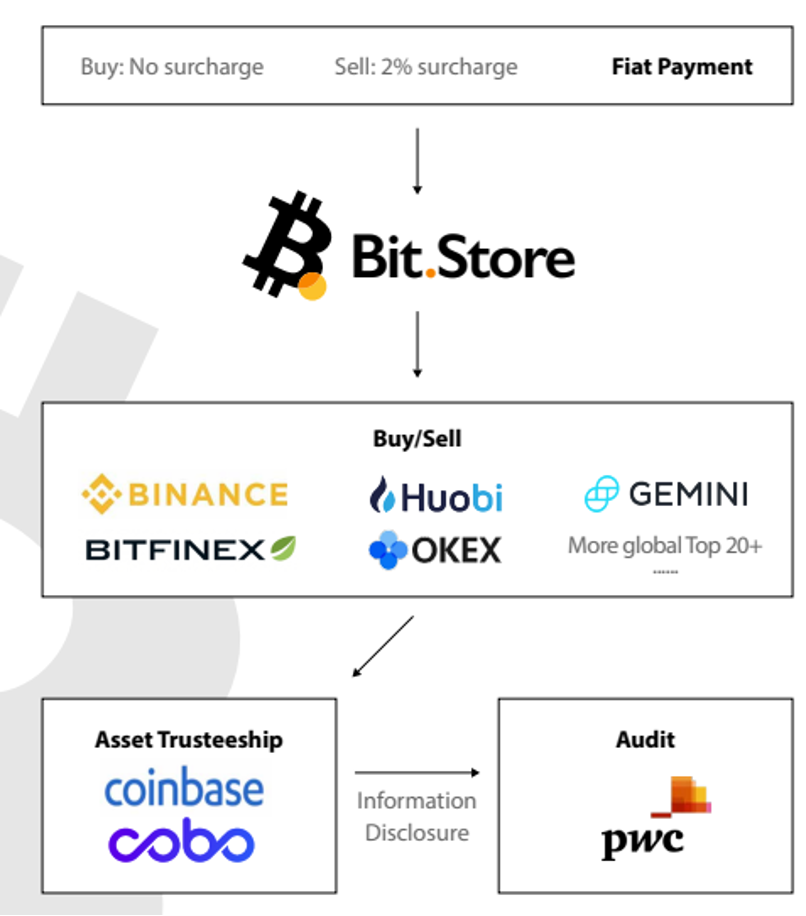

Bit.Store is a cryptocurrency payment card infrastructure solution. Initially, Bit.Store primarily operated as a cryptocurrency exchange platform in the Southeast Asian market, connecting with many large centralized exchanges to buy and sell tokens on the platform. Recently, Bit.Store launched cryptocurrency payment cards, including virtual cards (USD-denominated) and physical cards (EUR-denominated), supported by Mastercard or Visa, with payment technology services provided by Alchemy.

Licenses: Currently holds multiple licenses in various locations, including Hong Kong MSO license; US MSB license; European EMI license; Canadian MSB license; Indonesian trade license/South American trade license, among others. Its payment technology service provider, Alchemy Pay, also holds business licenses in multiple locations, enabling it to conduct payment business in multiple regions. Furthermore, Alchemy Pay acquired a 15% stake in Bit.Store, with the main goal of "filling in the gaps" and expanding the original accumulation of Alchemy Pay in the Southeast Asian region to include payment business in North America, Europe, South America, and other regions.

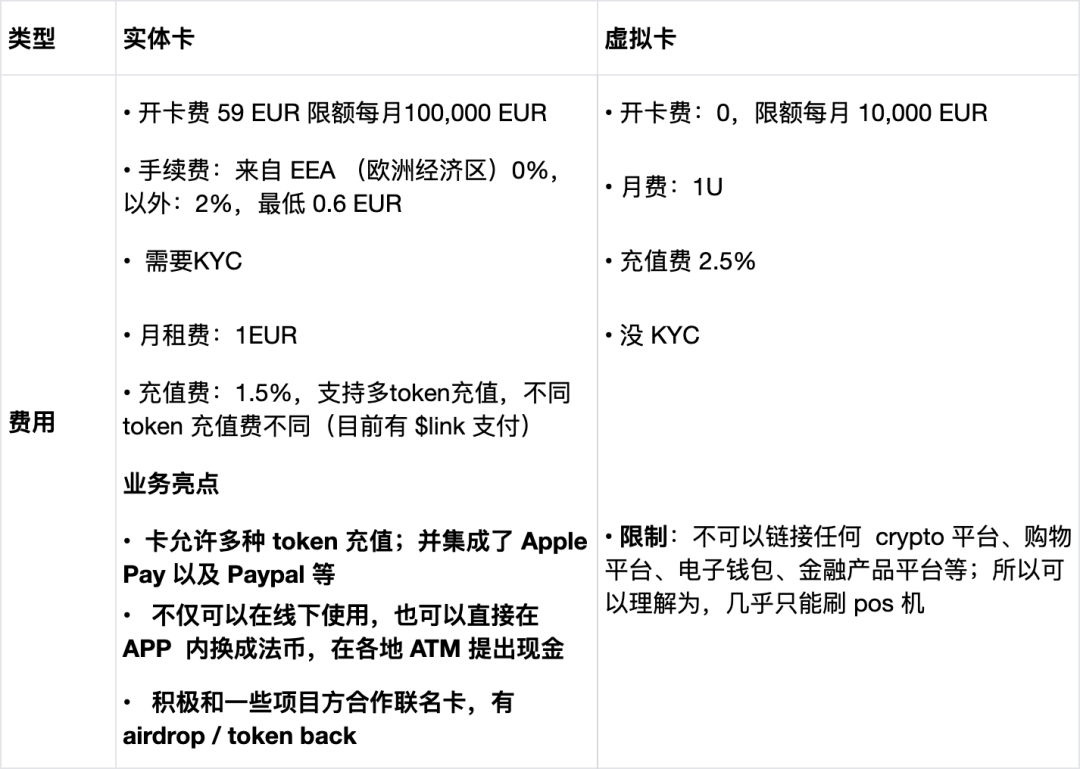

Bit.Store Physical & Virtual Cards: Many card issuers primarily offer virtual cards, but Bit.Store's highlight is that physical cards can be used for ATM cash withdrawals offline.

Source: @Bit.Store

In the case of Bit.Store, we can see that it conducts its business model through earning transaction fees, card fees, exchange rate spreads, and more. Its advantage lies in its diverse licenses in various regions, connecting physical cards to the widest range of traditional online payment channels (such as Apple Pay, Paypal), and providing ATM cash withdrawal services that many card issuers cannot offer offline. In the Web3 direction, it not only relies on large exchanges and custody platforms to provide ample cryptocurrency liquidity but also actively collaborates with projects to launch co-branded cards based on hot narratives.

Ripple is a fintech company that innovatively developed the blockchain protocol Ripple, aiming to facilitate fast, low-cost global transactions of various assets for banks and financial institutions worldwide through the establishment of a decentralized ledger—Ripple Net. Ripple Net is a distributed ledger that provides transaction transparency, immutability, and instant settlement. Its token is $XRP.

- Why Ripple Net is Needed: Challenges in Traditional Bank Handling of Cross-Border Transactions

In traditional banking systems, each bank has its own internal ledger, recording the credit and debt relationships with its customers. Transfers between customers within the same bank are relatively simple and fast, but transfers between different banks become complex, requiring completion through trust relationships or third-party intermediaries. This leads to slow transaction speeds, high costs, and potential errors when handling global transactions.

Example: Suppose customer A at Bank A in the US has $100 and wants to transfer $50 to customer B at Bank B in Indonesia. In traditional banking systems, this transaction may require multiple intermediary banks, involving high fees and several days for settlement. However, through the Ripple ledger, Bank A in the US can directly issue a promissory note representing $50 on the Ripple network, swiftly, at low cost, and in real-time transferring the funds to Bank B in Indonesia.

- Solutions Provided by Ripple Net Ledger Innovation Technology

a. xCurrent: xCurrent allows banks to send real-time messages to each other, confirm payment details, and track payment progress, enabling end-to-end instant settlement.

b. xRapid: xRapid acts as a "liquidity assistant" for banks and payment providers. When there is a need to quickly convert funds between different currencies, xRapid helps them obtain the target currency at a low cost and extremely fast speed. It reduces the need to pre-establish currency accounts in various locations by utilizing XRP liquidity.

c. xVia: xVia handles the remaining complex processes.

In summary, xCurrent serves as a bridge for communication between banks, xRapid acts as a liquidity accelerator, and xVia provides a simplified interface for payment processes. These three products collectively form Ripple's payment ecosystem, aiming to reduce global intermediaries in payments, increase payment speed, lower payment costs, and provide a more secure and transparent decentralized network. Currently, over 100 banks, payment providers, exchanges, and enterprises globally have joined Ripple Net, using services such as real-time remittances, international P2P payments, electronic invoices, global currency accounts, real-time cash pools, and more.

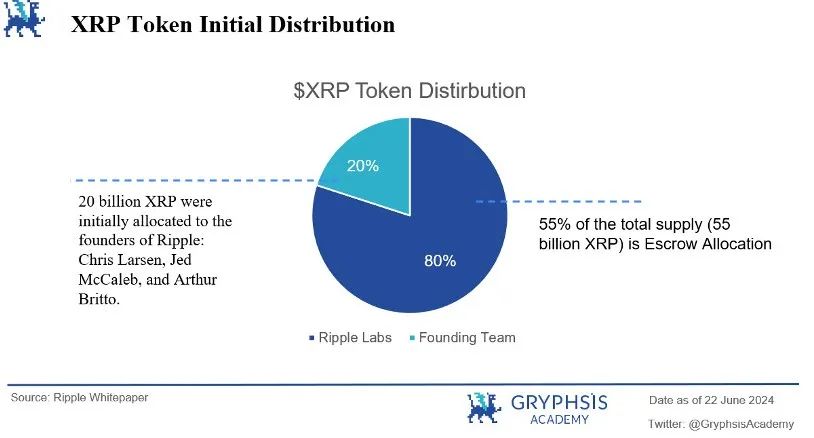

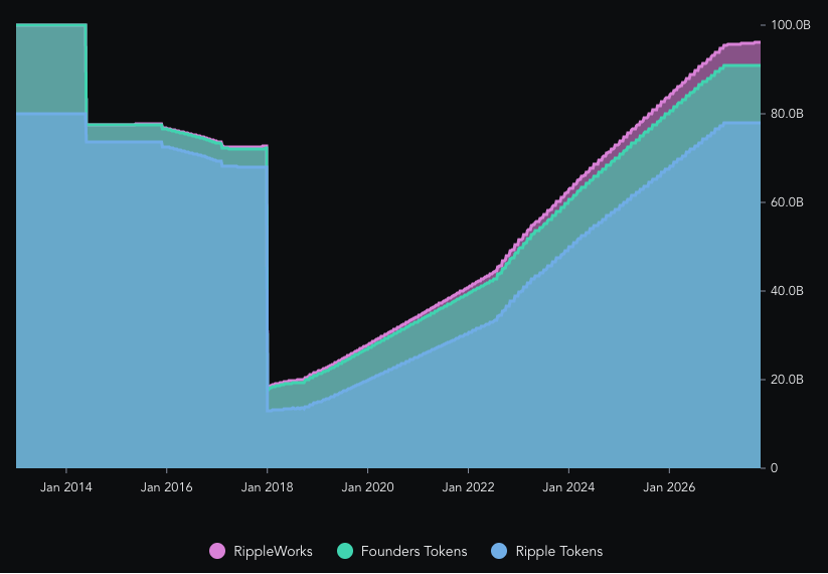

- Token Economics:

The total supply of XRP is fixed at 100 billion tokens, with 20% owned by the token founders and 80% owned by Ripple itself, totaling 80 billion tokens. The initial 25 billion XRP distributed by Ripple has been distributed and sold, and an additional 55 billion XRP has been stored in 55 smart contract escrow accounts, each containing 1 billion XRP tokens.

The contracts systematically release 1 billion tokens to the market each month, with a total cycle of 55 months. At the start of the next unlock, unused XRP will be returned to the escrow account. When each transaction is conducted on XRPL, some XRP is used as a transaction fee and destroyed, creating deflationary pressure. However, due to the low fees, the deflationary pressure is minimal.

Source: TokenInsight

Token Use Cases:

a. Wallet Reserves:

In the Ripple network, each account needs to hold a certain amount of XRP as "wallet reserves" to prevent network congestion and spam transactions, ensuring the smooth operation of the network. The amount of wallet reserves is calculated based on the account's activity level. For example, the more IOUs (debt certificates representing other currencies) held by an account, the more wallet reserves are required.

b. Trust Lines:

Trust lines are a type of debt relationship established between accounts in the Ripple network, allowing one account to borrow assets (such as USD, EUR, etc.) from another account. These borrowed assets exist in the form of IOUs in the Ripple network. Setting up trust lines requires mutual agreement and is usually unrelated to XRP, but XRP can be used as one of the assets in the trust line.

c. Transaction Fees:

When conducting transactions on the Ripple network, transaction fees need to be paid in the form of XRP. Transaction fees are used to maintain the network's operation, including transaction verification and recording. The transaction fees on the Ripple network are relatively low, usually less than 1 cent per transaction, and the transaction speed is very fast, with an average transaction time of about 3 to 5 seconds. A portion of the transaction fees is equivalent to the destruction of tokens.

Evaluation:

The project's token distribution model and release speed chart are not very healthy. Firstly, the token release chart shows that the founders hold a very large portion, approximately around 20%. Secondly, a large portion of the total supply is concentrated in the top 100 wallets, indicating a very high level of concentration.

Based on the token release chart, the token release speed is very fast, with significant fluctuations, and the deflationary mechanism of burning transaction fees is not very effective. Another factor affecting XRP's price is its ongoing legal dispute with the U.S. Securities and Exchange Commission (SEC). The lawsuit accuses Ripple Labs of conducting unregistered securities offerings, bringing significant uncertainty and risk to investors.

Although there have been some favorable rulings for Ripple, the ongoing status of the case continues to affect investor sentiment and market FUD. When its legal risks are resolved, the token's actual use is operational, and there are better ways to address its less effective token deflation mechanism, it can better realize its token value.

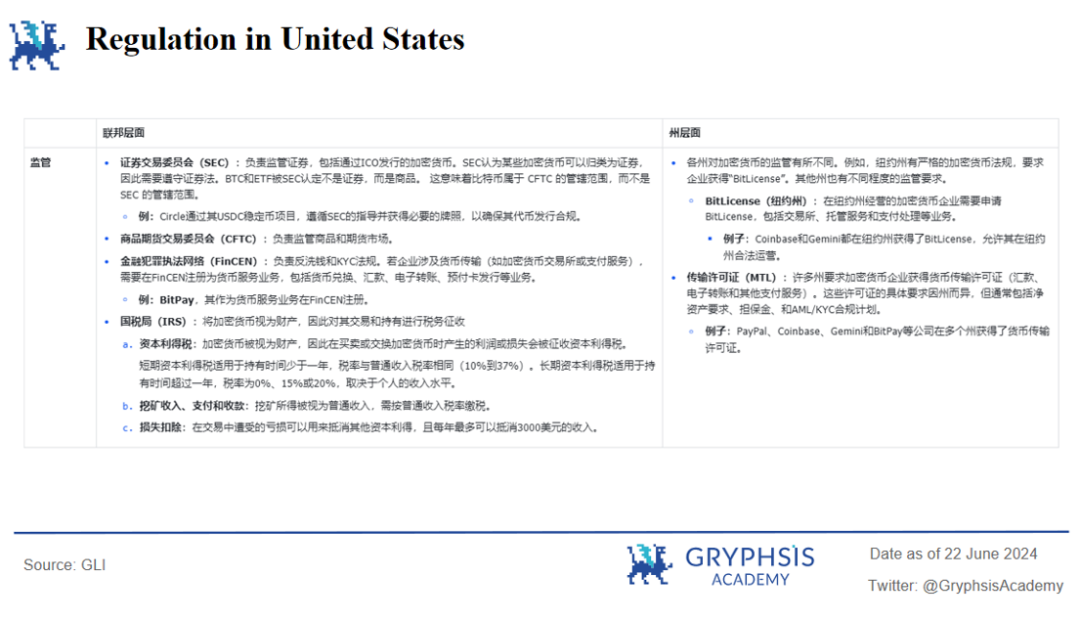

Cryptocurrency regulation in the United States is jointly composed of federal-level Securities and Exchange Commission (SEC) and Commodity Futures Trading Commission (CFTC) regulations, as well as regulations from individual states. The U.S. has very strict requirements for AML, KYC, and investor protection. In recent years, there have been frequent legal actions against cryptocurrency companies. Despite facing the complexity of federal and state-level regulations, with the approval of ETFs, cryptocurrencies are gradually clarifying their regulatory path and moving towards the center of the narrative.

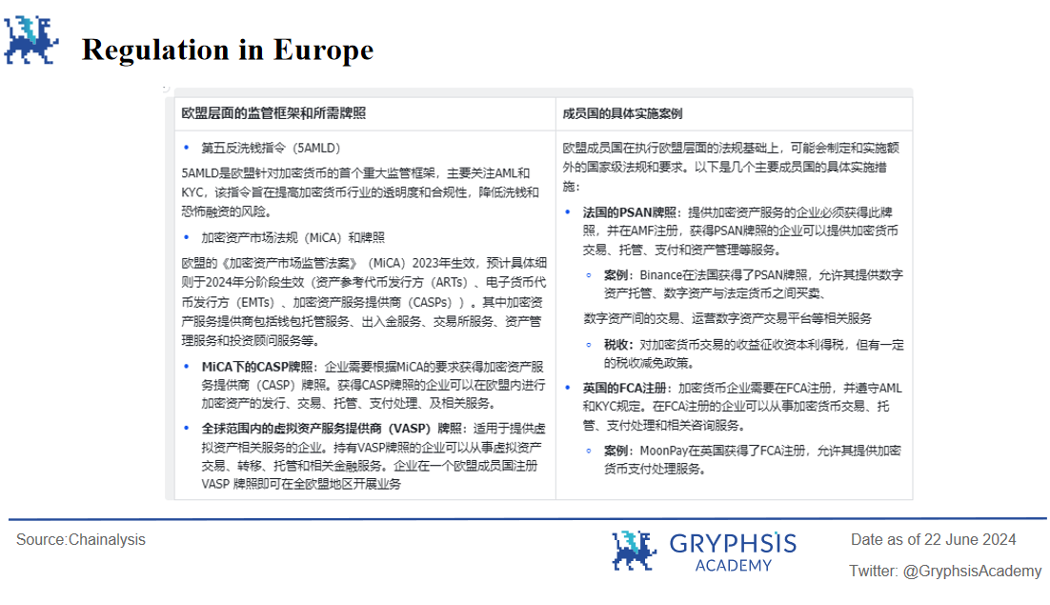

The European Union has implemented unified regulation across its 27 member states through the Markets in Crypto-Assets Regulation (MiCA), requiring all Crypto-Asset Service Providers (CASPs) to obtain licenses as specified by MiCA and operate throughout the entire EU through a "passport mechanism," directly forming a large cryptocurrency market radiating to 27 countries and 450 million EU population.

As registering for a VASP license in one EU member state allows businesses to operate throughout the entire EU region, Lithuania, with its most lenient cryptocurrency regulatory policies in the EU, has attracted many centralized exchanges and payment institutions to register and operate.

Cryptocurrency regulation in Dubai is managed by the Virtual Asset Regulatory Authority and the Dubai Financial Services Authority, with licenses mainly including VASP licenses, investment token and cryptocurrency licenses, and payment service licenses.

a. Virtual Asset Service Provider (VASP) License:

Applicable to companies providing virtual asset-related services, the business mainly involves trading, custody, payment, lending, etc., including secure custody of client assets, internal controls, AML and KYC compliance, regular reporting, etc.

Example: Binance obtained a VASP license, allowing it to provide various services in Dubai, including spot trading, margin trading, and staking products.

b. Investment Token and Cryptocurrency License:

Regulated by the DFSA, covering the issuance and trading of investment tokens and cryptocurrencies, ensuring compliance and transparency.

Example: Ripple's $XRP was approved for cryptocurrency services in the Dubai International Financial Centre.

c. Payment and Remittance Service License:

Mainly used for receiving, transmitting, or transferring virtual assets.

The competitiveness of leading companies in different tracks of the crypto payment industry is reflected in the following aspects:

a. Fiat On/Off-Ramp Services:

In the field of fiat on/off-ramp services for cryptocurrencies, especially with the increasing strictness of off-ramp compliance and anti-money laundering standards, obtaining regional cryptocurrency licenses has become particularly crucial. For fiat on/off-ramp service providers, it is not only important to find crypto-friendly partner banks and stable liquidity providers, especially more challenging after the closure of banks like Silvergate Bank, but also to build a strong compliance system.

Given the regional nature of license acquisition, companies that obtain local operational qualifications more quickly through strategic partnerships, already have a foundation of payment licenses, and establish deep cooperative relationships with crypto-friendly banks often demonstrate stronger competitive advantages. Additionally, early market entrants also have the opportunity to enjoy the dividends of market first-mover advantage.

b. Using Cryptocurrencies for Purchasing Goods or Services in the Real Economy:

The competitiveness of businesses using cryptocurrencies to purchase goods or services in the real economy mainly lies in whether the company has a strong brand influence, an extensive network of payment partners, and deep integration capabilities with merchants and payment platforms. Companies with a wide user base, especially those that have established brands in the traditional payment field, such as Visa and Mastercard, are more likely to gain the trust of non-crypto users with their strong brand endorsement, technical processing capabilities, and large-scale transaction processing capabilities.

However, in the early stages of cryptocurrency payments, the use of this payment method is more by Web3-native crypto users. Therefore, it is crucial to increase the awareness and trust of these users through education and marketing activities, which is essential for leveraging the large non-crypto user base. This also presents an opportunity for native crypto payment companies.

c. On-Chain Payments:

The competitiveness of on-chain payments mainly stems from innovative blockchain technology and its applications. For example, on-chain identity aggregation technology enhances user privacy protection and security, allowing users to freely verify and use identities across different platforms. Fund flow technology enables real-time fund movement, providing innovative payment models for demand-driven and time-sensitive services.

NFT Checkout services have lowered the barrier for users to enter the NFT market by simplifying the payment process, further driving the popularization of crypto payments. Therefore, native on-chain payment companies focus more on improving payment efficiency, reducing on-chain transaction costs, and enhancing user-friendly feature innovation.

a. Complex Global Regulatory Environment

Significant differences in cryptocurrency regulations across countries require companies to comply with legal requirements in different regions. Cryptocurrency regulations are rapidly evolving, including new tax policies, anti-money laundering regulations, market conduct rules, and the high difficulty and slow speed of license applications, increasing the difficulty and cost of compliance for companies. For example, the MiCA regulations in the EU and federal and state regulations in the U.S. have different compliance requirements, requiring a significant amount of compliance resources.

b. Macro-Economic Impact Risks, Systemic Risks, Liquidity Risks

○ Macro-Economic Impact

Widespread adoption of cryptocurrencies in some emerging and low-income regions may weaken the effectiveness of monetary policy, leading to capital outflows from local banking systems and currency fluctuations, thereby affecting the stability of the financial system.

○ Network Security and Technological Innovation

Cryptocurrency exchanges and wallets face the risk of network attacks. The complexity of blockchain technology and the irreversibility of transaction processing increase the difficulty of technical management. Once errors or hacker attacks occur, the difficulty of recovering losses is significant. Data security of blockchain networks still requires substantial resources and advanced technology investment.

○ Market Volatility and Liquidity Risks

After the closure of exchanges like FTX, crypto-friendly bank Silvergate Bank experienced significant capital outflows due to over-reliance on crypto deposits, most of which were uninsured and non-interest-bearing. This overly concentrated and rapidly expanding business model has brought multi-level capital risks. The collapse of the FTX exchange triggered a crisis of trust in the entire cryptocurrency market, leading to a large outflow of funds from crypto-related financial institutions. However, with the halving of BTC and the approval of ETF spot trading, more regulatory agencies and funds entering the market will help mitigate market volatility.

c. Intense Industry Competition and Financing

For traditional payment companies, user education will be a major challenge, as many users have insufficient knowledge of cryptocurrencies and lack the necessary knowledge to use crypto payment services securely. For Web3-native companies, it is important to leverage their community base and low education cost of native crypto users, continuously using innovative technology, interesting narratives, and good services to maintain market competitiveness. If they can attract investments from well-known investment institutions, it will naturally bring more attention and traffic.

In recent years, traditional payment companies have been deploying Web3 payments, launching stablecoins, and peer-to-peer transaction infrastructure, among other products. The driving forces behind this trend include the high profit potential of the cryptocurrency industry, intense competition and high operating costs in traditional payment businesses, and the payment advantages brought by new technologies.

Web3 payment scenarios are diverse, ranging from individuals being able to use MoonPay and Alchemy Pay for fiat-to-crypto on/off-ramp services, to financial institutions conducting global fast and low-cost transactions on RippleNet, and to low-cost, diverse on-chain payments that everyone can participate in. These innovations not only improve payment transparency and efficiency but also meet users' needs for payment diversity and cross-border transactions.

Looking ahead, as more countries begin to regulate and legalize cryptocurrency payments, the popularity of crypto payments will further increase. The development of blockchain technology and applications will further drive the convenience, efficiency, and security of Web3 payment services.

As the acceptance of crypto payments by users and businesses increases, we can foresee that Web3 payments will become a part of everyday payment methods as the crypto industry develops, driving the global financial system towards a more decentralized, transparent, and efficient direction.

References

[1]https:// Web3caff.com/zh/archives/72783

[2]https://www.mastercard.com/news/press/2024/may/mastercard-crypto-credential-goes-live-with-first-peer-to-peer-pilot-transactions-adds-new-partners-to-the-ecosystem/

[3]https://triple-a.io/cryptocurrency-ownership-data/

[4]https://www.techflowpost.com/article/detail_14351.html

[5]https://go.chainalysis.com/crypto-spring-report.html

[6]https://www.globallegalinsights.com/practice-areas/blockchain-laws-and-regulations/usa/

[7]https://investor.pypl.com/financials/annual-reports/default.aspx

Crypto Payment Industry Research Report - Bing Ventures & Alchemy Pay

Research Report of Ripple - Multicoin Capital

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。