Two key features required for governance tokens: control over economic value and reliability of control.

Author: Outerlands Capital

Translation: DeepTechFlow

Governance tokens are a complex and controversial topic, with various opinions among crypto investors, ranging from "innovative" to "fundamentally unnecessary." We lean towards the former and believe that well-structured governance tokens can add significant value to projects.

Key Points

In this article, we propose a four-quadrant framework for evaluating governance tokens based on the reliability of token holders' rights and control over economic value.

After presenting the framework, we conduct case studies on tokens in each quadrant, and finally provide advice for builders and investors on how to construct and evaluate governance tokens.

Introduction

Governance tokens are typically defined as tokens that grant holders voting rights on certain project parameters, which may include implementing product updates, fee/income generation, and business development decisions. While market participants often describe governance tokens as a unique category, more accurately, governance tokens are a feature or attribute that any token may possess. From Layer 1, DeFi, infrastructure to gaming, every crypto submarket has examples of governance tokens.

In this article, we explore the utility of governance tokens and when they can successfully or unsuccessfully unlock the underlying value of their projects. We first introduce the role of governance tokens in cryptocurrencies, address common criticisms, and demonstrate their reasons for existence. This preliminary analysis reveals the two key features required for governance tokens: control over economic value and reliability of control.

We derive a framework from these key features and apply it to case studies to illustrate the differences between projects that meet and do not meet our standards. Finally, we summarize how projects and their potential investors should consider the design and valuation of governance tokens.

Should Governance Tokens Exist?

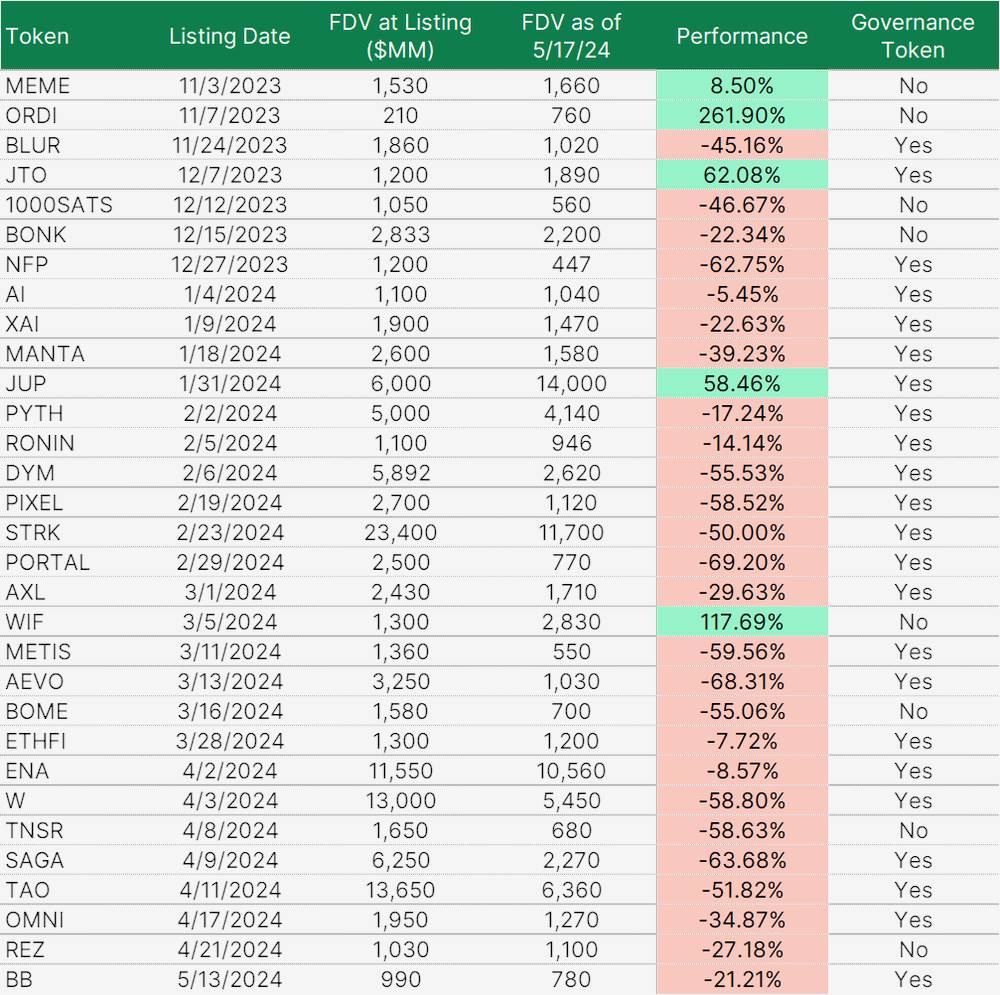

Chart 1: Performance of Binance tokens newly listed since November 2023. Source: @tradetheflow_, Outerlands Capital Research

Some market participants and builders believe that there is no reason for governance tokens to exist, or at least there should be fewer tokens than there are now. Newly launched venture-backed tokens have performed relatively poorly, with high valuations, struggling to compete with large-cap tokens and meme coins, which reinforces the above view.

Common criticisms include:

Protocols operate just as well, if not better, without decentralized governance (or even without tokens), and the existence of tokens only reduces efficiency.

Many teams only launch tokens to profit early, without a genuine reason to create utility.

The utility provided by governance tokens often has little impact on smaller investors, who lack sufficient influence to truly influence the strategic direction of projects.

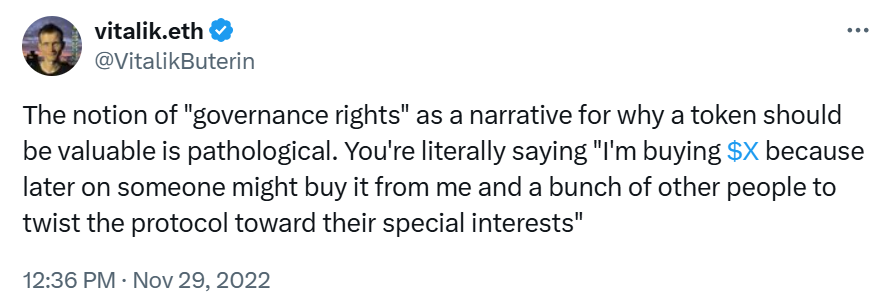

It is worth noting that not all influential figures are the ones who widely criticize governance tokens. Respected figures such as Ethereum co-founder Vitalik Buterin and Hasu, strategic lead at Flashbots, have expressed doubts about the benefits of governance tokens.

Chart 2: Vitalik Buterin's comments on governance tokens

While the above statements may be correct in some cases, we believe that all of these statements are incorrect. If structured properly, projects using governance tokens can retain aspects of centralization that are typically beneficial to startups while unlocking additional value from decentralized governance. For example, teams can retain control over project direction and product development while providing governance token holders with control over other important parameters (such as protocol revenue distribution or approval of new upgrades). Projects can strategically use airdrops and other community distribution plans to reward those aligned with the protocol's long-term interests. We believe governance tokens can add value through two main avenues:

We believe governance tokens can add value through two main avenues:

Governance tokens can help applications manage inherent risks in their business models. This is more achievable with governance tokens than with tokenless governance systems because they provide the incentive to do so. For example, governance tokens can help mitigate vulnerabilities from centralized attack vectors within the protocol. While layer 2 networks like Optimism and Arbitrum are continuously developing their own technologies, they already collectively accommodate billions of dollars in TVL on-chain. If centralized actors like Offchain Labs (developer of Arbitrum) could upgrade contracts or modify system parameters at will, it would pose significant risks to the network. In other words, if certain contracts suddenly received malicious code upgrades, funds could be stolen. However, this technology is still under development and needs upgrades to remain competitive. By decentralizing these decision-making powers, projects become more resilient because no single entity can be targeted by malicious actors.

Governance tokens can provide tangible economic value in the form of utility to their holders. One use case is GMX, a crypto derivatives platform that pays a certain percentage of platform trading fees to those who purchase and hold its tokens. Many centralized exchanges also offer trading fee discounts to their token holders. Tokens can also provide similar utility for other projects to offer economic incentives in exchange for development funds or adjusting incentive mechanisms.

Many governance tokens meet at least one of the above criteria, and we are optimistic that there will be more such tokens in the future.

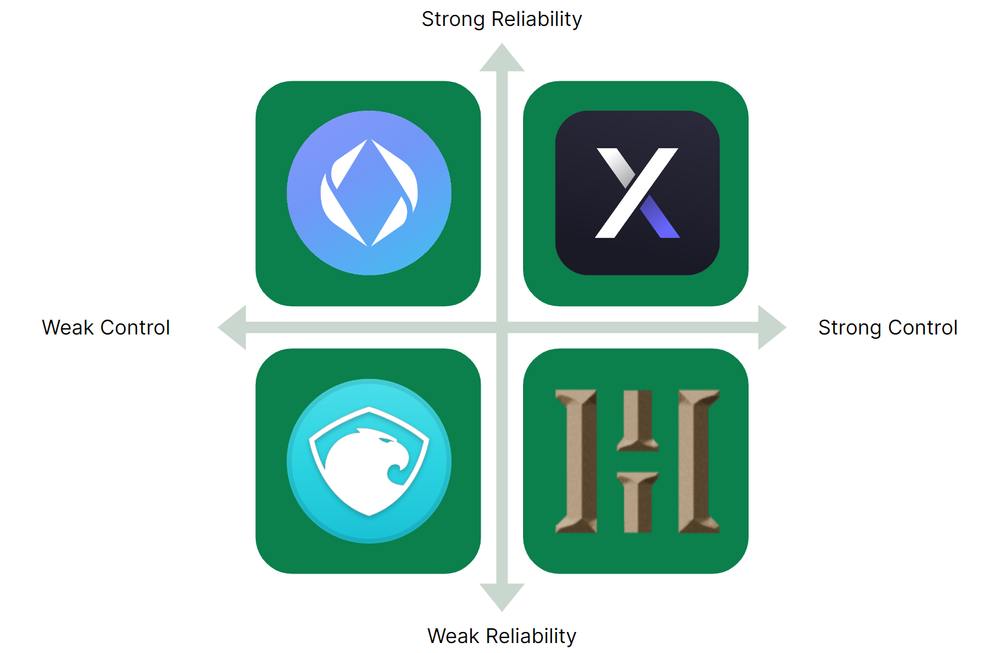

Outerlands Capital's Governance Token Evaluation Framework

We view governance tokens from four quadrants, where,

The Y-axis represents reliability, i.e., the strength of rights granted to token holders. Tokens with strong reliability specify clear rights for holders that are unlikely to change, making holders more certain of their control over given parameters. Meanwhile, tokens with weak reliability only nominally grant voting rights to holders, with significant uncertainty as to whether holders' rights will be respected by the team or protocol. Chris Dixon also made a similar point in the book "Read Write Own," emphasizing the importance of a protocol's ability to make strong commitments.

The X-axis represents control, defined as the economic value or other utility held by token holders. Tokens with strong control provide ecosystem participants (users, investors, etc.) with many reasons to hold the token, while tokens with weak control have little incentive to do so.

Chart 3: Four quadrants of token governance. Source: Outerlands Capital Research

Attributes of Tokens with Strong Reliability

Below are the attributes that Outerlands Capital looks for in tokens with strong reliability:

A strong charter that aligns with the core spirit of the project.

- The threshold for amending the charter should be higher than other governance votes (e.g., a 2/3 supermajority and a 10% quorum).

A comprehensive governance process, including:

Multiple tracks for proposals to balance efficiency and democracy based on urgency and importance:

Daily operational functions (e.g., funding, salaries, etc.) should be directly controlled by the team or delegated to specific committees to make decisions faster than standard governance allows. Token holders should still have visibility into these functions and the option to object when necessary.

Key decisions (e.g., major technical deployments, financial investments above a certain amount, or risk management functions) should undergo multi-stage discussions over a longer period (more than 1 week).

A dedicated forum and voting platform that is easily accessible and interactive for token holders.

The ability for token holders to delegate their governance power to knowledgeable/aligned parties.

A democratic election of an emergency DAO/safety committee to respond to critical events such as hacks, with the DAO being able to modify or remove the committee.

On-chain execution/enforcement of important decisions (so token holders do not have to trust the team to fulfill voting results). This must undergo rigorous auditing and be properly constructed to avoid governance attacks, and on-chain execution should include reasonable time locks.

A real-world representation of the DAO by a foundation or other legal entity (may not apply to fully anonymous teams). This limits the legal liability of governance participants and makes it easier for others to do business with the DAO (as they can interact with a more traditional corporate structure).

Strong control over any specific utility promised to token holders (such as revenue distribution or regular buybacks). Ideally, this can be achieved directly at the protocol level or through smart contracts (the most powerful commitment), but legal protection is also an option.

Attributes of Tokens with Strong Control

Broadly speaking, tokens with strong control grant holders the power to control important economic parameters. The most obvious mechanisms investors look for are those similar to traditional equity. A project that distributes income to holders (with holders having control over the distribution method) or conducts token buybacks on the open market is easily evaluated based on its cash flow. As the underlying business grows, the token also shares in its success, making investing in the token a simple way to bet on the business. Investors can use traditional metrics such as discounted cash flow analysis or relative valuations based on revenue/profit multiples.

However, in addition to capturing equity-like value, there are several important control factors that may incentivize holding tokens. These include:

Other forms of economic utility, including protocol fee discounts or priority access to products for users holding a certain amount of tokens.

Control over technical upgrades and deployment of new protocol versions, which may impact stakeholders' economic interests.

Control over changes related to the token economy, including inflation/deflation and distribution, which may affect the voting power of existing token holders.

Influence over business development decisions that could impact the protocol's financial success, such as team salaries, partnerships, incentive programs, fees paid to third parties like exchanges and market makers, and more.

Framework Case Studies

The following case studies demonstrate tokens in the four quadrants where governance can enhance and/or diminish the fundamental value of the project.

Strong Control, Strong Reliability: dYdX

The decentralized derivatives exchange dYdX (token: DYDX) is an example of a token in the strong control, strong reliability quadrant. Founded in 2017, dYdX offers perpetual contract trading for 66 trading pairs (as of June 2024). In November 2023, dYdX upgraded to its v4 trading software, including a migration to its own Cosmos app chain and significant improvements to the token economic model through changes in the governance process, token utility, and revenue collection methods.

Today, the DYDX token provides the following control mechanisms:

DYDX is the staking token for the app chain, meaning stakers earn fees through trading to secure the network, compensating for the security they provide to the network. Like most PoS blockchains, DYDX stakers earn fees proportionally to the amount of tokens they stake, creating a linear relationship between earnings and token purchase. Token holders who do not wish to stake can delegate their DYDX to others in exchange for a small portion of the earnings they generate. At current activity levels, the chain generates over $43 million in annualized fees for validators.

DYDX holders have the right to propose and vote on decisions that directly impact the development direction of the dYdX chain. Recent proposals include the introduction of new perpetual contract markets, trading incentive programs, funding for the dYdX Foundation, and technical upgrades.

Through the aforementioned upgrades, the DYDX token provides many benefits to stakeholders, including access to governance and control over protocol revenue, as well as significant influence over future project developments.

In terms of reliability, the new token is crucial for the project in many ways. In addition to the technology, one of the core reasons why the dYdX team migrated from Ethereum-based rollups to Cosmos was its superior decentralization achieved through a distributed set of PoS validators. This not only reduces the regulatory risk of running a centralized sequencer but also makes it possible to directly distribute income to token holders through the protocol (in the form of staking rewards), a strong commitment that would be difficult to reverse compared to an income-sharing system run by the team. The other proposals mentioned in the third point also apply similarly, with all of these proposals being executed on-chain after successful voting.

Weak Control, Strong Reliability: Ethereum Name Service (ENS)

The Ethereum Name Service (ENS) is a decentralized naming service for wallets, websites, and operations, and is an example of a token in the weak control, strong reliability quadrant.

On the surface, ENS is one of the more successful projects in the crypto space, with its revenue reaching $16.57 million over the past year (as of May 2024), placing it among the top 25 revenue-generating projects (tracked by Token Terminal). Despite this, the ENS token's market cap ranks well outside the top 100 (despite only about 31.5% of the supply being in circulation). This outcome is primarily attributed to the mission outlined in the DAO's charter, which includes:

Fees are a mechanism to prevent large-scale domain squatting and provide funding for DAO operations. Excess profit is not a priority. The average ENS domain is renewed at $5 per year, far below half of what the most popular Web2 providers charge. ENS may double the fees, but the loss of demand would be minimal.

The income accumulated in the ENS treasury should be used for the development of the ENS ecosystem and ensure its long-term viability. Any excess income should fund other public goods in the Web3 ecosystem.

This is not a direct criticism of ENS Labs (the non-profit organization responsible for core software development) for compiling the charter before handing it over to the DAO. They possess several traits required for strong reliability, including voting delegation, on-chain execution, and different proposal tracks. The Cayman Islands foundation represents the DAO in the real world, providing limited liability for participants (addressing the legal issues mentioned in the OokiDAO case). If other projects wish to operate in a non-profit manner, ENS serves as a good example.

However, its public interest-oriented philosophy limits the potential control of token holders over the project. With the low likelihood of ENS increasing fees or distributing income in the future, the token has limited appeal to investors and lacks an attractive growth story. Even if domain sales significantly increase, token holders should not expect to receive a portion of those fees. The structure of the ENS charter makes it difficult to be a target for aggressive investors. As a result, only a small group is interested in purchasing governance tokens, including:

Individuals with a strong interest in DAO and a willingness to contribute to its development and success. These individuals are more likely to become representatives rather than accumulate a large number of tokens.

Projects looking to collaborate with ENS, which must obtain or be delegated at least 100,000 tokens (currently valued at approximately $2 million) to propose changes.

Projects already integrated with ENS, hoping to maintain the protocol as free public infrastructure.

While these groups are not entirely without demand, they alone cannot form a strong economic flywheel like dYdX.

Strong Control, Weak Reliability: Hector Network

Hector Network is a project in the strong control, weak reliability quadrant. It is one of the many forks of Olympus DAO that emerged in 2021, claiming to be the future reserve currency of DeFi.

Originally a replica of Olympus DAO on the Fantom blockchain, Hector evolved over time into an on-chain asset manager. New investors could deposit funds into its treasury through the rebase mechanism and receive new tokens, while existing stakers maintained the current claim value. The team could then use the funds in the treasury to develop new projects and invest in assets for returns. At the same time, token holders were granted control over important protocol parameters, including treasury investment decisions, which helped rank their control portion of the token highly in our framework.

The Hector Network team attempted to bring value to the treasury through the construction of multiple DeFi-focused products. However, due to poor execution and a market downturn in 2022, these products failed to succeed. Community dissatisfaction with the team grew, and despite the roadmap failures, the team paid themselves hefty salaries (reportedly $52 million over 18 months).

When token holders called for the exercise of their governance rights over the remaining treasury, the Hector Network team began reviewing individuals in the project's Discord and implementing governance restrictions due to the lack of legal or smart contract protections for HEC holders. When the team was eventually persuaded to propose a treasury liquidation, only about $16 million remained, and the value of HEC tokens had dropped 99% from their all-time high.

Providing stronger management protection for HEC holders could have steered the project in a different direction. Inspired by traditional equity investment tools, implementing protective measures would have been a good starting point. Specific redemption periods (i.e., the contract opens for a week every quarter), regular return distributions, and/or investment locks based on smart contracts could have allowed HEC token holders to exit their investment at face value before the downturn. Many had sounded the alarm on this before the DAO's eventual dissolution in the months leading up to it, but they were powerless due to the poor reliability of their governance capabilities.

Weak Control, Weak Reliability: Aragon

In some cases, governance tokens have failed to provide control over the underlying project and have been unreliable in protecting the rights they confer. A relevant example is Aragon: a project that provides legal, technical, and financial infrastructure for DAO operations. Several major crypto projects, including Lido, Decentraland, and API3, use its services.

While the team initially explored multiple use cases for ANT, they pivoted to using ANT as a general governance token as previous ideas failed to gain traction. Unfortunately, the described vague governance rights did not provide much control for holders, as evidenced by the lack of meaningful proposals and sparse community activity.

In June 2022, this situation changed as the Aragon Association and its community passed a proposal to transfer the treasury to a DAO managed by token holders, with a planned date of November 2022, but the process was repeatedly delayed until the first transfer took place in May 2023. At that time, the total value of the treasury was approximately $200 million, and ANT was trading at a discount due to the delays and holder frustration.

The decline in confidence in the team piqued the interest of aggressive investors, including Arca (a cryptocurrency hedge fund), who began purchasing tokens at a discount lower than the treasury's value to expedite the transition of DAO control, increase transparency, and use the treasury funds to buy back tokens, restoring ANT to book value.

However, the Aragon Association did not allow token holders to exercise their so-called governance rights over the remaining treasury, instead suspending the transfer of the remaining funds, banning members from the project's Discord, and accusing aggressive investors of coordinating a 51% attack, claiming that holders only have governance rights over the on-chain products and protocols built by Aragon.

The next six months were tumultuous for Aragon, and it wasn't until November 2, 2023, that the Aragon Association internally decided to dissolve and distribute the funds in the treasury to token holders. The team did not allow ANT holders to vote on the plan, citing so-called legal reasons, despite their previous involvement in the treasury transfer. Predictably, many terms were deemed unfair to holders, leaning in favor of the team, leading to ongoing legal battles.

A governance structure that gives holders greater control and reliability from the start could have helped alleviate much of the pain, possibly by empowering holders to dissolve the token before it reached this point, or designing it correctly in a manner similar to ENS. In the next section, we will provide recommendations to help project founders and investors avoid negative control and reliability situations in governance.

Considerations for Builders and Investors

Our governance token framework and accompanying case studies outline the general characteristics we believe strong governance tokens should have. However, each token is unique, which means the specific functionalities and parameters of governance should vary based on the project.

However, it is universally important for builders to create a roadmap that steadily progresses toward the defined end state. This means that if a project team decides to integrate decentralized governance, they should strive to make the rights of token holders strong and clear, preferably protected through strong commitments such as legal or smart contract mechanisms. Providing vague governance rights and then retracting them is worse than waiting for the right time to decentralize decision-making.

Builders should also determine if it is necessary to issue governance tokens before doing so. As reviewed in the previous section, governance tokens can increase value through risk management and as a form of equity. In terms of risk management, projects must decide if certain decisions are better suited to be made by a decentralized group of token holders rather than a smaller centralized team. They can then design a governance token that gives holders control over these parameters.

If governance tokens do not align with the team's interests, if there are other forms of risk to manage, utility can still be provided. For example, Chainlink's LINK token does not confer governance rights but has a watchful function designed to enhance network security. LINK is also a critical resource for bootstrapping the Chainlink oracle ecosystem and paying service fees.

If there is no risk that needs to be managed by token holders, the cryptographic equity route can still be chosen, depending on the jurisdiction and regulatory challenges the team is willing to tackle. However, if investors choose to invest in new governance tokens, they should have a clear understanding of what they will receive (control over certain fees, the ability to initiate buybacks, etc.).

Not all projects wish to design tokens for profit-driven investors. This may be due to uncertain regulatory environments, a desire for alignment with public goods (seen in non-profit organizations and public interest companies as well), or other reasons. While these reasons weaken the investment value of tokens, many of them are valid. Projects taking this path should set expectations accordingly, letting investors know what they are investing in.

Conclusion

The design and implementation issues of cryptocurrency governance are far from resolved, but many tokens with governance functions today provide clear value for the projects they represent. Encouragingly, there are also signs that the market is beginning to more effectively price governance tokens, with many of the most egregious violators (including several highlighted in this article) being forced to shut down or remedy their failures.

Our governance token assessment framework aims to drive this trend, providing a perspective on how to design and invest in tokens, ultimately channeling more value into projects that have clearly defined token holder rights (control) and actively protect those rights (reliability).

Finally, we want to emphasize that whether a cryptocurrency project is brand new or mature, it is not too late to identify shortcomings and make changes. This industry is still very young and can achieve a transformation from weak to strong in a short time, especially with the help of the framework described in this article.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。