Author: Tom Analysis, SoSoValue Researcher

The Hong Kong Securities and Futures Commission officially announced the list of approved virtual asset spot ETFs, including the Bitcoin spot ETFs under Huaxia (Hong Kong), CSOP, and Bosera International, as well as the Ethereum spot ETFs. These 6 spot ETF products were open for subscription from April 25th to 26th and were listed on the Hong Kong Stock Exchange on April 30th.

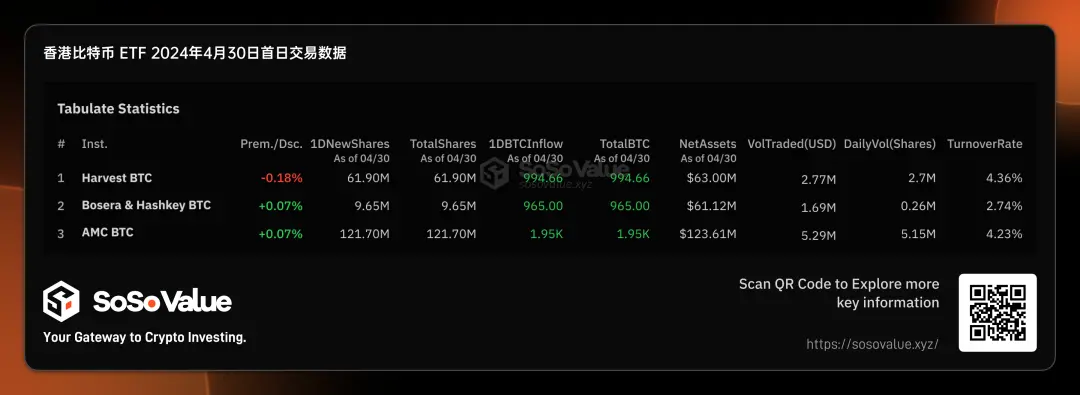

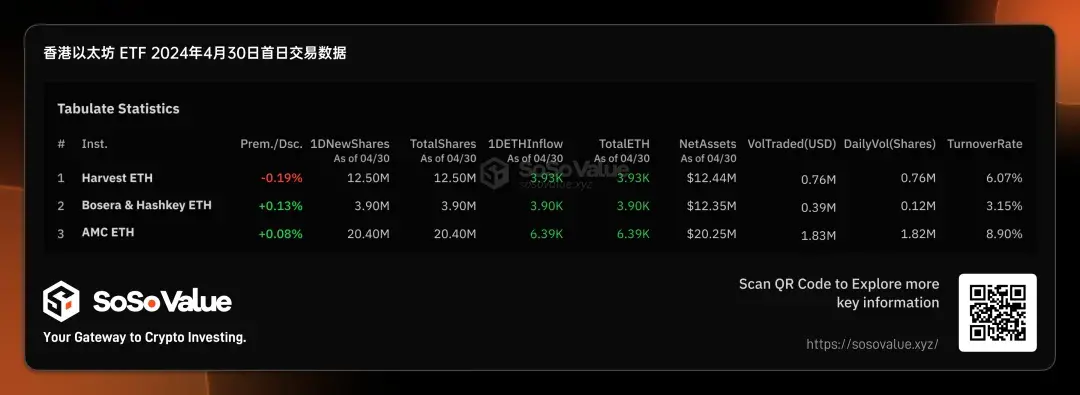

Through the subscription, the 6 Hong Kong spot ETFs obtained a decent initial scale. According to SoSo Value data, the total net value of the 3 Bitcoin ETFs is 248 million USD, and the total net value of the 3 Ethereum ETFs is 45 million USD, with a combined net value of nearly 300 million USD. In contrast, the initial total net value of the U.S. Bitcoin spot ETF product, excluding Grayscale (GBTC) which converted from a trust to an ETF, was only 130 million USD. However, in terms of first-day trading volume, the Hong Kong crypto ETFs were much lower than their U.S. counterparts. According to SoSo Value data, the 6 Hong Kong crypto ETFs had a first-day trading volume of only 12.7 million USD on April 30th, far below the 4.66 billion USD trading volume of the U.S. ETFs on their first day of listing.

We observed a significant mismatch between the initial scale and first-day trading volume of the Hong Kong crypto ETFs. We will analyze how large the Hong Kong crypto spot ETFs can actually grow to, what kind of impact they can have on the crypto market, and how to seize relevant investment opportunities through the supply and demand relationship of the Hong Kong ETFs.

Figure 1: Overview of Hong Kong Crypto Spot ETF Data (Source: SoSo Value)

Demand Side: Restricted participation of mainland Chinese RMB investors may limit incremental funds, leading to lower trading volume

For this Hong Kong crypto ETF, there are still strict restrictions on investor qualifications, and mainland Chinese investors cannot participate in trading. For example, Futu Securities requires the account opener to be a non-mainland Chinese and non-U.S. resident in order to trade. It is currently not allowed for mainland funds to trade through the Southbound Stock Connect, and it is expected to be difficult to achieve for a considerable period of time.

In terms of fees, the Hong Kong crypto ETFs are not advantageous compared to U.S. ETFs, and they are not very attractive to institutions looking for long-term holdings. According to SoSo Value data, among the 11 U.S. Bitcoin spot ETFs, except for Grayscale and Hashdex, the largest ones such as IBIT and CBOE have management fees of around 0.25%, while the comprehensive fees of the 3 Hong Kong Bitcoin ETFs are relatively high, with Huaxia at 1.99%, CSOP at 1.00%, and the lowest Bosera at 0.85%. Even with short-term fee waivers, they still do not have a fee advantage. Due to the fee difference, the holding cost of the U.S. Bitcoin ETFs is lower for institutional investors who are optimistic about the crypto market and hope to hold long-term positions.

Looking ahead, the funds on the demand side may mainly come from two sources: 1) Hong Kong retail investors. For retail investors with Hong Kong identity cards, the threshold for purchasing the Hong Kong crypto ETFs is lower. For example, to purchase the U.S. Bitcoin spot ETF, one needs to have professional investor qualifications (PI), and applying for PI qualifications requires proof of an 8 million HKD investment portfolio or total assets of 40 million HKD. The Hong Kong Bitcoin spot ETF allows retail trading, and the trading hours also better suit the Asian time zone, which is an important incremental factor. 2) Traditional investors interested in Ethereum. The Hong Kong Ethereum spot ETF is the first global launch, so for investors who have difficulty holding the asset but are optimistic about the future of Ethereum, it may bring incremental funds to the Ethereum ETF.

Figure 2: Fee Rates of U.S. Bitcoin Spot ETFs (Source: SoSo Value)

Figure 3: Fee Rates of Hong Kong Crypto Spot ETFs (Source: SoSo Value Compilation)

Supply Side: In-kind creation and redemption increase ETF share supply and boost initial scale

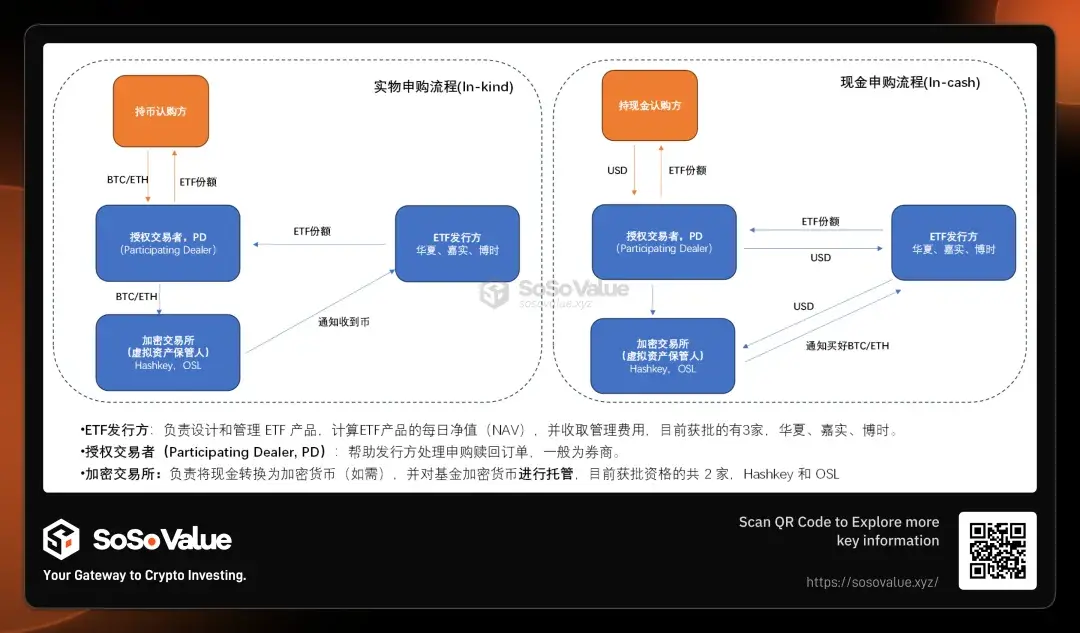

The biggest difference between the Hong Kong crypto spot ETF and the U.S. Bitcoin spot ETF is that, in addition to cash creation and redemption, the former has added in-kind creation and redemption. This directly determines that, at the ETF share level, the Hong Kong crypto ETF may have more supply.

In-kind creation and redemption refer to investors using cryptocurrencies (Bitcoin or Ethereum) to exchange for ETF shares when subscribing (creating) or redeeming ETF shares, instead of using cash. In subscription, investors provide a certain amount of cryptocurrency to the ETF in exchange for ETF shares; in redemption, investors return ETF shares in exchange for the corresponding cryptocurrency.

Referring to the comparison of the Hong Kong crypto currency subscription process in Figure 2, it can be seen that in-kind subscription brings two major differences compared to cash subscription:

1) Holders can directly subscribe with cryptocurrency: For some large holders, such as miners, it is easy for them to convert their own cryptocurrency into ETF shares, which can be held or sold for cash on the Hong Kong Stock Exchange, providing a very flexible handling method.

2) For the crypto market, in-kind subscription does not bring incremental funds into the market, but rather involves the transfer of cryptocurrencies between different accounts. Cash subscription, on the other hand, brings actual buying pressure to on-chain crypto assets.

Therefore, the subscribers of the Hong Kong crypto ETF shares include both traditional cash subscribers and large holders. Although the specific share of in-kind and cash subscriptions has not been disclosed by various fund companies, according to public communication from OSL, the proportion of initial in-kind subscriptions may exceed 50%, which also explains why the initial fundraising scale of the Hong Kong crypto ETF can reach nearly 300 million USD, with credit due to in-kind subscriptions. However, on the other hand, these in-kind subscribed ETF shares may be converted into sell orders in subsequent secondary market trading.

Figure 4: Comparison of In-kind vs. Cash Subscription Process for Hong Kong Crypto Spot ETF

Comprehensive supply and demand: Focus on the premium/discount rate to seize investment opportunities

Based on the comprehensive analysis of supply and demand in the previous section, unlike the U.S. Bitcoin spot ETF, we can track the daily net inflow of ETF funds (Total Net Inflow, specific reference: https://sosovalue.xyz/assets/us-btc-spot) to intuitively judge the impact of incremental funds brought to on-chain crypto assets by the Bitcoin ETF. The supply and demand of the Hong Kong crypto spot ETF is more complex, and the data disclosed by various fund companies cannot clearly distinguish between in-kind and cash creation and redemption volumes. In this context, we believe that the premium/discount rate in the open market (Hong Kong Stock Exchange trading) may be a better observation indicator.

As we analyzed earlier, the premium/discount in on-exchange trading on the Hong Kong Stock Exchange is the best reflection of the forces of supply and demand. If an ETF is trading at a discount, it indicates a stronger selling interest, an oversupply, and market makers are motivated to purchase ETF shares at a discount on the Hong Kong Stock Exchange and then redeem the shares from the ETF issuer off-exchange to profit from the price difference. This leads to a reduction in the overall net assets of the ETF, outflow of funds, and a negative impact on the overall crypto market. The entire process can be summarized as follows: ETF trading at a discount → stronger selling interest → potential redemptions → negative impact on the crypto market. Conversely, if the ETF is trading at a premium, it indicates stronger buying interest, potential subscriptions, and a positive impact on the crypto market.

According to SoSo Value data, as of the close on April 30th, except for CSOP Bitcoin Spot ETF (3439.HK) and CSOP Ethereum Spot ETF (3179.HK) which had negative premiums of -0.18% and -0.19% respectively, all other products were trading at a premium. Intraday trading processes also generated a maximum premium of 0.33%, with restrained selling and relatively strong buying on the first day. Considering the impact of market makers on the first day of ETF listing, this premium/discount data should be continuously monitored. If the positive premium can be sustained, it is likely to continue attracting investor subscriptions, especially from holders, and the scale of the Hong Kong crypto spot ETF is expected to exceed the estimated value of 500 million USD. However, if it turns into a discount, arbitrage trading redemptions of ETF shares should be monitored, as the ETF issuer sells off cryptocurrencies, leading to a downturn in the crypto market.

Figure 5: Supply and Demand Mechanism of Hong Kong Crypto Spot ETF (Source: SoSo Value Compilation)

Hong Kong Crypto ETF has another important value for investors: it has created a pathway for the conversion and circulation of crypto assets into tradable financial assets

The rapid approval of the Hong Kong crypto spot ETF, although it may have a smaller short-term impact on the crypto market compared to the U.S. spot ETF, provides a pathway for crypto assets to be converted into traditional financial assets through the in-kind creation and redemption mechanism in the long term. By using in-kind creation, cryptocurrencies can be converted into ETF shares, and holding crypto asset ETFs can serve as proof of assets in traditional financial markets due to their fair value pricing and liquidity. This allows for various leveraged operations, such as collateralized borrowing and the construction of structured products, further bridging the gap between crypto assets and traditional finance, and allowing for a more comprehensive reflection and realization of the value of crypto assets.

From a more macro and long-term perspective, the approval of Bitcoin and Ethereum spot ETFs in Hong Kong is an important development for the global crypto market. This policy will have a long-term impact on the financial landscape in the Chinese-speaking region and is also an important step in further legitimizing cryptocurrencies in the global financial system.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。