Cryptocurrency has reflexivity.

Author: ROUTE 2 FI

Compiled by: Deep Tide TechFlow

As new tokens continue to enter the market, the total market value of altcoins is steadily increasing.

I believe that when BTC.D trends downward and the altcoin market arrives, only a few altcoins will experience significant increases. Not every altcoin that people are accustomed to will experience significant increases.

Reflexivity: What happens when too many altcoins and tokens are continuously unlocked and poured into the market?

Let's talk about altcoins, how they have recently been launched, and their impact on the market.

In this cycle, there is a trend of launching tokens with high FDV, large-scale airdrops, low float, and massive unlocks from venture capital firms.

Cryptocurrency has reflexivity. What does this mean?

This article is inspired by Twitter, Telegram chats, and conversations with crypto friends, and it's something I've wanted to write for a long time. Special thanks to Cobie, Thor Hartvigsen, Thiccy, Andrew Kang, and Regan Bozman for their thoughts on this. Follow them on Twitter.

Reflexivity: The Great Idea of Feedback Loops

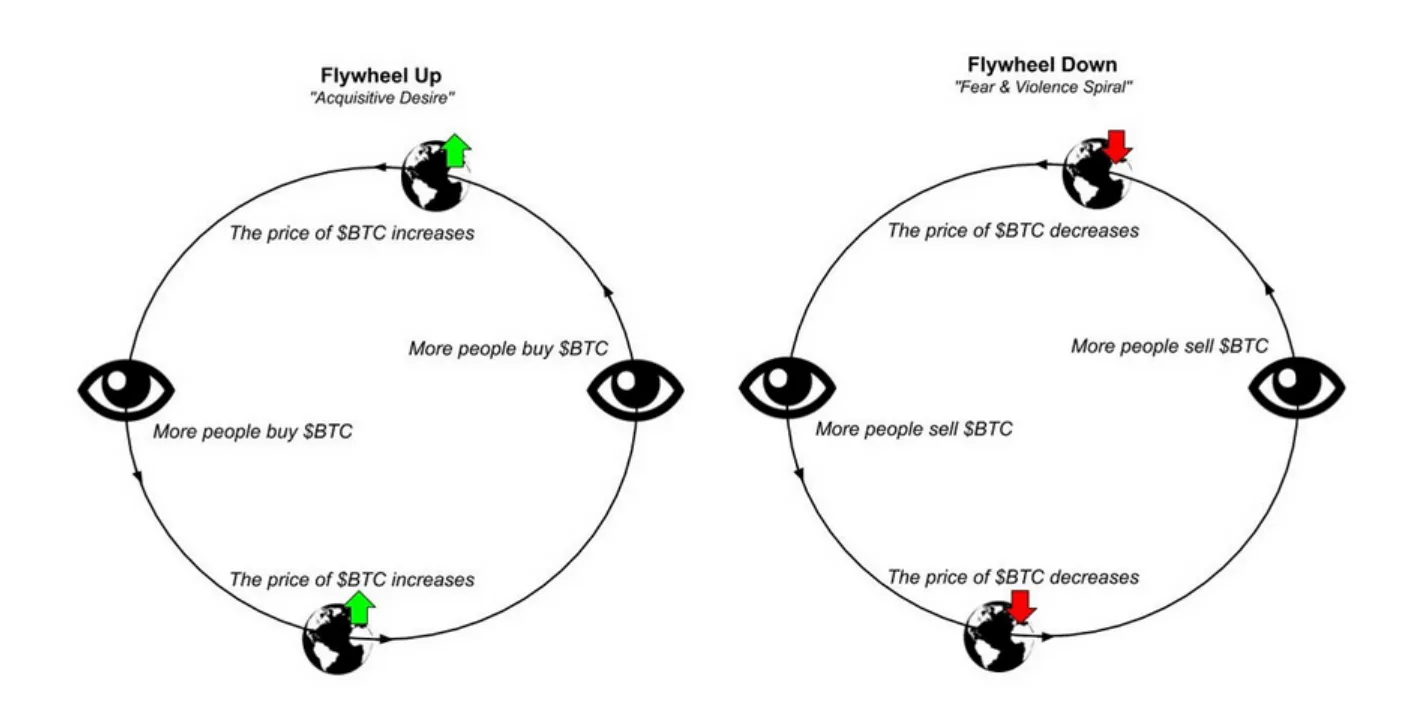

Originally proposed by George Soros, reflexivity is a theory that the positive feedback loop between expectations and economic fundamentals may cause price trends to deviate significantly and persistently from equilibrium prices. Bitcoin has always been characterized by strong reflexivity. Bitcoin's positive cycles may last a long time, however, its negative cycles are notorious for their length and depth.

According to Cryptonary, it is important to remember that when analyzing the market and its movements and operations, the concept of market reflexivity contradicts conventional wisdom. In theory, the market is always seeking equilibrium, and all participants are rational individuals making decisions based on facts. Bubbles, panic events, and boom and bust cycles are abnormal fluctuations in the market; prices will eventually return to equilibrium. Prices have no impact on the factors that establish equilibrium.

On the other hand, in market reflexivity, everyone makes judgments based on their interpretation of reality, and prices affect market fundamentals. You can see how this works: if pricing affects fundamentals, then price changes will inevitably affect fundamentals, thereby affecting investors' expectations, which in turn affect prices, as investors act based on these revised expectations. As group behavior reinforces price movements, prices move further and further away from reality, eventually becoming the new reality - a self-fulfilling prophecy, if you will.

Prices should tend toward equilibrium, but due to market reflexivity, they often deviate from that equilibrium for extended periods. It is only when market participants realize that their view of the market is no longer based on reality that prices begin to reverse their current trend, which usually happens after prices have been above or below fair levels for a long time.

Friends, this is why we have the following chart:

You see, reflexivity is two-way. There is no doubt that a ball thrown into the air will eventually fall back to the ground.

If the price of Bitcoin rises significantly in a short period of time, then after the initial movement, the price may continue to rise for a period. Conversely, the same applies. The cryptocurrency market is still in its early stages, so significant price fluctuations are "easier" to occur.

Look at the chart above. This perfectly describes reflexivity. I believe you now have a good understanding of this concept, so let's continue.

Now, let's take a look at altcoins and what will happen in the future as all these new tokens enter the market.

New Tokens Are Great (Until Circulating Supply Increases)

I have previously written about supply and demand issues in cryptocurrencies, but let's reiterate a bit.

Market cap: Circulating supply × price

Fully diluted valuation (FDV): All tokens (including unreleased ones) × price

Understanding the VC/angel investment game (especially from the perspective of retail investors) is important.

Most cryptocurrency companies raise funds from investors through SAFT (Simple Agreement for Future Tokens). In the stock market, SAFT can be compared to a Simple Agreement for Future Equity (SAFE), which allows investors in startups to convert their cash investments into equity at a future point in time, subject to specific conditions being met.

To illustrate what a typical SAFT transaction might look like, let's consider a very simple example.

Token name: Yolo Coin

FDV: $100 million

Unlocking conditions: 10% at TGE, then 1-year cliff, followed by linear unlocking over 3 years

Circulating supply at TGE: 12% (part of it through airdrop)

Yolo Coin was launched after much hype, and the FDV is now $1 billion (10 times that of seed investors). Investors are happy because they can sell at break-even prices, and they still have 90% of the allocated tokens, which will gradually unlock over the next 36 months (after a 1-year cliff period).

But wait? Why is the VC lockup period so long? The short answer is to ensure long-term consistency and prevent it from being dumped at TGE.

Let's see why this is a problem:

Due to investors being locked up for a long time, this means that when they eventually start unlocking, there will be sustained selling pressure on the market.

Look at the chart below.

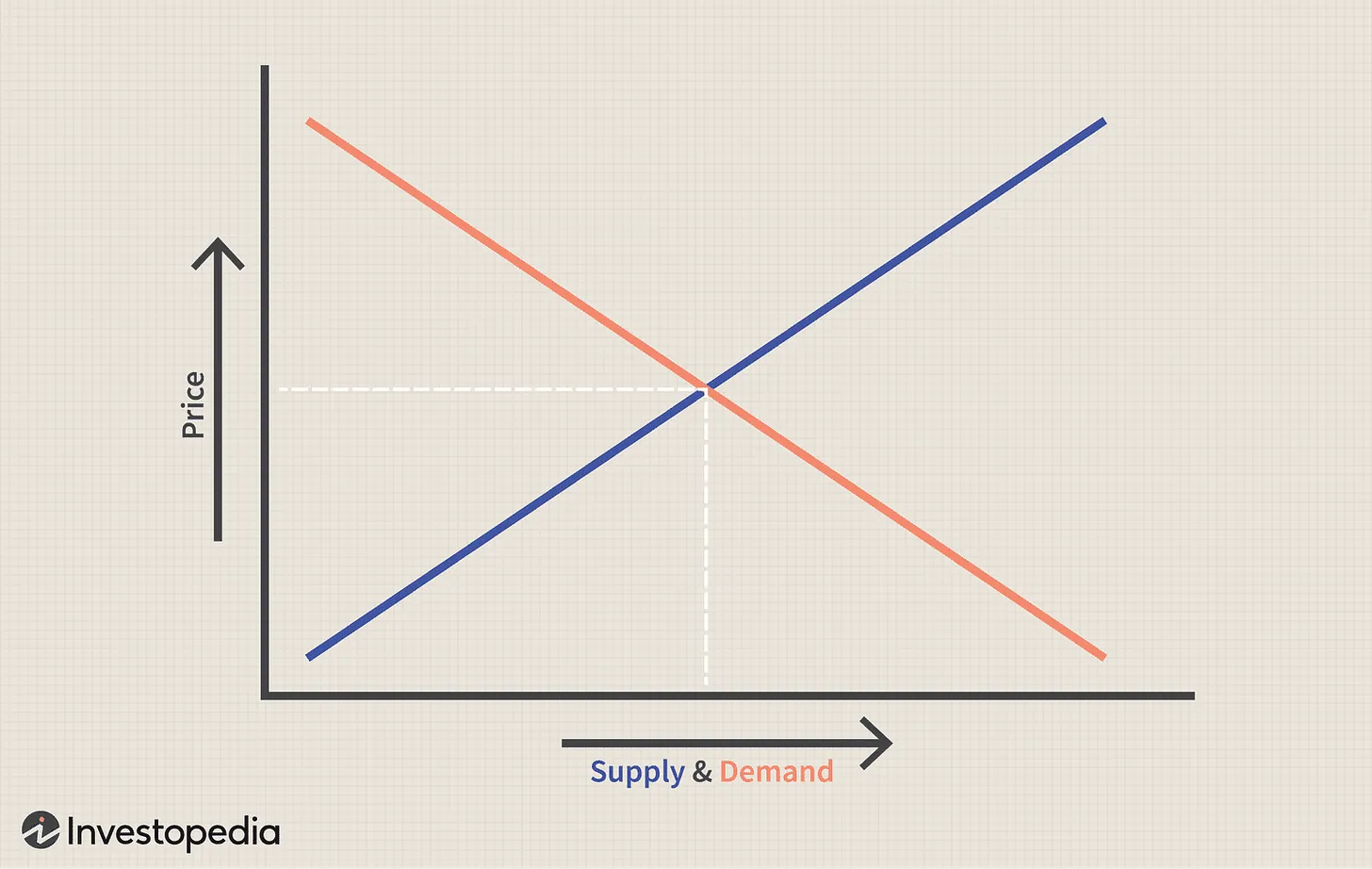

Assuming Yolo Coin's price is $1 (investor price = $0.10). 12% of the supply enters the market at launch, but as tokens gradually unlock, more and more supply will pour into the market.

This leads to an increase in supply.

But the question is: Where is the demand? Who will buy the tokens that VC investors are selling?

You might think that the price will rise due to factors X, Y, and Z, such as an increase in TVL in DeFi protocols, a bullish event, etc., which may be effective for a period of time. But at some point, supply will surpass demand, and due to the significant increase in inflation, we will start to spiral downward.

Early buyers will be trapped, leading to pessimism in the community, a decrease in the TVL of protocols, developers (if any) leaving to seek better opportunities, team members resigning, and so on.

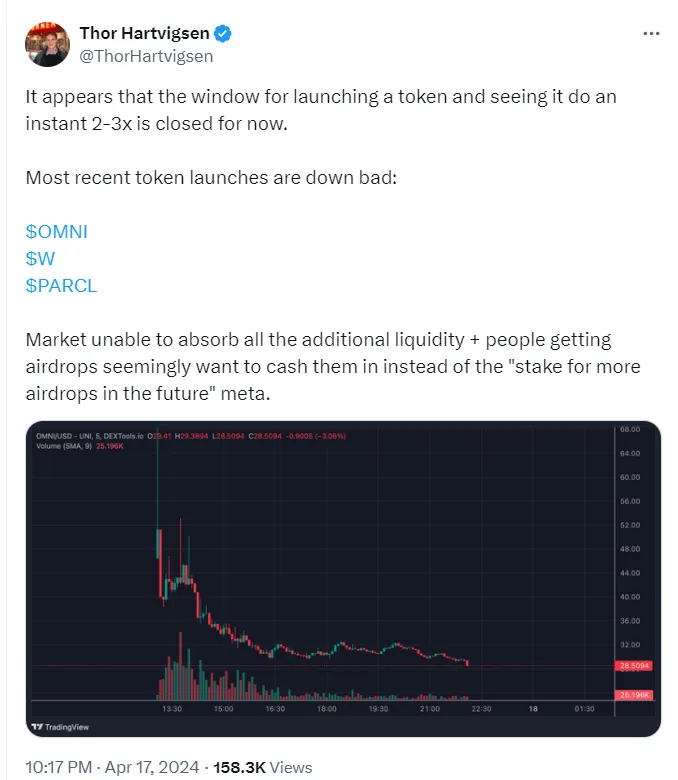

Thor Hartvigsen summed it up well: "The market will not be able to absorb all the additional liquidity + those who received airdrops seem to want to cash out rather than hope for more airdrops in the future."

So far, the biggest change in this cycle is the dispersion in space. We have been taught to believe that altcoins will skyrocket together. But now, there are probably about 300 decent projects with insufficient liquidity.

We often hear about altcoin seasons, but this time I think the situation will be different. We are used to hearing that every token will skyrocket under the right conditions. But is this true?

Please remember, there are far more "utility" tokens in the market today than in 2021. Now, 3-5 "high-quality" tokens are entering the market every week. The total market value is increasing, and everyone seems to be happy. But ask yourself, who will buy all these tokens? Unless institutions or retail investors enter in large numbers, this will only be an eternal PvP competition.

Two weeks ago, an example was the Wormhole airdrop. Launched with a valuation of $100 billion. Now ask yourself why you want to own it. I can't see any reason other than pure speculation. Since its launch, the price has dropped by 40%, bringing its FDV to $60 billion.

As Cobie said, "Market cap is a measure of demand, while FDV is a measure of supply."

This means that market cap is the total value of public demand and it increases and decreases with price changes. If the price goes up, FDV will also increase, but it will also increase as tokens unlock.

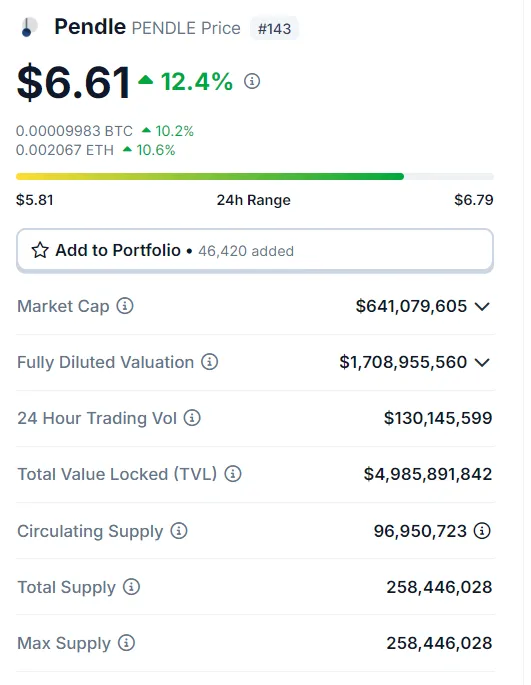

Let's take a look at Pendle. Everyone loves Pendle now because their TVL has increased significantly due to yield farming and the narrative of Eigenlayer.

Also note that out of 2.58 million, 950,000 tokens are circulating in the market today (37%). As the price rises, the market cap will increase. However, the increase in market cap does not mean there is additional demand for the locked tokens. To explain why, think from the perspective of investors. I know people participated in Pendle for less than 10 cents. Now the price is over $6. Do you really think the token holders who are unlocking care whether the price is $6 or $7? No, so they will sell. Similarly: supply increases, but demand remains the same. (I have not checked Pendle's unlocking schedule, nor do I know how much FDV people have invested. Just making some assumptions to explain supply and demand).

Are high FDV tokens scary? Not always, a good example is $TIA in November 2023. $TIA currently has an FDV of $12 billion, but because the locked tokens will not be listed until the fall of 2024, the situation is not so bad, and other traders may be scared off by the high FDV.

For more information on this, see Cobie's article.

Okay, but back to the issue of demand. Where are the buyers?

As I mentioned in the introduction, new "high-quality" projects are launched every week with very high FDV. This means a large supply enters the market, and these tokens will have to decline (at least in the long run) unless new buyers come in.

Retail investors like to invest in meme coins and SOL shitcoins. They don't buy high-tech VC tokens. They have learned from the trends of 2021. They are smarter today. Unpermissioned token listings and greedy venture capital firms are not conducive to the long-term development of individual tokens. There are 100 new tokens launched every year. This dilutes existing tokens.

It is now April 2024, and the influx of altcoins seems more selective, but not enough to offset the large number of unlocks.

Is there a solution?

We have learned that the low float token model is not good. But can we solve it?

Clearly, a significant part of the problem is the number of projects being launched. Not everyone can buy all these projects. But a more linear unlocking schedule might be wise (as opposed to Arbitrum), and there is also retroactive airdrops: consider Ethena and EtherFi, which are conducting 2 rounds of airdrops. Perhaps a reintroduction of ICOs would help, creating more loyal fans.

I believe that when BTC.D trends downward, only a few altcoins will experience significant increases. Not everyone will be as people are accustomed to. There are more cryptocurrency participants today than in the previous cycle, but people are smarter now.

According to Thiccy, more than $250 million worth of altcoins are supplied daily from new tokens and all tokens in the market, and due to upward reflexivity (positive feedback loop), most of these tokens have not been sold when people received airdrops or invested in rounds, because the market is just going up ("why sell today when I can sell for more tomorrow" mentality). This is why we saw a lot of selling in April, the market just needed a reason (war).

Okay, so token unlocks, new token listings, and staking rewards for existing tokens have led to a daily increase of $250 million in altcoin supply in 2024 so far. Due to the launch of many new tokens, FDV growth has exceeded circulation, with an annual growth of about 70%. The gap between FDV and circulating supply represents the amount of future supply that will enter the market, and this gap has increased by over $150 billion since the beginning of the year. As mainstream coin inflows slow down, the weight of daily altcoin supply becomes increasingly apparent. The deeper I understand trading, the more I realize that tactically shorting crypto altcoins is actually beneficial. At least when you are trading currency pairs.

In any case, the total market value of altcoins is steadily increasing due to the continuous launch of new tokens and the result of new supply entering the market.

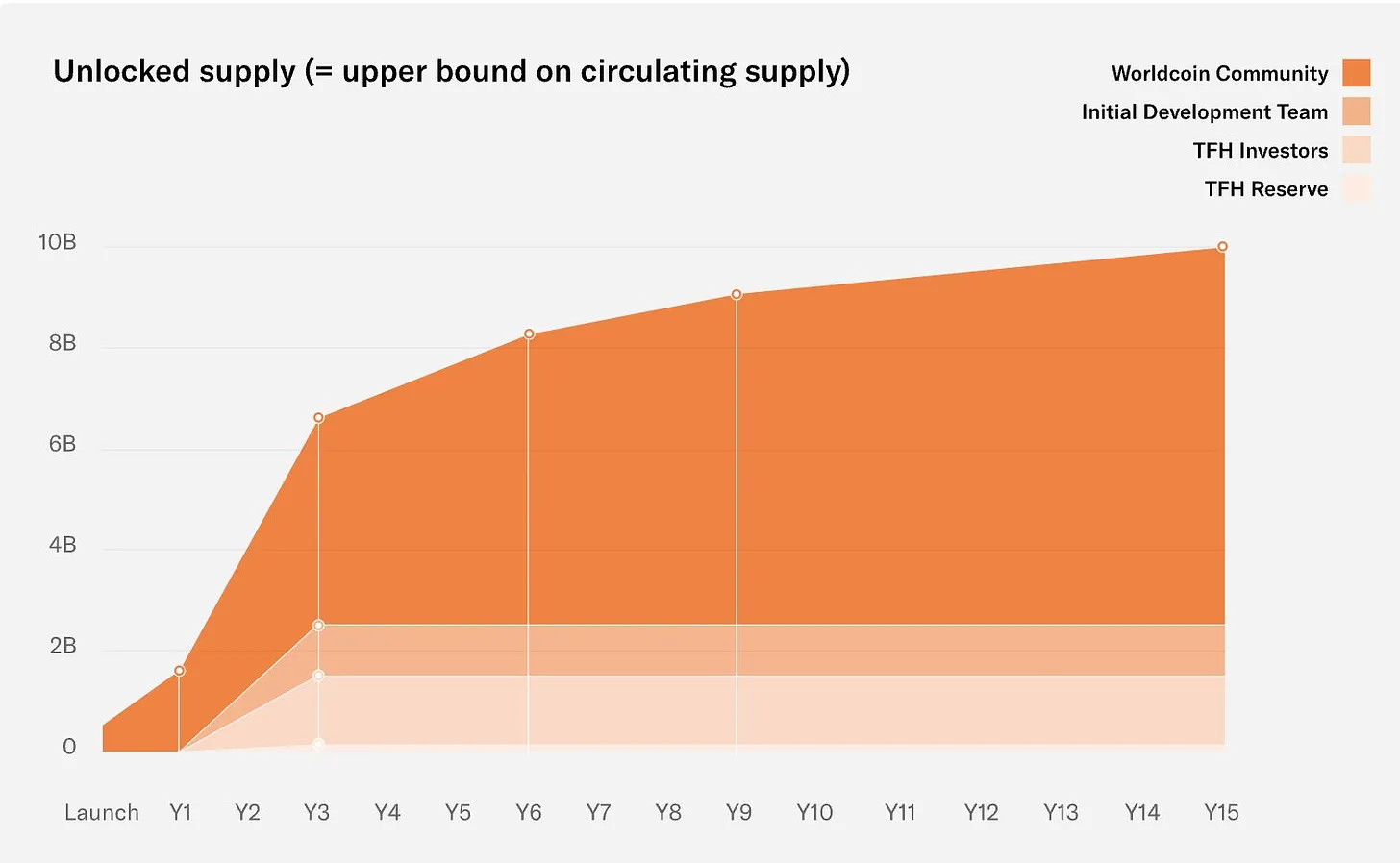

There are some high market cap/FDV tokens in the examples above. Look at Worldcoin: a market cap of $10 billion, but an FDV of $640 billion. What does this mean?

This means that Worldcoin will continue to supply tokens to the market in the future. In July 2024, they will start releasing frantically, with 6 million $WLD tokens entering the market every day. And today, there are only 181 million $WLD tokens in the market.

It is easy to see from the basic supply and demand curve that it will be very difficult to maintain the price of $WLD when this supply enters the market.

Who will buy 6 million $WLD tokens every day?

What does this mean for the bull market?

As long as BTC/ETH is rising, this may not have a big impact. We will see all of this happen in bearish conditions.

However, I like Anteater's approach, which is to be bullish on strong coins and bearish on weak coins. This is a hedging strategy, unlike Ethena, which is triangular arbitrage. Hedging in a bull market may sound strange, but there will be several downtrends as we reach the peak of the bull market. The process of reaching the peak is not smooth sailing.

Additionally, there have been several posts on crypto Twitter recently saying that this cycle has already passed 70%. Who knows, so decide based on the risk you can bear.

I believe that most new VC scam coins (high FDV coins) will eventually be heavily sold off. You can use this for hedging trades, or use it when you want to hedge.

Examples of weak coins may be $STRK, $APE, $BOME, $ADA, $CRV, and $XRP. Or if altcoins are performing well overall, combine these weak altcoins with strong altcoins: currently strong ones are: $ENA, $TON, $FTM, $PENDLE. However, this is not advice to buy/sell these coins, as market momentum changes rapidly.

The benefit of meme coins is that they are actually one of the few honest coins. Look at $WIF, $PEPE, $DOGE, $POPCAT, etc. The circulation and total supply are the same. No one will dump your coins according to a crazy unlocking schedule. It's just a pure PVP game.

Finally, let's hear some words from crypto trader Wazz:

I think his argument is rational and makes sense. Too many altcoins, too many projects, and too many unlocked tokens will enter the market in the future.

If the price of Bitcoin rises significantly in a short period of time, it is almost certain that the price will rise for a period after the initial rise. Conversely, the same applies. The low liquidity of the crypto market means that prices are easily subject to significant fluctuations.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。