Every vesting schedule is a compromise.

Author: Achim Struve

Translation: Luffy, Foresight News

What is token vesting?

Many early Web3 companies started with a great idea from an innovative decentralized technology world. But even the best ideas need some form of funding to kickstart and establish the expected flywheel economy. These self-sustaining ecosystems are often built on fungible cryptocurrencies, and token economies can be used to help users adopt, incentivize behavior, and the product itself. Therefore, in addition to raising funds in equity business, raising funds in future tokens is also a common strategy, especially in the case of overall market sentiment recovery in the crypto market.

Token vesting refers to the amount of tokens released to the market over a certain period. In fundraising, token vesting refers to the release of allocated token supply to early investors and contributors. As they play a crucial role in the building stage of Web3 startups, they can receive discounted or even "free" tokens, meaning they have a lower entry point than later investors and market participants. Adjusting the token allocation of these privileged entities through the supply release schedule will align their long-term interests with Web3 startups, while being fairer to later entrants.

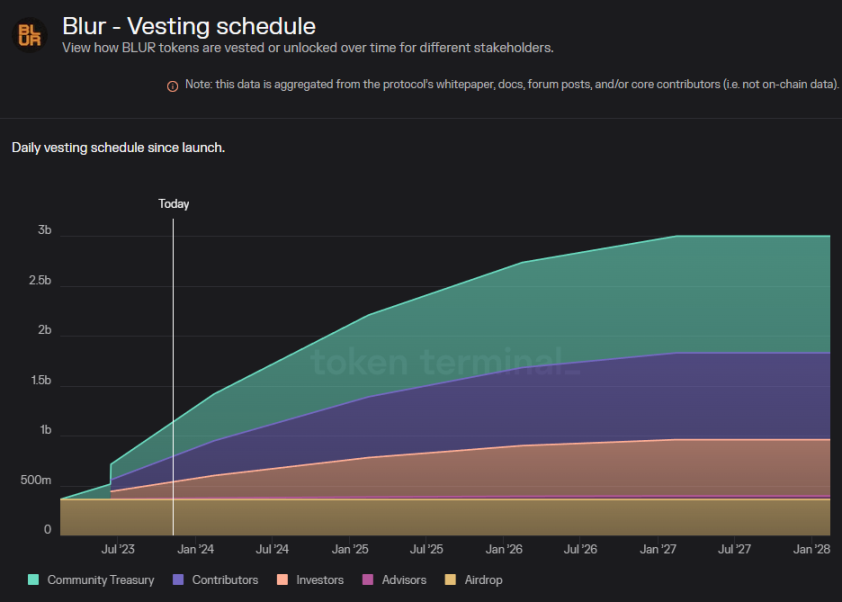

Figure 1: Blur token vesting, Source: Token Terminal

Figure 1 shows the vesting schedule of $BLUR tokens. Apart from airdrops, most of the supply will be gradually released over 4 years after a 6-month lock-up. These figures are quite common in the latest market narrative. In the bull market cycle of 2021, the usual vesting period was between 12 and 18 months. Entering the formal topic of this article, how to design the right vesting terms for our early investors and contributors?

Short-term or long-term vesting?

The previous section pointed out the possible ranges of vesting schedules we see in the market. These ranges are mainly narrative-driven and are based on "what others are doing" rather than "what is best for the entire Web3 initiative." When designing vesting schedules, factors other than "what is best" should also be considered, such as:

Early investors and contributors

Recognizing early investors and contributors in the vesting schedule is to acknowledge and reward the stakeholders who have supported the project since its inception and have taken on the associated risks. These individuals and entities typically provide the necessary capital and resources for the initial development and growth of the project. They want to receive liquid tokens early, while also hoping for the long-term health of the startup they invested in.

Fairness

Market participants consider vesting terms when conducting due diligence on Web3 projects. If they perceive the vesting terms as unfair, it may lead to negative sentiment towards the project and hinder future adoption. Fairness refers to the fair distribution of interests among all stakeholders. Fairness ensures that no party gains a disproportionate advantage or disadvantage due to vesting terms. This is to create a level playing field, allowing long-term participants to be rewarded for their commitment while still enabling new entrants to participate and benefit. In most cases, this means the lower the entry point for investors, the longer the vesting period.

Maintaining investability

Token valuation tables and corresponding vesting schedules play a crucial role in future investability and are in tension with the startup's need for rapid funding. Lower valuation sales may attract more funds early on but could diminish future rounds of investability, as later investors may feel disadvantaged compared to initial investors.

Ecosystem sustainability and stability

The design of the vesting schedule should take into account the need for sustainable development of the project ecosystem. This requires setting a schedule to avoid token flooding the market and causing value dilution, thus maintaining stability. A well-considered vesting schedule can prevent significant price fluctuations, ensuring that token issuance matches the growth and development stages of the project, providing support for the ecosystem. A more advanced approach to maintaining sustainability and stability is to adopt an adjustable vesting method.

Timing and intervals

The timing factor is related to the specific time intervals for releasing tokens to stakeholders. It is crucial to align the token release timing with strategic milestones and the overall progress of the project. Proper timing helps maintain momentum, indicates project maturity, and manages market supply. By determining the vesting time based on the project roadmap and development stages, participants can be assured that vesting is part of a strategic plan, not a short-term incentive plan. Remember, the actual release of tokens should not be one-time but gradual. A large supply entering the market immediately may cause significant fluctuations. A better practice is to release gradually over time to reduce market manipulation and volatility.

Community vesting

Community incentive measures are often allocated over specific periods. Some recent vesting schedule designs include individual address-based allocations for market contributors. Maximizing the effectiveness of these community incentive measures is crucial. This means that every dollar distributed in token form should contribute to accumulating more than a dollar's worth of value for the protocol. In many cases, this is achieved by incentivizing core ecosystem behaviors and product adoption.

These aspects are not exhaustive, and there are many different perspectives to carefully weigh and consider when it comes to token release in an economic system. A fundamental pillar is to create the right demand to offset token release. Imbalances between supply and demand can lead to fluctuations and disruptions in the token ecosystem. Strong Web3 startups pay attention to these dynamics and attempt to anticipate different scenarios.

Case Study: Simulated Vesting Schedules

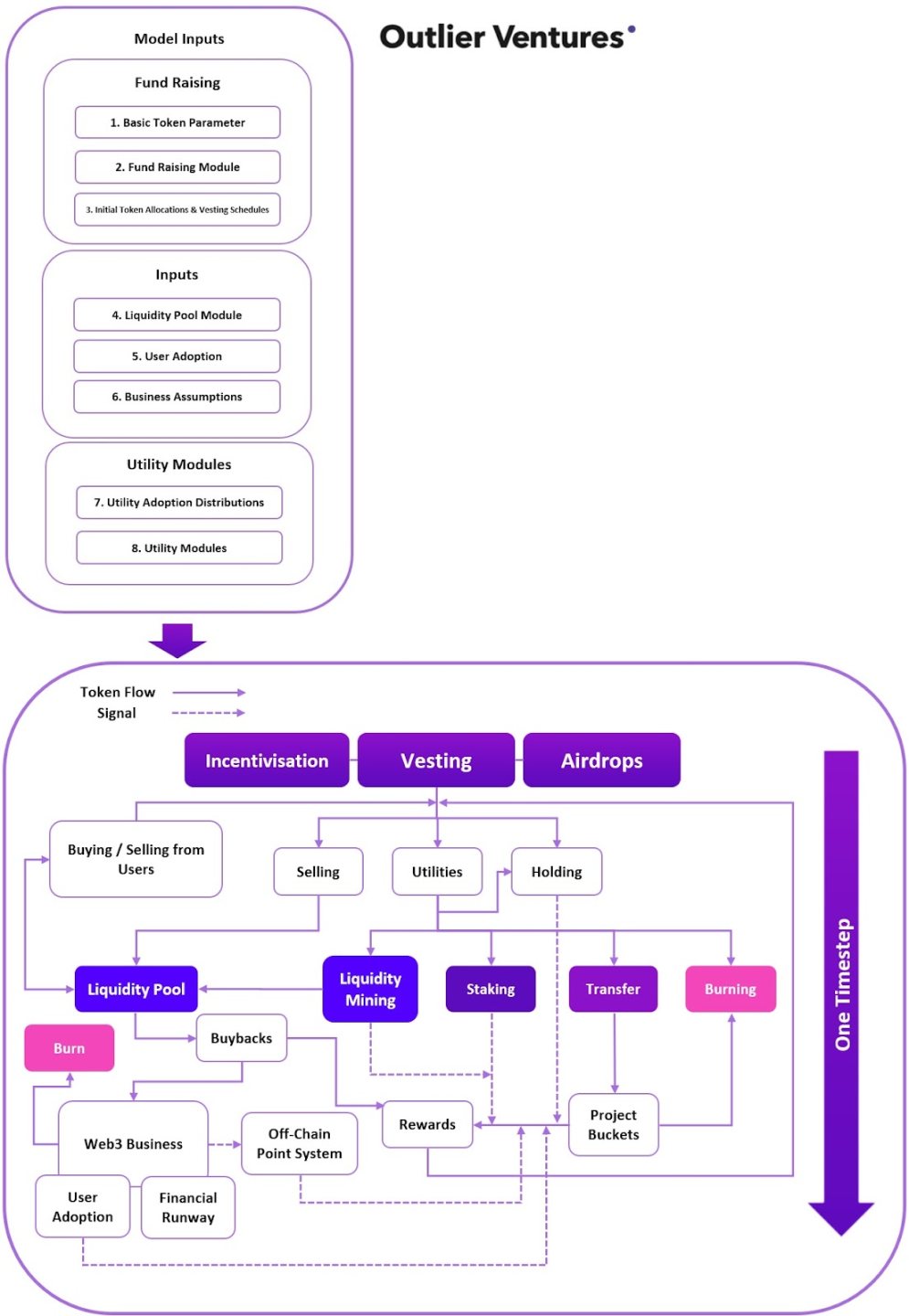

The following case study shows the impact of vesting schedules of different lengths on token valuation. It was conducted using the Outlier Ventures open-source Quantitative Token Model (QTM) radCAD under standard settings and moderate adoption assumptions. Figure 2 shows the general structure of QTM, which has evolved continuously since its initial release.

Figure 2: Abstract structure of Quantitative Token Model (QTM)

Remember, no model can predict any token valuation, and they should not be considered financial advice, especially suggestions from static and simplified models. However, through QTM, we can assume a given adoption scenario and then apply different vesting schedules to test what would happen if they were altered. In the study below, the model applied the same conditions except for different vesting periods to understand the impact of vesting periods on token valuation stability.

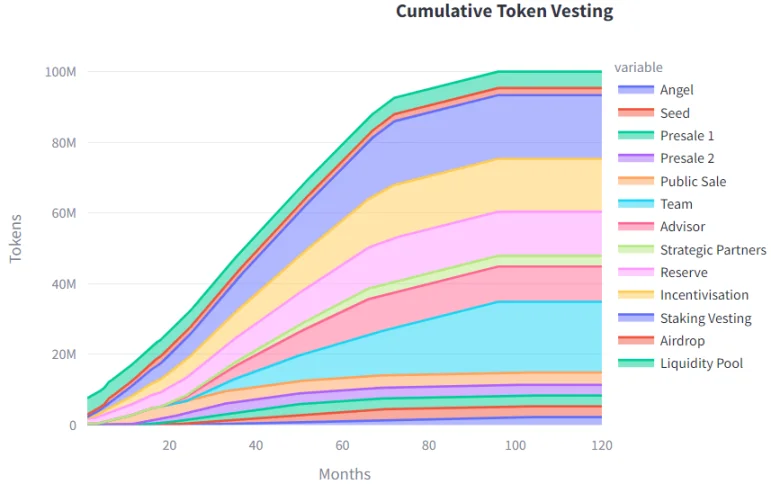

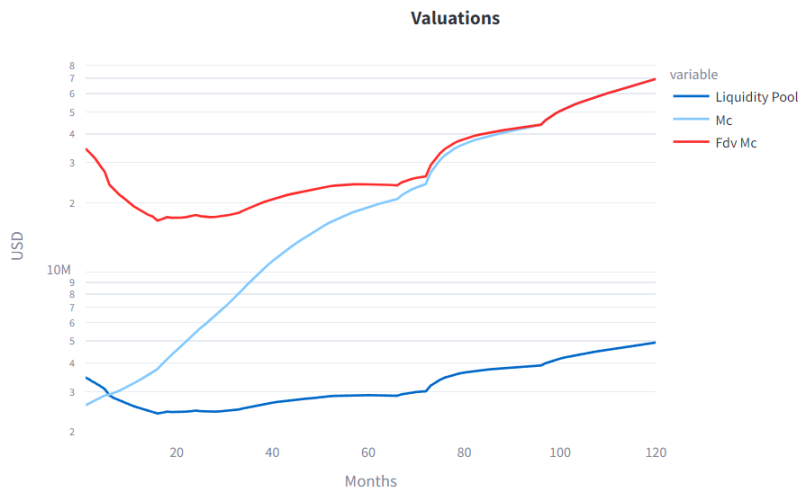

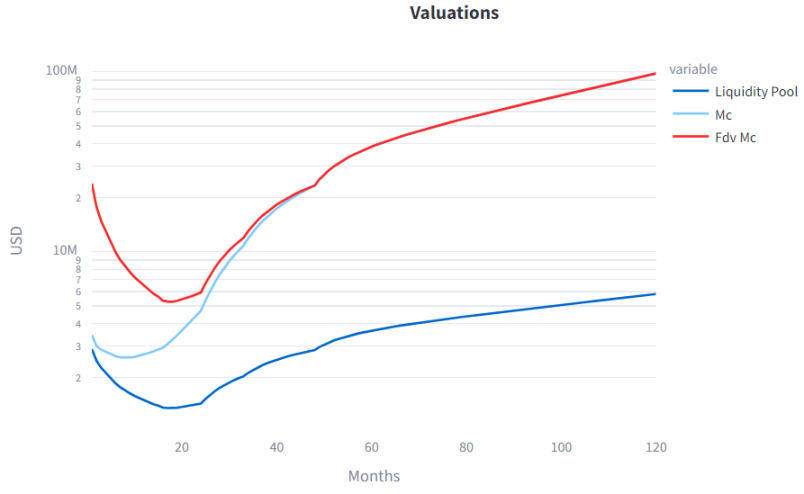

Figure 3: Slow (top) and fast (bottom) vesting schedules in the Quantitative Token Model (QTM) case study

Figure 3 shows the assumed vesting schedules in two test scenarios. The top figure depicts slow vesting, while the bottom figure depicts fast vesting. It involves various stakeholders such as different funding stages, early investor groups, teams, advisors, partners, reserves, incentives, and staking vesting, airdrops, and liquidity pools. These ecosystem participants are common for various protocols. In this case study, no specific product or token utility was specified, except for general staking and transfer utility that can represent various different mechanisms (e.g., store purchases or ecosystem transaction fees). The exact use case is unrelated to this study.

In the case of slow vesting, it takes 8 years to fully release all tokens into the economic system; while in the case of fast vesting, it takes 4 years. This includes the period from the token issuance start, including lock-ups, with most investors completing vesting ahead of time.

Figure 4: Token valuation resulting from slow (top) and fast (bottom) vesting schedules as per QTM simulation

Figure 4 shows the token and liquidity pool valuation simulated by QTM under the two different vesting plans given in Figure 3. It is worth noting that the vertical axis is on a logarithmic scale. In both cases, the fully diluted valuation (FDV) market cap (MC) at launch is $40 million. Both cases exhibit similar curve shapes, with FDV MC decreasing at the start of the simulation and starting to rise after a period of time. The circulating MC only decreases in the fast vesting scenario, but also starts to increase after 8 months. A decline in valuation over the first 2 to 3 years is observed in many Web3 token issuances, due to the release of a large token supply to the market while the startup is still in the building phase. Subsequently, assuming successful business models, token design, and go-to-market methods, valuation may rise again due to increased demand.

An interesting point is the valuation range in both scenarios. Compared to the launch valuation, the FDV MC in the slow vesting scenario decreases by approximately 58% after 16 months and reaches a peak increase of 74% at the end of the 10-year simulation. In the fast vesting scenario, the FDV MC valuation decreases by approximately 87% after 18 months, but reaches a peak increase of 145% at the end of the simulation. While QTM cannot predict these results in an absolute manner, it allows us to gain insights into the effects of parameter variations under the same boundary conditions and basic assumptions. It is noteworthy that slower vesting leads to a smaller difference between final valuation and launch valuation, resulting in less volatility compared to the fast vesting scenario. Slower vesting leads to a smaller decrease in valuation, but at the cost of potentially reducing long-term upside potential.

Here we need to discuss two issues: (1) What is the fundamental reason for this phenomenon? (2) What does this mean for our own vesting schedule design?

- The reason for a greater decrease in valuation in the fast vesting scenario is the release of more token supply into the economy in a shorter time. When more supply meets the same demand, it leads to a more severe decrease in valuation. At the same time, releasing more supply into the economy faster results in less supply released later. In both cases, it is assumed that Web3 business and token demand continue to grow healthily. Therefore, compared to the slower vesting scenario, there is less supply released later in the fast vesting scenario, resulting in higher valuation later when demand remains the same.

- Considering the previous reasoning, we can conclude that faster vesting schedules tend to be beneficial for long-term token valuation. This is true in the given circumstances, but there are still more factors to consider, such as community sentiment. Significant devaluation of tokens is rarely associated with positive market perception, and may even lead to long-term damage to the protocol's image, ultimately resulting in decreased adoption. While the protocol cannot control market conditions and actual token demand, there are still some factors that can be controlled, such as vesting schedule design.

Conclusion

The above discussion and case study indicate that there is no perfect static vesting schedule that considers all influencing factors, such as the interests of early investors and contributors, market participants, fairness, investability, sustainability, token stability, and appropriate incentives. Every vesting schedule is a compromise.

QTM simulations show the differences in token valuation and volatility between slow and fast vesting plans. We acknowledge that this is not an accurate prediction of the future, as the model has a static and deterministic nature, but it supports the conclusion that slower vesting tends to result in less volatility. Although the simulation shows higher long-term token valuation in the fast vesting scenario, it could damage the potential reputation of the protocol if early market investors and token holders suffer significant losses.

Another aspect of vesting schedule design that should not be underestimated is the complexity and intricacy of implementing vesting schedules. In the author's view, the most favorable vesting occurs when it aligns with actual demand and protocol adoption, as it benefits all participants, including early investors. However, this approach requires careful engineering design and on-chain execution, which may be challenging for all early, especially smaller-scale, Web3 startups.

If the protocol does not have the capability to adopt more advanced methods, good practices can still be applied to traditional static vesting schedules to better design the token economy:

- Vesting schedule design corresponds to various nodes in the protocol's growth roadmap.

- Tokens should not be released to the market if there is no utility and fundamental demand.

- Web3 businesses go through three stages: build, expand, and saturate. Most tokens should be distributed at the start of the expand stage, not during the build stage. Matching lock-ups and vesting periods accordingly is crucial.

- Early investors need to be thoroughly explained the delay in vesting through lock-ups and longer periods. Ultimately, they will benefit from a conservative vesting plan as it provides breathing room for better product adoption, thus providing more counterparties for their profits to materialize.

- There is no perfect vesting schedule, and only if the Web3 business has the capability, should more engineering resources be allocated to advanced token vesting design. Therefore, finding the appropriate compromise among the various aspects discussed above is crucial.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。