The most mainstream is the utilization-based pricing model used by Aave.

Author: David Ma

Translation: Luffy, Foresight News

In Part 1, I classified the lending protocols in Web3. To quickly recap, a lending protocol is a set of rules used to manage how borrowers temporarily borrow assets from lenders and commit to returning these assets. This protocol will define how interest is charged to borrowers and how collateral is built to protect lenders. Part 1 of this series explored topics related to interest periods: current and fixed-term, loan rolling, perpetual, etc., and classified some protocols within this framework.

In this article, I will continue to discuss how various lending protocols determine interest rates.

Interest Rates

Interest rates are the additional fees that borrowers pay to lenders. For ease of comparison, interest rates are usually quoted in annualized format, expressed in annual percentage rate (APR) or annual percentage yield (APY). The difference between the two is that APR assumes no compounding, while APY assumes compounding. For example, an APR of 10% compounded semi-annually would result in an APY of 10.25%.

The relationship between the two is represented by the following formula:

APY = (1 + APR / k)^k — 1, where k is the number of compounding times per year.

In Web3, most loans are continuously compounded (with a large k value) because most loans are current loans. Therefore, they quote in APY to tell lender users how much they will earn in a year assuming the interest rate remains unchanged. For fixed-term loans, APR quoting is more common.

By the way, if the 2020-style rudimentary liquidity mining comes back, be wary of APY predatory quoting, as these opportunities will not last long, and the compounding results are difficult to achieve. It is much more reliable to calculate with APR in mind. For fixed reward pools, doubling TVL means halving the rewards.

Now, after explaining the definitions, we can discuss interest rate pricing.

Pricing Methods

Pricing is the mechanism for calculating how much interest borrowers and lenders pay each other. Although not exhaustive, this article will introduce some of these mechanisms:

- Order book pricing: Most flexible and market-driven, but requires a trade-off in user experience

- Utilization-based pricing: This model has found product-market fit in DeFi, but its efficiency is not 100%, and it performs poorly in extreme cases

- Auction: Good pricing, high loan efficiency, but requires advance planning by users, secondary market fragmentation, and other minor frictions

- Ajna utilization model: A modification of the classic utilization model, suitable for use in oracle-less protocols

- Tazz perpetual loan financing model: A new p2pool loan primitive that allows the market to price interest rates, making collateral fully modular

- Manual pricing: Governance-led pricing

Order Book Pricing

The most common asset pricing method is to allow the market to adjust itself through an order book. Borrowers and lenders place limit orders, specifying the amount and interest rate they are willing to borrow or lend. When orders match, the transaction is executed.

However, order books also have drawbacks:

- Inexperienced users do not know how to price for themselves. These users just want to trade without paying huge costs.

- Placing limit orders is like a free option. The worse the market liquidity, the slower the block time, the more valuable the option. In other words, the more the theoretical true price changes when orders are not executed, the greater the option value contained in these limit orders themselves.

- Good operation of the order book requires active management. You need to cancel outdated limit orders and play the bidding war game with other participants.

- It requires a large number of transactions.

This is why order books are still not popular on-chain. Instead, AMM, RFQ, and auctions are more suitable for blockchain products.

In terms of lending, order books face even greater challenges:

- Order book trading creates peer-to-peer loan matching, and default risk is irreplaceable.

- Continuous issuance of fixed-term loans creates positions that cannot be fully swapped with each other. Instead, protocols like Pendle and Notional choose to issue loans with fixed terms on specific dates. Available loan terms are 37 days, 159 days, etc., which is somewhat strange.

- Short-term loans create more transactions. You can automate rolling, but how do you price the next loan?

All of these lead to market fragmentation, or at least a complex trading experience. That is to say, NFT lending platforms like Blur and Arcade.xyz still rely on a user experience similar to order books. They have come up with features to mitigate poor user experience.

Blur integrates a form of perpetual loans to eliminate the dimension of term.

Blur and Arcade both have "collection offers," where lenders view the entire NFT collection as interchangeable, and any NFT in the collection can be used as collateral.

Ever wondered how to interpret Blur's collection lending chart? I wrote a post about it here.

Arcade's P2P loan matching and collection offers

AMM is a subclass of order book. If a protocol can gather enough people into the lending market for interchangeable tokens, then AMM is a good choice. Interest rates have better mean reversion ability than token prices, so using AMM to obtain LP rates is safer than LP tokens. This is how Pendle, Notional, and Tazz work.

In summary, while order books can handle simple assets well, lending order books have too many dimensions to consider and require clever ways to reduce the complexity of user experience.

Utilization-Based Pricing

The utilization rate of a lending asset pool refers to the ratio of the total amount of borrowed assets to the total amount of lendable assets.

Utilization-based pricing defines interest rates as some increasing function of the utilization rate.

The first and largest on-chain lending platform, Aave, adopts this approach. It is still the most popular interest rate pricing method for liquidity and interchangeable assets.

Please note that Aave did not start with this design. EthLend (the name before Aave rebranding) outlined a p2p fixed-term order book in its 2018 whitepaper, and the utilization-based model was introduced in their 2020 whitepaper. This thorough rethinking of financial primitives (Uniswap AMM is another example) is one of the joys of DeFi.

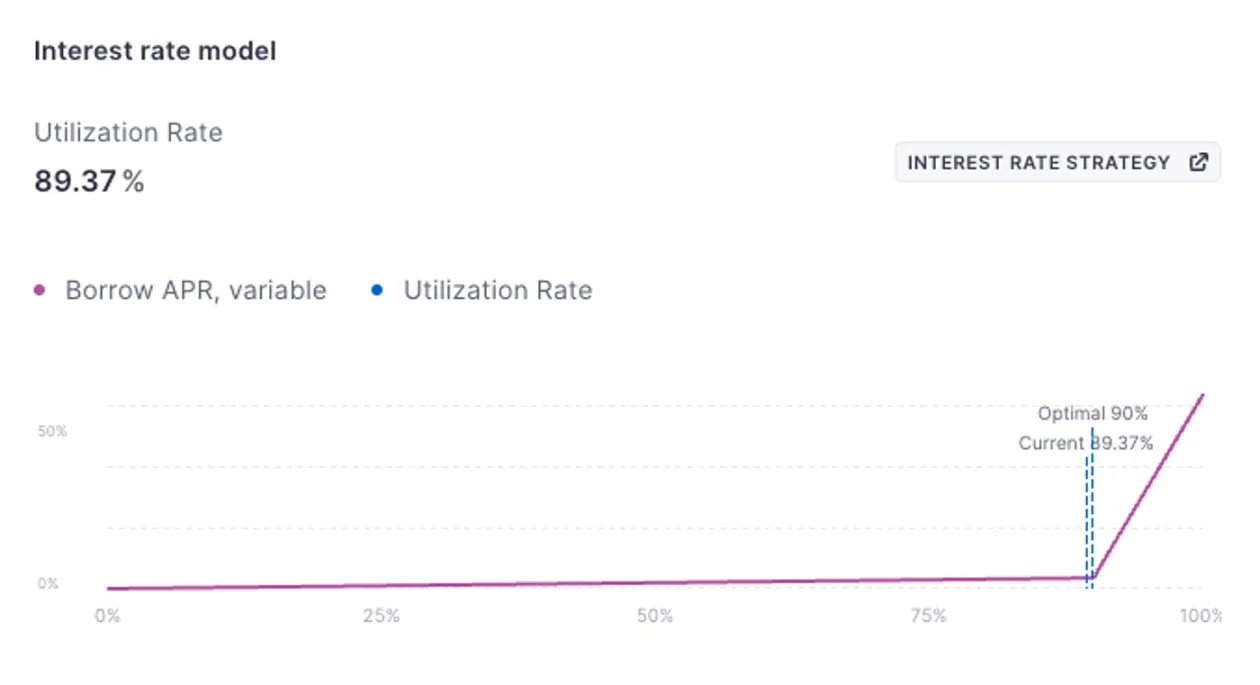

Aave's borrowing rates

Since the whitepaper does not explain the motivation behind this method, my guess is very simple. Consider an economic model—when interest rates are high, fewer people are willing to borrow, and more people are willing to lend. The "optimal" interest rate is when the number of borrowers matches the number of lenders, and the utilization rate is 100%.

When interest rates are too low, there are more borrowers than lenders. The utilization rate will reach 100%, but it does not tell us where we are in the model. Additionally, lenders cannot exit their loans.

When interest rates are too high, a large supply of loans will be idle. The APY spread (1 - utilization rate) increases as the interest rate increases. This is before the platform charges fees.

The challenge is to keep the interest rate close to the optimal rate while maintaining a buffer for lenders to exit, as the unobservable lending curve changes with market conditions.

The term "interest rate mode" used by Aave is a bit misleading. Math enthusiasts like to call it a PID controller, but it is only partially automated. Aave first selects a target utilization rate (e.g., 90%) and a twist curve. If the utilization rate frequently exceeds 90%, Aave's governance will steepen the interest rate curve, attempting to lower the utilization rate. If the utilization rate is too low, the opposite occurs.

Sometimes, the PID controller reacts too slowly to market conditions. For example, during the Ethereum merge in September 2022, pre-merge ETH will be forked into PoS ETH and PoW ETH. The market values PoW ETH at about 2% of the value of PoS ETH. Market participants saw this and wanted to hold as much pre-merge ETH in their wallets as possible. One way to do this is to use stablecoins as collateral and borrow ETH. As long as the cumulative interest within the borrowing period is less than 2%, it is a profitable trade. Earning 2% in less than a week means being able to pay over 100% APR. Aave's interest rate cap is 100%. Needless to say, in the days leading up to the merge, the utilization rates for ETH on Aave, Compound, Euler, Inverse, and every PID controller lending protocol reached their limits. If I remember correctly, Inverse did not set an interest rate cap, and the APR eventually reached 1000%.

One final note about utilization-based pricing is that it naturally fits with the peer-to-peer structure, making it suitable for current loans. Therefore, we often see these attributes naturally combined.

In summary, the benefit is a user experience under normal market conditions: borrow and leave at any time. But when the utilization rate reaches 100% (such as during the Ethereum merge), lenders are left in a non-recourse situation. Other drawbacks include 10% of loan buffer assets leading to low capital efficiency, and the inability to provide fixed-term loans.

Auction

Auction is a time-tested method for issuing new debt (primary market issuance). US Treasury bonds are the most liquid government securities globally, and they use auctions to price new debt. In lending protocols, borrowers and lenders submit secret bids to regularly held auctions to find the market clearing interest rate and issue new debt to participants at the clearing rate.

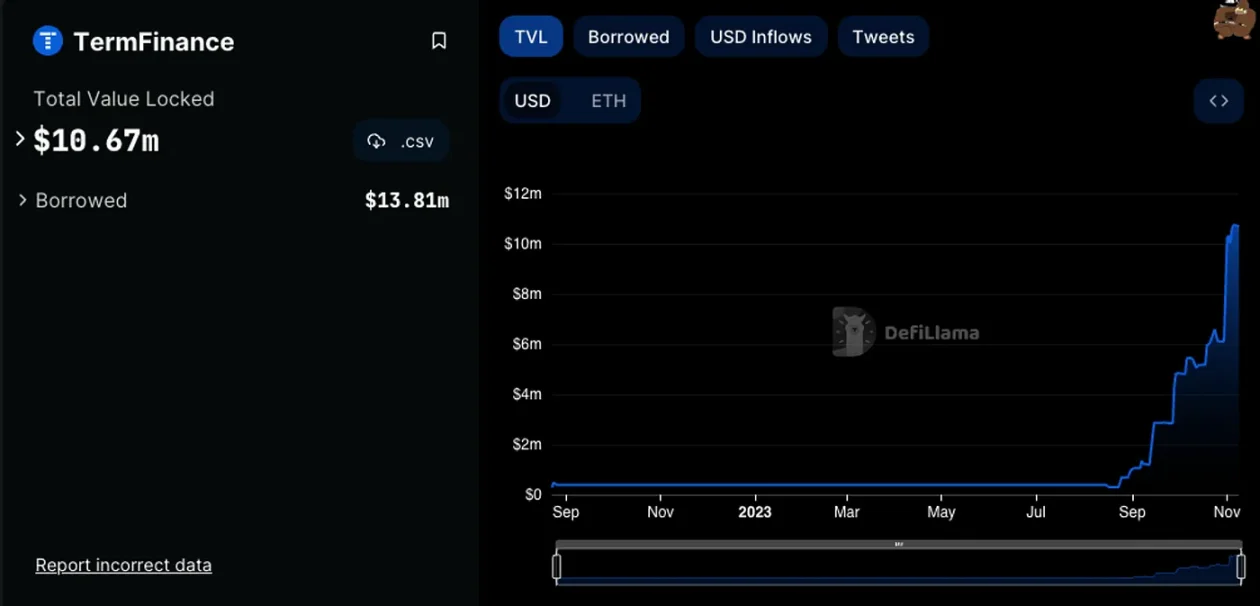

Term Finance is a relatively new protocol inspired by this mechanism. Their auction implementation details are worth reading.

Auctions can effectively match lenders and borrowers. Unlike order books, which require capital to be locked up for pending orders or loan pools based on utilization models that need to provide a buffer for lenders, no capital is idle. The only non-productive period is the time when assets are locked during the auction.

Auctions also produce high-quality pricing because market participants gather at a Schelling point to aggregate their information.

The downside is that auctions require some advance planning and are not as user-friendly. This is a good choice for US Treasury bonds, but in the cryptocurrency space, participation in the fixed-term loan market is not high enough. Another challenge is market fragmentation, as cryptocurrencies have many similar but non-interchangeable assets. This would be a more difficult product to launch, but I hope that one day, Term Finance will be able to issue Ethereum Treasury bonds with full support from the Ethereum community.

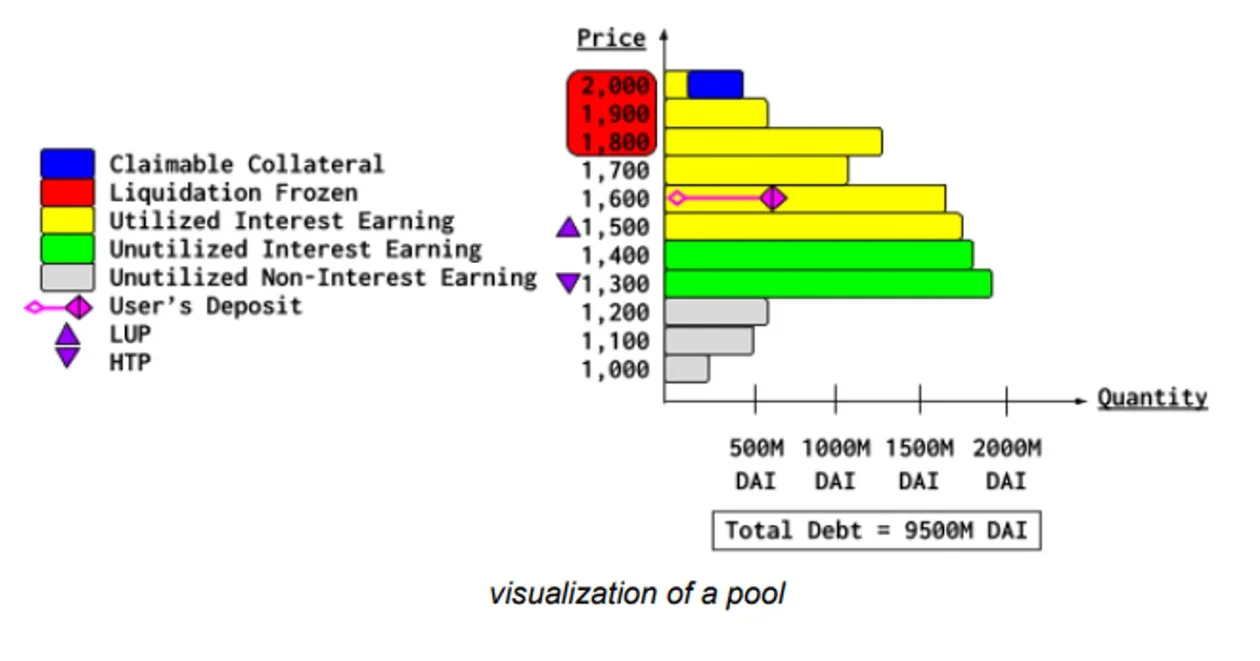

Ajna's Utilization Model

Ajna is one of the few lending protocols that does not rely on oracles. A full explanation of how Ajna achieves this goal is beyond the scope of this article. Instead, its interest rate design is worth discussing.

Lenders first select the valuation of the collateral (e.g., ETH) they are willing to lend tokens (e.g., USDC) against. Borrowers match from the highest valuation downwards. Borrowers with the highest risk (highest loan-to-collateral ratio) set a "highest threshold price" (HTP), and borrowers with lower valuations do not earn interest.

https://www.ajna.finance/pdf/Ajna_ELI5.pdf

Lenders do not want to set the valuation too high because they may incur losses due to default. Lenders also do not want to set the valuation too low because they will not earn any interest.

The interest rate is determined by the utilization rate function, but the calculation here only considers lenders who set the collateral valuation higher than the HTP. The interest rate starts at 10% and is multiplied or divided by 1.1 every 12 hours, depending on the comparison of the utilization rate to the "target utilization rate."

The main advantage is that, despite using a pool design, this mechanism operates without any oracles. On the other hand, lenders need to constantly monitor their valuations. Like other utilization-based interest rate pricing mechanisms, the APR is also affected by the lending that is not utilized.

Although borrowers and lenders can leave at any time (current), Ajna's minimum loan period is 1 week. Since Ajna has not been in the market for long, it is still too early to fully understand the pros and cons of this mechanism.

Truly permissionless and immutable protocols are rare because they are difficult to execute correctly. But when they do happen, they become the cornerstone of composability. I sincerely hope that Ajna can become the Uniswap of the lending world.

Tazz's Perpetual Loan Financing Model

Tazz is an upcoming lending protocol that introduces a new interest rate pricing primitive. Similarly, a full description of this mechanism is beyond the scope of this article.

Like Aave, Tazz debt starts as interest-free perpetual loans. Debt tokens (ATokens in Aave's terminology) can be traded on any DEX. Except for protocol bankruptcy, Aave's ATokens are almost always close to 1:1 with the actual token trading price, while Tazz's debt tokens (ZTokens) are priced by the market. The price of ZTokens determines the nominal debt's accumulated interest rate (i.e., funding). If the nominal debt continues to increase, collateral parameters will trigger liquidation.

Continuous funding payments are proportional to k (1 - ZToken relative to token price TWAP). The lower the k, the longer the loan term, and the more susceptible it is to interest rate risk.

Note that in this mechanism, collateral and the rest of the protocol are fully modular. You can set up collateral-free, NFT collateral, LP tokens, illiquid tokens, locked tokens, oracle-based collateral pricing, or one-time pricing asset pools. This does not matter because the market can price the interest rates required to take on the risk.

This enables:

- Peer-to-peer lending

- 100% loan utilization, hence lower spreads

- Merged liquidity

- Any collateral type

One potential drawback is that it requires monitoring of the pool price (but less than Ajna). If unrealistic prices persist for too long, it can lead to unrealistic interest rates. The liquidity market for ZToken will allow borrowers and lenders to not have to monitor too closely.

Manual / Governance Pricing

Given the GHO de-pegging, this model is worth mentioning. There are some debt collateral positions (CDPs) stablecoins. Maker's DAI is the largest, followed by Liquity's LUSD, Lybra's eUSD, Prisma's mkUSD, and others.

Although CDPs may not look like loans, they are. Borrowers collateralize with ETH (Maker v1), LST (Prisma, Lybra), or other assets. The borrower creates a CDP, and the protocol's oracle calculates the dollar value at a 1:1 price. CDPs can be sold on the open market, allowing the borrower to "borrow" another asset, and the lender receives the CDP. The loan is perpetual, and the value may not be fixed at $1. Borrowers pay interest to the protocol, and lenders can receive another interest rate from the protocol (e.g., Dai savings rate). Sometimes, there is a "stability module" as a protection fund to prevent CDP de-pegging.

The downside of manual pricing is that it is affected by governance processes, lengthy debates, low community governance participation, and therefore, the response is slow. The benefit is that human processes are harder to manipulate than code that may lead to extreme situations.

GHO has been declining since its creation

Aave's GHO is a CDP with manual interest rates. Currently, the borrowing rate for GHO is 3% (lower than Treasury bonds and Dai's 5%), and their lending (savings) rate on Aave is 0%. Therefore, there are too many borrowers and too few lenders, leading to the decline in GHO price.

The debate on Aave's governance forum has been ongoing for several months. The essence of the debate boils down to whether to peg the exchange rate or maintain stable interest rates (hence variable interest rates). GHO cannot have both until it gains more market dominance.

Conclusion

In this article, we have introduced various methods of interest rate pricing in lending protocols. Of course, there are many other methods, but the goal of this series is to establish a classification system. So far, we have considered interest term and interest pricing as the two main perspectives for analyzing and classifying protocols. In the next article, I will discuss collateral.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。