Author: flowie, ChainCatcher

MakerDAO, which has been gaining momentum on RWA, has been steadfastly investing in RWA assets for nearly half a year. Last month, it increased its RWA assets by $100 million within a week, currently holding over $3.3 billion in RWA assets.

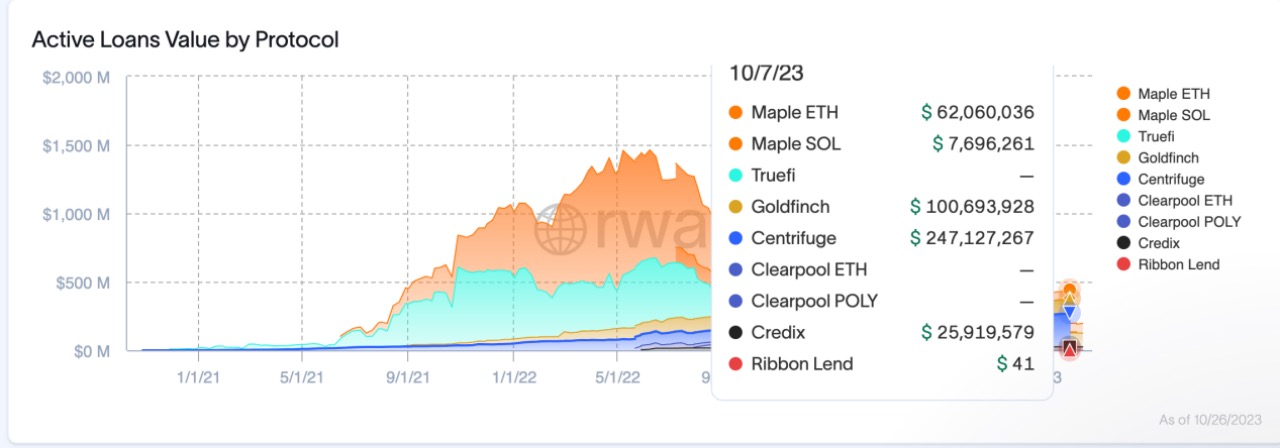

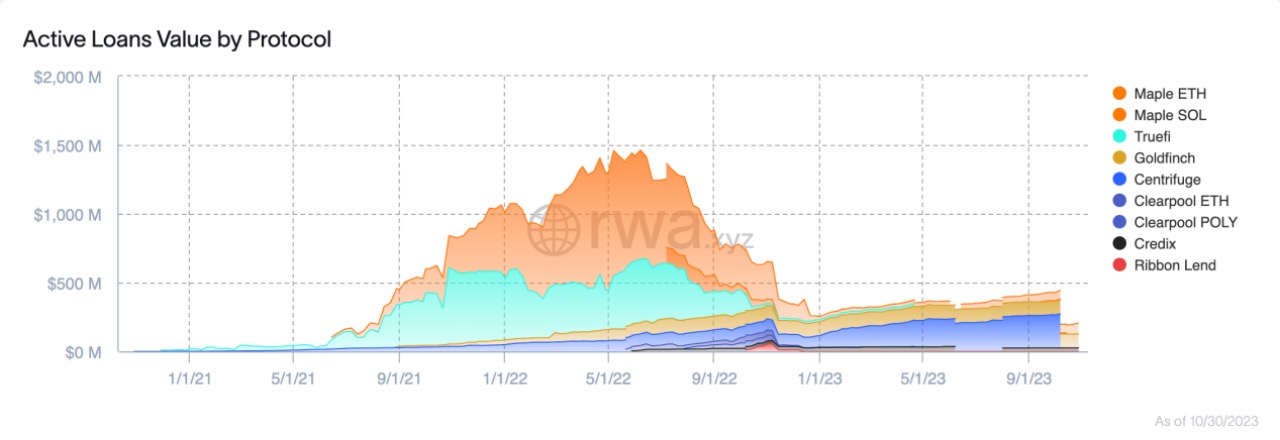

As the underlying technical service provider for MakerDAO's expansion of RWA assets, Centrifuge has also successfully capitalized on the trend this year, becoming the protocol with the largest active loan amount on-chain. According to RWA.xyz data platform, the active loan amount of Centrifuge on January 1, 2023, was approximately $84 million, and as of now, it has grown to over $240 million, an increase of 286%, far surpassing the former credit leaders Maple and TrueFi.

According to the crypto data platform RootData, Centrifuge has completed four rounds of financing, raising a total of $15.8 million, with investors including Coinbase Ventures, IOSG Ventures, and others.

Despite gaining favor from the top DeFi platform MakerDAO and well-known investment institutions, Centrifuge, like Maple and TrueFi in the past, cannot avoid defaults and bad debts. Earlier this year, Centrifuge was reported to have approximately $5.8 million in overdue loans in two lending pools. In August, the community also claimed that impending loan defaults would put MakerDAO's $1.84 million investment at risk. According to RWA.xyz, Centrifuge currently has accumulated over $15.5 million in unpaid loans. The MakerDAO community even proposed to stop providing loans to the tokenized credit pools on Centrifuge.

As the fastest-growing on-chain credit protocol this year, how does Centrifuge operate? And what mechanisms does it have in place to deal with controversial defaults and bad debts?

RWA Becomes the New Lifeline for On-Chain Credit, Centrifuge Rises to the Top

In addition to on-chain US Treasury bonds, on-chain lending has also played a role in boosting the RWA track, with well-known DeFi platforms such as MakerDAO, Compound, Frax, and Aave all making moves in this field. Apart from these established DeFi platforms, some on-chain credit protocols have also benefited from the RWA narrative. According to RWA.xyz data, on-chain credit increased by over $200 million from January 1 to September 30, a growth of over 80%.

However, compared to traditional credit markets where credit loans have a large market share, the development of credit in the crypto field is just beginning. Around the end of 2021, institutional on-chain credit protocols represented by TrueFi and Maple emerged. In contrast to the traditional DeFi over-collateralized lending model of Compound and Aave (lending one type of digital asset by over-collateralizing another type of asset), they mainly provide low-collateral or uncollateralized lending services to crypto-native trading institutions, market makers, and others. However, applying institutions need to submit some information for credit review, such as monthly reports including balance sheets, and annual independent audit financial statements. Even on Maple, borrowers need to register with the credit risk data platform Credora, which provides real-time information to lenders to help them assess the risk levels accumulated by borrowers on different crypto trading platforms.

The low-collateral or uncollateralized credit model has also attracted many institutional clients, such as Alameda Research, Wintermute, BlockTower, and others. In mid-2022, Maple's active loans on the Ethereum chain alone reached nearly $1 billion, and TrueFi also reached nearly $500 million at its peak. Goldfinch, which has active loans second only to Maple and TrueFi, raised $37 million in three rounds of financing from large crypto risk funds such as a16z and Coinbase Ventures, as well as angel funds including Balaji Srinivasan, Ryan Selkis, and Tarun Chitra.

However, as the crypto market entered a deep bear market and DeFi's overall liquidity was insufficient, and with the occurrence of CeFi defaults, institutional lending protocols represented by Maple and TrueFi suffered significant defaults. For example, after the Terra and Three Arrows Capital default incident in June last year, Maple Finance officially stated that after the bankruptcy of the crypto lending company Babel Finance and the default of $10 million in loans, it might face short-term liquidity challenges and cash shortages.

With the FTX default, Maple Finance experienced even larger-scale bad debts. Due to its borrower Orthogonal Trading's misreporting of the FTX risk exposure and the impact of the FTX incident, Maple Finance defaulted on $36 million in unpaid loans in the M11 credit pool due on December 4, 2022. Funds from multiple institutions such as Nexus Mutual and Sherlock deposited in Maple Finance's lending pool were affected. Similarly, TrueFi also suffered defaults from BlockWater. By the end of 2022, both Maple Finance and TrueFi had significantly decreased to around $20 million.

In 2023, with the rise of the RWA narrative, there has been a turnaround in the on-chain lending field, and the market landscape has undergone significant changes. In addition to the former leading credit protocols represented by Maple seeing a rebound in the active loan amount on-chain, there are also protocols like Centrifuge, which has been low-key but has experienced rapid growth in on-chain credit data, surpassing Maple to become the new leader in the credit field. Goldfinch, favored by many well-known capital institutions including a16z, has been steadily developing without much growth or significant decline.

Previously hit hard by the uncollateralized credit model, Maple expanded to include collateralized lending models with real-world assets and over-collateralized models this year. In addition, in April this year, Maple launched an on-chain US Treasury bond lending pool, restarted its lending pool on Solana, and went live on the Base network. In August, Maple completed a $5 million financing round. The active on-chain loans of Maple have now grown from over $20 million at the beginning of the year to nearly $100 million.

Compared to Maple, Centrifuge, which has been dedicated to collateralized lending with real-world assets from the beginning, has seen even more significant growth. The active on-chain loans of Centrifuge have now grown to over $240 million, nearly tripling from the beginning of the year, making it the largest protocol for on-chain credit loans at present.

MakerDAO Boosts Centrifuge to Become the New Leader in On-Chain Credit

Centrifuge is actually an early on-chain lending protocol, founded in 2017. Unlike credit protocols such as Maple and TrueFi, which are more oriented towards crypto financial institutions, Centrifuge emphasizes lending against traditional real-world assets and can be considered one of the earliest players in RWA.

As early as 2020, Centrifuge, as a technical service provider, helped MakerDAO build an RWA vault with 6s Capital's real estate development guaranteed loans as collateral. The rapid growth of Centrifuge's on-chain active loans this year is mainly attributed to MakerDAO's layout in RWA assets.

Centrifuge's official website reveals that out of the 6 lending pools, 8 are related to MakerDAO. For example, there are investments in real estate bridge loans through the New Silver series, investments in structured credit through the BlockTower series, and investments in trade credit based on accounts receivable through the Harbor Trade Credit series, with MakerDAO being the priority investor in these pools. (Further details on Centrifuge's tiered investment mechanism will be discussed later). Currently, the funds related to MakerDAO amount to approximately $200 million, accounting for 80% of Centrifuge's total TVL (approximately $250 million).

According to the MakerDAO asset inventory statistics, the BlockTower S3 and BlockTower S4 vaults integrated with Centrifuge were established this year and have provided $70 million and $56 million in DAI supply, respectively, as of now. This means that MakerDAO has provided over $120 million in loan funding support to Centrifuge this year.

Currently, the APR of the funds related to MakerDAO ranges from 4% to 15%, mostly higher than the average 4% APR in DeFi.

In addition to MakerDAO, Centrifuge also became a technical service provider for Aave's investment in RWA assets as early as 2021. Aave and Centrifuge jointly established a dedicated lending pool for RWA, which operates separately from Aave's lending market and currently has a fund size of approximately $5.5 million.

In comparison to MakerDAO, Aave's investment in RWA assets through Centrifuge is still relatively small. However, with the ongoing popularity of the RWA narrative, Aave also intends to increase its RWA asset holdings this year. In August, Aave passed a proposal to collaborate with Centrifuge Prime to invest in US Treasury bonds, with an initial investment of $1 million USDC, aiming to increase the investment amount to 20% of the stablecoin holdings. Perhaps Aave's continued investment in RWA assets will bring a new wave of growth to Centrifuge.

How does Centrifuge achieve collateralized lending with real-world assets? What is the default risk mechanism?

As the preferred RWA technical service provider for established DeFi protocols such as MakerDAO and Aave, what problems does Centrifuge solve and how does it operate?

In general, Centrifuge, as a lending platform, is primarily focused on connecting two parties: those seeking to earn returns through lending, mainly crypto protocols such as MakerDAO and Aave, and those seeking financing, typically startups or organizations with real-world assets such as real estate, accounts receivable, and invoices. To bridge the gap between the real world and DeFi in terms of asset flow, Centrifuge needs to provide legal and asset on-chain support.

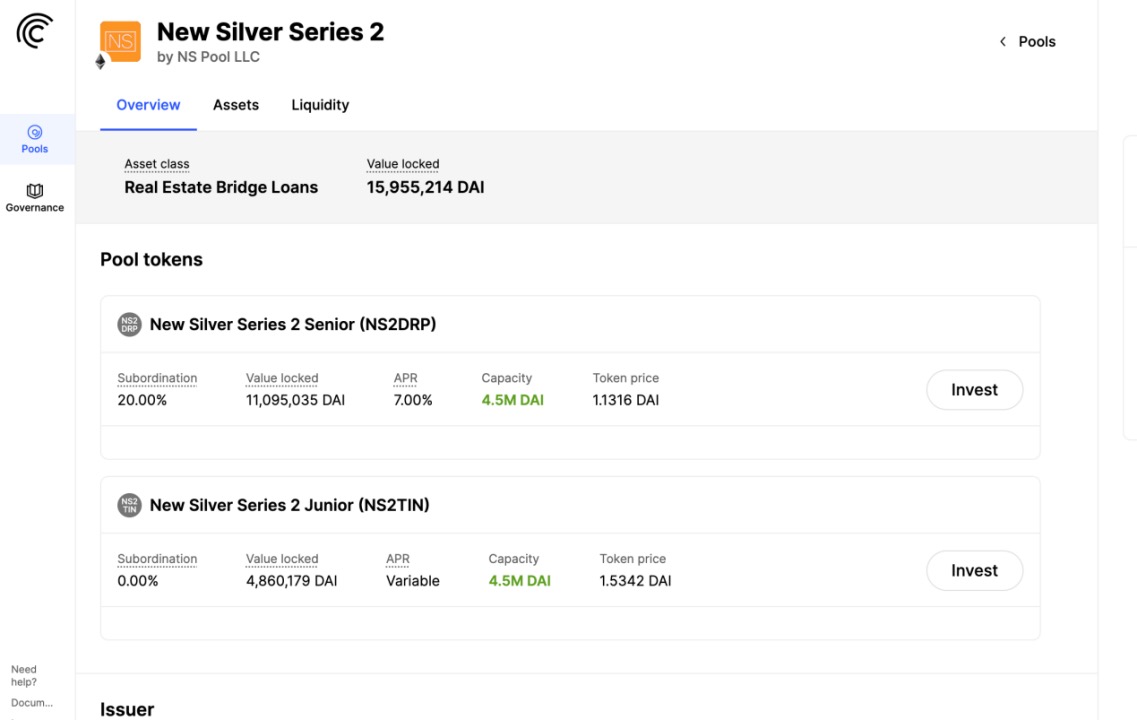

Due to the complexity of the entire process involving both on-chain and off-chain aspects, let's take the example of one of Centrifuge's lending pools, the New Silver Series 2, to analyze the entire operational process.

The New Silver Series 2 lending pool is initiated by New Silver as the asset issuer, providing financing for a portfolio of real estate bridge loans, which are provided to real estate developers for a period of 12 to 24 months. New Silver, established in 2018, is a non-bank lending institution that primarily provides bridge loans to the real estate industry to help borrowers pay for new property purchases before selling their existing properties.

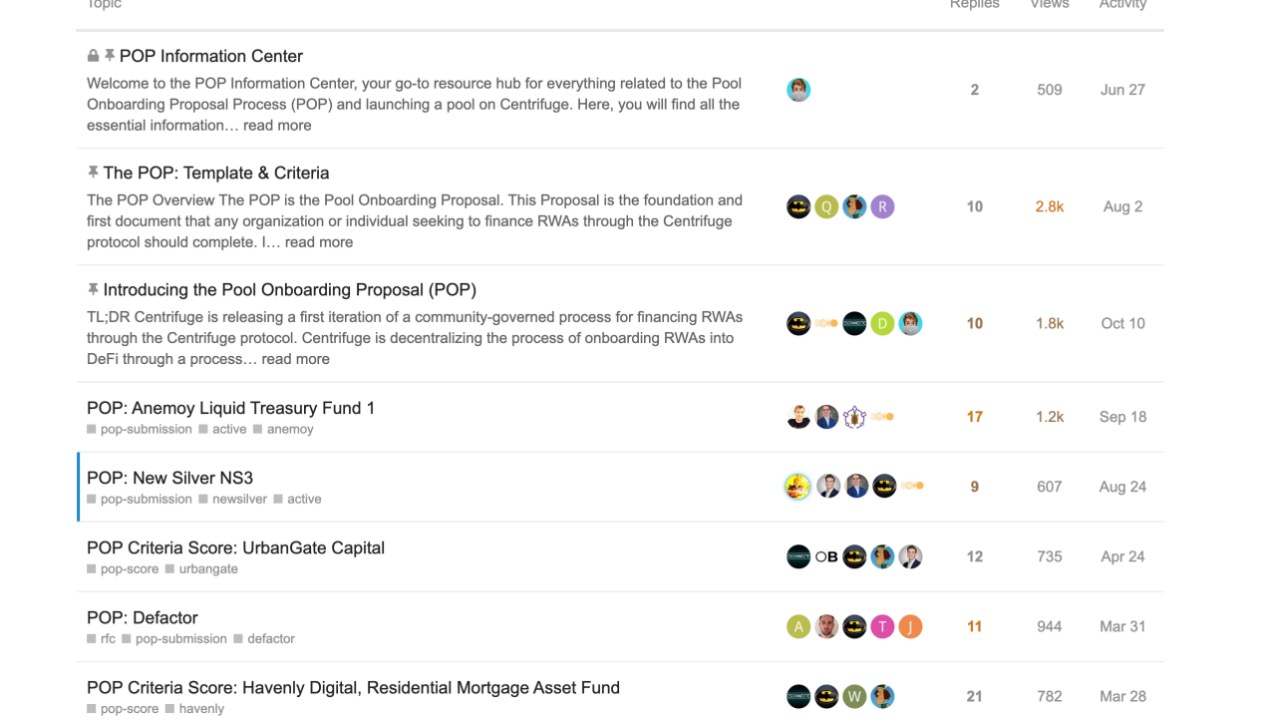

As the asset demand party, New Silver first needs to initiate a Pool Onboarding Proposal (POP) on the Centrifuge forum, clearly stating their purpose, credit situation, and the use of funds, among other details. (However, the POP for the New Silver Series 2 pool does not seem to be fully disclosed on the forum at the moment.)

The submitted POP will undergo due diligence and be subject to risk assessment and legal review by a third party, resulting in an analysis report. After the evaluation, it will proceed to the final discussion, where Centrifuge's credit risk group and CFG token holders will vote on the onboarding.

Upon successful onboarding, the asset issuer and investors need to initiate the process based on Centrifuge's off-chain legal risk framework and on-chain asset tokenization.

Off-chain, the asset issuer, New Silver, needs to establish a special purpose vehicle (SPV) to serve as the entity for this financing, segregating the assets to be pledged from the company's other assets. Additionally, a third-party professional team is required to conduct asset valuation, audits, and trust services to further enhance security. The borrower signs a financing agreement with the SPV.

For investors, Centrifuge needs to conduct KYC and anti-money laundering checks, currently mainly in collaboration with Securitize. Additionally, investors need to sign a subscription agreement with the SPV established by New Silver.

On-chain, the data needs to be stored on the Centrifuge Chain based on the Centrifuge P2P messaging protocol. New Silver can tokenize all off-chain real asset data on the Centrifuge Chain. This chain, developed on the Substrate framework, can share the security of the Polkadot network and has been bridged to Ethereum. New Silver can use the Centrifuge Chain to package the data into NFTs and collateralize them in Centrifuge's Tinlake lending pool (on the Ethereum chain) to initiate the borrowing mechanism, using the stablecoins provided by investors.

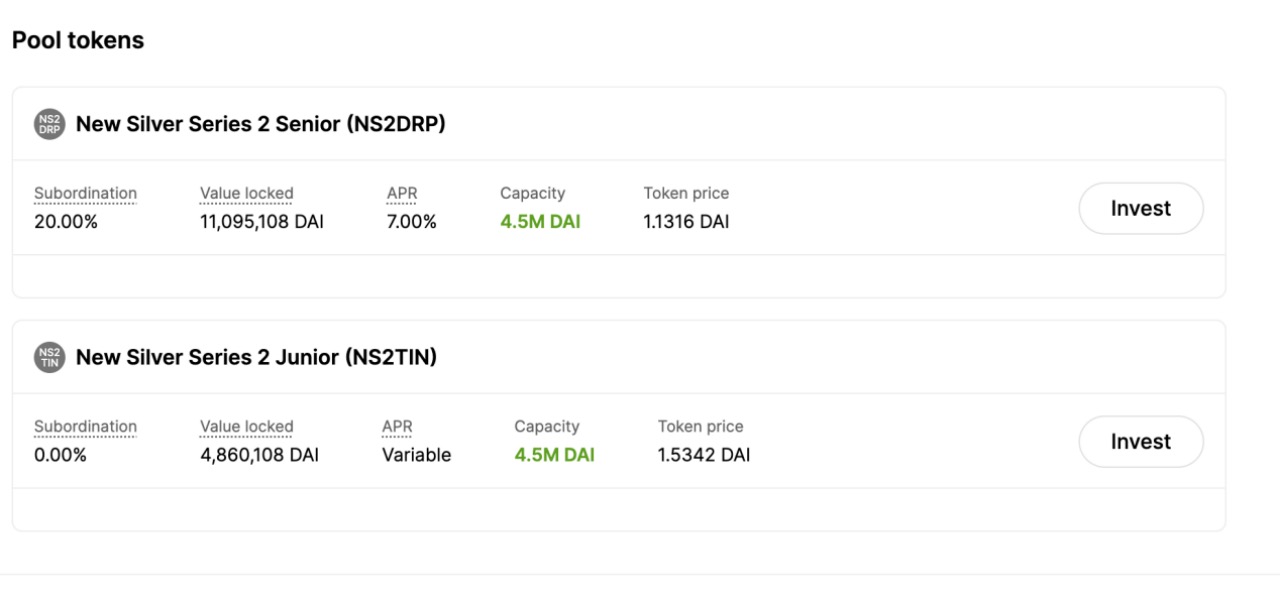

For investors, how do they participate in the Tinlake lending pool? What is the default risk mechanism for loans? Centrifuge has implemented a risk grading system and issued two different ERC20 tokens, DROP and TIN, with different risk and return profiles for investors to subscribe to.

Investors need to purchase DROP and TIN tokens with DAI. Holders of DROP tokens have priority in profit distribution from the asset pool and enjoy a fixed interest rate, while bearing losses in the event of risks (such as loan defaults), typically with lower risk and lower returns. For example, holders of New Silver's DROP tokens enjoy a fixed 7% interest rate. Holders of TIN tokens receive profit distribution after DROP token holders, with a floating interest rate, but need to bear losses first, typically with higher returns and higher risks.

To illustrate further, if the asset issuer/borrower borrows $1 million, with DROP token holders providing 20% of the funds and TIN token holders providing 80%, and the asset issuer/borrower needs to pay 10% interest after the period, DROP token holders are entitled to a 5% fixed interest rate as agreed.

Finally, when the loan matures, only $600,000 is repaid. In this case, the DROP token holders receive their principal of $200,000 and interest of $10,000 at a 5% interest rate. After the repayment, there is $390,000 remaining for the TIN token holders, but they originally invested $800,000, so they can only recover a portion of their principal.

However, if the DROP and TIN token holders provided 80% and 20% of the funds, and the asset issuer did not default, the DROP token holders would receive their principal of $800,000 and $40,000 in interest, while the TIN token holders would receive their principal of $200,000 and $50,000 in interest, at an interest rate of 25%, far exceeding the fixed 5% interest rate for DROP token holders. Therefore, investors can choose between DROP and TIN tokens to hedge risks and returns.

In addition to risk and return stratification, Centrifuge's lending pools are revolving and can be invested in and redeemed at any time, but it must ensure that DROP tokens are redeemed before TIN tokens, and TIN tokens cannot fall below the set minimum ratio. When the asset issuer repays the financing amount and interest at maturity, the pledged NFTs will also be returned to them.

Centrifuge's Commitment to Becoming RWA Infrastructure

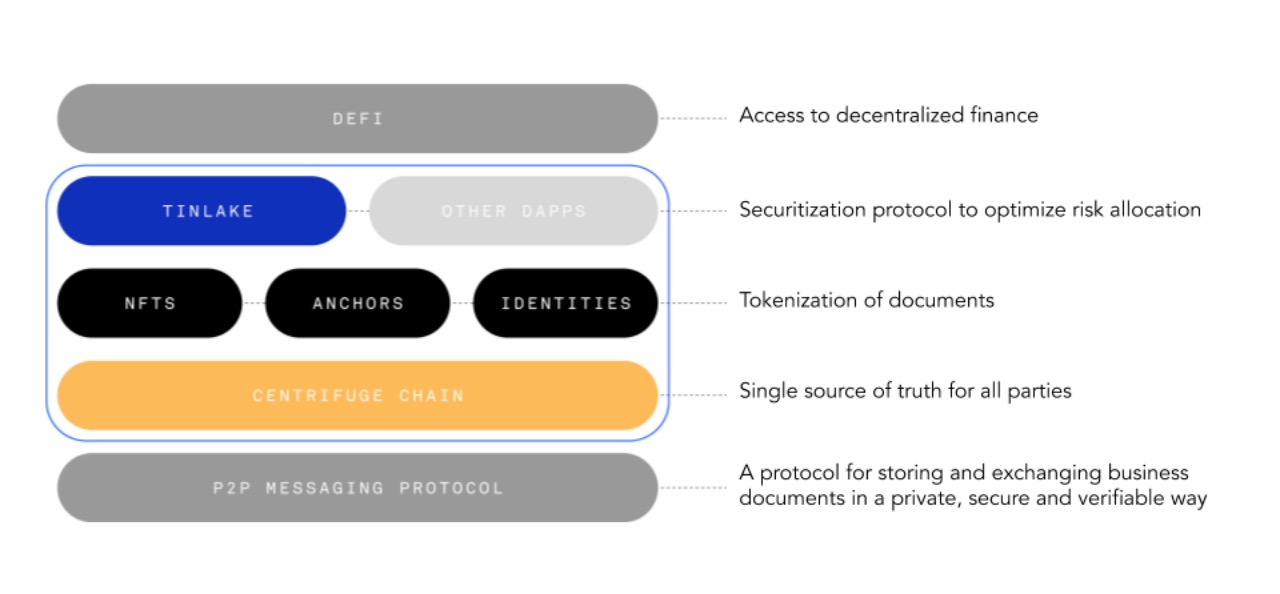

In general, as a platform bridging DeFi and real-world assets, Centrifuge has several core products and components in its ecosystem.

First is the Tinlake protocol, a lending platform for end-users, currently deployed on Ethereum. It converts real-world assets into ERC-20 tokens and provides access to decentralized lending protocols. Tinlake charges a 4% service fee on the total supply in each lending pool.

Second is the Centrifuge P2P messaging protocol, which allows collaborators to securely and privately create, exchange, and verify asset data, and tokenize assets into NFTs.

Third is the Centrifuge Chain, developed on the Substrate framework, which shares the security of the Polkadot network and has been bridged to Ethereum. Currently, asset issuers primarily tokenize real assets on the Centrifuge Chain.

The Centrifuge Chain also has its native token, CFG, used to incentivize network and ecosystem development, as well as community governance. CFG can also be bridged to Ethereum and used as an ERC-20 token.

CFG is mainly used to pay transaction fees on the Centrifuge Chain, incentivize node maintenance for network security, and stake CFG to qualify for financing and participate in governance, among other uses. Although the Tinlake protocol is currently mainly on the Ethereum chain rather than the Centrifuge Chain, the use cases and value capture potential for CFG are limited. However, with the significant growth in active loans backed by MakerDAO on the Ethereum chain this year, the token's performance has also improved. According to data from CMC, the current price of CFG is $0.54, which is more than three times higher than the approximately $0.15 at the beginning of the year, but still significantly lower than the record of over $2 during the bull market in 2021.

In terms of CFG's use cases, in March 2022, Centrifuge announced plans to launch and expand real-world asset pools on the Centrifuge Chain, replacing the Tinlake protocol on Ethereum, to expand the use cases for CFG, including fee and staking mechanisms. However, the migration of the Tinlake protocol has not been completed yet.

As the demand for RWAs in the crypto space grows, Centrifuge has also updated some products and expanded its business this year, aiming to become RWA infrastructure. The Tinlake lending application announced a new round of upgrades in May, with improvements in user interface and KYC experience, as well as integration with multiple public chains and wallets. Additionally, in July, a credit lending group was established, consisting of experts in the financial and lending fields, to review and assess the risks of Centrifuge's lending pools.

Furthermore, in June 2022, Centrifuge announced the launch of Centrifuge Prime, a product focused on providing a full set of legal framework and on-chain asset tokenization services for DAOs and DeFi protocols to bridge real-world assets. In August, Aave passed a proposal to collaborate with Centrifuge Prime to invest in US bonds.

However, despite gaining favor from leading DeFi protocols such as MakerDAO and Aave, Centrifuge, like the former Maple and TrueFi on-chain protocols, has not been able to avoid defaults and bad debts. This year, Centrifuge has experienced consecutive defaults, with over $15.5 million in outstanding loans. In August, the community also mentioned that an impending default loan would pose a risk of loss to MakerDAO's $1.84 million investment. The MakerDAO community even proposed to stop providing loans to tokenized credit pools on Centrifuge.

Compared to on-chain risks, the off-chain review, assessment, and liquidation of asset issuers/borrowers may pose a significant challenge. In the traditional credit field of finance, past P2P lending has brought significant harm to many investors and even the financial industry. As it attempts to lower the financing threshold for small and medium-sized enterprises and organizations in the real world, how on-chain credit protocols can avoid being exploited by malicious actors and establish investor protection mechanisms through legal and technical means may be a long and challenging road.

免责声明:本文章仅代表作者个人观点,不代表本平台的立场和观点。本文章仅供信息分享,不构成对任何人的任何投资建议。用户与作者之间的任何争议,与本平台无关。如网页中刊载的文章或图片涉及侵权,请提供相关的权利证明和身份证明发送邮件到support@aicoin.com,本平台相关工作人员将会进行核查。